RSS Feed

RSS Feed by Calculated Risk on 3/31/2011 08:11:00 PM

Thursday, March 31, 2011

Restaurant Performance Index increases in February

Earlier:

• Kansas City Manufacturing Survey at Record High, Chicago PMI Strong in March

• Employment Situation Preview: More Jobs, but still Grim

This is one of several industry specific indexes I track each month.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

The index increased to 100.7 in February indicating expansion.

Unfortunately the data for this index only goes back to 2002.

From the National Restaurant Association: Restaurant Industry Outlook Improved in February as Restaurant Performance Index Stood Above 100 for the Fifth Time in Six Months

The National Restaurant Association’s Restaurant Performance Index (RPI) – a monthly composite index that tracks the health of and outlook for the U.S. restaurant industry – stood at 100.7 in February, up 0.4 percent from its January level. In addition, February represented the fifth time in the last six months that the RPI stood above 100, which signifies expansion in the index of key industry indicators.Increased traffic and sales, and a positive outlook for capital spending and hiring ... a solid report. Also, February was a record high sales month for the restaurant industry.

“February’s RPI gain was driven by solid improvements in the same-store sales and customer traffic indicators,” said Hudson Riehle, senior vice president of the Research and Knowledge Group for the Association. “Restaurant operators reported positive same-store sales and customer traffic results in February, after January’s results were dampened by extreme weather conditions in many parts of the country.”

“In addition to improving sales and traffic indicators, restaurant operators’ outlook for capital spending hit a 40-month high, while their expectations for staffing growth rose to the highest level in nearly four years,” Riehle added.

...

Restaurant operators reported a solid improvement in same-store sales in February. ... Restaurant operators also reported a net increase in customer traffic levels in February.

...

Bolstered by an improving sales outlook, restaurant operators’ plans for capital spending rose to its highest level in 40 months. ... For the fifth consecutive month, restaurant operators reported a positive outlook for staffing gains in the months ahead.

Irish Bank Stress Tests and European Bond Spreads

by Calculated Risk on 3/31/2011 05:18:00 PM

On the Irish banks from the Irish Times: Irish banks require an extra €24 billion recapitalisation

Ireland’s beleaguered banking sector is to be recapitalised by a further €24 billion and restructured around two core retail banks ... This is the fifth attempt to recapitalise the banks and brings the total cost of bailing out the sector from €46 billion to €70 billion.Here is a look at European bond spreads from the Atlanta Fed weekly Financial Highlights released today (graph as of March 30th):

...

[Minister for Finance Michael Noonan] indicated the Government would seek "significant contributions" from subordinated bondholders in the banks to contribute to the cost of recapitalising the sector.

Mr Noonan also signalled the Government was no longer considering the imposition of losses on senior bondholders in Bank of Ireland and Allied Irish Banks. However, he said the Government but would re-examine the possibility of imposing losses on senior bondholders at Anglo Irish Bank, if that lender required additional capital.

Click on graph for larger image in new window.

Click on graph for larger image in new window.From the Atlanta Fed:

Most peripheral European bond spreads (over German bonds) continue to be elevated, particularly those of Greece, Ireland, and Portugal, with the latter two countries seeing their financial situations worsening.Here are the Ten Year yields for Ireland, Portugal, Greece, and Germany. The spreads to Germany widened more today with Greece up to 948 bps, Ireland up to 687 bps, and Portugal up to 505 bps. The good news is the spreads have been declining for the other European countries.

Since the March FOMC meeting, the 10-year Greece-to-German bond spread has declined by 38 basis points (bps), through March 29. Also, the Spanish spread has declined by 17 bps.

However, the spread for Ireland and Portugal has risen by 49 bps and 44 bps, respectively.

Employment Situation Preview: More Jobs, but still Grim

by Calculated Risk on 3/31/2011 02:36:00 PM

Tomorrow the BLS will release the March Employment Situation Summary at 8:30 AM ET. The consensus is for an increase of 195,000 payroll jobs in March, and for the unemployment rate to hold steady at 8.9%.

• The weak payroll report in January was blamed on the weather (only 63,000 jobs added after revision). So there might have been some bounce back in February (192,000 payroll jobs added). The two month average was 127,500 payroll jobs added (145,000 private). Anything less in March would be very disappointing.

• The BLS reference period is the calendar week that contains the 12th day of the month (or pay period including the 12th for the establishment survey). There were several significant world events in March, especially in Japan (the earthquake was on March 11th) and Libya. Sometimes hiring can be delayed due to world events, but based on the timing, I don't think there will be any impact on the March report.

• Usually the ISM manufacturing and service reports are released before the BLS employment report. Not this month because the first Friday of the month is on the 1st (Happy April Fools' Day!). However all of the regional Fed manufacturing surveys and the Chicago PMI indicated strong expansion in March.

• Weekly initial unemployment claims averaged 394,250 in March, about the same as in February (392,500). That is the good news (fewer layoffs), but so far hiring hasn't picked up.

• Weekly initial unemployment claims averaged 394,250 in March, about the same as in February (392,500). That is the good news (fewer layoffs), but so far hiring hasn't picked up.

Click on graph for larger image in graph gallery.

• ADP reported Private Employment increased by 201,000 from February to March on a seasonally adjusted basis, and has averaged 211,000 over the last four months.

And some less optimistic news:

• Consumer Sentiment decreased sharply in March. This is frequently coincident with improvements in the labor market - but also strongly related to gasoline prices (Gasoline was probably the reason for the decline in March).

• Consumer Sentiment decreased sharply in March. This is frequently coincident with improvements in the labor market - but also strongly related to gasoline prices (Gasoline was probably the reason for the decline in March).

The final March Reuters / University of Michigan consumer sentiment index declined to 67.5 from the preliminary March reading of 68.2 - and down from 77.5 in February. This is the lowest level since November 2009.

• And on unemployment: Gallup Finds U.S. Unemployment Rate at 10.0% in March NOTE: The Gallup poll results are Not Seasonally Adjusted (NSA), so use with caution. But this does suggest a seasonally adjusted unemployment rate slightly higher than the 8.9% in February.

• Even if the payroll report shows improvement, the employment situation remains grim. There are 7.4 million fewer payroll jobs now than before the recession started in 2007 with 13.7 million Americans currently unemployed. Another 8.3 million are working part time for economic reasons, and about 4 million more workers have left the labor force. Of those unemployed, 6 million have been unemployed for six months or more.

If the BLS reports 200 thousand payroll jobs added tomorrow - that will be welcome - but it is just a small step in the right direction. Many of the unemployed and marginally employed will not see any improvement for some time.

My guess is in the 150,000 to 175,000 range for payroll jobs, with the unemployment rate increasing slightly.

Kansas City Manufacturing Survey at Record High, Chicago PMI Strong in March

by Calculated Risk on 3/31/2011 11:00:00 AM

• Note: The Irish bank stress test results will be released at 4:30 PM local time (11:30 AM ET). The Irish Times has a live blog discussing the results.

• From the Kansas City Fed: Survey of Tenth District Manufacturing

Growth in Tenth District manufacturing activity accelerated rapidly in March, posting a record high for the second straight month. Expectations moderated slightly from last month, but still remained solid. Price indexes for raw materials reached historically high levels, and more firms indicated plans to pass cost increases on to customers.This is the last of the regional Fed surveys for January. The regional surveys provide a hint about the ISM manufacturing index, as the following graph shows.

The month-over-month composite index was 27 in March, up from 19 in February and 7 in January. This reading set a new all time survey high. ... The employment index inched higher from 23 to 25, also a new survey record.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.The New York and Philly Fed surveys are averaged together (dashed green, through March), and averaged five Fed surveys (blue, through March) including New York, Philly, Richmond, Dallas and Kansas City. The Institute for Supply Management (ISM) PMI (red) is through February (right axis).

The regional surveys suggest the ISM manufacturing index will in the 60+ range (strong expansion). The ISM index for March will be released tomorrow, April 1st. The consensus is for a decrease to 61.2 from 61.4 in February.

And from earlier this morning ...

• From the Chicago Business Barometer™ Decelerated: The overall index decreased to 70.6 from 71.2 in February. This was slightly above consensus expectations of 70.0. Note: any number above 50 shows expansion, so this is a strong reading.

"EMPLOYMENT grew to its second-highest level since February 1973." The employment index increased sharply to 65.6 from 59.8. This is the highest level since December 1983.

"NEW ORDERS increased to the highest point since December 1983". The new orders index decreased to 74.5 from 75.9.

Prices were up sharply, but over all this was a strong report.

Ireland: Stress Test Results to be released at 11:30 AM ET

by Calculated Risk on 3/31/2011 10:16:00 AM

Weekly Initial Unemployment Claims at 388,000

by Calculated Risk on 3/31/2011 08:30:00 AM

The DOL reports on weekly unemployment insurance claims:

In the week ending March 26, the advance figure for seasonally adjusted initial claims was 388,000, a decrease of 6,000 from the previous week's revised figure of 394,000. The 4-week moving average was 394,250, a increase of 3,250 from the previous week's revised average of 391,000.

Click on graph for larger image in graph gallery.This graph shows the 4-week moving average of weekly claims for the last 40 years. The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased this week to 394,250.

The number of weekly claims for last week was revised up - so this was reported as a decline. But what really matters is this is the 5th consecutive week with the 4-week average below the 400,000 level. There is nothing magical about 400,000, but this is a small positive step for the labor market.

Wednesday, March 30, 2011

Irish Finance Minister: Bank stress test results of "major significance"

by Calculated Risk on 3/30/2011 10:37:00 PM

The Irish bank stress test results will be released tomorrow.

From the Irish Times: Noonan to propose 'radical' bank sector restructuring

... The results of the tests will lead [Finance Minister] Michael Noonan to undertake “a radical new approach” to fix the banks, a Government source said.Here are the Irish yields from Bloomberg for 2 year and 10 year bonds.

Mr Noonan will make a “watershed” argument for a EU-wide solution around passing bank losses on to bondholders ... The Minister will speak for 20 minutes in the Dáil immediately after the announcement of the test results by the Central Bank.

Mr Noonan told Fine Gael TDs and Senators at the party’s parliamentary party meeting last night that the test results would be of major significance and would dominate the news over the weekend.

...

ECB chief Jean-Claude Trichet chaired a teleconference meeting of the bank’s governing council from China yesterday to discuss the situation in the Irish banks. A further meeting may be held today as the ECB finalises its response.

Earlier:

• CoreLogic: Shadow Inventory Declines Slightly

• Lawler: The “Shrill Cry” from Lobbyists on QRM

Fannie Mae and Freddie Mac Delinquency Rates decline slightly

by Calculated Risk on 3/30/2011 07:46:00 PM

Fannie Mae reported that the serious delinquency rate decreased to 4.45% in January from 4.48% in December. This is down from 5.52% a year ago.

Freddie Mac reported that the serious delinquency rate decreased to 3.78% in February from 3.82% in January. (Note: Fannie reports a month behind Freddie). This is down from a record high 4.20% in February 2010.

These are loans that are "three monthly payments or more past due or in foreclosure".

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

Some of the rapid increase in 2009 was probably because of foreclosure moratoriums, and also because loans in trial mods were considered delinquent until the modifications were made permanent. As modifications have become permanent, they are no longer counted as delinquent.

The slowdown in the rate of decline in the 2nd half of last year was probably related to the new foreclosure moratoriums.

Earlier:

• CoreLogic: Shadow Inventory Declines Slightly

• Lawler: The “Shrill Cry” from Lobbyists on QRM

Lawler: The “Shrill Cry” from Lobbyists on QRM

by Calculated Risk on 3/30/2011 04:11:00 PM

Earlier on Shadow Inventory:

• CoreLogic: Shadow Inventory Declines Slightly

In the following long post, housing economist Tom Lawler clears up some misunderstandings and misinformation regarding the new proposed mortgage rules: The “Shrill Cry” from Lobbyists on QRM

Yesterday the Office of the Comptroller of the Currency, Treasury (OCC); Board of Governors of the Federal Reserve System (Board); Federal Deposit Insurance Corporation (FDIC); U.S. Securities and Exchange Commission (Commission); Federal Housing Finance Agency (FHFA); and Department of Housing and Urban Development (HUD) jointly issued their proposed rule on “credit risk retention” for assets collateralizing asset-backed securities pursuant to the Dodd-Frank Act, and the proposed rule included a proposed definition of a “qualified residential mortgage (QRM)” For ABS backed by QRMs, the DFA provides for an exemption of the risk-retention rule. For folks who don’t remember, the “inclusion” of an exemption for QRMs was in the act because of heavy lobbying by financial institutions and housing-related trade groups, and it put regulators in the uncomfortable position of trying to decide what types of mortgages were so inherently “low risk” that they should/could be excluded from the rule designed to ensure that ABS issuers had “skin in the game.”

Regulators yesterday proposed defining “QRM” much more restrictively than the lobbyists who had successfully gotten the concept of a “QRM” into the legislation, including a LTV restriction of 80% (and no piggybacks), front/back end DTIs of 28% and 36%, respectively, and other “borrower credit history” restrictions. Industry lobbyists quickly commented negatively.

A comment on Regional Fed Talk

by Calculated Risk on 3/30/2011 02:18:00 PM

Much has been made about recent comments by St Louis Fed President James Bullard and Philly Fed President Charles Plosser. Kansas City Fed president Thomas Hoenig added his voice today: Fed should head for the exit, Hoenig says

A few comments:

• When Plosser gave his EXIT speech last week, he started by saying: "As always, and perhaps particularly so today, the views I express are my own and do not necessarily represent those of the Federal Reserve System or my colleagues on the Federal Open Market Committee." Notice that he emphasized these are his views.

• Tim Duy wrote today: Fed Watch: Running the Fed Like an Economics Department

It seems to me that the Fed lacks a coherent communication strategy – there is no willingness on the part of the leadership to enforce talking points. As a consequence, there is enormous pointless chatter from Fed officials that might be interesting in some sense, but provide misleading guidance about policy direction. Recent talk about scaling back the size of the large scale asset program, for instance. Almost certainly not going to happen – so why talk about it? Sadly, it appears to be an almost deliberate effort to create uncertainty among market participants at a time when the opposite is so important.A key European analyst wrote to his clients today:

Professor Bernanke likes to allow his students to roam the campus and say what they think. This collegiate approach leads to vibrant debate, but debate that may have previously only occurred behind the closed doors of the FOMC.And that is the point: these comments are the opinions of a few regional presidents - some non-voting - and do not represent the views of the majority on the FOMC.

• The "big three", Fed Chairman Bernanke, Vice Chair Janet Yellen, and NY Fed President William Dudley will all speak over the next two weeks, starting with Dudley this Friday, Bernanke on April 4th, and Yellen on April 11th. I expect they will speak with one voice and stand behind the current QE2 policy stance and the "exceptionally low levels for the federal funds rate for an extended period" guidance. I also expect they will also argue that the increase in inflation is transitory.

Although I read all the regional Fed speeches, I'm not sure why some market participants have been paying closer attention to certain speeches. Perhaps they are unaware of Professor Bernanke's "collegiate approach"!

I believe the current policy will continue as planned.

CoreLogic: Shadow Inventory Declines Slightly

by Calculated Risk on 3/30/2011 10:25:00 AM

From CoreLogic: CoreLogic Reports Shadow Inventory Declines Slightly, However, Nine Months’ Worth of Supply Remains

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

This graph from CoreLogic shows the breakdown of "shadow inventory" by category. For this report, CoreLogic estimates the number of 90+ day delinquencies, foreclosures and REOs not currently listed for sale. Obviously if a house is listed for sale, it is already included in the "visible supply" and cannot be counted as shadow inventory.

CoreLogic estimates the "shadow inventory" (by this method) at about 1.8 million units.

CoreLogic ... reported today that the current residential shadow inventory as of January 2011 declined to 1.8 million units, representing a nine months’ supply. This is down slightly from 2.0 million units, also a nine

months’ supply, from a year ago.

CoreLogic estimates current shadow inventory, also known as pending supply, by calculating the number of distressed properties not currently listed on multiple listing services (MLS) that are seriously delinquent (90 days or more), in foreclosure and real estate owned (REO) by lenders. Transition rates of “delinquency to foreclosure” and “foreclosure to REO” are used to identify the currently distressed non-listed properties most likely to become REO properties. Properties that are not yet delinquent but may become delinquent in the future are not included in the estimate of the current shadow inventory. Shadow inventory is typically not included in the official metrics of unsold inventory.

...

Of the 1.8-million unit current shadow inventory supply, 870,000 units are seriously delinquent (4.2 months’ supply), 445,000 are in some stage of foreclosure (2.1 months’ supply) and 470,000 are already in REO (2.2 months’ supply).

The second graph shows the same information as "months-of-supply". This is in addition to the visible months-of-supply (inventory listed for sale). Note: It is the visible inventory that mostly impacts prices, but this suggests the visible inventory will stay elevated for some time (no surprise).

The second graph shows the same information as "months-of-supply". This is in addition to the visible months-of-supply (inventory listed for sale). Note: It is the visible inventory that mostly impacts prices, but this suggests the visible inventory will stay elevated for some time (no surprise).CoreLogic also notes:

In addition to the current shadow inventory supply, there are nearly 2 million current negative equity loans that are more than 50 percent “upside down” that will likely become shadow supply in the near future.This report provides a couple of key numbers: 1) there are 1.8 million homes seriously delinquent, in the foreclosure process or REO that are not currently listed for sale, and 2) there are about 2 million current negative equity loans that are more than 50 percent “upside down”.

ADP: Private Employment increased by 201,000 in March

by Calculated Risk on 3/30/2011 08:15:00 AM

ADP reports:

Private-sector employment increased by 201,000 from February to March on a seasonally adjusted basis, according to the latest ADP National Employment Report® released today. The estimated change of employment from January 2011 to February 2011 was revised down to 208,000 from the previously reported increase of 217,000.Note: ADP is private nonfarm employment only (no government jobs).

...

The average monthly increase in employment over the last four months – December through March – has been 211,000, consistent with a gradual if uneven decline in the unemployment rate. This is almost three times the average monthly gain of 74,000 over the preceding four months of August through November.

This was about at the consensus forecast of an increase of about 205,000 private sector jobs in March.

The BLS reports on Friday, and the consensus is for an increase of 195,000 payroll jobs in March, on a seasonally adjusted (SA) basis, and for the unemployment rate to hold steady at 8.9%.

MBA: Mortgage Purchase Application activity decreases slightly

by Calculated Risk on 3/30/2011 07:19:00 AM

The MBA reports: Mortgage Applications Decrease in Latest MBA Weekly Survey

The Refinance Index decreased 10.1 percent from the previous week. The seasonally adjusted Purchase Index decreased 1.7 percent from one week earlier.

...

"Treasury and mortgage rates increased towards the end of last week, as global markets calmed following the recent crises in Japan and the Middle East. Refinance volume predictably fell in response to these rate increases. As rates climb back to 5 percent, fewer homeowners have both the incentive and the ability to refinance," said Michael Fratantoni, MBA's Vice President of Research and Economics. "Purchase volume remained roughly flat as we enter what is typically the peak homebuying season."

...

The average contract interest rate for 30-year fixed-rate mortgages increased to 4.92 percent from 4.80 percent, with points decreasing to 0.83 from 0.96 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.This graph shows the MBA Purchase Index and four week moving average since 1990.

The four-week moving average of the purchase index is still moving sideways suggesting fairly weak home sales "as we enter what is typically the peak homebuying season". Note: There is a large percentage of cash buyers too.

Here come the downgrades for Q1 GDP Growth: Part II

by Calculated Risk on 3/30/2011 12:06:00 AM

Based on the February Personal Income and Outlays report, it is pretty clear that GDP growth in Q1 is going to be sluggish. We are going to see a number of downgrades, this once via David Leonhardt at the NY Times: As Economy Sputters, a Timid Fed (pay)

"a prominent research firm ... Macroeconomic Advisers, has downgraded its estimate of economic growth in the current quarter to a paltry 2.3 percent, from 4 percent."Leonhardt mostly discusses the Fed, QE2 and whether the Fed is properly balancing unemployment and inflation.

Earlier posts on Case-Shiller house prices:

• Case Shiller: Home Prices Off to a Dismal Start in 2011

• Real House Prices and Price-to-Rent

• House Price Graph Gallery

Tuesday, March 29, 2011

State and Local tax revenue increases in 2010

by Calculated Risk on 3/29/2011 08:34:00 PM

The Census Bureau released the State and Local tax revenue data for Q4 2010 today. Here is the page.

From Conor Dougherty at the WSJ: Tax Revenue Snaps Back

State and local tax revenue has nearly snapped back to the peak hit several years ago—a gain attributed to a reviving economy and tax increases implemented during the recession.Local governments are mostly funded by property taxes, and it usually takes some time for falling prices to show up in property taxes. Local property tax revenue is just starting to decline in the Census data.

But the improvement masks deeper problems for state and local governments that are likely to linger for years. To weather the recession, state governments relied on now-depleted federal stimulus funds ...

Total tax receipts for state and local governments hit $1.29 trillion in 2010, just 2.3% shy of the $1.32 trillion taken in during 2008, not adjusted for inflation, according to Census Bureau data.

State revenue is mostly from individual income taxes and sales taxes (see tables at the Census Bureau) and this revenue is still well below the pre-recession levels.

Even with improving revenue, there will be more state and local fiscal tightening this year - and that will remain a drag on economic growth.

Proposed New Mortgage Lending Rules

by Calculated Risk on 3/29/2011 03:56:00 PM

Earlier, several regulators released proposed new mortgage lending rules. Here is the press release from the Federal Reserve.

And here is the 233 page document.

Alan Ziebel at the WSJ has an overview: Regulators Unveil Mortgage-Lending Rules

The proposal ... is designed to encourage safer lending practices by mandating that issuers of mortgage-backed securities either follow conservative principles, such as requiring 20% down payments for mortgages, or hold a portion of the loans on their books. Companies that package loans into securities would have to hold at least 5% of the credit risk, unless the loans meet an exemption for high-quality loans.I've noted before that a 10% down payment with mortgage insurance seems reasonable. These front end and back end debt-to-income (DTI) guidelines used to be pretty standard.

... The proposal requests public comment on an alternative approach that would allow for a 10% down payment and mortgage insurance.

It also recommends that homeowners spend only 28% of their pretax income on their primary mortgage and 36% on total debt ...

It is important to note that more risky loans can still be made - but the lender has to hold some of the credit risk (a "skin in the game" incentive to adequately underwrite the loans).

Lenders are arguing for a little more flexibility to meet the qualified residential mortgage (QRM) exemption, from the MBA:

"While factors like downpayment, debt to income (DTI) ratio and past payment history can be accurate predictors of loan performance, we do not believe that each ought to be considered independently.My reaction is the rule is fine (I'd go with the 10% down payment and mortgage insurance). For the riskier loans, the lender can hold on to some credit risk (a great incentive to properly underwrite the loan).

"Rather, the rule should allow for consideration of a borrowers entire credit profile before determining whether risk retention is necessary on a given loan. For example, we believe that a lower downpayment loan could be less risky if a borrower has a strong history of making payments on time and if the borrower's debt to income ratio is on the lower end of the scale. The rule should provide more flexibility in this regard."

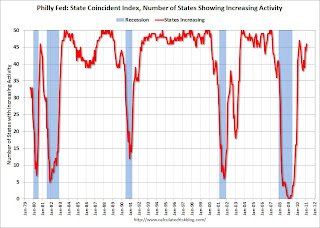

Philly Fed February State Coincident Indexes

by Calculated Risk on 3/29/2011 02:48:00 PM

Earlier posts on Case-Shiller house prices:

• Case Shiller: Home Prices Off to a Dismal Start in 2011

• Real House Prices and Price-to-Rent

• House Price Graph Gallery

Click on map for larger image.

Click on map for larger image.

The recovery may be sluggish, but it is fairly widespread geographically.

Here is a map of the three month change in the Philly Fed state coincident indicators. Forty six states are showing increasing three month activity. Four states are showing declining three month activity: Kansas, Delaware, New Jersey, and New Mexico.

Here is the Philadelphia Fed state coincident index release (pdf) for February 2011.

In the past month, the indexes increased in 44 states, decreased in three (Kansas, New Jersey, and Wyoming), and remained unchanged in three (Delaware, New Mexico, and South Dakota) for a one-month diffusion index of 82.

The second graph is of the monthly Philly Fed data for the number of states with one month increasing activity.

The second graph is of the monthly Philly Fed data for the number of states with one month increasing activity. The indexes increased in 44 states, decreased in 3, and remained unchanged in 4. Note: this graph includes states with minor increases (the Philly Fed lists as unchanged).

Several states fell back into declining activity in the 2nd of half of last year, but the situation has improved a little in early 2011.

Note: These are coincident indexes constructed from state employment data. From the Philly Fed:

The coincident indexes combine four state-level indicators to summarize current economic conditions in a single statistic. The four state-level variables in each coincident index are nonfarm payroll employment, average hours worked in manufacturing, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average). The trend for each state’s index is set to the trend of its gross domestic product (GDP), so long-term growth in the state’s index matches long-term growth in its GDP.

Real House Prices and Price-to-Rent

by Calculated Risk on 3/29/2011 11:24:00 AM

The following graph shows the quarterly Case-Shiller National Index (through Q4 2010), and the monthly Case-Shiller Composite 20 and CoreLogic House Price Indexes through January 2011 in real terms (adjusted for inflation using CPI less shelter).

Note: some people use other inflation measures to adjust for real prices.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

In real terms, the National index is back to Q1 2000 levels, the Composite 20 index is back to January 2001, and the CoreLogic index back to May 2000.

A few key points:

• The real price indexes are all at new post-bubble lows.

• I don't expect national real prices to fall to '98 levels. In many areas - if the population is increasing - house prices increase slightly faster than inflation over time, so there is an upward slope for real prices.

• Real prices are still too high, but they are much closer to the eventual bottom than the top in 2005. This isn't like in 2005 when prices were way out of the normal range.

• Nominal prices will probably fall some more and my forecast is for a decline of 5% to 10% from the October 2010 levels for the national price indexes.

Price-to-Rent

In October 2004, Fed economist John Krainer and researcher Chishen Wei wrote a Fed letter on price to rent ratios: House Prices and Fundamental Value. Kainer and Wei presented a price-to-rent ratio using the OFHEO house price index and the Owners' Equivalent Rent (OER) from the BLS.

Here is a similar graph through January 2011 using the Case-Shiller Composite 20 and CoreLogic House Price Index.

Here is a similar graph through January 2011 using the Case-Shiller Composite 20 and CoreLogic House Price Index.

This graph shows the price to rent ratio (January 1998 = 1.0).

An interesting point: the measure of Owners' Equivalent Rent (OER) is at about the same level as two years - so the price-to-rent ratio has mostly followed changes in nominal house prices since then. Rents are starting to increase again, and OER will probably increase in 2011 - lowering the price-to-rent ratio.

This ratio could decline another 10%, and possibly more if prices overshoot to the downside. The decline in the ratio will probably be a combination of falling house prices and increasing rents.

I know some people are forecasting nominal price declines of 20% to 30% from the current level. Those forecasts are based on more distressed supply hitting the market (almost 7 million loans are delinquent and 11.1 million borrowers have negative equity). However I think that forecast for house prices is too pessimistic.

One of the reasons that prices will probably not fall that far is all the cash buyers - especially at the low end. See from Bloomberg: Cash-Paying Vultures Pick Bones of U.S. Housing Market as Mortgages Dry Up (ht Mike In Long Island, db).

Earlier:

• Case Shiller: Home Prices Off to a Dismal Start in 2011

Case Shiller: Home Prices Off to a Dismal Start in 2011

by Calculated Risk on 3/29/2011 09:00:00 AM

S&P/Case-Shiller released the monthly Home Price Indices for January (actually a 3 month average of November, December and January).

This includes prices for 20 individual cities and and two composite indices (for 10 cities and 20 cities).

Note: Case-Shiller reports NSA, I use the SA data.

From S&P:Home Prices Off to a Dismal Start in 2011

ata through January 2011, released today by Standard & Poor’s for its S&P/Case-Shiller1 Home Price Indices ... show further deceleration in the annual growth rates in 13 of the 20 MSAs and the 10- and 20-City Composites compared to the December 2010 report. The 10-City Composite was down 2.0% and the 20-City Composite fell 3.1% from their January 2010 levels. San Diego and Washington D.C. were the only two markets to record positive year-over-year changes. However, San Diego was up a scant 0.1%, while Washington DC posted a healthier +3.6% annual growth rate. The same 11 cities that had posted recent index level lows in December 2010, posted new lows in January.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery. The first graph shows the nominal seasonally adjusted Composite 10 and Composite 20 indices (the Composite 20 was started in January 2000).

The Composite 10 index is off 31.4% from the peak, and down 0.2% in January (SA). The Composite 10 is still 2.2% above the May 2009 post-bubble bottom.

The Composite 20 index is also off 31.3% from the peak, and down 0.2% in January (SA). The Composite 20 is only 0.7% above the May 2009 post-bubble bottom and will probably be at a new post-bubble low soon.

The second graph shows the Year over year change in both indices.

The second graph shows the Year over year change in both indices.The Composite 10 SA is down 2.0% compared to January 2010.

The Composite 20 SA is down 3.1% compared to January 2010.

The third graph shows the price declines from the peak for each city included in S&P/Case-Shiller indices.

Prices increased (SA) in 8 of the 20 Case-Shiller cities in January seasonally adjusted. From S&P (NSA):

Prices increased (SA) in 8 of the 20 Case-Shiller cities in January seasonally adjusted. From S&P (NSA):In January, the 10-City and 20-City Composites were down 0.9% and 1.0%, respectively, from their December 2010 levels. The monthly statistics show that 19 of the 20 MSAs and both the 10-City and 20-City Composite were down in January 2011 versus December 2010, the only exception being Washington D.C. which posted a month-over-month increase of 0.1%. Seventeen of the 20 MSAs and both Composites have posted more than three consecutive months of negative monthly returns. In January 2011, 12 of the 20 MSAs and the 20-City Composite are down by more than 1% compared to their levels in the previous month.Prices in Las Vegas are off 58% from the peak, and prices in Dallas only off 7.3% from the peak.

From S&P (NSA):

Continuing the trend set late last year, we witnessed 11 MSAs posting new index level lows in January 2011, from their 2006/2007 peaks. These cities are Atlanta, Charlotte, Chicago, Detroit, Las Vegas, Miami, New York, Phoenix, Portland (OR), Seattle and Tampa. These same 11 cities had posted lows with December’s report, as well.Both composite indices are still slightly above the post-bubble low (SA), but the indexes will probably be at new lows in early 2011.

Monday, March 28, 2011

Sports Stadium bonds in trouble?

by Calculated Risk on 3/28/2011 10:43:00 PM

Small and large ...

From Michelle McNiel at the Wenatchee World The debt dilemma (ht Ken)

Ask any public official and they’ll say default is simply not an option when it comes to the Town Toyota Center’s $42 million debt.And from Darrell Preston and Aaron Kuriloff at Bloomberg: Texans’ NFL Stadium Bonds Fall Amid Default Talk (ht Brian)

But the “D” word is creeping into conversations around the community, fueled by uncertainty over just how the massive debt is going to be paid on the 4,300-seat events center.

Harris County-Houston Sports Authority bonds that financed venues for the Houston Texans and two other sports teams have fallen as much as 34 percent amid speculation the agency may default on payments.

...

The authority financed the building of Minute Maid Park, home to the Houston Astros Major League Baseball team; Reliant Stadium, for the Texans; and Toyota Center, for the Houston Rockets National Basketball Association team.

...

the authority sold $509.7 million in bonds between 1998 and 2000 [for Reliant Stadium], along with $461.6 million the following year.

Neutron Loans hit California City

by Calculated Risk on 3/28/2011 07:24:00 PM

I'm reminded of this quote:

“All of the old-timers knew that subprime mortgages were what we called neutron loans — they killed the people and left the houses,” said Louis S. Barnes, 58, a partner at Boulder West, a mortgage banking firm in Lafayette, Colo. ... from a 2007 NY Times article (pay)

And from the O.C. Register today: Vacant homes a clue to Santa Ana's census drop

A big jump in the number of vacant homes could be a key to understanding this city's surprising drop in population as recorded by the 2010 census.Some probably double up. Another earlier article suggested some former residents may have moved back to Mexico. But the reason is neutron loans ...

...

Santa Ana's drop, in raw numbers, was the largest of any California city.

...

The census counted 76,896 housing units in Santa Ana and determined that 3,722 of them were vacant. [CR Note: the 2000 Census showed 74,588 housing units in Santa Ana and 1,586 vacant. So the vacancy rate more than doubled]

Among cities in Orange County, Santa Ana had among the highest concentrations of mortgage defaults in 2009, which could explain why the census found so many vacant homes in 2010.

... it's unclear where the people who left behind vacant homes went, since other states didn't show big influxes of people from California, [John Malson, acting chief of the demographic research unit at the Department of Finance] said. ... "We assumed a lot of people were moving back home or doubling up," he said. "It just seems that there might be a missed population from the census."

Personal Saving Rate and Income less Transfer Payments

by Calculated Risk on 3/28/2011 03:43:00 PM

A couple more graphs based on the Personal Income and Outlays report.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

This first graph shows real personal income less transfer payments as a percent of the previous peak. This has been slow to recover - and real personal income less transfer payments declined slightly in February. This remains 3.2% below the previous peak.

The personal saving rate decreased to 5.8% in January.

Personal saving -- DPI less personal outlays -- was $676.7 billion in February, compared with $710.5 billion in January. Personal saving as a percentage of disposable personal income was 5.8 percent in February, compared with 6.1 percent in January.

This graph shows the saving rate starting in 1959 (using a three month trailing average for smoothing) through the February Personal Income report.

This graph shows the saving rate starting in 1959 (using a three month trailing average for smoothing) through the February Personal Income report. When the recession began, I expected the saving rate to rise to 8% or more. However that was just a guess. After increasing sharply during the recession, the saving rate has been mostly moving sideways for the last two years - so spending growth has mostly kept pace with income growth, and that will probably continue all year.

Here come the downgrades for Q1 GDP Growth

by Calculated Risk on 3/28/2011 12:50:00 PM

Before the February Personal Income and Outlays report, most analysts were expecting real GDP growth of over 3% in Q1. As an example, Paul Kasriel at Northern Trust was forecasting 3.1% real GDP growth with 2.2% real Personal Consumption Expenditure (PCE) growth, and Goldman Sachs was forecasting 3.5% real GDP growth with 3.0% real PCE growth.

Both of those forecast now look too high.

Note: The quarterly change is not calculated as the change from the last month of one quarter to the last month of the next. Instead, you have to average all three months of a quarter, and then take the change from the average of the three months of the preceding quarter.

So, for Q1, you would average PCE for January, February, and March, then divide by the average for October, November and December. Of course you need to take this to the fourth power (for the annual rate) and subtract one. Also the March data isn't released until after the advance Q1 GDP report.

There are a few commonly used methods to forecast quarterly PCE growth after the release of the second month of the quarter report (February for Q1). Some analysts use the "two month" method (averaging the growth from October-to-January with the growth from November-to-February). Others use the mid-month method and just use the growth from November-to-February.

Either way, the first two months of Q1 2011 suggest PCE growth of around 1.4% for the quarter as shown in the following table.

| PCE, Billions (2005 dollars), SAAR | 3 Month Change (annualized) | Quarter (Annualized) | |

|---|---|---|---|

| Jan-10 | $9,189.30 | ||

| Feb-10 | $9,228.20 | ||

| Mar-10 | $9,258.60 | ||

| Apr-10 | $9,257.20 | 2.99% | |

| May-10 | $9,280.50 | 2.29% | |

| Jun-10 | $9,289.30 | 1.33% | 2.2% |

| Jul-10 | $9,302.60 | 1.98% | |

| Aug-10 | $9,333.90 | 2.32% | |

| Sep-10 | $9,355.40 | 2.88% | 2.4% |

| Oct-10 | $9,402.80 | 4.38% | |

| Nov-10 | $9,426.60 | 4.03% | |

| Dec-10 | $9,439.30 | 3.64% | 4.0% |

| Jan-11 | $9,435.10 | 1.38% | |

| Feb-11 | $9,459.00 | 1.38% | |

| Mar-11 |

Although there are other components of GDP (investment, trade, government spending and inventory changes), it appears Q1 GDP growth will be lower than expected.

I still expect stronger GDP growth in 2011 than in 2010, but it appears 2011 is off to a sluggish start - and I'm concerned about world events and high oil prices.

Texas Manufacturing Activity Strengthens Further, Pending Home sales increase in February

by Calculated Risk on 3/28/2011 10:30:00 AM

• From the Dallas Fed: Texas Manufacturing Activity Strengthens Further

Texas factory activity increased in March, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, rose sharply to 24, its highest level in nearly a year.Another strong report. The last of the regional reports will be released on Thursday, and the ISM manufacturing index will be released on Friday (should be very strong again).

...

Labor market indicators continued to reflect expansion. The employment index came in at a reading of 12, similar to February. Twenty percent of manufacturers reported hiring new workers compared with eight percent reporting layoffs. The hours worked index jumped to 13, with the share of firms reporting decreases in employee workweeks falling to its lowest level since 2006. The wages and benefits index rose from 9 to 12, although the great majority of respondents noted no change in labor costs.

• From the NAR: February Pending Home Sales Rise

The Pending Home Sales Index,* a forward-looking indicator, rose 2.1 percent to 90.8, based on contracts signed in February, from 88.9 in January. The index is 8.2 percent below 98.9 recorded in February 2010. The data reflects contracts and not closings, which normally occur with a lag time of one or two months.This suggests a slight increase in existing home sales in March and April.

Personal Income and Outlays Report for February

by Calculated Risk on 3/28/2011 08:30:00 AM

The BEA released the Personal Income and Outlays report for January:

Personal income increased $38.1 billion, or 0.3 percent ... Personal consumption expenditures (PCE) increased $69.1 billion, or 0.7 percent.The following graph shows real Personal Consumption Expenditures (PCE) through January (2005 dollars). Note that the y-axis doesn't start at zero to better show the change.

...

Real PCE -- PCE adjusted to remove price changes -- increased 0.3 percent in February, in contrast to a decrease of less than 0.1 percent in January.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.PCE increased 0.7% in February, but real PCE only increased 0.3% as the price index for PCE increased 0.4 percent in February.

Personal income growth was slightly below expectations. Note: Core PCE - PCE excluding food and energy - increased 0.2 percent in February.

Even though PCE growth was at expectations, real PCE was low - and this suggests analysts will downgrade their forecasts for Q1 GDP. Using the two month estimate for PCE growth (averaging the growth of January and February over the first two months of the previous quarter) suggests PCE growth of around 1.4% in Q1 (down sharply from 4.0% in Q4).

Weekend on U.S. economy:

• Here is the Summary for Week ending March 25th.

• Lawler: Census 2010 and Excess Vacant Housing Units

• Schedule for Week of March 27th

Sunday, March 27, 2011

Ireland Update: Stress Tests, New ECB Liquidity Facility, and ... bondholder haircuts?

by Calculated Risk on 3/27/2011 07:29:00 PM

The next round of Irish bank stress test results are due on March 31st. Meanwhile the ECB is seeking a new liquidity facility and Ireland is talking haircuts for senior bondholders ...

• From Bloomberg: Ireland Seeks to Share Bank-Loss Burdens With Bond Holders, Noonan Says

Ireland wants to share bank losses with senior bondholders as part of a “final solution” for the country’s debt-laden financial system, Agriculture Minister Simon Coveney said.• From the Financial Times: Ireland seeks ECB deal to secure banks

Finance Minister Michael Noonan will seek agreement from European authorities to share losses with bond holders after stress-test results on March 31 determine how much extra capital the banks need, Coveney said.

• From the WSJ: ECB Seeks New Liquidity Plan for Irish Banks

the Sunday Business Post newspaper reported over the weekend that the tests will expose a capital shortfall of €18 billion to €23 billion. That is more than the €10 billion earmarked by the European Union, International Monetary Fund and European Central Bank in Ireland's November bailout deal, but less than the €35 billion many analysts had estimated the banks would require.Yesterday and Today:

• Here is the Summary for Week ending March 25th.

• Lawler: Census 2010 and Excess Vacant Housing Units

• Schedule for Week of March 27th

Japan Nuclear Update

by Calculated Risk on 3/27/2011 02:46:00 PM

• From Kyodo News: Woes deepen over radioactive water at nuke plant, sea contamination

Japan on Sunday faced an increasing challenge of removing highly radioactive water found inside buildings near some troubled nuclear reactors at the Fukushima Daiichi plant, with the radiation level of the surface of the pool in the basement of the No. 2 reactor's turbine building found to be more than 1,000 millisieverts per hour.• From the LA Times: Officials retract reports of extremely high radiation at Fukushima plant

... efforts to restore power and enhance cooling efficiency at the crisis-hit nuclear power plant is showing slow progress partly due to the radioactive pools of water found at the Nos. 1, 2, 3 and 4 units.

Workers there are planning to turn on the lights in the control room of the No. 4 reactor, while also trying to inject freshwater into tanks storing spent nuclear fuel at the plant's Nos. 1, 2, 3 and 4 reactors to prevent crystallized salt from seawater already injected from hampering the smooth circulation of water and thus diminishing the cooling effect.

• From the NY Times: Higher Levels of Radiation Found at Japan Reactor Plant

Yesterday and Today:

• Here is the Summary for Week ending March 25th.

• Lawler: Census 2010 and Excess Vacant Housing Units

• Schedule for Week of March 27th

Schedule for Week of March 27th

by Calculated Risk on 3/27/2011 09:27:00 AM

Yesterday:

• Here is the Summary for Week ending March 25th.

• Lawler: Census 2010 and Excess Vacant Housing Units

The key report for this week will be the March employment report to be released on Friday, April 1st.

Other key reports include the February Personal Income and Outlays report on Monday, the Case-Shiller house price index on Tuesday, the ISM manufacturing index on Friday, and vehicle sales also on Friday.

8:30 AM: Personal Income and Outlays for February. The consensus is for a 0.4% increase in personal income and a 0.6% increase in personal spending.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.Real Personal Consumption Expenditures (PCE) - PCE adjusted for inflation - decreased 0.1 percent in January.

Using the February data we can obtain an early estimate for Q1 real PCE growth (annualized) using the two-month method (usually pretty close).

10:00 AM: Pending Home Sales for February. The consensus is for pending sales home sales to be flat (a leading indicator for existing home sales).

10:30 AM: Dallas Fed Manufacturing Survey for March. The Texas production index increased last month to 9.7 (from 0.2 in January).

9:00 AM: S&P/Case-Shiller Home Price Index for January. Although this is the January report, it is really a 3 month average of November, December and January.

This graph shows the seasonally adjusted Composite 10 and Composite 20 indices through December (the Composite 20 was started in January 2000).

This graph shows the seasonally adjusted Composite 10 and Composite 20 indices through December (the Composite 20 was started in January 2000).Prices are falling again, and the Composite 20 index will probably be close to a new post-bubble low in January. The consensus is for prices to decline about 0.4% in January; the seventh straight month of house price declines.

10:00 AM: Conference Board's consumer confidence index for March. The consensus is for a decrease to 65.0 from 70.4 last month due to world events and higher gasoline prices.

7:00 AM: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index. This index has been very weak over the last couple months suggesting weak home sales through the first few months of 2011.

8:15 AM: The ADP Employment Report for March. This report is for private payrolls only (no government). The consensus is for +205,000 payroll jobs in March, down slightly from the 217,000 reported in February.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for a decrease to 380,000 from 382,000 last week.

9:45 AM: Chicago Purchasing Managers Index for March. The consensus is for a slight decrease to a still very strong 70.0 (down from 71.2 in March).

10:00 AM: Manufacturers' Shipments, Inventories and Orders for February. The consensus is for a 0.3% increase in orders.

11:00 AM: Kansas City Fed regional Manufacturing Survey for March. The index was at an all time high 19 in February.

8:30 AM: Employment Report for March.

The consensus is for an increase of 195,000 non-farm payroll jobs in March, after an increase of 192,000 in February (that was partially "payback" for the weak January report).

The consensus is for an increase of 195,000 non-farm payroll jobs in March, after an increase of 192,000 in February (that was partially "payback" for the weak January report). This graph shows the net payroll jobs per month (excluding temporary Census jobs) since the beginning of the recession. The estimate for March is in blue.

The consensus is for the unemployment rate to remain at 8.9% in March.

The second employment graph shows the percentage of payroll jobs lost during post WWII recessions - aligned at maximum job losses.

The second employment graph shows the percentage of payroll jobs lost during post WWII recessions - aligned at maximum job losses.This shows the severe job losses during the recent recession - there are currently 7.5 million fewer jobs in the U.S. than when the recession started.

10:00 AM: ISM Manufacturing Index for March. The consensus is for a slight decrease to 61.2 from the strong 61.4 in February. All of the regional manufacturing surveys showed continued expansion in March.

10:00 AM: Construction Spending for February. The consensus is for no change in construction spending.

All day: Light vehicle sales for March. Light vehicle sales are expected to decrease to 13.2 million (Seasonally Adjusted Annual Rate), from 13.4 million in February.

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the February sales rate.

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the February sales rate. Edmunds is forecasting: "Edmunds.com analysts predict that March’s Seasonally Adjusted Annualized Rate (SAAR) will be 13.07 million, down from 13.38 in February 2011."

Best wishes to All!

Saturday, March 26, 2011

LPS: Overall mortgage delinquencies declined slightly in February

by Calculated Risk on 3/26/2011 10:24:00 PM

Earlier:

• Here is the Summary for Week ending March 25th.

• Lawler: Census 2010 and Excess Vacant Housing Units

LPS Applied Analytics recently released their February Mortgage Performance data. From LPS:

•Delinquency rates resumed their decline after an increase in January and foreclosure inventories remain stable, slightly below historic highs.

• Delinquencies continue to improve as new problem loan rates decline and cure rates increase.

• Foreclosure start declines and foreclosure suspensions are reducing the upward pressure on inventories caused by foreclosure sale moratoria.

• An enormous backlog of foreclosures still exists with overhang at every level:

–There are three times the number of loans deteriorating greater than 90+ days delinquent as compared to foreclosure starts.

–There are also three times the number foreclosure starts vs. foreclosure sales.

–Foreclosure inventory levels are over 30 times monthly foreclosure sale volume.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.This graph provided by LPS Applied Analytics shows the percent delinquent, percent in foreclosure, and total non-current mortgages.

The percent in the foreclosure process has been trending up because of the foreclosure moratoriums.

According to LPS, 8.80% of mortgages are delinquent (down from 8.90% in January), and another 4.15% are in the foreclosure process (about the same as 4.16% in January) for a total of 12.96%. It breaks down as:

• 2.49 million loans less than 90 days delinquent.

• 2.16 million loans 90+ days delinquent.

• 2.2 million loans in foreclosure process.

For a total of 6.86 million loans delinquent or in foreclosure.

The second graph shows the break down of serious deliquencies.

The second graph shows the break down of serious deliquencies.The number of seriously delinquent loans has stopped decreasing - mostly because the number of seriously delinquent loans that have not made a payment in over a year continues to increase.

Note: I've seen some people include these almost 7 million delinquent loans as "shadow inventory". This is not correct because 1) some of these loans will cure, and 2) some of these homes are already listed for sale (so they are included in the visible inventory).

Lawler: Census 2010 and Excess Vacant Housing Units

by Calculated Risk on 3/26/2011 05:54:00 PM

CR Note: This long and detailed note on the 2010 Census data is from economist Tom Lawler. Here is a spreadsheet for the 50 states (and D.C.) including the 2000 and 1990 Census data.

This starts with a brief excerpt (click read more for the full post). For those not interested in why some data drives demographers to drink, here is the Summary for Week ending March 25th.

Census 2010: Households, Housing Stock, and Vacant Housing Units: Understanding Why Demographers Drink by Tom Lawler

Census has now released the final Census 2010 counts for state and local population and housing units – occupied and vacant. Here are some national totals, as well as a comparison to the “official” Census 2000 counts – which are “known” to be off, but by uncertain amounts.

| Census 2010 | Census 2000 | Change | % Change | |

|---|---|---|---|---|

| Population | 308,745,538 | 281,421,906 | 27,323,632 | 9.7% |

| Total Housing Units | 131,704,730 | 115,904,641 | 15,800,089 | 13.6% |

| Occupied | 116,716,292 | 105,480,101 | 11,236,191 | 10.7% |

| Vacant | 14,988,438 | 10,424,540 | 4,563,898 | 43.8% |

| Gross Vacancy Rate | 11.38% | 8.99% | 2.39% |

For those who follow housing production, one of the “striking” things about the Census 2010 vs. the Census 2000 data is the apparent growth in the housing stock – 15.8 million units.

Summary for Week ending March 25th

by Calculated Risk on 3/26/2011 11:31:00 AM

World events once again dominated the headlines last week, with the Japanese nuclear issues, Libya, the Middle-East (especially Syria) and also the European financial crisis (Portugal, Ireland, Greece - even Spain and more) all on the front page.

In the U.S., the economic data was weaker, mostly because the major economic releases were housing related. New home sales were at a record low, and existing home sales fell sharply. But also durable goods orders were weaker than expected and consumer sentiment declined sharply from February (probably due to high gasoline prices and world events).

On the positive side, initial weekly unemployment claims continued to decline and the Richmond Fed manufacturing survey indicated continued expansion in March.

Below is a summary of economic data last week mostly in graphs:

• New Home Sales Fall to Record Low in February

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

The Census Bureau reported New Home Sales in February were at a seasonally adjusted annual rate (SAAR) of 250 thousand. This was down from a revised 301 thousand in January.

The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate. This was a new record low sales rate and well below the consensus forecast of 290 thousand homes sold (SAAR).

The 2nd graph shows "months of supply". Months of supply increased to 8.9 in February from 7.4 months in January. The all time record was 12.1 months of supply in January 2009. This is very high (less than 6 months supply is normal).

The 2nd graph shows "months of supply". Months of supply increased to 8.9 in February from 7.4 months in January. The all time record was 12.1 months of supply in January 2009. This is very high (less than 6 months supply is normal).

The third graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).

In February 2010 (red column), 19 thousand new homes were sold (NSA). This is a new record low for the month of February.

In February 2010 (red column), 19 thousand new homes were sold (NSA). This is a new record low for the month of February.

The previous record low for February was 27 thousand in 2010. The high was 109 thousand in 2005.

This was a very weak report ...

• February Existing Home Sales: 4.88 million SAAR, 8.6 months of supply

The NAR reported: February Existing-Home Sales Decline

This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1993.

This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1993.

Sales in February 2011 (4.88 million SAAR) were 9.6% lower than last month, and were 2.8% lower than February 2010.

The next graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Inventory is not seasonally adjusted, so it really helps to look at the YoY change.

Although inventory increased from January to February (as usual), inventory decreased 1.2% YoY in February. This is a small YoY decrease and follows six consecutive month of year-over-year increases in inventory.

Although inventory increased from January to February (as usual), inventory decreased 1.2% YoY in February. This is a small YoY decrease and follows six consecutive month of year-over-year increases in inventory.

Inventory should increase over the next few months (the normal seasonal pattern), and the YoY change is something to watch closely this year. Inventory and "months of supply" are already very high, and further YoY increases in inventory would put more downward pressure on house prices.

This graph shows existing home sales Not Seasonally Adjusted (NSA).

This graph shows existing home sales Not Seasonally Adjusted (NSA).

The red columns in January and February are for 2011.

Sales NSA were about the same level as the last three years. February is usually the second weakest month of the year for existing home sales (close to January). The real key is what happens in the spring and summer - and March sales and inventory will give a clearer picture of existing home sales activity.

• AIA: Architecture Billings Index increased slightly in February

From the American Institute of Architects: Architecture Firm Billings Increase Slightly in February. Note: This index is a leading indicator for new Commercial Real Estate (CRE) investment.

This graph shows the Architecture Billings Index since 1996. The index showed billings were slightly higher in February (at 50.6).

This graph shows the Architecture Billings Index since 1996. The index showed billings were slightly higher in February (at 50.6).

According to the AIA, there is an "approximate nine to twelve month lag time between architecture billings and construction spending" on non-residential construction. So this indicator suggests the drag from CRE investment will end mid-year 2011 or so - but there won't be a strong increase in investment.

• Consumer Sentiment declines in March

The final March Reuters / University of Michigan consumer sentiment index declined to 67.5 from the preliminary March reading of 68.2 - and down from 77.5 in February. This is the lowest level since November 2009 and was below the consensus forecast of 68.0.

In general consumer sentiment is a coincident indicator and is usually impacted by employment (and the unemployment rate) and gasoline prices.

With higher gasoline prices and the scary world news, a low reading isn't that surprising.

• Other Economic Stories ...

• From the Chicago Fed: Economic Growth Near Average in February

• From the Richmond Fed: Manufacturing Activity Continues to Advance in March; Expectations Remain Upbeat

• ATA Truck Tonnage Index declined in February

• Moody's: Commercial Real Estate Prices declined 1.2% in January

• DOT: Vehicle Miles Driven increased slightly in January

• Q4 Real GDP Growth revised up to 3.1%

• Unofficial Problem Bank list increases to 985 Institutions

Best wishes to all!

Unofficial Problem Bank list increases to 985 Institutions

by Calculated Risk on 3/26/2011 08:15:00 AM

Note: this is an unofficial list of Problem Banks compiled only from public sources.

Here is the unofficial problem bank list for Mar 25, 2011.

Changes and comments from surferdude808:

The Unofficial Problem Bank List continued to climb as the FDIC released its actions for February 2011. This week, there were eight additions and five removals, which leaves the list with 985 institutions with assets of $431.1 billion.

The removals include the failed The Bank of Commerce, Wood Dale, IL ($163 million); one action termination against First Bank, Williamstown, NJ ($212 million); and three sales to private investors by West Michigan Community Bank, Hudsonville, MI ($123 million); Treaty Oak Bank, Austin, TX ($110 million Ticker: TOAK); and Community State Bank, Austin, TX ($21 million).

Among the eight additions are Plumas Bank, Quincy, CA ($483 million Ticker: PLBC); Country Bank, Aledo, IL ($213 million); and First Financial Bank, Bessemer, AL ($205 million).

Other changes include the issuance of seven and termination of one Prompt Corrective Order. The FDIC terminated the PCA order against Seattle Bank, Seattle, WA and issued orders against The Village Bank, Saint George, UT ($209 million); First Heritage Bank, Snohomish, WA ($179 million); Summit Bank, Prescott, AZ ($81 million); and four subsidiaries of Capitol Bancorp (Ticker: CBCR): Michigan Commerce Bank, Ann Arbor, MI ($934 million); Bank of Las Vegas, Las Vegas, NV ($375 million); Sunrise Bank of Arizona, Phoenix, AZ ($353 million); and Central Arizona Bank, Casa Grande, AZ ($76 million). (Edited by CR: see here for correction on Capitol Bancorp)

With the passage of another quarter, it is time to update the transition matrix. The Unofficial Problem Bank List debuted on August 7, 2009 with 389 institutions with assets of $276.3 billion (see table). Over the past 19 months, 176 institutions have been removed from the original list with 120 due to failure, 40 due to action termination, and 16 due to unassisted merger. Almost 31 percent of the 389 institutions on the original list have failed, which is substantially higher than the 12 percent figure usually cited by the media as the failure rate for institutions on the FDIC Problem Bank List. Failed bank assets have totaled $166.6 billion or 60 percent of the $276.3 billion on the original list.

Since the publication of the original list, another 940 institutions have been added. However, only 772 of those 940 additions remain on the current list as 168 institutions have been removed in the interim. Of the 168 interim removals, 119 were due to failure, 32 were due to unassisted merger, 15 from action termination, and two from voluntary liquidation. In total, 1,329 institutions have made an appearance on the Unofficial Problem Bank List and 239 or 18.0 percent have failed. Of the 344 total removals, failure is the primary form of exit (239 or 69.5 percent) while only 55 or 16.0 percent have been rehabilitated. The average asset size of removals because of failure is $1.04 billion. Currently, the average asset size of institutions on the current list is $438 million versus $710 million on the original list.

| Unofficial Problem Bank List | |||

|---|---|---|---|

| Change Summary | |||

| Number of Institutions | Assets ($Thousands) | ||

| Start (8/7/2009) | 389 | 276,313,429 | |

| Subtractions | |||

| Action Terminated | 40 | (5,853,210) | |

| Unassisted Merger | 16 | (2,478,895) | |

| Voluntary Liquidation | 0 | - | |

| Failures | 120 | (166,633,042) | |

| Asset Change | (16,154,143) | ||

| Still on List at 3/25/2011 | 213 | 85,194,139 | |

| Additions | 772 | 345,874,340 | |

| End (3/25/2011) | 985 | 431,068,479 | |

| Interperiod Deletions1 | |||

| Action Terminated | 15 | 15,245,458 | |

| Unassisted Merger | 32 | 26,763,786 | |

| Voluntary Liquidation | 2 | 833,567 | |

| Failures | 119 | 81,716,210 | |

| Total | 168 | 124,559,021 | |

| 1Institution not on 8/7/2009 or 3/25/2011 list but appeared on a list between these dates. | |||

{kind=link}