RSS Feed

RSS Feed by Calculated Risk on 6/30/2010 09:55:00 PM

Wednesday, June 30, 2010

Fannie Mae: Serious Delinquency rate declines in April

Click on graph for larger image in new window.

Click on graph for larger image in new window.

Fannie Mae reported today that the rate of serious delinquencies - at least 90 days behind - for conventional loans in its single-family guarantee business decreased to 5.30% in April, down from 5.47% in March - and up from 3.42% in April 2009.

"Includes seriously delinquent conventional single-family loans as a percent of the total number of conventional single-family loans."

This is similar to the report from Freddie Mac (although Fannie Mae releases data one month later). Just as for Freddie Mac, some of the earlier rapid increase was probably because of foreclosure moratoriums, and distortions from modification programs because loans in trial mods were considered delinquent until the modifications were made permanent.

More modifications have become permanent (and no longer counted as delinquent) and Fannie Mae is foreclosing again (they have a record number of REOs) - so there has been a slight decline in the delinquency rate.

Lawler: Residential Listings in June

by Calculated Risk on 6/30/2010 05:47:00 PM

CR Note: How the NAR calculates existing home inventory is a bit of a mystery. Housing economist Tom Lawler has been tracking inventory several different ways. The following post is from Tom Lawler:

This morning there were 3,973,439 residential listings on realtor.com, up 1.6% from late May and up 0.3% from a year ago. Listings in California, which declined sharply during 2009, were up 2.3% on the month and up 7.4% from a year ago. States with especially large monthly increases in listings including Washington (14.5%, after an 8.4% drop in May – Washington data are whacky!), Alaska (5.1%), Maine (4.9%), and Colorado (4.3%). Florida listings were up 0.3% on the month but down 9.5% from a year ago. Click on graph for larger image in new window.

Click on graph for larger image in new window.

I’m not sure how often realtor.com listings by states are “refreshed,” or whether the updates are identical across states. However, the realtor.com data appear to “synch up” better to reports from various MLS than do the monthly National Association of Realtor data – which often displays monthly swings completely out of whack with the various “inventory trackers” that I and others follow. The NAR wasn’t willing to give me details of its methodology, but it apparently uses the sample data from various realtor associations/boards/MLS, and it may estimate the national totals with gross-ups based on “months’ supply.” Whatever the case, the monthly NAR numbers appear to have “spurious volatility” unrelated to actual swings in listings.

CR Note: This seems to suggest an increase in inventory in June. Using Realtor.com isn't perfect, but it is a consistent and transparent method.

Market Update

by Calculated Risk on 6/30/2010 04:06:00 PM

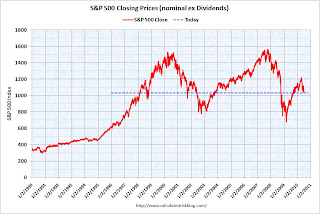

The end of Q2 ... Click on graph for larger image in new window.

Click on graph for larger image in new window.

The first graph shows the S&P 500 since 1990 (this excludes dividends).

The dashed line is the closing price today. The S&P 500 was first at this level in February 1998; over 12 years ago.

Click on graph for interactive version in new window.

The graph has tabs to look at the different bear markets - "now" shows the current market - and there is also a tab for the "four bears".

Fed's Lockhart: Sustainable final demand not yet supporting growth

by Calculated Risk on 6/30/2010 01:39:00 PM

From Atlanta Fed President Dennis Lockhart: Recovery and the Challenge of Uncertainty

The central question is whether the recovery that is now well under way will be sustained or will falter, resulting in a slowdown or even a second recession—the so-called double dip.

...

Rising consumer activity surprised many in the first quarter of the year, but in April and May consumers seemed to put away their wallets to a certain extent. ... Business spending on equipment and software has been strong in the first half of the year. ... Manufacturing production is up about 8 percent over the past year through May.

...

Here's a key point about these contributors to recovery—each could be transitory. The economy has not yet arrived at a state where healthy and sustainable final demand is underpinning growth.

... I believe the recovery will move ahead at a modest pace and unemployment will gradually come down. Impediments to growth are being removed. Financial market function is being restored. Private balance sheets are being repaired. And necessary structural adjustments are under way.

The past few weeks, however, have seen a slight retrenchment from the mind-set of optimism and growing confidence that prevailed earlier in the year.

...

Several recent sources of uncertainty have clouded the outlook. I will cite four, including the oil spill in the Gulf.

First is European sovereign debt. ... Our financial system here in the United States has rather small and manageable direct exposure to the Greek government and the other sovereign borrowers. But as the situation has evolved, exposure to European banks as well as foreign and local corporations in the affected countries has complicated the estimation of risk.

...

A second source of uncertainty is ongoing state and local fiscal tightening.

...

A third area of uncertainty is commercial real estate. Banks across the country, especially small and regional banks, are heavily exposed to the commercial property sector and face a heavy docket of loan restructurings that may require sizable write-downs.

...

And there is the oil spill, which is, naturally, the central environmental and economic concern here in Louisiana and more broadly in the Gulf region. ...

The economic effect at the national level has been limited. I'm prepared to believe, however, that this relentless environmental disaster is an additional factor holding back consumer and business confidence. The spill disheartens us all and, I believe, makes the public a little more reticent to assume a smooth recovery path.

...

So, to pull this together, a recovery of the national economy is proceeding but not yet with solid and sustainable underpinnings. Inflation appears restrained. The outlook from here is beset by somewhat more than normal uncertainty.

Restaurant Index "Softened" in May

by Calculated Risk on 6/30/2010 11:57:00 AM

This is one of several industry specific indexes I track each month.  Click on graph for larger image in new window.

Click on graph for larger image in new window.

For the second consecutive month, same store sales and customer traffic both declined in May (year-over-year).

This has taken a toll on the positive outlook in the "expectations index" and the overall index showed contraction in May.

Unfortunately the data for this index only goes back to 2002.

Note: Any reading above 100 shows expansion for this index.

From the National Restaurant Association (NRA): Restaurant Industry Outlook Softened in May as Restaurant Performance Index Fell Below 100

The outlook for the restaurant industry softened in May, as the National Restaurant Association’s comprehensive index of restaurant activity fell below 100 for the first time in three months. The Association’s Restaurant Performance Index (RPI) – a monthly composite index that tracks the health of and outlook for the U.S. restaurant industry – stood at 99.7 in May, down 0.7 percent from April’s level of 100.4.Restaurants are a discretionary expense, and they tend to be 'first in, last out' of a recession for consumer spending (as opposed to housing that is usually first in and first out). Since restaurants both lead and lag recessions, this contraction could be because of the sluggish recovery or might suggest further weakness in consumer spending in the months ahead.

...

Restaurant operators reported a net decline in same-store sales for the second consecutive month in May.

...

Restaurant operators also reported softer customer traffic results in May.

...

Although sales and traffic results softened in May, restaurant operators reported an uptick in capital spending activity.

...

Although restaurant operators remain optimistic about sales growth in the months ahead, their optimism slipped somewhat in recent months.

emphasis added

Chicago PMI shows expansion in June

by Calculated Risk on 6/30/2010 09:45:00 AM

From the Institute for Supply Management – Chicago:

The Chicago Purchasing Managers reported the CHICAGO BUSINESS BAROMETER indicated the breadth of expansion showed little change, and chalked up a ninth month of growth.The overall index declined to 59.1 from 59.7 (just below expectations). Note: any number above 50 shows expansion.

Employment improved to 54.2 after showing a decline (below 50) in May.

The new orders index declined again to 59.1 from 62.7. This is the lowest level this year.

The national ISM manufacturing index will be released tomorrow.

ADP: Private Employment increased 13,000 in June

by Calculated Risk on 6/30/2010 08:15:00 AM

ADP reports:

Nonfarm private employment increased 13,000 from May to June 2010 on a seasonally adjusted basis, according to the ADP National Employment Report®. The estimated change in employment from April to May 2010 was revised up slightly, from the previously reported increase of 55,000 to an increase of 57,000.Note: ADP is private nonfarm employment only (no government jobs).

June’s rise in private employment was the fifth consecutive monthly gain. However, over these five months the increases have averaged a modest 34,000. Recent ADP Report data suggest that, following steady improvement through April, private employment may have decelerated heading into the summer.

This is below the consensus forecast of ADP showing an increase of 60,000 private sector jobs in June.

The BLS reports on Friday, and the consensus is for a decrease of 100,000 payroll jobs in June, on a seasonally adjusted (SA) basis, with the loss of around 250,000 temporary Census 2010 jobs (+150,000 ex-Census).

MBA: Mortgage Refinance Applications increase, Purchase Applications near 13 Year Low

by Calculated Risk on 6/30/2010 07:18:00 AM

The MBA reports: Mortgage Refinance Applications Increase as Rates Continue to Drop in Latest MBA Weekly Survey

The Refinance Index increased 12.6 percent from the previous week and is the highest Refinance Index observed in the survey since the week ending May 22, 2009. The seasonally adjusted Purchase Index decreased 3.3 percent from one week earlier.

...

“Amid continuing financial market volatility, mortgage rates dropped again last week, with rates on 15-year loans reaching a record low for the MBA survey. Refinance applications jumped in response, but remain at about half the level seen in the spring of 2009,” said Michael Fratantoni, MBA’s Vice President of Research and Economics. “Purchase applications declined for the seventh time in the last eight weeks, keeping the purchase index near 13-year lows.”

...

The average contract interest rate for 30-year fixed-rate mortgages decreased to 4.67 percent from 4.75 percent, with points decreasing to 0.96 from 1.07 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans. This is the lowest 30-year contract rate recorded in the survey since the week ending April 24, 2009.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the MBA Purchase Index and four week moving average since 1990.

The purchase index has collapsed following the expiration of the tax credit suggesting home sales will fall sharply too. This is the lowest level for 4-week average of the purchase index since 1996.

Tuesday, June 29, 2010

Shanghai Composite at lowest level since April 2009

by Calculated Risk on 6/29/2010 10:57:00 PM

Just an update ... Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the Shanghai SSE Composite Index and the S&P 500 (in blue).

The SSE Composite Index is at 2,384 - down almost 2% and off almost 25% since early April.

This is the lowest level since April 2009.

House Passes Homebuyer Tax Credit Closing Extension

by Calculated Risk on 6/29/2010 07:03:00 PM

From Reuters: U.S. House backs homebuyer tax credit extension

This is bad policy ... and the Senate will probably pass it tomorrow.

2nd Half: Slowdown or Double-Dip?

by Calculated Risk on 6/29/2010 04:00:00 PM

No one has a crystal ball, but it appears the U.S. economy will slow in the 2nd half of 2010.

For the unemployed and marginally employed, and for many other Americans suffering with too much debt or stagnant real incomes, there is little difference between slower growth and a double-dip recession. What matters to them is jobs and income growth.

In both cases (slowdown or double-dip), the unemployment rate will probably increase and wages will be under pressure. It is just a matter of degrees.

The arguments for a slowdown and double-dip recession are basically the same: less stimulus spending, state and local government cutbacks, more household saving impacting consumption, another downturn in housing, and a slowdown and financial issues in Europe and a slowdown in China. It is only a question of magnitude of the impact.

My general view has been that the recovery would be sluggish and choppy and I think this slowdown is part of the expected "choppiness". I still think the U.S. will avoid a technical "double-dip" recession.

Usually the deeper the recession, the more robust the recovery. That didn't happen this time (no "V-shaped" recovery), and it is probably worth reviewing why this period is different than an ordinary recession-recovery cycle.

An examination of the aftermath of severe financial crises shows deep and lasting effects on asset prices, output and employment. ... Even recessions sparked by financial crises do eventually end, albeit almost invariably accompanied by massive increases in government debt.

Click on graph for larger image in new window.

Click on graph for larger image in new window. The graph from Rudebusch's shows a modified Taylor rule. According to Rudebusch's estimate, the Fed Funds rate should be around minus 5% right now if we ignore unconventional policy (obviously there is a lower bound) and probably close to minus 3% if we include unconventional policy. Obviously the Fed can't lower rates using conventional policy, although it is possible for more unconventional policy.

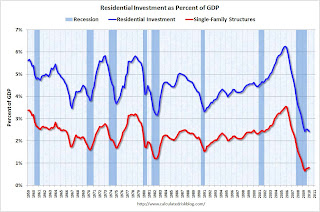

On this third point, I put together a table of housing supply metrics last weekend to help track the housing market. It is hard to have a robust economic recovery without a recovery in residential investment - and there will be no strong recovery in residential investment until the excess housing supply is reduced substantially.

During previous recoveries, housing played a critical role in job creation and consumer spending. But not this time. Residential investment is mostly moving sideways.

This graph shows residential investment (RI) and investment in single family structures as a percent of GDP. RI is mostly investment in single family structures, home improvement, multi-family structures and commissions on sale of existing structures.

This graph shows residential investment (RI) and investment in single family structures as a percent of GDP. RI is mostly investment in single family structures, home improvement, multi-family structures and commissions on sale of existing structures.It isn't the size of the sector (currently only about 2.5% of GDP), but the contribution during the recovery that matters - and housing is usually the largest contributor to economic growth and employment early in a recovery.

Two somewhat positive points: 1) builders will deliver a record low number of housing units in 2010, and that will help reduce the excess supply (see: Housing Stock and Flow), and 2) usually a recession (or double-dip) is preceded by a sharp decline in Residential Investment (housing is the best leading indicator for the business cycle), and it hard for RI to fall much further!

So I'm sticking with a slowdown in growth.

And a market update from Doug Short of dshort.com (financial planner).

And a market update from Doug Short of dshort.com (financial planner).Click on graph for interactive version in new window.

The graph has tabs to look at the different bear markets - "now" shows the current market - and there is also a tab for the "four bears".

State and Local Tax Revenue increased slightly compared to Q1 2009

by Calculated Risk on 6/29/2010 12:05:00 PM

The Census Bureau reported this morning that state and local tax revenues grew 0.8% in the first quarter 2010 compared to Q1 2009. This was the second straight quarter of growth compared to the same quarter of the previous year.

Individual income tax increased 2.7% compared to Q1 2009.

General sales tax revenues increased 0.3%.

Corporate income tax declined 5.4%.

Property taxes declined 0.6% (the first year-over-same quarter decline since 2003).  Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows state and local tax revenue on a rolling 4 quarter basis (this removes seasonality).

The three main sources of revenue are property taxes, sales taxes and personal income taxes. Property taxes tend to be the most stable, even with the sharp drop in real estate prices.

Most of the decline in revenue during the recession came from sharp declines in personal income and sales taxes.

Consumer Confidence Plummets in June

by Calculated Risk on 6/29/2010 10:03:00 AM

From the Conference Board: Consumer Confidence Index® Drops Sharply

The Conference Board Consumer Confidence Index® which had been on the rise for three consecutive months, declined sharply in June. The Index now stands at 52.9 (1985=100), down from 62.7 in May.I rarely mention consumer confidence because it is mostly a coincident indicator, but this is quite a miss (expectations were for about the same level as May).

...

Says Lynn Franco, Director of The Conference Board Consumer Research Center: “Consumer confidence, which had posted three consecutive monthly gains and appeared to be gaining some traction, retreated sharply in June. Increasing uncertainty and apprehension about the future state of the economy and labor market, no doubt a result of the recent slowdown in job growth, are the primary reasons for the sharp reversal in confidence. Until the pace of job growth picks up, consumer confidence is not likely to pick up.”

Case-Shiller: House Prices increased in April due to tax credit

by Calculated Risk on 6/29/2010 09:00:00 AM

IMPORTANT: These graphs are Seasonally Adjusted (SA). S&P has cautioned that the seasonal adjustment is probably being distorted by irregular factors. These distortions could include distressed sales and the various government programs.

S&P/Case-Shiller released the monthly Home Price Indices for April (actually a 3 month average).

This includes prices for 20 individual cities, and two composite indices (10 cities and 20 cities).

From S&P: While Most Markets Improved in April 2010, Home Prices Do Not Yet Show Signs of Sustained Recovery According to the S&P/Case-Shiller Home Price Indices

Data through April 2010, released today by Standard & Poor’s for its S&P/Case-Shiller1 Home Price Indices, the leading measure of U.S. home prices, show that annual growth rates of all 20 MSAs and the 10- and 20-City Composites improved in April compared to March 2010. The 10-City Composite is up 4.6% from where it was in April 2009, and the 20-City Composite is up 3.8% versus the same time last year. In addition, 18 of the 20 MSAs and both Composites saw improvement in prices as measured by April versus March monthly changes.

“Home price levels remain close to the April 2009 lows set by the S&P/Case Shiller 10- and 20-City Composite series. The April 2010 data for all 20 MSAs and the two Composites do show some improvement with higher annual increases than in March’s report. However, many of the gains are modest and somewhat concentrated in California. Moreover, nine of the 20 cities reached new lows at some time since the beginning of this year. The month-over-month figures were driven by the end of the Federal first-time home buyer tax credit program on April 30th. Eighteen cities saw month-to-month gains in April compared to six in the previous month. Miami and New York were the two that fared the worst in April compared to March. New York is the only MSA to have posted a new relative index low with April’s report.” says David M. Blitzer, Chairman of the Index Committee at Standard & Poor’s.

“Other housing data confirm the large impact, and likely near-future pullback, of the federal program. Recently released data for May 2010 show sharp declines in existing and new home sales and housing starts. Inventory data and foreclosure activity have not shown any signs of improvement. Consistent and sustained boosts to economic growth from housing may have to wait to next year. ”

Click on graph for larger image in new window.

Click on graph for larger image in new window. The first graph shows the nominal not seasonally adjusted Composite 10 and Composite 20 indices (the Composite 20 was started in January 2000).

The Composite 10 index is off 29.7% from the peak, and up 0.3% in April (SA).

The Composite 20 index is off 29.0% from the peak, and up 0.4% in April (SA).

The second graph shows the Year over year change in both indices.

The second graph shows the Year over year change in both indices.The Composite 10 is up 4.6% compared to April 2009.

The Composite 20 is up 3.8% compared to April 2009.

This is the third month with YoY price increases in a row.

The third graph shows the price declines from the peak for each city included in S&P/Case-Shiller indices.

Prices increased (SA) in 17 of the 20 Case-Shiller cities in April (SA).

Prices increased (SA) in 17 of the 20 Case-Shiller cities in April (SA). Prices in Las Vegas are off 55.9% from the peak, and prices in Dallas only off 5.2% from the peak.

Case Shiller is reporting on the NSA data (18 cities up), and I'm using the SA data. As S&P noted, there probably was a small boost to prices from tax credit related buying, but prices will probably fall later this year.

Monday, June 28, 2010

Ireland: Austerity in Action

by Calculated Risk on 6/28/2010 10:41:00 PM

From Liz Alderman in the New York Times: In Ireland, a Picture of the High Cost of Austerity

As Europe’s major economies focus on belt-tightening, they are following the path of Ireland. But the once thriving nation is struggling, with no sign of a rapid turnaround in sight.As the Irish government cut the budget, the economy contracted faster and the deficit as a percent of GDP increased.

...

Rather than being rewarded for its actions, though, Ireland is being penalized. ... Lacking stimulus money, the Irish economy shrank 7.1 percent last year and remains in recession.

Joblessness in this country of 4.5 million is above 13 percent, and the ranks of the long-term unemployed — those out of work for a year or more — have more than doubled, to 5.3 percent.

...

The budget went from surpluses in 2006 and 2007 to a staggering deficit of 14.3 percent of gross domestic product last year — worse than Greece. It continues to deteriorate.

And how will they break the downward cycle? Export to England and America ...

[T]he government is pinning nearly all its hopes on an export revival to lift the economy. Falling wage and energy costs, and a weaker euro, have improved competitiveness.This approach works for one country - or a few - but not if every country is doing it.

Fed Econ Letter: State budget crisis poses "modest risk to national recovery"

by Calculated Risk on 6/28/2010 07:24:00 PM

From Jeremy Gerst and Daniel Wilson at the SF Fed: Fiscal Crises of the States: Causes and Consequences. Here is their conclusion:

The current fiscal crises that most states are facing are generally the result of a severe macroeconomic downturn combined with a limited ability of the states to respond to such shocks. States are facing increased demand for public services at the same time revenue is falling. Federal stimulus support for state budgets is winding down over the next two years. Rainy-day funds are all but exhausted. Thus, state fiscal crises aren’t likely to go away soon and will probably get worse before they get better. The solutions states employ to close projected budget gaps will have painful effects on state residents and businesses but pose a more modest risk to the national recovery. Historically, the health of the national economy determines the health of state finances, not the other way around. Sustained improvement in the national economy is essential for states to grow their way out of their current problems and improve their fiscal conditions.Although the authors didn't quantify the impact, Mark Zandi, chief economist at Moody’s Analytics, recently estimated that state and local cutbacks may cut 0.25% from U.S. GDP in 2010 and 2011.

But this is just one drag on the economy. I've been forecasting a 2nd half slowdown in GDP growth based on:

1) less Federal stimulus spending in the 2nd half of 2010. The decline in stimulus will probably be a drag of about 0.5% on GDP growth by Q4.

2) the end of the inventory correction. The inventory adjustment contributed 3.79 percentage points in Q4 2009 of the 5.6% annualized growth rate, and 1.88 percentage points of the 2.7% GDP growth (annualized) in Q1 2010. This will probably fall close to zero in the 2nd half (maybe even slightly negative).

3) more household saving leading to slower growth in personal consumption expenditures. The personal saving rate increased to 4.0% in May, and will probably rise further in the 2nd half.

4) another downturn in housing (lower prices, less residential investment). This might subtract 0.25 to 0.5 percentage points from growth in the 2nd half.

5) slowdown and financial issues in Europe and a slowdown in China,

6) and the cutbacks at the state and local level. According the Mark Zandi, this will subtract about 0.25% from GDP growth.

As I've noted before, a quarter point here, and half point there ... and pretty soon you have some real drag.

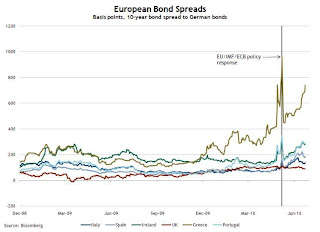

Misc: Greece Spreads Widen, Spanish Liquidity issues, Market Update

by Calculated Risk on 6/28/2010 04:00:00 PM

The 10-year Greece-to-German bond spread has widened to over 800 bps today. This is the highest level since the the EU / ECB policy response when the spread peaked at just under 1000 bps.

And from the Financial Times: Banks in Spain hit by end of ECB offer

Spanish banks have been lobbying the European Central Bank to act to ease the systemic fallout from the expiry of a €442bn ($542bn) funding programme this week ... On Thursday, the clock runs out ... One senior bank executive said: “Any central bank has to have the obligation to supply liquidity. But this is not the policy of the ECB. We are fighting them every day on this. It’s absurd.”This liquidity facility was put in place during the financial crisis. The ECB is offering one week and three month liquidity facilities, so there won't be any short term liquidity crisis - but there are concerns that his could lead to less lending in Spain.

excerpted with permission

And a market update from Doug Short of dshort.com (financial planner).Click on graph for interactive version in new window.

The graph has tabs to look at the different bear markets - "now" shows the current market - and there is also a tab for the "four bears".

Fed's Warsh: Reluctant to do more

by Calculated Risk on 6/28/2010 12:48:00 PM

From Fed Governor Kevin Warsh: It's Greek to Me

In my view, any judgment to expand the balance sheet further should be subject to strict scrutiny. I would want to be convinced that the incremental macroeconomic benefits outweighed any costs owing to erosion of market functioning, perceptions of monetizing indebtedness, crowding-out of private buyers, or loss of central bank credibility. The Fed's institutional credibility is its most valuable asset, far more consequential to macroeconomic performance than its holdings of long-term Treasury securities or agency securities. That credibility could be meaningfully undermined if we were to take actions that were unlikely to yield clear and significant benefits."Perceptions of monetizing indebtedness"? Although this "perception" is widespread on the internet, it isn't showing up in the bond market.

Indeed, the Federal Reserve should continue to give careful consideration to the appropriate size and composition of its existing holdings. Actual sales will not take place in the near term. But, depending on the evolution of the economy and financial markets, we should consider a gradual, prospective exit--communicated well-in-advance--from our portfolio of mortgage-backed securities. In making this judgment, we should continue to assess investor demand for these assets. Ultimately, in my view, gradual, predictable asset sales by the Fed should facilitate improvements in mortgage finance and financial markets.

Any sale of assets need not signal that policy rates are soon moving higher. Our policy tools can indeed be used independently. I would note that the Fed successfully communicated and demonstrated its ability to exit from most of its extraordinary liquidity facilities over late 2009 and early 2010, even as it continued its policy of extraordinary accommodation.

I definitely agree with Warsh on this point:

"Subprime mortgages were not at the core of the global crisis; they were only indicative of the dramatic mispricing of virtually every asset everywhere in the world."Tanta said it better a few years ago: "We're all subprime now!"

Chicago Fed: Economic Activity increased in May

by Calculated Risk on 6/28/2010 10:00:00 AM

Note: This is a composite index based on a number of economic releases.

From the Chicago Fed: Index shows economic activity continued to expand in May

The index’s three-month moving average, CFNAI-MA3, rose to its highest level since March 2006, increasing to +0.28 in May from +0.05 in April. May’s CFNAI-MA3 suggests that growth in national economic activity was above its historical trend. Moving above +0.20, the index’s three-month moving average in May also reached a level historically associated with a mature economic recovery following a recession.

Click on table for larger image in new window.

Click on table for larger image in new window.This graph shows the Chicago Fed National Activity Index (three month moving average) since 1967. According to the Chicago Fed:

A zero value for the index indicates that the national economy is expanding at its historical trend rate of growth; negative values indicate below-average growth; and positive values indicate above-average growth.This is the highest level in the index since March 2006, and indicates growth slightly above trend.

Personal Income up 0.4%, Spending Increases 0.2% in May

by Calculated Risk on 6/28/2010 08:30:00 AM

From the BEA: Personal Income and Outlays, April 2010

Personal income increased $53.7 billion, or 0.4 percent ... Personal consumption expenditures (PCE) increased $24.4 billion, or 0.2 percent.The following graph shows real Personal Consumption Expenditures (PCE) through May (2005 dollars). Note that the y-axis doesn't start at zero to better show the change.

...

Real PCE -- PCE adjusted to remove price changes -- increased 0.3 percent in May, in contrast to a decrease of less than 0.1 percent in April

...

Personal saving as a percentage of disposable personal income was 4.0 percent in May, compared with 3.8 percent in April.

Click on graph for large image.

Click on graph for large image.The quarterly change in PCE is based on the change from the average in one quarter, compared to the average of the preceding quarter.

Even with no growth in June, PCE growth in Q2 would be

The National Bureau of Economic Research (NBER) uses several measures to determine if the economy is in recession. One of the measures is real personal income less transfer payments (see NBER memo). This increased in May to $9,113.9 billion (SAAR) and is barely above the low of October 2009 ($8,987 billion).

This graph shows real personal income less transfer payments since 1969.

This graph shows real personal income less transfer payments since 1969.This measure of economic activity is moving sideways - similar to what happened following the 2001 recession.

This month income increased faster than spending ... meaning the saving rate increased.

This graph shows the saving rate starting in 1959 (using a three month trailing average for smoothing) through the May Personal Income report. The saving rate increased to 4.0% in April (increased to 3.7% using a three month average).

This graph shows the saving rate starting in 1959 (using a three month trailing average for smoothing) through the May Personal Income report. The saving rate increased to 4.0% in April (increased to 3.7% using a three month average). I still expect the saving rate to rise over the next couple of years slowing the growth in PCE.

The increase in income was good news, but personal income less transfer payments are still only 1.4% above the low of last year.

Sunday, June 27, 2010

Krugman: "The Third Depression"

by Calculated Risk on 6/27/2010 11:59:00 PM

From Paul Krugman in the NY Times: The Third Depression

Recessions are common; depressions are rare. As far as I can tell, there were only two eras in economic history that were widely described as “depressions” at the time: the years of deflation and instability that followed the Panic of 1873 and the years of mass unemployment that followed the financial crisis of 1929-31.From CR: I'm not as pessimistic as Professor Krugman, but I do think with almost double digit unemployment, the focus of policymakers should be jobs, jobs, jobs ...

...

We are now, I fear, in the early stages of a third depression. It will probably look more like the Long Depression than the much more severe Great Depression. But the cost — to the world economy and, above all, to the millions of lives blighted by the absence of jobs — will nonetheless be immense.

Housing Supply Metrics

by Calculated Risk on 6/27/2010 08:13:00 PM

Here is a table of various housing supply measures (just putting this in one place with links to the source data).

Note: here is the Weekly Summary and a Look Ahead. It will be a busy week!

| Total delinquent loans1 | 7.3 million |

| Seriously delinquent loans1,2 | 5.0 million |

| Total REO Inventory3 | 0.5 million |

| Fannie, Freddie, FHA REO4 | 210 thousand |

| Homeowners with Negative Equity5 | 11.2 million |

| Homeowner vacancy rate6 | 2.6% |

| Rental vacancy rate6 | 10.6% |

| Excess Vacant Units6,7 | 1.7 million |

| Existing Home Inventory8 | 3.89 million |

| Existing Home Months of Supply8 | 8.3 months |

| New Home Inventory9 | 213 thousand |

| New Home Months of Supply9 | 8.5 months |

1 Source: estimate based on the Mortgage Bankers Association’s (MBA) Q1 2010 National Delinquency Survey. "MBA’s National Delinquency Survey covers about 44.4 million first lien mortgages on one-to four-unit residential properties ... The NDS is estimated to cover around 85 percent of the outstanding first-lien mortgages in the country."

2 This is based on the MBA's estimate of loans 90+ days delinquent or in the foreclosure process.

3 Source: Radarlogic and Barclays as of Feb 2010.

4 Source: Fannie Mae, Freddie Mac and FHA. Fannie, Freddie, FHA REO Inventory Surges 22% in Q1 2010

5 Source: CoreLogic Q1 2010 Negative Equity Report

6 Source: Census Bureau Residential Vacancies and Homeownership in the First Quarter 2010

7 CR calculation.

8 Source: National Association of Realtors

9 Source: Census Bureau New Residential sales

Housing Bust in the Exurbs

by Calculated Risk on 6/27/2010 04:45:00 PM

From Thomas Curwen in the LA Times: Undone by their dreams

In 2005:

Amid the imposing two-story designs, they settled on a modest single-story home — yet with 2,400 square feet, it was large enough for their growing family. The sales representatives told them ... if they put down a $3,000 deposit they could lock in the price at $365,000.And the result in 2009:

They could barely scrape together the deposit, and they didn't have a down payment for the mortgage. The sales representatives didn't seem worried. ... Countrywide Financial Corp. turned them down. [they had filed bankruptcy 4 years earlier] Freedom Plus Mortgage said yes.

...

Every weekday morning at 6:30, the family would get into the minivan and head over the Cajon Pass. The commute was a little more than an hour.

They spoke to the bank but were told that they didn't qualify for a loan modification ... In October, the house was sold for $125,000.The buyers could "barely scrape together" a 1% deposit, they could hardly qualify (even Countrywide turned them down!), their commute to work was more than an hour each way ... the 2,400 sq ft tract house could probably be built for under $150K today on land that is very cheap ...

Update: I've upped the cost estimate. This is very low end construction (the only "upgrade" was a microwave). Perhaps my original estimate was too low (based on info from a builder), but I've heard some very low quotes recently. This could still be low.

This was an interesting story of boom and bust, but the ending was very predictable.

Weekly Summary and a Look Ahead

by Calculated Risk on 6/27/2010 11:40:00 AM

The key economic report this week will be the June Employment Report to be released on Friday. It will be a busy week ...

On Monday, the BEA will release the May Personal Income and Outlays report. The consensus is for a 0.5% increase in income, and a 0.2% increase in spending. Also on Monday, the May Chicago Fed National Activity Index will be released at 8:30 AM. This is a composite index of other data.

On Tuesday, the April Case-Shiller house price index will be released at 9:00 AM. The consensus is for a slight decline in the house price index. At 10:00 AM, the Conference Board will release Consumer Confidence for June (consensus is for about the same as in May or 63.3).

On Wednesday, the ADP employment report will be released (consensus is for an increase of 60K private sector jobs, up from 55K in May). Also on Wednesday, the Chicago Purchasing Managers Index for June will be released. Consensus is for the PMI to be about the same as May, or 59.7.

Also on Wednesday, Altanta Fed President will speak to the Rotary Club of Baton Rouge at 1 PM ET on the economic outlook.

On Thursday, the closely watched initial weekly unemployment claims will be released. Consensus is for a decline to 450K from 457K last week. The automakers will report vehicle sales for June. Expectations are for about a 11.4 million SAAR for light vehicles in June – down slightly from the 11.6 million rate in May. Some forecasts are even lower, from Edmunds:

Edmunds.com forecasts June's Seasonally Adjusted Annualized Rate (SAAR) will be 11.2 million, down from 11.6 million in May, which was a weak month.Also on Thursday, at 10 AM, the ISM Manufacturing index for June will be released (expectations are for a decrease to 59.0 from 59.7 in May) and Construction Spending for April (consensus is for a slight decline in spending).

Also on Thursday, the NAR will release May Pending Home sales at 10 AM. The consensus is for a decline of around 15%. Take the under! Economist Tom Lawler writes:

[M]y “best guess” estimate is that pending sales in May will be down about 35% from April.And on Friday, the BLS will release the June Employment report at 8:30 AM. The consensus is for a loss of 100K payroll jobs in June, and for the unemployment rate to increase slightly to 9.8% (from 9.7%). Of course the minus 100K includes a substantial decline in the number of temporary hires for Census 2010 (May was the peak month). It will be important to remove the Census hiring to try to determine the underlying trend. Consensus is around a gain of 150K payroll jobs ex-Census. (see Employment Report Preview for more).

Also on Friday, the American Bankruptcy Institute will probably report personal bankruptcy filings for June. This will probably show another "surge" in filings.

And Friday afternoon will be another BFF (Bank Failure Friday) ...

And a summary of last week:

The Census Bureau reported that New Home Sales in May were at a seasonally adjusted annual rate (SAAR) of 300 thousand.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows New Home Sales vs. recessions for the last 45 years.

Sales of new single-family houses in May 2010 were at a seasonally adjusted annual rate of 300,000 ... This is 32.7 percent (±9.9%) below the revised April rate of 446,000 and is 18.3 percent (±13.0%) below the May 2009 estimate of 367,000.The 300 thousand annual sales rate is a new all time record low. The previous record low annual sales rate was 338 thousand in September 1981.

This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1993.

This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1993. Sales in May 2010 (5.66 million SAAR) were 2.2% lower than last month, and were 19.2% higher than May 2009 (4.75 million SAAR).

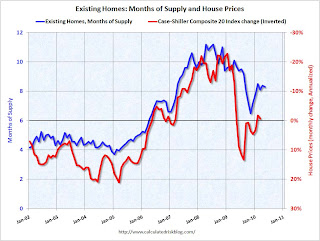

The next graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Inventory is not seasonally adjusted, so it is helpful to look at the YoY change.

Inventory increased 1.1% YoY in May. This is the second consecutive month of a year-over-year increases in inventory. Although the YoY increase is small, I expect it will be higher later this year.

Inventory increased 1.1% YoY in May. This is the second consecutive month of a year-over-year increases in inventory. Although the YoY increase is small, I expect it will be higher later this year.This increase in inventory is especially concerning because the reported inventory is already historically very high, and the 8.3 months of supply in May is well above normal. The months of supply will probably stay near this level in June, because of more tax credit related sales (reported at closing), but the months-of-supply could be close to double digits later this year.

And a double digit months-of-supply would be a really bad sign for house prices ...

This graph show months of supply and the annualized change in the Case-Shiller Composite 20 house price index (inverted).

This graph show months of supply and the annualized change in the Case-Shiller Composite 20 house price index (inverted).Below 6 months of supply (blue line) house prices are typically rising (red line, inverted).

Above 6 months of supply house prices are usually falling (although there were many programs to support house prices over the last year).

Later this year the months of supply will probably increase, and I expect house prices to fall further as measured by the Case-Shiller and CoreLogic repeat sales house price indexes.

The American Institute of Architects’ Architecture Billings Index declined to 45.8 in May from 48.5 in April. Any reading below 50 indicates contraction.

The American Institute of Architects’ Architecture Billings Index declined to 45.8 in May from 48.5 in April. Any reading below 50 indicates contraction.According to the AIA, there is an "approximate nine to twelve month lag time between architecture billings and construction spending" on non-residential construction. So there will probably be further declines in CRE investment through all of 2010, and probably well into 2011.

Best wishes to all.

G-20 poised to issue Statement

by Calculated Risk on 6/27/2010 09:08:00 AM

From Alan Beattie at the Financial Times in 2008 (via Bruce Bartlett):

An ineffectual international organisation yesterday issued a stark warning about a situation it has absolutely no power to change, the latest in a series of self-serving interventions by toothless intergovernmental bodies.And on a more serious note, from Bloomberg: G-20 May Stress Need to Cut Deficits as Leaders Split on Urgency of Target

“We are seriously concerned about this most serious outbreak of seriousness,” said the head of the institution ...

Group of 20 leaders are poised to endorse targets to tackle deficits while giving nations flexibility on when to start balancing their books, according to officials with knowledge of drafts of the final statement.From the NY Times: Leaders at Summit Talks Turn Attention to Deficit Cuts

...

The draft of the statement includes targets championed by Canadian Prime Minister Stephen Harper for countries to halve deficits by 2013 and start to stabilize their debt-to-output ratios by 2016, the officials said.

Despite President Obama’s pitch at the summit meeting for developed nations here for continued stimulus measures to prevent another global economic downturn, the United States will go along with other leaders who are more concerned about rising debt and join in a commitment to cut their governments’ deficits in half by 2013, administration officials said on Saturday.

Saturday, June 26, 2010

Freddie Mac: 90+ Day Delinquency Rate steady in May

by Calculated Risk on 6/26/2010 09:51:00 PM

Click on graph for larger image in new window.

Click on graph for larger image in new window.

Freddie Mac reported yesterday that the rate of serious delinquencies - at least 90 days behind - for conventional loans in its single-family guarantee business was steady at 4.06% in May, the same rate as April, and up sharply from 2.73% in May 2009.

"Single-family delinquencies are based on the number of mortgages 90 days or more delinquent or in foreclosure as of period end ..."

The "good" news is the delinquency rate has stopped rising rapidly. However some of the earlier increase was because of foreclosure mortatoriums, and distortions from modification programs - loans in trial mods were considered delinquent until the modifications were made permanent.

Even though Freddie Mac has started foreclosing, modifying loans, and accepting short sales, the number of new 90+ day delinquencies has kept pace.

The data from Fannie Mae will be released next week ...

Employment Report Preview

by Calculated Risk on 6/26/2010 06:26:00 PM

Just a few notes on the June employment report to be released on Friday, July 2nd:

Andrew Tilton of Goldman Sachs noted this in a research note yesterday:

"We are cautiously optimistic that June’s payroll report will show a pickup in private-sector payroll growth to around 150,000. In part, this is because there seems to be some “crowding out” of private sector payroll growth by short-term Census hiring—indeed, this may explain a good part of the payroll disappointment last month. Total payrolls should be down about 100,000 in June as a large portion of Census employment rolls off."There will be some preliminary reports on employment released during the coming week: the ADP employment report, the Chicago PMI, and the ISM surveys.

However it is concerning that the regional Fed manufacturing surveys were mixed on employment (manufacturing has been one of the stronger sectors):

In addition weekly initial unemployment claims have remained elevated. Initial weekly claims have averaged 464,000 thousand in June, almost the same level as each of the previous 5 months.

Here is a repeat of the graph showing percent job losses during recessions, aligned at the bottom:

Click on graph for larger image.

Click on graph for larger image.This graph shows the job losses from the start of the employment recession, in percentage terms.

The dotted line shows the impact of Census hiring. In May, there were 564,000 temporary 2010 Census workers on the payroll. Just under half of those Census jobs will go away in June, and the two red lines will meet sometime later this year.

Second Liens and Personal Bankruptcy

by Calculated Risk on 6/26/2010 12:31:00 PM

From Mary Ellen Podmolik at the Chicago Tribune: Moral bankruptcy?

[Filing bankruptcy] may seem an extreme riff on the difficult decisions homeowners make to unburden themselves of debt owed on properties that have lost substantial value. Lawyers and housing counselors say, however, that personal bankruptcy filings are becoming more commonplace as debt-holders seek sums due them, particularly on second "piggyback" mortgages used to buy homes.I suspect eliminating debt from 2nd liens is one of the reasons there has been a surge in personal bankruptcy filings this year. The deep recession and high unemployment rate are probably the main reasons.

"It's a big trend," said Dan Lindsey, a supervisory attorney at the Legal Assistance Foundation of Metropolitan Chicago. "Banks are having a hard enough time dealing with the first mortgages. The second (mortgages), there's no equity there to collect so they're being charged off and sold to debt buyers and rearing their ugly heads later. It's a drastic last resort to file Chapter 7, but in some cases it's appropriate."

...

"My other option was to say I'll roll the dice with the bank," [former homeowner Del] Phillips said. "Will they really come after me? I wouldn't put it past the bank industry to do that. It's going to kill me to pay a bank for a house I no longer owned. I was, like, there's no way I'm going to pay the bank another dime."

Unofficial Problem Bank List increases to 797 Institutions

by Calculated Risk on 6/26/2010 09:16:00 AM

Note: this is an unofficial list of Problem Banks compiled only from public sources.

Here is the unofficial problem bank list for June 25, 2010.

Changes and comments from surferdude808:

CR provided a tease earlier on some of changes to the Unofficial Problem Bank List that would be happening as the FDIC released its enforcement actions for May yesterday. As CR predicted, it was a busy week as 24 institutions were added while 8 were removed. Also, the agencies issued numerous Prompt Corrective Action Orders.

Overall, the Unofficial Problem Bank List stands at 797 institutions with aggregate assets of $409.6 billion, up from 781 institutions with assets of $404.5 billion last week. Removals include the failed Peninsula Bank ($644 million), First National Bank ($253 million), and High Desert State Bank ($83 million). The FDIC terminated actions against De Witt State Bank ($39 million), Citizens State Bank of Lankin ($37 million), BankHaven ($22 million), and The Farmers Bank ($18 million). The other removal was for VisionBank of Iowa ($87 million) which merged with its affiliate sister bank -- Ames Community Bank ($383 million) that also happens to be on the Unofficial Problem Bank List as it is operating under a Written Agreement.

There were 24 institutions with aggregate assets of $6.5 billion added to the list this week. Notable additions include Bank of Choice, Greeley, CO ($1.3 billion); Nova Bank, Berwyn, PA ($598 million); CornerstoneBank, Atlanta, GA ($536 million); and Sterling Federal Bank, F.S.B., Sterling, IL ($501 million). Geographically, five institutions from Georgia, three from Missouri, and two from California, Colorado, Illinois, and Pennsylvania were added.

In a sign that the agencies may be taking their regulatory authority seriously, they issued 11 Prompt Corrective Action Orders against institutions on the Unofficial Problem Bank List. Generally, a PCA Order is a narrow enforcement action proscribing for an institution to raise its regulatory capital ratios by a certain date. As way of background, in 1991 via the Federal Deposit Insurance Corporation Improvement Act (FDICIA) Congress mandated for the regulators to take certain actions including closing troubled institutions promptly. The intent was to prevent a recurrence of the "zombie thrifts" that regulators allowed to stay open for many years despite being insolvent, which contributed the large price tag of the last banking crisis. The PCA legislation requires regulators to take certain actions that are triggered by so-called capital trip wires. For example, regulators are supposed to stop an institution from issuing brokered deposits or giving managers golden parachutes when they are no longer "well capitalized." Another trip wire requires for regulators to close an institution when its tangible capital ratio breeches 2 percent. The thinking behind this provision is that closure before equity goes negative would lessen losses to the deposit insurance fund and the potential that taxpayer monies would be needed to support resolutions. Some industry observers believe the regulators have been remiss in enforcing PCA, particularly the timely closing of insolvent institutions. To support this conclusion, observers point to Corus Bank and Guaranty Bank that posted negative equity in their Call Reports several quarters before they were closed or the substantial loss rates on failed institutions that reported satisfactory capital ratios just before failure.

The 11 institutions receiving a PCA Order include LibertyBank ($768 million); Butte Community Bank ($523 million Ticker: CVLL); Metro Bank of Dade County ($442 million); Ravenswood Bank ($301 million); SouthwestUSA Bank ($214 million); Blue Ridge Savings Bank, Inc. ($209 million); Legacy Bank ($169 million); Olde Cypress Community Bank ($169 million); Shoreline Bank ($110 million); Badger State Bank ($93 million); and Thunder Bank ($33 million).

Friday, June 25, 2010

Year of the Short Sale, and Deed in lieu

by Calculated Risk on 6/25/2010 09:45:00 PM

From Kenneth Harney in the WaPo: Foreclosure alternative gaining favor (ht ghostfaceinvestah)

There are two programs in Home Affordable Foreclosure Alternatives (HAFA), short sales and deed in lieu of foreclosure.

Harney writes:

Some of the largest mortgage servicers and lenders in the country are gearing up campaigns to reach out to carefully targeted borrowers with cash incentives that sometimes range into five figures, plus a simple message: Let's bypass the time-consuming hassles of short sales and foreclosures. Just deed us the title to your underwater home, and we'll call it a deal. ...The deal can be quick, and the first lender will agree not to pursue a deficiency judgment. However 2nds are a problem, and "deed in lieu" transactions still hit the borrower's credit history.

Borrowers with 2nds considering a "deed in lieu" transaction should contact the 2nd lien holders. HAFA offers a payout to 2nd lien holders in deed in lieu transactions who agree to release borrowers from debt (see point 4 here for payouts under deed in lieu).

Under the HAFA deed in lieu program, the borrower needs to be proactive with 2nd lien holders.

The deed in lieu program is gaining in popularity, from Harney:

Bank of America, has mailed 100,000 deed-in-lieu solicitations to customers in the past 60 days, and its volume of completed transactions is breaking company records, according to officials. ... To sweeten the pot, Bank of America is offering cash incentives that range from $3,000 to $15,000 ... [Matt Vernon, Bank of America's top short sale and deed-in-lieu executive] said.On the credit impact, from Carolyn Said at the San Francisco Chronicle:

[Craig Watts, a spokesman for FICO] said it is a "widespread myth" that short sales and deeds in lieu of foreclosure have less impact on credit scores than do foreclosures.And a video from HAMP / HAFA: "Your Graceful Exit"

"Generally speaking, when you can't pay your mortgage, in the eyes of the FICO score what matters is that you were not able to fill your obligation as you originally agreed and that failure is highly predictive of future risk," he said.

Bank Failure #86: High Desert State Bank, Albuquerque, New Mexico

by Calculated Risk on 6/25/2010 07:04:00 PM

Road running deposits flee

Wiley banker struck

by Soylent Green is People

From the FDIC: First American Bank, Artesia, New Mexico, Assumes All of the Deposits of High Desert State Bank, Albuquerque, New Mexico

As of March 31, 2010, High Desert State Bank had approximately $80.3 million in total assets and $81.0 million in total deposits. ...That makes three today ...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $20.9 million. ... High Desert State Bank is the 86th FDIC-insured institution to fail in the nation this year, and the second in New Mexico. The last FDIC-insured institution closed in the state was Charter Bank, Santa Fe, on January 22, 2010.

Bank Failures #84 & #85: Florida and Georgia

by Calculated Risk on 6/25/2010 06:24:00 PM

Ringed on three sides by water

Way out blocked by Feds

Savannah shut down

Sheila's Summer season starts

Sad situation.

by Soylent Green is People

From the FDIC: Premier American Bank, Miami, Florida, Assumes All of the Deposits of Peninsula Bank, Englewood, Florida

As of March 31, 2010, Peninsula Bank had approximately $644.3 million in total assets and $580.1 million in total deposits. ...From the FDIC: The Savannah Bank, National Association, Savannah, Georgia, Assumes All of the Deposits of First National Bank Savannah, Georgia

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $194.8 million. Compared to other alternatives, ... Peninsula Bank is the 84th FDIC-insured institution to fail in the nation this year, and the fourteenth in Florida. The last FDIC-insured institution closed in the state was Bank of Florida – Southwest, Naples, on May 28, 2010.

As of March 31, 2010, First National Bank had approximately $252.5 million in total assets and $231.9 million in total deposits. ...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $68.9 million. Compared to other alternatives, ... First National Bank is the 85th FDIC-insured institution to fail in the nation this year, and the ninth in Georgia. The last FDIC-insured institution closed in the state was Satilla Community Bank, Saint Marys, on May 14, 2010.

FDIC: May Enforcement Actions

by Calculated Risk on 6/25/2010 04:45:00 PM

Just a BFF (Bank Failure Friday) preview. It looks like surferdude808 will be busy updating the Unofficial Problem Bank list today ... the FDIC released their May Enforcement Actions.

There are eight Prompt Corrective Actions (PCA) for last month ... and that seems especially high.

ATA Truck Tonnage Index declines in May

by Calculated Risk on 6/25/2010 12:59:00 PM

From the American Trucking Association: ATA Truck Tonnage Index Fell 0.6 Percent in May

The American Trucking Associations’ advance seasonally adjusted (SA) For-Hire Truck Tonnage Index decreased 0.6 percent in May, which was the first month-to-month drop since February of this year. This followed an upwardly revised 1 percent increase in April. The latest reduction put the SA index at 109.6 (2000=100).

...

Compared with May 2009, SA tonnage increased 7.2 percent, which was the sixth consecutive year-over-year gain. In April, the year-over-year increase was 9.5 percent. Year-to-date, tonnage is up 6.2 percent compared with the same period in 2009.

ATA Chief Economist Bob Costello said that truck freight tonnage is going to have ups and downs, but the trend continues in the right direction. “Despite the month-to-month drop in May, the trend line is still solid. There is no way that freight can increase every month, and we should expect periodic decreases. This doesn’t take away from the fact that freight volumes are quite good, especially considering the reduction in truck supply over the last couple of years.”

This graph from the ATA shows the Truck Tonnage Index since Jan 2006 (no larger image).

This graph from the ATA shows the Truck Tonnage Index since Jan 2006 (no larger image). This index has only shown a gradual increase since December.

Rail traffic was also soft in May.

KB Home: "Month of May was particularly challenging" for housing industry

by Calculated Risk on 6/25/2010 11:33:00 AM

On the conference call this morning, Jeffrey Mezger, president and chief executive officer of KB Home said the month of May was "particularly challenging" for the housing industry.

Paraphrasing ..

Q&A just started ...

On the current quarter (ended May 31st) from MarketWatch: KB Home shares fall on 'disappointing' results

Q1 GDP revised down to 2.7%

by Calculated Risk on 6/25/2010 08:32:00 AM

The Q1 real GDP rate was revised down again (third estimate) to 2.7% from the 2nd estimate of 3.0%.

Consumer spending was weaker in Q1 than originally estimated. PCE growth (personal consumption expenditures) was revised down to 3.0% in Q1 from the previous estimate of 3.5%.

Some more from Reuters: Economy Grew Slower in First Quarter than Expected, Up 2.7%

... business spending, which only rose at a 2.2 percent rate instead of 3.1 percent as reported last month. This was as a spending on structures was revised down to show a slightly bigger decline than reported last month. Growth in software and equipment investment was also lowered to a 11.4 percent rate from 12.7 percent.The "Change in private inventories" was revised up to a contribution of 1.88 percentage points from the previous estimate of 1.65. So inventory adjustment accounted for over two-thirds of the GDP growth in Q1 - and the inventory adjustment appears over. This is a weak third estimate.

...

Another drag on growth came from exports whose growth was eclipsed by a rise in imports, resulting in a trade deficit that subtracted from GDP.

... real final sales to domestic purchasers, considered a better measure of domestic demand, rose at a 1.6 percent rate instead of the 2.0 percent pace reported last month.

Thursday, June 24, 2010

Late Night Reading

by Calculated Risk on 6/24/2010 11:59:00 PM

Just a couple of depressing articles ...

From Paul Krugman in the NY Times: The Renminbi Runaround

As of Thursday, the currency was only about half a percent higher than its typical level before the announcement. And all indications are that watching the future movement of the renminbi will be like watching paint dry: Chinese officials are still making statements denying that a rise in their currency will do anything to reduce trade imbalances, and prices in the forward market, in which traders agree to exchange currencies at various points in the future, suggest a rise of only about 2 percent in the renminbi by the end of this year. This is basically a joke.From Michael Pettis: What might history tell us about the Greek crisis?

Update: Unemployment Benefits, Housing Tax Credit

by Calculated Risk on 6/24/2010 07:32:00 PM

From Lori Montgomery at the WaPo: Senate again rejects emergency spending package

The Senate on Thursday rejected a package of tax cuts, state aid and emergency jobless benefits ... [try again] after the July 4 recess. By then, more than 2 million people will have seen their unemployment benefits cut off, according to the U.S. Department of Labor.What this means is that anyone receiving extended unemployment benefits (there are several tiers) will not be eligible for the next tier when their unemployment benefits expire.

This bill also contains the extension of the closing date for the homebuyer tax credit. As of right now, homebuyers must close by June 30th to receive the tax credit.

But of course the housing industry wants even more. From Zach Fox at SNL Financial: Analysts: Record low new-home sales could lead to another tax credit

Even though he is not in favor of another tax credit, [Michael Widner, an analyst with Stifel Nicolaus & Co.] said May's exceptionally low number means plenty of industry insiders will push for one.Hopefully there will not be another housing tax credit. And hopefully the change in eligibility date for extended unemployment benefits will be approved.

"On the one hand, I know that the phones are ringing off the hook in D.C. right now for people clamoring for a new tax credit," Widner said. "So the shock value of an all-time low is going to be a lot of people saying: 'Oh my God, we gotta do more to stimulate housing.' ... And on the other hand, you're going to get people, who frankly I side with more, saying: 'You know, look, obviously the tax credit did nothing but pull demand forward, and in the wake of the tax credit you see the void left behind.'"

Misc: Quote of the Day, Greece Bond Spreads increase Sharply, and Market Update

by Calculated Risk on 6/24/2010 04:00:00 PM

Here is a graph from the Atlanta Fed weekly Financial Highlights released today (graph as of June 23rd): Click on graph for larger image in new window.

Click on graph for larger image in new window.

From the Atlanta Fed:

Greek bond spreads (over German bonds) have risen recently, near the highs seen before the European policy package was announced in early May.Note: The Atlanta Fed data is one day old. Nemo has links to the current data on the sidebar of his site.

Other euro zone countries’ bond spreads are also elevated during the same period.

Since tightening in early May, the 10-year Greece-to-German bond spread has risen to nearly 300 basis points (bps) (from 4.38% to 7.39%) through June 22. Other European peripherals’ spreads are elevated, with Portugal up 138 bps over the period, Ireland up 111 bps, and Spain 86 bps higher.

The spreads have widened further today: Greece is up sharply to 781 bps today.

And a market update from Doug Short of dshort.com (financial planner).Click on graph for interactive version in new window.

The graph has tabs to look at the different bear markets - "now" shows the current market - and there is also a tab for the "four bears".

And here is the quote of the day from BofA (via Bloomberg, ht Bill):

"Given the depth of the nation’s recessionary impacts on homeowners, a considerable number of customers will transition from homeownership over the next two years.""Transition from homeownership ..." Ouch.

Barbara Desoer, president of Bank of America’s home-loan and insurance unit, said in testimony prepared for a congressional hearing June 24, 2010

Lennar: June Home Sales off 20% to 25% from 2009

by Calculated Risk on 6/24/2010 02:43:00 PM

From Bloomberg: Lennar Home Sales Down as Much as 25% in June as Tax Credit Ends, CEO Says (ht Brian)

Lennar Corp.’s home sales are down 20 percent to 25 percent this month compared with a year earlier ... Chief Executive Officer Stuart Miller said.In June 2009, new home sales were at a 396K seasonally adjusted annual rate. This is just one home builder, but a 20% to 25% decline would put sales in June at about the record low level of May. This is almost certain to the worst June sales rate since the Census Bureau started keeping records in 1963.

“The entire market knew there’d be a slowdown as we came off the tax credit,” Miller said on a conference call with investors today. “It’s just that the reality of it doesn’t feel good.”

Hotel Occupancy Rate increases

by Calculated Risk on 6/24/2010 01:12:00 PM

From HotelNewsNow.com: STR: US results for week ending 19 June

In year-over-year measurements, the industry’s occupancy last week increased 5.8 percent to 66.7 percent. Average daily rate rose 1.1 percent to US$98.03—the third time in four weeks that the measurement has risen. Revenue per available room rose 7.0 percent to US$65.36.The following graph shows the four week moving average for the occupancy rate by week for 2008, 2009 and 2010 (and a median for 2000 through 2007).

Click on graph for larger image in new window.

Click on graph for larger image in new window.Notes: the scale doesn't start at zero to better show the change.

On a 4-week basis, occupancy is up 8.1% compared to last year (the worst year since the Great Depression) and still almost 7% below normal. About half way back!

Last year leisure travel (summer) held up better than business travel, now it appears business travel is recovering - and we will soon see if leisure travel will also pick up this year.

Data Source: Smith Travel Research, Courtesy of HotelNewsNow.com