RSS Feed

RSS Feed by Calculated Risk on 7/16/2011 06:02:00 PM

Saturday, July 16, 2011

Schedule for Week of July 17th

Earlier:

• Summary for Week Ending July 15th

Three key housing reports will be released this week: July homebuilder confidence on Monday, June housing starts on Tuesday, and June existing home sales on Wednesday.

The Philly Fed manufacturing survey will be released on Thursday. Also the speech by NY Fed VP Brian Sack on Wednesday might be interesting.

10 AM ET: The July NAHB homebuilder survey. The consensus is for a reading of 14, up slightly from 13 in June. Any number below 50 indicates that more builders view sales conditions as poor than good. This index has been below 25 for four years.

8:30 AM: Housing Starts for June. After collapsing following the housing bubble, housing starts have mostly been moving sideways for over two years - with slight ups and downs due to the home buyer tax credit.

8:30 AM: Housing Starts for June. After collapsing following the housing bubble, housing starts have mostly been moving sideways for over two years - with slight ups and downs due to the home buyer tax credit. Total housing starts were at 560 thousand (SAAR) in May, up 3.5% from the revised April rate of 541 thousand. Single-family starts increased 3.7% to 419 thousand in May.

The consensus is for an increase to 575,000 (SAAR) in June.

Early: The AIA's Architecture Billings Index for June (a leading indicator for commercial real estate).

Early: The AIA's Architecture Billings Index for June (a leading indicator for commercial real estate).This graph shows the Architecture Billings Index since 1996. The index decreased in May to 47.2 from 47.6 in April. Anything below 50 indicates a decrease in billings.

This index usually leads investment in non-residential structures (hotels, malls, office) by 9 to 12 months.

7:00 AM: The Mortgage Bankers Association (MBA) will release the mortgage purchase applications index. This index has been very weak over the last couple months suggesting weak home sales through summer (not counting all cash purchases).

10:00 AM: Existing Home Sales for June from the National Association of Realtors (NAR). The consensus is for sales of 4.9 million at a Seasonally Adjusted Annual Rate (SAAR) in June, up from 4.81 million SAAR in May.

10:00 AM: Existing Home Sales for June from the National Association of Realtors (NAR). The consensus is for sales of 4.9 million at a Seasonally Adjusted Annual Rate (SAAR) in June, up from 4.81 million SAAR in May.Note: the NAR is working on benchmarking existing home sales for previous years with other industry data (expectations are for large downward revisions). Perhaps the NAR will provide an update on when these revisions will be released.

Expected: The Moody's/REAL Commercial Property Price Indices (commercial real estate price index) for May.

6:15 PM: NY Fed Vice President Brian Sack speaks before the Money Marketeers of New York University.

8:30 AM: The initial weekly unemployment claims report will be released. The number of claims has been elevated for the last couple of months. The consensus is for an increase to 415,000 from 405,000 last week.

10:00 AM: Philly Fed Survey for July. The consensus is for a reading of 5.0 (above zero indicates expansion), up from -7.7 last month.

10:00 AM: Conference Board Leading Indicators for June. The consensus is for a flat reading for this index.

10:00 AM: FHFA House Price Index for May 2011. This is based on GSE repeat sales and is no longer as closely followed as Case-Shiller (or CoreLogic).

10:00 AM: Fed Chairman Ben Bernanke on the Dodd-Frank Act, Before the Committee on Banking, Housing, and Urban Affairs, U.S. Senate.

10:00 AM: Regional and State Employment and Unemployment for June 2011

Summary for Week Ending July 15th

by Calculated Risk on 7/16/2011 11:09:00 AM

Last week was filled with disappointing data. So much so that Goldman Sachs downgraded their forecast last night:

Following another week of weak economic data, we have cut our estimates for real GDP growth in the second and third quarter of 2011 to 1.5% and 2.5%, respectively, from 2% and 3.25%. Our forecasts for Q4 and 2012 are under review, but even excluding any further changes we now expect the unemployment rate to come down only modestly to 8¾% at the end of 2012.Before we get to the data, there were a couple other key stories last week: 1) the European bank stress tests disappointed most analysts (only a few banks were required to raise capital, see from the Financial Times: Banks’ stress test pass rate under fire), and 2) the debt ceiling negotiations continued, although this appears to be almost over (see: Debt Ceiling Charade: Almost Over).

The main reason for the downgrade is that the high-frequency information on overall economic activity has continued to fall substantially short of our expectations.

...

One key question in coming months is whether final demand recovers to the 2%-2½% pace that is probably necessary to keep GDP growth near trend and prevent the unemployment rate from rising more noticeably.

• Retail Sales increased 0.1% in June

On a monthly basis, retail sales increased 0.1% from May to June (seasonally adjusted, after revisions), and sales were up 8.1% from June 2010.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales have been mostly moving sidways since March.

Retail sales are up 16.6% from the bottom, and now 2.5% above the pre-recession peak.

This was about at expectations for no change in retail sales. Retail sales ex-autos were unchanged, and gas station sales declined 1.3% last month as prices fell. Another weak retail sales report ...

• Trade Deficit increased sharply in May to $50.2 billion

The Department of Commerce reports:

[T]otal May exports of $174.9 billion and imports of $225.1 billion resulted in a goods and services deficit of $50.2 billion, up from $43.6 billion in April, revised. May exports were $1.0 billion less than April exports of $175.8 billion. May imports were $5.6 billion more than April imports of $219.4 billion.

Exports decreased in May and imports increased (seasonally adjusted). Exports are well above the pre-recession peak and up 15% compared to May 2010; imports are almost back to the pre-recession peak, and up about 16% compared to May 2010.

Exports decreased in May and imports increased (seasonally adjusted). Exports are well above the pre-recession peak and up 15% compared to May 2010; imports are almost back to the pre-recession peak, and up about 16% compared to May 2010.The petroleum deficit increased in May as both prices and the quantity of oil imported increased. Oil averaged $108.70 per barrel in May, up from $103.18 per barrel in April, and up from $76.95 in May 2010. There is a bit of a lag with prices, and import prices will probably be a little lower in June.

The trade deficit with China increased to $24.96 billion (NSA), so once again the deficit is mostly oil and China.

• Industrial Production increased 0.2% in June, Capacity Utilization unchanged

From the Fed: Industrial production and Capacity Utilization

From the Fed: Industrial production and Capacity Utilization This graph shows Capacity Utilization. This series is up 9.4 percentage points from the record low set in June 2009 (the series starts in 1967).

Capacity utilization at 76.7% is still "3.7 percentage points below its average from 1972 to 2010" - and below the pre-recession levels of 81.2% in November 2007.

Industrial production increased in June to 93.1.

Industrial production increased in June to 93.1.Both industrial production and capacity utilization have been moving sideways recently. This was below the consensus forecast of a 0.4% increase in Industrial Production in June, and an increase to 76.9% for Capacity Utilization.

The suggests there is still significant excess industrial capacity.

• NFIB: Small Business Optimism Index "basically unchanged" in June

From the National Federation of Independent Business (NFIB): Small Business Optimism Stagnates

This graph shows the small business optimism index since 1986. The index decreased to 90.8 in June from 90.9 in May.

This graph shows the small business optimism index since 1986. The index decreased to 90.8 in June from 90.9 in May.This index is still very low - and had been trending up - but optimism has declined for four consecutive months now.

This graph shows the net hiring plans for the next three months.

Hiring plans increased in June and this is the highest level since February.

Hiring plans increased in June and this is the highest level since February.According to NFIB: “Although June’s employment growth was weak, 15 percent (seasonally adjusted) of small firms reported unfilled job openings, a 3 point increase and an indication that the unemployment rate will ease back below 9 percent in the coming months. "

Weak sales is still the top business problem with 24 percent of the owners reporting that weak sales continued to be their top business problem in June.

• Ceridian-UCLA: Diesel Fuel index increased in June

Press Release: Pulse of Commerce Index Rebounds – Up 1.0 Percent In June

Press Release: Pulse of Commerce Index Rebounds – Up 1.0 Percent In JuneThis graph shows the index since January 2000.

This index has mostly been moving sideways all year. As Leamer noted, this "could be the start of a positive trend, but a one month spike does not make a trend, particularly in light of the many false starts experienced over the last year."

• Consumer Sentiment declines sharply in July

The preliminary July Reuters / University of Michigan consumer sentiment index declined sharply to 63.8 from 71.5 in June.

In general consumer sentiment is a coincident indicator and is usually impacted by employment (and the unemployment rate) and gasoline prices. However, even with lower gasoline prices, consumer sentiment declined sharply - possible because of the heavy coverage of the debt ceiling charade.

In general consumer sentiment is a coincident indicator and is usually impacted by employment (and the unemployment rate) and gasoline prices. However, even with lower gasoline prices, consumer sentiment declined sharply - possible because of the heavy coverage of the debt ceiling charade.This was well below the consensus forecast of 71.0 and definitely in the recession range.

• Other Economic Stories ...

• AAR: Rail Traffic soft in June

• BLS: Job Openings unchanged in May

• NY Fed: Empire State Survey indicates contraction

• Key Measures of Inflation ease in June

• Eight Banks Fail European Stress Tests

Have a great weekend!

Unofficial Problem Bank list declines to 995 Institutions

by Calculated Risk on 7/16/2011 08:27:00 AM

Note: this is an unofficial list of Problem Banks compiled only from public sources.

There is the unofficial problem bank list for July 15, 2011.

Changes and comments from surferdude808:

It was an active week for the Unofficial Problem Bank List with 11 removals and two additions. The net result of the changes leave the list at 995 institutions with assets of $416.2 billion, down from 1,004 institutions and assets of $418.8 billion last week.

Among the removals are five cures, four failures, and two unassisted mergers. Actions were terminated against Intercredit Bank, National Association, Miami, FL ($258 million); Heritage Bank National Association, Spicer, MN ($170 million); The American National Bank of Beaver Dam, Beaver Dam, WI ($110 million); Gibraltar Bank, Oak Ridge, NJ ($95 million); and The First National Bank of Cold Spring, Cold Spring, MN ($74 million). The four failures are First Peoples Bank, Port Saint Lucie ($228 million Ticker: FPBI); High Trust Bank, Stockbridge, GA ($193 million); One Georgia Bank, Atlanta, GA ($186 million); and Summit Bank, Prescott, AZ ($72 million). The removals from unassisted merger are Cascade Bank, Everett, WA ($1.5 billion); and Bank of Greensburg, Greensburg, LA ($92 million). Long time readers may remember the less than forthright conversations we had with Cascade Bank about it becoming subject to an enforcement action. Still we are happy to see them migrate off the list without failing.

The two additions this week are Mission National Bank, San Francisco, CA ($1984 million Ticker: MNBO); and Traders National Bank, Tullahoma, TN ($156 million).

This message was posted on the OTS enforcement web page "On July 21, 2011, the Office of Thrift Supervision will become part of the Office of the Comptroller of the Currency. Check back on July 21 for more information." We anticipate for the OTS website to be taken down and their practice of timely disclosures of enforcement actions to stop. Actions against thrifts will likely be disclosed on a monthly basis in the same manner the OCC uses for national banks.

Friday, July 15, 2011

Debt Ceiling Charade: Almost Over

by Calculated Risk on 7/15/2011 11:27:00 PM

I've been hearing from more and more people that they are concerned about the debt ceiling negotiations. Many of these people are busy with their daily lives, and they don't usually pay close attention to politics or budget issues.

This concern is probably why consumer sentiment fell sharply in the Reuters / University of Michigan preliminary July survey.

No worries.

The debt ceiling is about paying the bills, not the deficit. However it is not uncommon for the party in control of Congress to try to use the debt ceiling as a tool to try to negotiate on budget priorities. That is what has been happening.

But at any time Congress can agree to pay the bills, and they will this time too. As Senator McConnell (R) noted this week, if the U.S. defaults, the American people would blame the party in control of Congress - the Republican party - and the "Republican brand" would be forever toxic. The leaders of the party can't allow that to happen, and the are now looking for the exit.

From Lisa Mascaro and Kathleen Hennessey at the LA Times: House Republicans brace for compromise on debt

Republican leaders in the House have begun to prepare their troops for politically painful votes to raise the nation's debt limit ... Republican leaders orchestrated a series of public moves intended to soften the blow for conservatives. They agreed to give the House an opportunity to vote on two top conservative priorities: a so-called cut-cap-and-balance bill, which would order $111 billion in cuts in federal programs for 2012 and impose a cap on future spending, and a constitutional amendment that would require a balanced federal budget.Ignore the votes this coming week. These bills will not pass the Senate, and no Republican or Democratic President would sign them anyway - they are just for show. The real votes start the following week, and the debt ceiling will be increased.

The Democratic leadership in the Senate is also expected to allow votes on one, and perhaps both, measures. Neither is expected to become law ... Congress is likely to spend much of next week on those measures, then could take up a debt ceiling measure in the Senate toward the end of next week.

This is almost over.

Bank Failure #55: Summit Bank, Prescott, AZ

by Calculated Risk on 7/15/2011 09:18:00 PM

Setback Summit soon shutdown

Shambled shipwreck sunk!

by Soylent Green is People

From the FDIC: The Foothills Bank, Yuma, Arizona, Assumes All of the Deposits of Summit Bank, Prescott, Arizona

As of March 31, 2011, Summit Bank had approximately $72.0 million in total assets and $66.4 million in total deposits. ... The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $11.3 million. ... Summit Bank is the 55th FDIC-insured institution to fail in the nation this year, and the second in Arizona.That makes four today.

Earlier:

• From the NY Fed: Empire State Manufacturing Survey indicates conditions deteriorated in July

• Consumer Sentiment declines sharply in July

• Industrial Production increased 0.2% in June, Capacity Utilization unchanged

• Eight Banks Fail European Stress Tests

• Key Measures of Inflation ease in June

Stand-up Economist Yoram Bauman on Politics and the Federal Budget

by Calculated Risk on 7/15/2011 07:15:00 PM

Here is a new routine from stand-up economist Yoram Bauman on YouTube ...

Earlier:

• From the NY Fed: Empire State Manufacturing Survey indicates conditions deteriorated in July

• Consumer Sentiment declines sharply in July

• Industrial Production increased 0.2% in June, Capacity Utilization unchanged

• Eight Banks Fail European Stress Tests

• Key Measures of Inflation ease in June

Bank Failure #54: First Peoples Bank, Port Saint Lucie, FL

by Calculated Risk on 7/15/2011 06:08:00 PM

Sweating, clock staring bankers

F.D.I.C. Time!

by Soylent Green is People

From the FDIC: Premier American Bank, National Association, Miami, Florida, Assumes All of the Deposits of First Peoples Bank, Port Saint Lucie, Florida

As of March 31, 2011, First Peoples Bank had approximately $228.3 million in total assets and $209.7 million in total deposits. ... The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $7.4 million. ... First Peoples Bank is the 54th FDIC-insured institution to fail in the nation this year, and the seventh in Florida.The Friday afternoon ritual continues - three down today so far.

Earlier:

• From the NY Fed: Empire State Manufacturing Survey indicates conditions deteriorated in July

• Consumer Sentiment declines sharply in July

• Industrial Production increased 0.2% in June, Capacity Utilization unchanged

• Eight Banks Fail European Stress Tests

• Key Measures of Inflation ease in June

Bank Failure #52 & 53 in 2011: Two More in Georgia

by Calculated Risk on 7/15/2011 04:19:00 PM

Two more tumble off the tree

A bitter harvest

by Soylent Green is People

From the FDIC: Ameris Bank, Moultrie, Georgia, Acquires All the Deposits of Two Georgia Institutions: High Trust Bank, Stockbridge and One Georgia Bank, Atlanta

As of March 31, 2011, High Trust Bank had total assets of $192.5 million and total deposits of $189.5 million; and One Georgia Bank had total assets of $186.3 million and total deposits of $162.1 million.

...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) for High Trust Bank will be $66.0 million and for One Georgia Bank, $44.4 million. ...The closings are the 52nd and 53rd FDIC-insured institutions to fail in the nation so far this year and the fifteenth and sixteenth in Georgia.

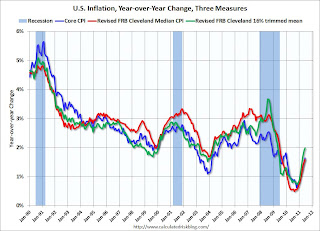

Key Measures of Inflation ease in June

by Calculated Risk on 7/15/2011 01:13:00 PM

This week Fed Chairman Bernanke reiterated the Fed's position that further easing (i.e. QE3) would require both persistent economic weakness and a greater risk of deflation. From Bernanke's testimony:

[T]he possibility remains that the recent economic weakness may prove more persistent than expected and that deflationary risks might reemerge, implying a need for additional policy support.One thing to watch will be the following key measures.

Earlier today the BLS reported:

The Consumer Price Index for All Urban Consumers (CPI-U) decreased 0.2 percent in June on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. ... The gasoline index declined sharply in June, falling 6.8 percent. ... In contrast, the index for all items less food and energy increased 0.3 percent for the second consecutive month.The Cleveland Fed released the median CPI and the trimmed-mean CPI this morning:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.1% (1.7% annualized rate) in June. The 16% trimmed-mean Consumer Price Index increased 0.1% (1.7% annualized rate) during the month.Note: The Cleveland Fed has a discussion of a number of measures of inflation: Measuring Inflation. You can see the median CPI details for June here.

Over the last 12 months, the median CPI rose 1.6%, the trimmed-mean CPI rose 2.0%, the CPI rose 3.6%, and the CPI less food and energy rose 1.6%.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.On a year-over-year basis, these measures of inflation are increasing, but still mostly below the Fed's target. The trimmed-mean is at 2.0% year-over-year; at the Fed's target.

On a monthly basis, the median Consumer Price Index increased 1.7% at an annualized rate, down from 2.1% annualized in May. The 16% trimmed-mean Consumer Price Index also increased 1.7% annualized in June, down from 2.8% annualized in May. And core CPI increased 3.1% annualized, down from 3.5% annualized in May.

With the slack in the system, the year-over-year measures will probably stay near or be below 2% this year.

Earlier:

• From the NY Fed: Empire State Manufacturing Survey indicates conditions deteriorated in July

• Consumer Sentiment declines sharply in July

• Industrial Production increased 0.2% in June, Capacity Utilization unchanged

• Eight Banks Fail European Stress Tests

Eight Banks Fail European Stress Tests

by Calculated Risk on 7/15/2011 12:20:00 PM

Here is the page for the European Banking Authority (EBA)

EBA Press release (pdf)

Stress Test Summary report (pdf)

From the WSJ: 8 Banks Fail EU 'Stress Tests'

Eight banks flunked the European Union's "stress tests," with a combined shortfall of €2.5 billion ($3.54 billion) in capital under a simulated worst-case economic scenario, the European Banking Authority said.Only €2.5 billion in capital needed? And the banks are reported to hold an aggregate €1.1 trillion euros in government debt from Greece, Ireland, Portugal and Spain? I think investors will remain skeptical.

The EU regulator said Friday that another 16 banks narrowly passed the tests, which examined the abilities of 90 top lenders across Europe to endure a deteriorating economy and strained financial system.

By awarding a relatively clean bill of health to the vast majority of Europe's banking industry, the tests are likely to be greeted with skepticism.