RSS Feed

RSS Feed by Calculated Risk on 4/08/2012 09:09:00 AM

Sunday, April 08, 2012

Housing Story: Owning vs. Renting

From Eric Wolff at the North County Times: 'This is crazy': Home ownership cheaper than renting

Monthly payments on a house are now cheaper than monthly rents on a similar house in most of North San Diego and Southwest Riverside counties, according to an analysis of county-supplied and Realtor data by the North County Times.These comparisons aren't perfect, however the price-to-rent ratio (that doesn't include interest rates) is back to normal too, so stories like this aren't a surprise.

... prices for houses plummeted and interest rates fell below 4 percent, a 40-year low. The combination of factors has created a house market in North San Diego and Southwest Riverside county in which homeowners are getting a better deal than renters, at least after they've paid their down payment.

"I don't think this has ever happened before," said G.U. Krueger, a principal economist for HousingEcon.com. "It's a function of the huge housing price collapse which has left a lot of people in the lurch."

Or, as Carlsbad real estate agent Tyson Lund put it: "This is crazy."

...

There are, of course, a host of caveats not included in the calculation. The analysis does not amortize the down payment on the house, nor does it include the maintenance costs that homeowners accrue to keep their homes in good repair, though many economists argue the mortgage interest tax deduction offered by the federal government balances those expenses. Still, the calculation depends on a homebuyer having enough money to make a down payment, and sufficient credit to get a loan. In 2011, banks raised the bar on those to whom they'd lend, making it difficult for many people to get mortgages. ... "If rates were back to 5.5 percent or 6 percent, then the mortgages become more expensive than rents. I would not call 4 percent a normalized housing market," [Nathan Moeder, a principal at The London Group] said in an email. "Today, people are able to afford more home because of the interest rates."

Saturday, April 07, 2012

HUD Secretary on Principal Reductions

by Calculated Risk on 4/07/2012 08:17:00 PM

HUD Secretary Shaun Donovan will be on C-SPAN Sunday morning (see here).

Here are some comments on Fannie and Freddie principal reductions:

Q: Why should Fannie and Freddie be forced to do write-downs?A few days ago, FHFA acting director Edward DeMarco said:

DONOVAN: This isn’t about force. This is about making the right decision for homeowners and for the taxpayer. We believe and there is a lot of agreement, many economists, those who have looked closely at this data who believe where you have someone who is deeply underwater, where you’re in a situation where there is really no light at the end of the tunnel, no sense that even if you’re paying your mortgage for three, four, five years or even a decade, that you’ll get back to building equity again. Families will give up at some point. We think the data shows that. Really the issue here is about the numbers and the analysis and whether this is not only good for homeowners but also good for the taxpayer. And we believe with the changes that we’ve made over the last few months that the case is compelling. And my experience with Ed DeMarco is whatever his personal feelings are, he is dedicated to making sure that he follows the law and what the conservator is required to do. And we believe based on the analysis that we’ve done that the evidence is that principal write-downs should happen in cases where it’s not only good for the homeowner but also good for the taxpayer.

Q: Three out of four deeply underwater borrowers with loans backed by Fannie and Freddie are paying. How concerned are you that some of those borrowers may stop paying if you offer debt reduction to borrowers who are delinquent?

DONOVAN: The vast majority of homeowners don’t operate that way. They know that their home is where they’re going to raise their kids. They’re part of a community there. The home is much more than an investment. And so we really know this from studies we’ve done, that the vast majority of folks, these families, aren’t going to just put all of that at risk to default on purpose on their homes.

And so what we’re really talking about is a small group of folks, maybe demographically single folks who aren’t giving up those same things, who see that there may be from defaulting that you know they could move across the street or other things. So there is a small group. But we shouldn’t punish the vast majority of folks where strategic default isn’t really a risk, just to fix what may be really a risk with a small percentage.

This isn’t that hard a problem to design around. Take the mortgage-servicing settlement that we recently reached. In that case what we’re doing is putting in place protections so that we avoid some of the risks of strategic default. For example, in that case many of the servicers are simply going to set a date at which you’re eligible based on delinquency and what that means is there’s nothing you can do. You can’t make yourself eligible. You can’t start to default on your mortgage and all of a sudden start to get a windfall from that by getting a principal reduction. And so while I understand the concerns about this, I think one the vast majority of homeowners are not at risk for strategic default. And two, even for those where there is some risk, there is a way to design it so that … it avoids those risks.

[W]e are currently evaluating the recent Treasury Department proposal to HAMP regarding principal forgiveness and expect a decision this month.So a decision will probably be made very soon.

Earlier:

• Summary for Week Ending April 6th

• Schedule for Week of April 8th

Unofficial Problem Bank List and Quarterly Transition Matrix

by Calculated Risk on 4/07/2012 05:25:00 PM

This is an unofficial list of Problem Banks compiled only from public sources.

Here is the unofficial problem bank list for April 6, 2012. (table is sortable by assets, state, etc.)

Changes and comments from surferdude808:

Quiet week for the Unofficial Problem Bank List as there were only two removals. The changes leave the list with 946 institutions with assets of $376.5 billion. A year ago, the list 982 institutions with assets of $433.2 billion. The action against First Savings Bank Northwest, Renton, WA ($1.0 billion Ticker: FFNW) was replaced by an informal action and Pilsen State Bank, Lincolnville, KS ($11 million) was dissolved through an unassisted merger.

With the passage of the first quarter of 2012, it is time to update the Unofficial Problem Bank List transition matrix. The list debuted on August 7, 2009 with 389 institutions with assets of $276.3 billion (see table). Over the past 32 months, 230 institutions or about 59 percent of the institutions on the original list have been removed with 137 from failure, 71 from action termination, 20 from unassisted merger, and two from voluntary liquidation. About 35 percent of the 389 institutions on the original list have failed, which is substantially higher than the 12 percent figure usually cited by the media as the failure rate for institutions on the FDIC Problem Bank List.

Since the publication of the original list, another 1,122 institutions have been added. However, only 789 of those additions remain on the current list as 333 institutions have been removed in the interim. Of the 333 inter-period removals, 178 were from failure, 72 were from an unassisted merger, 78 from action termination, and five from voluntary liquidation.

In total, 1,511 institutions have made an appearance on the Unofficial Problem Bank List and 315 or 20.8 percent have failed. Of the 563 total removals, the primary way of exit from the list is failure at 315 institutions or 56 percent. Only 149 or around 27 percent have been able to rehabilitate themselves to see their respective action terminated. Alternatively, another 92 or nearly 16 percent found merger partners most likely to avoid failure. Total assets that have appeared on the list amount to $789.8 billion and $282.3 billion have been removed due to failure. The average asset size of removals from failure is $896 million.

| Unofficial Problem Bank List | |||

|---|---|---|---|

| Change Summary | |||

| Number of Institutions | Assets ($Thousands) | ||

| Start (8/7/2009) | 389 | 276,313,429 | |

| Subtractions | |||

| Action Terminated | 71 | (19,039,409) | |

| Unassisted Merger | 20 | (3,401,337) | |

| Voluntary Liquidation | 2 | (4,855,164) | |

| Failures | 137 | (178,872,611) | |

| Asset Change | (14,066,292) | ||

| Still on List at 3/31/2012 | 167 | 56,078,616 | |

| Additions | 789 | 321,473,577 | |

| End (3/31/2012) | 948 | 377,552,193 | |

| Intraperiod Deletions1 | |||

| Action Terminated | 78 | 44,376,836 | |

| Unassisted Merger | 72 | 42,937,646 | |

| Voluntary Liquidation | 5 | 1,259,188 | |

| Failures | 178 | 103,460,185 | |

| Total | 333 | 192,033,855 | |

| 1Institutions not on 8/7/2009 or 3/31/2012 list but appeared on a list between these dates. | |||

Schedule for Week of April 8th

by Calculated Risk on 4/07/2012 01:28:00 PM

Earlier:

• Summary for Week Ending April 6th

The key reports for this week are the February Trade Balance report, to be released on Thursday, and the March Consumer Price Index (CPI), to be released on Friday.

FHFA acting director Edward DeMarco is speaking on Tuesday: "Addressing the Weak Housing Market: Is Principal Reduction the Answer?"

There will be several speeches by Fed officials, including both Fed Chairman Ben Berananke, and Fed Vice Chairman Janet Yellen.

Morning: LPS House Price Index for January.

7:15 PM ET: Speech by Fed Chairman Ben Bernanke, "Fostering Financial Stability", At the 2012 Federal Reserve Bank of Atlanta Financial Markets Conference, Stone Mountain, Georgia

7:30 AM: NFIB Small Business Optimism Index for March.

7:30 AM: NFIB Small Business Optimism Index for March. Click on graph for larger image in graph gallery.

This graph shows the small business optimism index since 1986. The index increased to 94.3 in February from 93.9 in January. This is the sixth increase in a row after for the index, and the index is now at second highest level since December 2007. The consensus is for an increase to 94.8.

9:30 AM ET: Speech by FHFA acting director Edward DeMarco: "Addressing the Weak Housing Market: Is Principal Reduction the Answer?" at the The Brookings Institution, 1775 Massachusetts Ave., NW Washington, DC.

10:00 AM ET: Job Openings and Labor Turnover Survey for February from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for February from the BLS. This graph shows job openings (yellow line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings were unchanged in January, and the number of job openings (yellow) has generally been trending up, and are up about 21% year-over-year compared to January 2011.

10:00 AM: Monthly Wholesale Trade: Sales and Inventories for February. The consensus is for a 0.6% increase in inventories.

7:00 AM: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index. This index has been weak this year, although this does not include all the cash buyers.

8:30 AM: Import and Export Prices for February. The consensus is a for a 0.9% increase in import prices.

2:00 PM: Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

6:15 PM: Speech by Fed Vice Chair Janet Yellen, "The Economic Outlook and Monetary Policy", At the Money Marketeers of New York University Dinner Meeting, New York, New York

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for claims to increase slightly to 359,000.

8:30 AM: Trade Balance report for February from the Census Bureau.

8:30 AM: Trade Balance report for February from the Census Bureau. Both exports and imports increased in January. Imports stalled in the middle of 2011, but increased towards the end of the year (seasonally adjusted). Exports are well above the pre-recession peak and up 8% compared to January 2011; imports just passed the pre-recession high and imports are up about 8% compared to January 2011.

The consensus is for the U.S. trade deficit to decrease to $51.7 billion in February, up from from $52.6 billion in January. Export activity to Europe will be closely watched due to economic weakness.

8:30 AM: Producer Price Index for March. The consensus is for a 0.3% increase in producer prices (0.2% increase in core).

8:30 AM: Consumer Price Index for March. The consensus is a 0.3% increase in prices. The consensus for core CPI to increase 0.2%.

9:55 AM: Reuter's/University of Michigan's Consumer sentiment index (perliminary for April). The consensus is for sentiment to be unchanged at 76.2.

1:00 PM: Speech by Fed Chairman Ben Bernanke, "Reflections on the Crisis and the Policy Response", At the Russell Sage Foundation and The Century Foundation Conference on "Rethinking Finance," New York, New York

Summary for Week ending April 6th

by Calculated Risk on 4/07/2012 07:43:00 AM

The March employment report was below expectations with only 120,000 payroll jobs added. The unemployment rate declined slightly to 8.2%. U-6, an alternate measure of labor underutilization that includes part time workers and marginally attached workers, declined to 14.5% from 14.9% in February.

Is this the beginning of even slower employment growth, or was this just noise? That is a key question and will put additional pressure on the April report.

In 2011, the economy added 1.84 million payroll jobs (2.1 million private sector), and, even after the weak March report, the economy is on pace to add over 2.5 million payroll jobs this year. That is still sluggish growth given the slack in the system, but better than 2011.

Other reports below expectations included March auto sales, February construction spending, and the March ISM service survey. The ISM manufacturing survey was slightly above expectations.

A couple of other positives: initial weekly unemployment claims continued to decline, and, for commercial real estate, the office and mall vacancy rates are now declining.

Overall it was a disappointing week and suggests sluggish growth.

Here is a summary in graphs:

• March Employment Report: 120,000 Jobs, 8.2% Unemployment Rate

Click on graph for larger image.

Click on graph for larger image.

This graph shows the jobs added or lost per month (excluding temporary Census jobs) since the beginning of 2008.

From the BLS: "Nonfarm payroll employment rose by 120,000 in March, and the unemployment rate was little changed at 8.2 percent, the U.S. Bureau of Labor Statistics reported today."

The second graph shows the employment population ratio, the participation rate, and the unemployment rate. The unemployment rate was declined to 8.2% (red line).

The Labor Force Participation Rate decreased to 63.8% in March (blue line). This is the percentage of the working age population in the labor force. The participation rate is well below the 66% to 67% rate that was normal over the last 20 years, although most of the decline is due to demographics.

The Labor Force Participation Rate decreased to 63.8% in March (blue line). This is the percentage of the working age population in the labor force. The participation rate is well below the 66% to 67% rate that was normal over the last 20 years, although most of the decline is due to demographics.

The Employment-Population ratio decreased slightly to 58.5% in March (black line).

The third graph shows the job losses from the start of the employment recession, in percentage terms. The dotted line is ex-Census hiring.

The third graph shows the job losses from the start of the employment recession, in percentage terms. The dotted line is ex-Census hiring.

This shows the depth of the recent employment recession - much worst than any other post-war recession - and the relatively slow recovery due to the lingering effects of the housing bust and financial crisis.

This was weaker payroll growth than expected (expected was 201,000).

• ISM Manufacturing index indicates slightly faster expansion in March

PMI was at 53.4% in March, up from 52.4% in February. The employment index was at 56.1%, up from 53.2%, and new orders index was at 54.5%, down from 54.9%.

PMI was at 53.4% in March, up from 52.4% in February. The employment index was at 56.1%, up from 53.2%, and new orders index was at 54.5%, down from 54.9%. Here is a long term graph of the ISM manufacturing index.

This was slightly above expectations of 53.0%. This suggests manufacturing expanded at a faster rate in March than in February. It appears manufacturing employment expanded in March with the employment index at 56.1%.

• ISM Non-Manufacturing Index indicates slower expansion in March

The March ISM Non-manufacturing index was at 56.0%, down from 57.3% in February. The employment index increased in March to 56.7%, up from 55.7% in February. Note: Above 50 indicates expansion, below 50 contraction.

The March ISM Non-manufacturing index was at 56.0%, down from 57.3% in February. The employment index increased in March to 56.7%, up from 55.7% in February. Note: Above 50 indicates expansion, below 50 contraction. This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

This was below the consensus forecast of 56.7% and indicates slightly slower expansion in March than in February.

• U.S. Light Vehicle Sales at 14.4 million annual rate in March

Based on an estimate from Autodata Corp, light vehicle sales were at a 14.37 million SAAR in March. That is up 10.4% from March 2011, but down 4.4% from the sales rate last month (15.03 million SAAR in Feb 2012).

Based on an estimate from Autodata Corp, light vehicle sales were at a 14.37 million SAAR in March. That is up 10.4% from March 2011, but down 4.4% from the sales rate last month (15.03 million SAAR in Feb 2012).This graph shows light vehicle sales since the BEA started keeping data in 1967.

March was above the August 2009 rate with the spike in sales from "cash-for-clunkers". Only February had a higher sales rates since early 2008. This was below the consensus forecast of 14.7 million SAAR.

Even though this was below expectations, growth in auto sales will make another strong positive contribution to GDP in Q1 2012.

• Construction Spending declined in February

This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.

This graph shows private residential and nonresidential construction spending, and public spending, since 1993. Note: nominal dollars, not inflation adjusted.Private residential spending is 63.5% below the peak in early 2006, and up 10% from the recent low. Non-residential spending is 32% below the peak in January 2008, and up about 15% from the recent low.

Public construction spending is now 13% below the peak in March 2009.

The year-over-year improvement in private residential investment is an important change (the positive in 2010 was related to the tax credit), and this suggest the bottom is in for residential investment.

• Reis: Office, Mall and Apartment Vacancy Rates

Reis reported the apartment vacancy rate (82 markets) fell to 4.9% in Q1 from 5.2% in Q4 2011. The vacancy rate was at 6.1% in Q1 2010 and peaked at 8.0% at the end of 2009.

Reis reported the apartment vacancy rate (82 markets) fell to 4.9% in Q1 from 5.2% in Q4 2011. The vacancy rate was at 6.1% in Q1 2010 and peaked at 8.0% at the end of 2009.This graph shows the apartment vacancy rate starting in 1980 (prior to 1999 the data is annual). Back in the early '80s, there was overbuilding in the apartment sector (just like for offices) with the very loose lending that led to the S&L crisis. Once the lending stopped, starts of built-for-rent units slowed, and the vacancy rate started to decline.

Following the financial crisis, starts and completions of multi-family units fell to record lows (there were a record low number of completions last year). Builders have increased construction, but it usually takes over a year to complete a multi-family building, so this new supply hasn't reached the market yet. As Reis noted, the number of completions will increase this year, but the vacancy rate will probably decline further.

This will also impact on house prices. The upward pressure on rents will make the price-to-rent ratio a little more favorable for buying.

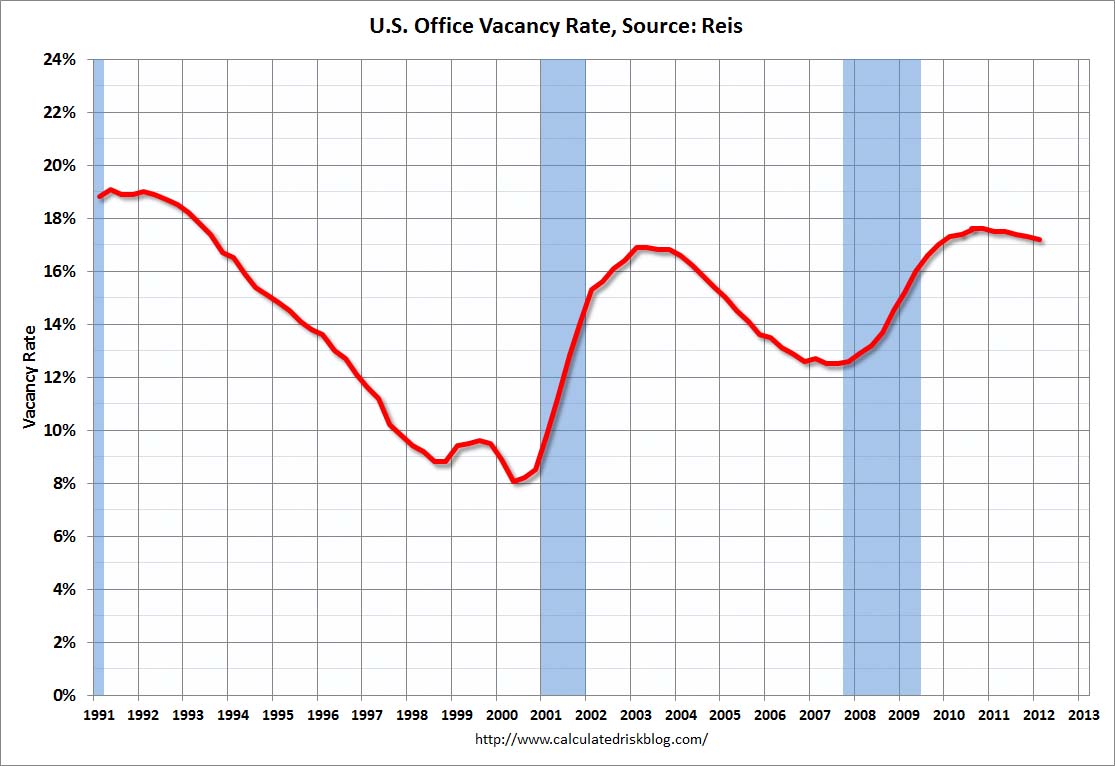

Reis reported the office vacancy rate declined slightly to 17.2% in Q1 from 17.3% in Q4 2011. The vacancy rate was at 17.6% in Q1 2011.

Reis reported the office vacancy rate declined slightly to 17.2% in Q1 from 17.3% in Q4 2011. The vacancy rate was at 17.6% in Q1 2011.This graph shows the office vacancy rate starting in 1980 (prior to 1999 the data is annual). Back in the early '80s, there was overbuilding in the office sector even as the vacancy rate was rising. This was due to the very loose lending that led to the S&L crisis.

In the '90s, office investment picked up as the vacancy rate fell. Following the bursting of the stock bubble, the vacancy rate increased sharply and office investment declined.

During the housing bubble, office investment started to increase even before the vacancy rate had fallen below 14%. This was due to loose lending - again. Investment essentially stopped following the financial crisis.

The good news is there is very little new office construction right now and the vacancy rate will probably continue to decline.

Ries reported the regional mall vacancy rate declined to 9.0% in Q1, and the strip mall vacancy rate declined to 10.9% from 11.0%.

Ries reported the regional mall vacancy rate declined to 9.0% in Q1, and the strip mall vacancy rate declined to 10.9% from 11.0%.This graph shows the vacancy rate for regional and strip malls since Q1 2000.

It appears the vacancy rate is starting to decline, but very slowly. Just like for office space, there is almost no new supply of malls being built.

• Weekly Initial Unemployment Claims decline to 357,000

The DOL reports:

The DOL reports:In the week ending March 31, the advance figure for seasonally adjusted initial claims was 357,000, a decrease of 6,000 from the previous week's revised figure of 363,000. The 4-week moving average was 361,750, a decrease of 4,250 from the previous week's revised average of 366,000.The previous week was revised up to 363,000 from 359,000.

The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims declined to 361,750.

The 4-week moving average is at the lowest level since early 2008.

• Other Economic Stories ...

• FOMC Minutes: No Push for QE3

• Federal Reserve Issues Statement on Rental of REOs

• Trulia announces new "mix adjusted" House Asking Price Monitor, Prices up 1.4% from Q4

• Ceridian-UCLA: Diesel Fuel index increased 0.3% in March

• ADP: Private Employment increased 209,000 in March

• LPS: February Foreclosure Starts and Sales Reversed Prior Month’s Increases

Friday, April 06, 2012

Stand-up economist Yoram Bauman: S*** happens: the economics version

by Calculated Risk on 4/06/2012 10:32:00 PM

Language warning on video below ...

Earlier Employment posts:

• March Employment Report: 120,000 Jobs, 8.2% Unemployment Rate

• Employment Summary and Discussion

• Construction Employment, Duration of Unemployment, Unemployment by Education and Diffusion Indexes

• All Employment Graphs

AAR: Rail Traffic "mixed" in March

by Calculated Risk on 4/06/2012 04:01:00 PM

From the Association of American Railroads (AAR): AAR Reports Mixed Rail Traffic for March

The Association of American Railroads (AAR) today reported reported U.S. rail carloads originated in March 2012 totaled 1,123,298, down 69,190 carloads or 5.8 percent, compared with March 2011. Intermodal volume in March 2012 was 928,350 containers and trailers, up 31,348 units or 3.5 percent compared with March 2011.

...

Commodities with carload declines in March were led by coal, down 84,854 carloads or 15.8 percent from March 2011. Other commodities with declines included grain, down 9,088 carloads or 9.7 percent; chemicals, down 4,278 carloads or 3.4 percent; nonmetallic minerals, down 1,863 carloads or 9.7 percent; and farm products excluding grain, down 479 carloads or 13.3 percent. Carloads excluding coal and grain were up 4.4 percent or 24,752 carloads in March 2012 over March 2011.

...

“There is no denying that coal is a crucial commodity for railroads, and there’s also no denying that recent declines in coal traffic are presenting significant challenges to railroads right now,” said AAR Senior Vice President John T. Gray. “That said, it’s encouraging that many commodities that are better indicators of the state of the economy than coal is — things like motor vehicles, lumber and wood products, and crushed stone — saw higher rail carloadings in March.”

Click on graph for larger image.

Click on graph for larger image.This graph shows U.S. average weekly rail carloads (NSA).

U.S. railroads originated 1,123,298 total carloads in March 2012, down 5.8% (69,190 carloads) from the same period in 2011. Total carloads averaged 280,825 per week in March 2012, down from 298,122 in March 2011. Coal and, to a lesser extent, grain were the main reasons for the decline. Excluding coal and grain, U.S. rail carloads were up 4.4% (24,752 carloads) in March 2012 over March 2011, though the 4.4% gain is the smallest gain for this category of rail traffic in six monthsAccording to the AAR, the decline in coal is because coal is being used less for electricity generation.

The second graph is for intermodal traffic (using intermodal or shipping containers):

Graphs reprinted with permission.

Graphs reprinted with permission.Intermodal traffic is now above the peak year in 2006.

Intermodal continued to impress in March. U.S. railroads originated 928,350 containers and trailers in March 2012, up 3.5% (31,348 units) over March 2011 and the 28th straight year-over-year monthly increase. Average weekly U.S. intermodal loadings in March 2012 were the highest of any March in history.

Earlier Employment posts:

• March Employment Report: 120,000 Jobs, 8.2% Unemployment Rate

• Employment Summary and Discussion

• Construction Employment, Duration of Unemployment, Unemployment by Education and Diffusion Indexes

• All Employment Graphs

Construction Employment, Duration of Unemployment, Unemployment by Education and Diffusion Indexes

by Calculated Risk on 4/06/2012 01:09:00 PM

The first graph below shows the number of total construction payroll jobs in the U.S. including both residential and non-residential since 1969.

Construction employment decreased by 7 thousand jobs in March, giving back some of the gains from January. Last year was the first year with an increase in construction employment since 2006, and the first with an increase in residential construction employment since 2005.

Unfortunately this graph is a combination of both residential and non-residential construction employment. The BLS only started breaking out residential construction employment fairly recently (residential specialty trade contractors in 2001).

Usually residential investment (and residential construction) leads the economy out of recession, and non-residential construction usually lags the economy. Because this graph is a blend, it masks the usual pickup in residential construction following previous recessions. Of course there was no pickup for residential construction this time because of the large excess supply of vacant homes - although that appears to be changing and residential construction employment will probably increase this year.

Click on graph for larger image.

Click on graph for larger image.

Construction employment is now generally increasing, and construction will add to both GDP and employment growth in 2012.

As I've noted for years, there are usually two bottoms for housing following a bubble: 1) when housing starts, new home sales, and residential construction bottoms, and 2) when house prices bottom. The bottom is in for construction and construction employment.

This graph shows the duration of unemployment as a percent of the civilian labor force. The graph shows the number of unemployed in four categories: less than 5 week, 6 to 14 weeks, 15 to 26 weeks, and 27 weeks or more.

This graph shows the duration of unemployment as a percent of the civilian labor force. The graph shows the number of unemployed in four categories: less than 5 week, 6 to 14 weeks, 15 to 26 weeks, and 27 weeks or more.All categories are generally moving down (the less than 5 week category is back to normal levels). The other categories are still high.

The the long term unemployed declined to 3.4% of the labor force - this is still very high, but the lowest since September 2009.

This graph shows the unemployment rate by four levels of education (all groups are 25 years and older).

This graph shows the unemployment rate by four levels of education (all groups are 25 years and older).Unfortunately this data only goes back to 1992 and only includes one previous recession (the stock / tech bust in 2001). Clearly education matters with regards to the unemployment rate - and it appears all four groups are generally trending down.

Note: This says nothing about the quality of jobs - as an example, a college graduate working at minimum wage would be considered "employed".

This is a little more technical. The BLS diffusion index for total private employment was at 59.6 in March, down slightly from 60.7 in January. For manufacturing, the diffusion index increased to 67.9, up from 59.9 in February.

This is a little more technical. The BLS diffusion index for total private employment was at 59.6 in March, down slightly from 60.7 in January. For manufacturing, the diffusion index increased to 67.9, up from 59.9 in February. Think of this as a measure of how widespread job gains are across industries. The further from 50 (above or below), the more widespread the job losses or gains reported by the BLS. From the BLS:

Figures are the percent of industries with employment increasing plus one-half of the industries with unchanged employment, where 50 percent indicates an equal balance between industries with increasing and decreasing employment.It appears job growth was still fairly widespread in March.

We'd like to see the diffusion indexes consistently above 60 - and even in the 70s like in the '1990s.

Earlier Employment posts:

• March Employment Report: 120,000 Jobs, 8.2% Unemployment Rate

• Employment Summary and Discussion

• All Employment Graphs

Employment Summary and Discussion

by Calculated Risk on 4/06/2012 10:17:00 AM

The number of payroll jobs added in March was disappointing, and this is reminding many observers of the slowdown in 2011.

But we also have to remember that this is just one month, and that there were clear reasons for the slowdown last year. In 2011, the economy was negatively impacted by the tsunami, bad weather, high oil prices and the debt ceiling debate. Of course oil prices are high again, but hopefully there will be no natural disasters, and also no threats of defaulting on the debt.

The report wasn't all bad news. It looks like the drag from state and local layoffs is nearing the end, the unemployment rate declined (although partially because of workers leaving the labor force), the number of people working part time for economic reasons declined, and the number of people unemployed for more than 6 months declined - and hourly wages increased a little faster.

Some numbers: There were 120,000 payroll jobs added in March, with 121,000 private sector jobs added, and 1,000 government jobs lost. The unemployment rate declined to 8.2%. U-6, an alternate measure of labor underutilization that includes part time workers and marginally attached workers, declined to 14.5% from 14.9% in February. This remains very high - U-6 was in the 8% range in 2007 - but this is the lowest level of U-6 since early 2009.

The participation rate decreased slightly to 63.8% (from 63.9%) and the employment population ratio also decreased slightly to 58.5%.

The change in January payroll employment was revised down from +284,000 to +275,000, and February was revised up from +227,000 to +240,000.

The average workweek declined 0.1 hours to 34.5 hours, and average hourly earnings increased 0.2%. "The average workweek for all employees on private nonfarm payrolls edged down by 0.1 hour to 34.5 hours in March. ... In March, average hourly earnings for all employees on private nonfarm payrolls rose by 5 cents, or 0.2 percent, to $23.39." This is sluggish earnings growth, and earnings are still being impacted by the large number of unemployed and marginally employed workers.

There are a total of 12.67 million Americans unemployed and 5.3 million have been unemployed for more than 6 months. These numbers are declining, but still very high.

Overall this report was disappointing, and this report will make the April report even more important as analysts try to determine if this is the beginning of slower growth - or if this was just a one month slowdown in hiring.

Percent Job Losses During Recessions

Click on graph for larger image.

Click on graph for larger image.

This graph shows the job losses from the start of the employment recession, in percentage terms - this time aligned at maximum job losses.

In the previous post, the graph showed the job losses aligned at the start of the employment recession.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:

The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) fell from 8.1 to 7.7 million over the month. These individuals were working part time because theirThe number of part time workers decreased sharply in March - and is back to 2008 levels - but this is still very high.

hours had been cut back or because they were unable to find a full-time

job.

These workers are included in the alternate measure of labor underutilization (U-6) that declined to 14.5% in March from 14.9% in February - the lowest level since early 2009.

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 5.308 million workers who have been unemployed for more than 26 weeks and still want a job. This was down from 5.426 million in February. This is very high, but this is the lowest number since 2009.

More graphs coming ...

March Employment Report: 120,000 Jobs, 8.2% Unemployment Rate

by Calculated Risk on 4/06/2012 08:30:00 AM

From the BLS:

Nonfarm payroll employment rose by 120,000 in March, and the unemployment rate was little changed at 8.2 percent, the U.S. Bureau of Labor Statistics reported today.This graph shows the jobs added or lost per month (excluding temporary Census jobs) since the beginning of 2008.

...

The civilian labor force participation rate (63.8 percent) and the employment-population ratio (58.5 percent) were little changed in March.

...

The change in total nonfarm payroll employment for January was revised from

+284,000 to +275,000, and the change for February was revised from +227,000

to +240,000.

Click on graph for larger image.Job growth started picking up early last year, but then the economy was hit by a series of shocks (oil price increase, tsunami in Japan, debt ceiling debate) - and then growth started picking up again. This is only one month, but the concern is job growth will slow again.

The second graph shows the employment population ratio, the participation rate, and the unemployment rate. The unemployment rate was declined to 8.2% (red line).

The Labor Force Participation Rate decreased to 63.8% in March (blue line). This is the percentage of the working age population in the labor force. The participation rate is well below the 66% to 67% rate that was normal over the last 20 years, although most of the decline is due to demographics.The Employment-Population ratio decreased slightly to 58.5% in March (black line).

The third graph shows the job losses from the start of the employment recession, in percentage terms. The dotted line is ex-Census hiring.This shows the depth of the recent employment recession - much worst than any other post-war recession - and the relatively slow recovery due to the lingering effects of the housing bust and financial crisis.

This was weaker payroll growth than expected (expected was 201,000). More later ...

Reis: Strip Mall Vacancy Rate declines slightly in Q1

by Calculated Risk on 4/06/2012 12:44:00 AM

From Reuters: US strip-mall vacancy falls 1st time in 7 yrs

The average vacancy rate at U.S. strip malls fell for the first time in nearly seven years in the first quarter and rents inched up, but it is too early to call a rebound for a sector battered by the housing bust and recession, a report by Reis Inc showed.

During the first quarter, the national vacancy rate for strip malls fell to 10.9 percent from 11 percent the prior quarter, according to preliminary figures from Reis. ... "This is really only the first quarter where the vacancy rate declined. We need to see something a little bit more sustained than just a quarter or two before it really signals the beginning of a trend," Severino said.

...

At regional malls, the first-quarter vacancy rate fell to 9 percent from 9.2 percent the prior quarter. It was the second consecutive quarterly decline for the big malls.

Click on graph for larger image.This graph shows the vacancy rate for regional and strip malls since Q1 2000.

It appears the vacancy rate is starting to decline, but very slowly. Just like for office space, there is almost no new supply of malls being built.

Thursday, April 05, 2012

Existing Home Inventory declines 20% year-over-year in early April

by Calculated Risk on 4/05/2012 09:33:00 PM

Another update: I've been using inventory numbers from HousingTracker / DeptofNumbers to track changes in inventory. Tom Lawler mentioned this last year.

According to the deptofnumbers.com for (54 metro areas), inventory is off 20.4% compared to the same week last year. Unfortunately the deptofnumbers only started tracking inventory in April 2006.

This graph shows the NAR estimate of existing home inventory through February (left axis) and the HousingTracker data for the 54 metro areas through early April.

Click on graph for larger image.

Click on graph for larger image.

Since the NAR released their revisions for sales and inventory, the NAR and HousingTracker inventory numbers have tracked pretty well.

Seasonally housing inventory usually bottoms in December and January and then starts to increase again through mid to late summer. So seasonally inventory should increase over the next several months.

The second graph shows the year-over-year change in inventory for both the NAR and HousingTracker.

HousingTracker reported that the early April listings - for the 54 metro areas - declined 20.4% from the same period last year. The year-over-year decline will probably start to slow since listed inventory is getting close to normal levels. Also if there is an increase in foreclosures (as expected), this will slow the year-over-year decline.

HousingTracker reported that the early April listings - for the 54 metro areas - declined 20.4% from the same period last year. The year-over-year decline will probably start to slow since listed inventory is getting close to normal levels. Also if there is an increase in foreclosures (as expected), this will slow the year-over-year decline.

This is just inventory listed for sale, there is also a large "shadow inventory" that is currently not on the market, but is expected to be listed in the next few years. But this year-over-year decline remains a significant story.

Federal Reserve Issues Statement on Rental of REOs

by Calculated Risk on 4/05/2012 05:20:00 PM

This statement makes it clear that the Fed (and probably other regulators) will allow banks to rent residential Real Estate Owned (REO) for longer periods due to market conditions. I expect we will see more rental programs like the pilot program recently announced by BofA.

From the Federal Reserve:

The Federal Reserve Board on Thursday released a policy statement reiterating that statutes and Federal Reserve regulations permit rental of residential properties acquired in foreclosure as part of an orderly disposition strategy. The statement also outlines supervisory expectations for residential rental activities.Here is the statement.

The general policy of the Federal Reserve is that banking organizations should make good faith efforts to dispose of foreclosed properties (also known as "other real estate owned" or "OREO"), including single-family homes, at the earliest practicable date. In this context, and in light of the extraordinary market conditions that currently prevail, the policy statement explains that banking organizations may rent residential OREO properties within legal holding-period limits without demonstrating continuous active marketing of the property for sale, provided that suitable policies and procedures are followed.

Moreover, to the extent that OREO rental properties meet the definition of community development under the Community Reinvestment Act (CRA) regulations, the banking organizations would receive favorable CRA consideration. In all respects, banking organizations that rent OREO properties are expected to comply with all applicable federal, state, and local statutes and regulations, some of which the policy statement highlights. The policy statement, in providing guidance to banking organizations and examiners, also describes specific supervisory expectations for banking organizations with a larger number of rental OREO properties, generally more than 50 properties available for rent or rented.

The policy statement applies to banking organizations for which the Federal Reserve is the primary federal supervisor, including state member banks, bank holding companies, non-bank subsidiaries of bank holding companies, savings and loan holding companies, non-thrift subsidiaries of savings and loan holding companies, and U.S. branches and agencies of foreign banking organizations.

Employment Situation Preview

by Calculated Risk on 4/05/2012 02:55:00 PM

Tomorrow (Friday) the BLS will release the March Employment Situation Summary at 8:30 AM ET. Bloomberg is showing the consensus is for an increase of 201,000 payroll jobs in March, and for the unemployment rate to remain unchanged at 8.3%.

Note:

• The weather was mild in January and February, and it is possible that some hiring was pulled forward. Several analysts have pointed out that the BLS reported that few people were "not at work due to bad weather" in January and February. I looked back at previous years with mild weather (using the BLS "not at work, bad weather" measurement), and employment gains in March were solid following mild weather during January and February. So I don't expect much payback due to the weather.

• The economic questions for tomorrow (see pickem game on top right sidebar) is to take the over or under on the consensus for payroll jobs and to forecast the unemployment rate.

Here is a summary of recent data:

• The ADP employment report showed an increase of 209,000 private sector payroll jobs in March. Although ADP seems to track the BLS over time, the ADP report hasn't been very useful in predicting the BLS report. Also note that government payrolls declined by about 18,000 over the last three months (about 6,000 per month), so the ADP report suggests 209,000 private nonfarm payroll jobs added, minus 6,000 government workers - or around 203,000 total jobs added in March (close to the consensus).

• The ISM manufacturing employment index increased to 56.1% from 53.2% in February. A historical correlation between the ISM index and the BLS employment report for manufacturing, suggests that private sector BLS reported payroll jobs for manufacturing increased about 14,000 in March.

The ISM service employment index increased to 56.7% from 55.7% in March. Based on a historical correlation between the ISM non-manufacturing employment index and the BLS employment report for service, this reading suggests the gain of around 240,000 private payroll jobs for services in March.

Combined the ISM surveys suggest an employment report somewhat above the consensus.

• Initial weekly unemployment claims averaged about 366,000 in March, down slightly from 374,000 average in January and February.

For the BLS reference week (includes the 12th of the month), initial claims were at about the same level as in January and February when the economy added 284,000 and 227,000 payroll jobs respectively.

• The final March Reuters / University of Michigan consumer sentiment index increased to 76.2, up slightly from the February reading of 75.3. This is frequently coincident with changes in the labor market, but also strongly related to gasoline prices and other factors. This suggests a weak but improving labor market.

• And a little optimism from the NFIB (small business): NFIB Jobs Statement: Job Creation Shows Mixed Signals

“March came in like a lion on the job-front, but went out tempered by future job growth indicators. Overall, the March survey anticipates some strength in the job creation number with little change in the unemployment rate. With job openings and plans for job creation both falling, prospects for a surge in job creation in the small business sector are still not promising.The participants in the NFIB surveys still aren't doing much hiring, however the small business index from Intuit showed 65,000 small business jobs created in March.

Building on February’s increased jobs numbers, March’s survey gives us the best readings since January and February of 2011. The net change in employment per firm (seasonally adjusted) was 0.22, double the reading for February.

• And on the unemployment rate from Gallup: U.S. Unemployment Declines in March

U.S. unemployment, as measured by Gallup without seasonal adjustment, declined to 8.4% in March from 9.1% in February, while Gallup's seasonally adjusted rate fell to 8.1% from 8.6% in February.NOTE: The Gallup poll results are Not Seasonally Adjusted (NSA), so use with caution.

...

Gallup's monitoring of the unemployment situation includes the entire month, while the BLS uses a mid-month reference week.

Gallup's seasonally adjusted unemployment rate was essentially unchanged at 8.5% in mid-March from 8.6% in February, but then fell to 8.1% for all of March. How much of the sharp decline in unemployment during the second half of March will be picked up in the government's mid-month reference week is unclear.

There always seems to be some randomness to the employment report, but the overall situation has improved (lower initial weekly unemployment claims, more job openings). The ADP report suggests the consensus is close, and the ISM reports suggest the consensus is a little low.

Once again I'll take the over (above 201,000 payroll jobs), and I think a further decline in the unemployment rate is possible (this depends on the participation rate and if discouraged workers return to the labor force).

More: Office Vacancy Rate declines slightly to 17.2% in Q1

by Calculated Risk on 4/05/2012 12:43:00 PM

Early this morning I noted that Reis reported the office vacancy rate declined slightly to 17.2% in Q1 from 17.3% in Q4 2011. The vacancy rate was at 17.6% in Q1 2011.

Here are a few more comments and a long term graph from Reis.

Comments from Reis Senior Economist Ryan Severino:

National vacancies continued falling at a very modest pace in the first quarter, mirroring the tepid improvement in the labor market. The sector absorbed 5.998 million SF, the fifth consecutive quarterly gain in occupied stock since the beginning of 2011.

Although net absorption levels remain muted, five consecutive quarters of positive net absorption provide convincing evidence that the sector is indeed recovering. ... Given the rate of improvement that the sector is experiencing, it will be years before it is able to recover the space that was vacated during the recession and early stages of the economic recovery. The national vacancy rate has regressed back to levels unseen since 1993 and remains well above the cyclical low of 12.5% from 2007 before the onset of the recession.

...

National asking and effective rent growth improved slightly in the first quarter, continuing the slow upward trend that began in the first quarter of 2011. Annual gains of 1.6 and 2.1 percent, respectively, also indicate a moderate pace of improvement, but are unimpressive.

...

Weak supply growth remains a tailwind for improvement in the office sector. During the first quarter of 2012 only 1.917 million square feet of office space were completed. This represents the lowest quarterly level on record since Reis began tracking quarterly market data in 1999. ... With little supply being delivered, even the low levels of absorption that we are observing are sufficient enough to generate vacancy rate declines and rent growth.

Click on graph for larger image.This graph shows the office vacancy rate starting in 1980 (prior to 1999 the data is annual). Back in the early '80s, there was overbuilding in the office sector even as the vacancy rate was rising. This was due to the very loose lending that led to the S&L crisis.

In the '90s, office investment picked up as the vacancy rate fell. Following the bursting of the stock bubble, the vacancy rate increased sharply and office investment declined.

During the housing bubble, office investment started to increase even before the vacancy rate had fallen below 14%. This was due to loose lending - again. Investment essentially stopped following the financial crisis.

The good news is, as Severino noted, there is very little new office construction right now and the vacancy rate will probably continue to decline.

Office vacancy data courtesy of Reis.

Trulia announces new "mix adjusted" House Asking Price Monitor, Prices up 1.4% from Q4

by Calculated Risk on 4/05/2012 10:00:00 AM

This is an interesting new asking price monitor from Trulia. Usually people report median asking prices, but unfortunately the median is impacted by the mix of homes. However Trulia adjusts the asking prices both for the mix of homes listed for sale and for seasonal factors. Of course this is just asking prices, not sales prices, but this might provide an early hint at changes in house prices.

This has the advantage of giving a much earlier look at prices than the repeat sales indexes. As an example, the recent Case-Shiller report was for "January". But that was really a three month average of November, December and January - and the index is based on recorded closing prices - so some of this index was based on contracts signed last September. That is 6 or even 7 months ago.

The Trulia monitor will be released monthly, and the report today is for asking prices in March.

From Trulia:

Trulia today launched the Trulia Price Monitor and the Trulia Rent Monitor, the earliest leading indicators available of trends in home prices and rents. Based on the for-sale homes and rentals listed on Trulia.com, these Monitors take into account changes in the mix of listed homes, reflecting trends in prices and rents for similar homes in similar neighborhoods through March 31, 2012.

Nationally, asking prices on for-sale homes – which lead sales prices by approximately two or more months – were 1.4 percent higher in March than one quarter ago. Prices increased month over month 0.9 percent in March and 0.6 percent in February. The Trulia Price Monitor is seasonally adjusted, so these monthly and quarterly increases are on top of typical springtime price jumps. Unadjusted for seasonality, asking prices rose 2.4 percent quarter over quarter. According to the Monitor, asking prices had been declining prior to February and reached a low in January.

...

“Asking prices rose in February and March, but this doesn’t mean that the bottom is forever behind us. The robo-signing settlement will accelerate the foreclosure process, pushing more homes onto the market and dragging down prices in areas that suffered most from the housing crash,” said Jed Kolko, Trulia’s Chief Economist.

Click on graph for larger image.

Click on graph for larger image.The first graph from Trulia shows the month over month prices changes (seasonally adjusted) as reported by the monitor. This shows asking prices were falling for most of 2011, but have turned up in early 2012.

Here is a list of price and rent changes for the 100 largest metro areas.

And here is a map from Trulia showing the year-over-year change in asking prices.

And here is a map from Trulia showing the year-over-year change in asking prices.On a year-over-year basis many MSAs are still in the red (as opposed to quarter-over-quarter or month-over-month). According to the list of cities, 41 MSAs (out of 100) had increasing asking prices year-over-year, and 67 quarter-over-quarter.

There are still many more distressed sales to come, and asking prices could turn down again - but this does suggest prices have turned up recently.

Weekly Initial Unemployment Claims decline to 357,000

by Calculated Risk on 4/05/2012 08:30:00 AM

The DOL reports:

In the week ending March 31, the advance figure for seasonally adjusted initial claims was 357,000, a decrease of 6,000 from the previous week's revised figure of 363,000. The 4-week moving average was 361,750, a decrease of 4,250 from the previous week's revised average of 366,000.The previous week was revised up to 363,000 from 359,000.

The following graph shows the 4-week moving average of weekly claims since January 2000.

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims declined to 361,750.

The 4-week moving average is at the lowest level since early 2008 (including revisions).

And here is a long term graph of weekly claims:

Slow and steady improvement. This is the lowest level for claims since early 2008.

Reis: Office Vacancy Rate declines slightly in Q1 to 17.2%

by Calculated Risk on 4/05/2012 12:22:00 AM

From Reuters: Sluggish job growth crimps US office market rebound

The national vacancy rate slipped to 17.2 percent in the first quarter, a slight improvement from 17.3 percent in the 2011 fourth quarter, according to preliminary figures from Reis. A year earlier the vacancy rate was 17.6 percent. ... The national vacancy rate has risen to levels not seen since 1993 and remains well above the cyclical low of 12.5 percent posted in 2007 ...

The average U.S. office asking rent rate rose to $28.10 per square foot in the first quarter, up 0.5 percent from the 2011 fourth quarter. ...

Overall, the national office market has posted five quarters of improvement, leading Reis to believe the market is in the midst of a slow recovery. ... "The lack of new supply has been the saving grace for the office sector," Severino said. "The levels of demand that we're seeing right now, while they're positive, they're not really significant. It pales in comparison with cycles past."

Click on graph for larger image.

Click on graph for larger image.This graph shows the office vacancy rate starting in 1991.

Reis is reporting the vacancy rate declined to 17.2% in Q1, down from 17.3% in Q4. The vacancy rate was at a cycle high of 17.6% in Q3 and Q4 2010. It appears the office vacancy rate peaked in 2010 and is declining very slowly.

As Reis noted, there are very few new office buildings being built in the US, and new construction will probably stay low for several years.

Wednesday, April 04, 2012

Jamie Dimon's "Brain Freeze" and Comments on Housing

by Calculated Risk on 4/04/2012 08:27:00 PM

The WSJ has JPM CEO Jamie Dimon's letter to shareholders (ht Brian) A couple of excerpts:

I suspect that the mortgage crisis will be the worst financial catastrophe of our lifetime. What the world experienced was almost a collective brain freeze ... It was a disaster hidden by rising home prices and false expectations, and once that price bubble burst, we all were in trouble.Some people didn't experience a "brain freeze", but unfortunately most lenders did. I think lender's will forget again, but hopefully not for some time.

We need to write a letter to the next generation that says, “Never forget: 80% loan to value and verify appropriate income.”

...

But [JP Morgan] did participate in this disaster by originating mortgages that wouldn’t have been given a decade earlier (and won’t be given a decade later).

And on housing:

There has been a tremendous focus on the fact that housing prices remain depressed and, in fact, are still going down some. The large “shadow inventory” of homes in delinquency or foreclosure that has not yet hit the sale market adds to the fears that this will continue for a long time. New home construction still is very depressed – so, to most, the future looks bleak. However, if one looks at the leading indicators, all signs are flashing green – the turn is coming if it is not here already. We don’t want to be blindly optimistic, but the facts are the facts:

• America has never stopped growing. The United States has added 3 million people a year since the crisis began four years ago. We will add 30 million people in the next 10 years.

• This population growth normally would create a need for 1.2 million additional housing units each year. Household formation has been half of that for the past four years. Our economists believe that there is huge pent-up demand and that household formation will return to 1.2 million a year as job conditions improve.

• Job conditions have been improving, albeit slowly. In the last 24 months, 3.45 million jobs have been created.

• On average, only 845,000 new U.S. housing units were built annually over the last four years – and the destruction of homes from demolition, disaster and dilapidation has averaged 250,000 a year. The growth of new households, even at a reduced rate, has been able to absorb all of this new supply, and more. [CR note: I wonder about the source for the number of homes demolished?]

• The total inventory of single-family homes and condos for sale currently is 2.7 million units, down from a peak of 4.4 million units in May 2007. It now would take only six months to sell all of the houses for sale at existing sales rates, down from 12 months two years ago. (This low of an inventory number normally would be considered a positive sign for future housing prices.)

• While the shadow inventory mentioned above still is significant, it has shown a visible declining trend since peaking at the end of 2009, when the number of loans delinquent 90+ days or in foreclosure was 5.1 million homes. It now totals 3.9 million, and we estimate it could be 3 million in 12 months. The shadow inventory also may move more quickly as mortgage servicers get better at packaged sales and short sales and as real money investors start to buy foreclosed homes and rent them out for a good profit. Home prices still are going down a little bit, and they will stay depressed for a while. Distressed sales (short sales, foreclosure sales, real estate-owned sales) still are 25% of all sales, and these sales typically are priced 30% lower than non-distressed sales. As the percentage of distressed sales comes down over the next 12-24 months, their negative effect on housing prices will start to diminish.

...

• It now is cheaper to buy than to rent in half of the markets in America – this has not been true for more than 15 years. Relatively high rental prices can be a precursor to increasing home prices.

• At the same time, American consumers are finding more solid financial footing relative to their debt. The household debt service ratio, which is the ratio of mortgage plus consumer debt payments to disposable personal income, stands at its lowest level since 1994. This is a result of rapid consumer deleveraging – household mortgage debt now is down $1 trillion from its 2008 peak. (Reported U.S. mortgage data do not remove mortgage debt from an individual’s debt obligations until there is an actual foreclosure. It is estimated that $600 billion of the $9 trillion in currently outstanding mortgage debt is not paying interest today and effectively could be removed now from these numbers.)

• Recent senior loan officer surveys by the Federal Reserve show that, while there are not yet clear signs of credit loosening for new mortgages, at least the rush to tighten mortgage lending standards has abated.

...

More jobs, more households, more Americans, good value – it’s just a matter of time.

FHFA's DeMarco: FHFA to make decision on GSE Principal Reductions this month

by Calculated Risk on 4/04/2012 04:50:00 PM

From a speech today by FHFA acting director Edward DeMarco:

On a nationwide basis, Fannie Mae and Freddie Mac own or guarantee 60 percent of the mortgages outstanding, but they account for only 29 percent of seriously delinquent loans, obviously a much lower proportion than their share of the market.CR Note: I'd like to see the data on "payment reduction, not loan-to-value, is the key indicator of success in loan modifications".

Even though the Enterprises have a smaller share of seriously delinquent loans than other market participants, they account for just over half of all Home Affordable Modification Program, or HAMP modifications. Between HAMP modifications and their own proprietary loan modifications, Fannie Mae and Freddie Mac have completed more than 1.1 million loan modifications since the fourth quarter of 2008.

It has been well-publicized that there is one form of loan modification that FHFA has not embraced, that being principal forgiveness. To be clear, the disagreement is not about helping borrowers. FHFA, with the Enterprises, has been making great efforts to assist troubled homeowners with underwater mortgages who have the ability to make a mortgage payment and a willingness to do so. While we are currently evaluating the recent Treasury changes to HAMP regarding principal forgiveness, I would like to explain the position we have taken to date.

The fundamental point of a loan modification is to adjust the borrower’s monthly payment to an affordable level. We have seen repeatedly that what matters most in successfully helping borrowers is a meaningful reduction in the monthly payment to an amount that helps stabilize the family’s finances. Indeed, we have found that payment reduction, not loan-to-value, is the key indicator of success in loan modifications.

For many underwater borrowers, we achieve this by forbearing on principal – that is, charging a zero rate of interest on the forbearance amount and deferring its repayment. This focus on making the monthly mortgage payment affordable is an efficient way to provide assistance to the borrower and keep them in their home. If the borrower remains successful in this modified loan, this approach preserves for taxpayers an ultimate recovery on the debt.

Stated differently, the principal forbearance mod being used by Fannie Mae and Freddie Mac produces the same, lower monthly payment as a modification based on principal forgiveness. If the borrower ends up defaulting even with the modification, the loss to the taxpayer is the same either way. But if the borrower is successful, the taxpayer retains the opportunity to benefit from the upside – a reasonable deal given the support the taxpayer has provided to assist the family in keeping their home.

Moreover, this approach recognizes that three out of every four deeply underwater borrowers in Fannie Mae’s and Freddie Mac’s book of business today are current on their loans. These borrowers are demonstrating a continued willingness to meet their mortgage obligations. This should be recognized and encouraged, not dampened with incentives for people to not continue paying. As I have stated previously, we are currently evaluating the recent Treasury Department proposal to HAMP regarding principal forgiveness and expect a decision this month.

DeMarco makes a key point that "three out of every four deeply underwater borrowers in Fannie Mae’s and Freddie Mac’s book of business today are current on their loans". The key problem with a principal reduction program is that even if it makes sense for an individual borrower, it might not makes sense overall if a large number of current borrowers decide to default hoping for a principal reduction.

One way around this problem - that has been effective for some banks - is to sell underwater loans to a 3rd party, and let them do the principal reduction. Since the biggest risk is that the word gets out, and everyone underwater stops making payments, selling to a 3rd party allows the bank (or GSE) to say they don't do principal reductions, but they would still get most of the benefit (with some shared with the 3rd party).

It sounds like the FHFA will make a decision this month. I hope they release the internal studies first.