RSS Feed

RSS Feed by Calculated Risk on 4/29/2011 09:55:00 AM

Friday, April 29, 2011

Consumer Sentiment increases slightly in April compared to March

• From the Chicago Business Barometer™ Tempered: "The Chicago Purchasing Managers reported the CHICAGO BUSINESS BAROMETER slackened but remained strong, indicating expanding economic activity for the nineteenth consecutive month. In response to special questions about the Japanese disaster, panelists reported minimal impact."

The overall index decreased to 67.6 from 70.6 in March. This was below consensus expectations of 69.2. Note: any number above 50 shows expansion. The employment index decreased to a still strong 63.7 from 65.6. This was another fairly strong report.

• The final April Reuters / University of Michigan consumer sentiment index decreased to 68.9 in April from the preliminary 69.6. This was up slightly from the March reading of 67.5.

Click on graph for larger image in graphic gallery.

Click on graph for larger image in graphic gallery.

This was below the consensus forecast of 70.0.

In general consumer sentiment is a coincident indicator and is usually impacted by employment (and the unemployment rate) and gasoline prices.

This low reading is probably due to $4 per gallon gasoline prices.

Personal Income and Outlays Report for March

by Calculated Risk on 4/29/2011 08:30:00 AM

The BEA released the Personal Income and Outlays report for March:

Personal income increased $67.0 billion, or 0.5 percent ... Personal consumption expenditures (PCE) increased $60.7 billion, or 0.6 percent.Real PCE was revised up significantly for both January and February.

...

Real PCE -- PCE adjusted to remove price changes -- increased 0.2 percent in March, compared with an increase of 0.5 percent in February.

The following graph shows real Personal Consumption Expenditures (PCE) through March (2005 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.PCE increased 0.5% in March, but real PCE only increased 0.2% as the price index for PCE increased 0.4 percent in March.

Note: Core PCE - PCE excluding food and energy - increased 0.1% in March.

The second graph shows real personal income less transfer payments as a percent of the previous peak. This has been slow to recover - and real personal income less transfer payments declined slightly in March. This remains 3.1% below the previous peak.

The second graph shows real personal income less transfer payments as a percent of the previous peak. This has been slow to recover - and real personal income less transfer payments declined slightly in March. This remains 3.1% below the previous peak.The personal saving rate was unchanged at 5.5% in March.

Personal saving -- DPI less personal outlays -- was $651.2 billion in March, compared with $647.5 billion in February. Personal saving as a percentage of disposable personal income was 5.5 percent in March, the same as in February.

This graph shows the saving rate starting in 1959 (using a three month trailing average for smoothing) through the March Personal Income report.

This graph shows the saving rate starting in 1959 (using a three month trailing average for smoothing) through the March Personal Income report. One of the surprises in the Q1 GDP report was the 2.7% annualized growth rate for PCE. PCE growth in January and February was revised up significantly, and PCE in March increased at a 3.1% annualized rate (over the last 3 months).

Thursday, April 28, 2011

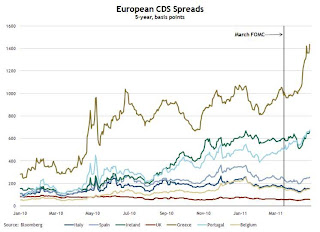

European Bond and CDS Spreads

by Calculated Risk on 4/28/2011 09:22:00 PM

Here is a look at European bond spreads from the Atlanta Fed weekly Financial Highlights released today (graph as of April 27th):

Click on graph for larger image in new window.

Click on graph for larger image in new window.

From the Atlanta Fed:

Since the March FOMC meeting, peripheral European bond spreads (over German bonds) continue to be elevated, with those of Greece, Ireland, and Portugal setting record highs.The second graph shows the Credit Default Swap (CDS) spreads:

Since the March FOMC meeting, the 10-year Greece-to-German bond spread has widened by 189 basis points (bps), through April 26. The spreads for Ireland and Portugal have soared higher by 85 and 237 bps, respectively, over the same period.

From the Atlanta Fed:

From the Atlanta Fed: The CDS spread on Greek debt has widened about 430 basis points (bps) since the March FOMC meeting, while those on Portuguese and Irish debt continue to be high.Here is a story from Reuters discussing the Greece CDS (and possible haircuts of 60%): Upward bias seen for Greek bond yields, trade choppy

The yield on Greece ten year bonds decreased to 15.7% today and the two year yield was down slightly to 24.9%.

Here are the ten year yields for Ireland at 10.4%, Portugal up to a record 9.7%, and Spain at 5.4%.

Earlier:

• Advance Report: Real Annualized GDP Grew at 1.8% in Q1

• Residential Investment and Non-Residential investment in Structures at Record Lows as Percent of GDP

Fannie Mae and Freddie Mac Delinquency Rates decline

by Calculated Risk on 4/28/2011 06:03:00 PM

Fannie Mae reported that the serious delinquency rate decreased to 4.44% in February from 4.45% in January. This is down from the all time high 5.59% in February 2010.

Freddie Mac reported that the serious delinquency rate decreased to 3.63% in March from 3.82% in February. (Note: Fannie reports a month behind Freddie). This is down from 4.13% in March 2010.

These are loans that are "three monthly payments or more past due or in foreclosure".

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

Some of the rapid increase in 2009 was probably because of foreclosure moratoriums, and also because loans in trial mods were considered delinquent until the modifications were made permanent. As modifications have become permanent, they are no longer counted as delinquent.

Although delinquencies typically decline in March, the decline for Freddie Mac delinquencies is larger than usual - and other data suggest the overall delinquency rate declined further in Q1. The MBA will release the Q1 National Delinquency Survey in May.

Earlier:

• Advance Report: Real Annualized GDP Grew at 1.8% in Q1

• Residential Investment and Non-Residential investment in Structures at Record Lows as Percent of GDP

Multifamily: Rents Rising, Record low completions, Starts increasing rapidly, more "hate" for owning

by Calculated Risk on 4/28/2011 03:04:00 PM

Here are some conference call comments from AvalonBay Communities, Inc (ht Brian). AVB has close to 50,000 apartment units. We've discussed many of these key point:

• The percent of residents moving out to purchase a home was at 12%; an all time record low (we are starting to feel the "hate" for owning).

• A record low number of multifamily units will be completed this year. AVB mentions starts of around 150,000 units this year, and probably 240,000 units next year (for delivery in 2013 and 2014). There were just over 100,000 multifamily starts in 2010, so there will be a strong increase this year.

• Rents are increasing - around 7% year-over-year for leases expiring in June (this probably includes some concessions last year). AVB is seeing some push back (moveouts) due to higher rents, but not a large number - this might limit future rent increases.

AVB: The factors driving the improvement in apartment fundamentals are reasonably well known. Probably most visibly is an improving economy, now generating approximately 200,000 new jobs per month. It's both the magnitude and the composition of the jobs that matter and importantly, a disproportionate share of the new jobs created have been in the under 35 age cohort. Over the past year, job growth in the younger age group has been at a rate more than two times than that of the economy as a whole. With more jobs, they are increasingly unbundling. Secondly, corporate investment and equipment and software is rising at an annual rate of approximately 15% nationally, setting off strong job growth in our key high tech markets such as San Jose, Seattle, and Boston. Another key factor affecting rental demand is the continued weakness in the for sale market. Yesterday, the first quarter homeownership data was released, which showed the homeownership rate falling once again, now down to 66.5%. The weakness in the for sale market provides an obvious and direct benefit to the rental market, with households that are increasingly choosing to rent versus buy. As you know, we tracked the reasons for moveout, and during the first quarter, the percent of residents moving out to purchase a home fell to 12%, down from 15% last quarter, and is now at the lowest level since we began tracking this data. Historically -- low to mid 20% range. The increase in rental housing demand is being met by a sharp reduction in the supply of new apartments. Just to put this into perspective, over the 10-year period from 1998 through 2008, there's an average of about 240,000 new rental completions per year. Last year, there were 160,000. And this year, completions are expected to be below 80,000 units, which would make it a 50-year low. This level of new completions is actually less than the estimated annual loss due to obsolescence, meaning that we're seeing essentially a net zero increase in the stock at a time of strong demand. Recently there's been a fair amount of discussion regarding the likelihood of an increased volume of new apartment starts, and there's little doubt that the volume will increase, it's important to remember that we're coming off of a 50-year low. For 2011, third party estimates project new rental starts in the range of about 150,000 new units, which is substantially below the 10-year average of 240,000 I previously mentioned. New starts are not expected to approach historical levels until late next year, 2012, which means it would likely not be until late '13 and into '14 that we'll see completions return to historical levels. And obviously it's the completions that are what's important in affecting the supply demand fundamentals. ...

AVB on Rents: Growth in portfolio rents is broad-based, as accelerating as we move into the peak leasing season in the second and third quarters, when over 60% of leases expire. During Q1, year-over-year growth in same-store revenues accelerated through the quarter from 3.2% in January to over 4% in March. This momentum is continuing, with April revenues projected to be up around 4.5%, driven by an average rental rate increase of 4.8% compared to April 2010. Renewal rates are continuing to escalate as well, with offers for renewal increases averaging around 7% per May lease expirations and over 8% for June expirations, up from around 5% April. For June, in Northern California, New York, New Jersey, and New England, the range is around 9 to 9.5%. Every region is experiencing acceleration and renewal increases, except the DC market, where renewal increases leveled off in the 7% range for June. As we mentioned last quarter, Seattle and Southern California had been lagging other regions in recovery. However, during Q1, these regions began to recover as they posted the highest levels of sequential rent growth for new leases over the quarter. Over the last three months alone, new lease rents, which are a blend of new move-ins and renewals, have risen in Seattle and Southern California by 9.5% and 6.5% respectively. Both of these regions have been helped by positive job growth over the last six months. With the recent improvement in Seattle and Southern California, every region is now experiencing improving performance. As the year progresses, we expect that the West Coast markets will continue to accelerate at a faster rate than the East Coast, although every region should continue to experience a healthy rate of growth.

Q&A:

Analyst: I just was wondering if you're seeing any pressure from rental housing?

AVB: We're not seeing anything new, any new pressure from rental housing. If you're alluding to, like, a gray market. If anything, we're seeing the gray market pull back. Whereas a year ago, I would have said there were certain submarkets where we saw more gray market activity. As I speak to the people that run the various regions, we're actually seeing less competition from that, that rental housing stock.

Analyst: What is the main reason moveouts are saying right now?

AVB: The top reason for move out that we're experiencing is when people are just relocating. But it's right consistent with historic averages. You know, as Bryce indicated, home purchase is an area where it's changed, where we're well under historic averages. And then related to rent increase or financial reasons, that's up. And that's up to around 14%, where it's typically run 8 to 10%.

Earlier:

• Advance Report: Real Annualized GDP Grew at 1.8% in Q1

• Residential Investment and Non-Residential investment in Structures at Record Lows as Percent of GDP

Kansas City Manufacturing Survey: Slower expansion in April

by Calculated Risk on 4/28/2011 12:18:00 PM

From the Kansas City Fed: Survey of Tenth District Manufacturing

Growth in Tenth District manufacturing activity moderated somewhat in April, but remained solid. Most producers continued to report healthyNote: both the composite index and employment index were at record highs last month. Any reading above zero indicates expansion.

expectations. Raw materials prices continued to rise, and more producers raised selling prices.

The month-over-month composite index was 14 in April, down from 27 in March and 19 in February. The employment index dropped from 25 to 17 ...

This is the last of the regional Fed surveys for April. The regional surveys provide a hint about the ISM manufacturing index, as the following graph shows.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.The New York and Philly Fed surveys are averaged together (dashed green, through April), and averaged five Fed surveys (blue, through April) including New York, Philly, Richmond, Dallas and Kansas City. The Institute for Supply Management (ISM) PMI (red) is through March (right axis).

The regional surveys suggest the ISM manufacturing index will in the mid-to-high 50s range (fairly strong expansion). The ISM index for April will be released on Monday, May 2nd.

Earlier:

• Advance Report: Real Annualized GDP Grew at 1.8% in Q1

• Residential Investment and Non-Residential investment in Structures at Record Lows as Percent of GDP

Residential Investment and Non-Residential investment in Structures at Record Lows as Percent of GDP

by Calculated Risk on 4/28/2011 10:08:00 AM

First from the NAR: Pending Home Sales Rise Again in March

The Pending Home Sales Index, a forward-looking indicator based on contract signings, rose 5.1 percent to 94.1 in March from a downwardly revised 89.5 in February [revised down from 90.8]. The index is 11.4 percent below 106.2 in March 2010 ...This suggests a slight increase in sales in April and May.

And a couple more graphs from the GDP report ...

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.Residential Investment (RI) decreased in Q1, and as a percent of GDP, RI is at a post-war record low at 2.21%.

Some people have asked how a sector that only accounts for 2.2% of GDP could be so important? The answer is that usually RI accounts for a large percentage of the employment and GDP growth in the first year or so of a recovery (and increases in RI have a positive impact on other areas like furniture, etc). Not this time because of the huge overhang of existing vacant units.

I'll break down Residential Investment (RI) into components after the GDP details are released this coming week. Note: Residential investment (RI) includes new single family structures, multifamily structures, home improvement, broker's commissions, and a few minor categories.

I expect RI to increase in 2011 and add to both GDP and employment growth - for the first time since 2005 (even with the weak start in Q1).

The second graph shows non-residential investment in structures and equipment and software.

The second graph shows non-residential investment in structures and equipment and software. Equipment and software investment has been increasing sharply, and investment growth increased in Q1 at a 11.6% annualized rate.

Non-residential investment in structures is at a record low of 2.48% of GDP, and will probably stayed depressed for some time. I expect non-residential investment in structures to bottom later this year, but the recovery will be very sluggish for some time with the high vacancy rates for offices and malls. I'll also post the investment in offices, malls and hotels after the GDP details are released.

Earlier:

• Advance Report: Real Annualized GDP Grew at 1.8% in Q1

Advance Report: Real Annualized GDP Grew at 1.8% in Q1

by Calculated Risk on 4/28/2011 08:55:00 AM

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 1.8 percent in the first quarter of 2011 (that is, from the fourth quarter to the first quarter) according to the "advance" estimate released by the Bureau of Economic Analysis

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.This graph shows the quarterly GDP growth (at an annual rate) for the last 30 years. The dashed line is the current growth rate. Growth in Q1 at 1.8% annualized was below trend growth (around 3.1%) - and very weak for a recovery, especially with all the slack in the system.

A few key numbers:

• Real personal consumption expenditures increased 2.7 percent (annual rate) in the fourth quarter, compared with an increase of 4.0 percent in Q4 2010. This is higher than the pace in January and February, and indicates a pickup in March.

• Investment: Nonresidential structures decreased 21.7 percent, equipment and software increased 11.6 percent and real residential fixed investment decreased 4.1 percent.

• Government spending subtracted 1.09 percentage points in Q1 (unusual), and change in private inventories added 0.93 percentage points.

The following graph shows the rolling 4 quarter contribution to GDP from residential investment, equipment and software, and nonresidential structures. This is important to follow because residential investment tends to lead the economy, equipment and software is generally coincident, and nonresidential structure investment trails the economy.

For the following graph, red is residential, green is equipment and software, and blue is investment in non-residential structures. The usual pattern - both into and out of recessions is - red, green, blue.

Residential Investment (RI) made a negative contribution to GDP in Q1 2011, and the four quarter rolling average is negative again following the slight boost from the tax credit early in 2010.

Residential Investment (RI) made a negative contribution to GDP in Q1 2011, and the four quarter rolling average is negative again following the slight boost from the tax credit early in 2010. Equipment and software investment has made a significant positive contribution to GDP for seven straight quarters (it is coincident).

The contribution from nonresidential investment in structures was negative in Q1. Nonresidential investment in structures typically lags the recovery.

The key leading sector - residential investment - has lagged this recovery because of the huge overhang of existing inventory. Usually RI is a strong contributor to GDP growth and employment in the early stages of a recovery, but not this time - and this is a key reason why the recovery has been sluggish so far. However I expect residential investment will turn positive this year mostly from investment in multi-family structures and home improvement.

Weekly Initial Unemployment Claims increase, 4-Week average over 400,000

by Calculated Risk on 4/28/2011 08:30:00 AM

The DOL reports on weekly unemployment insurance claims:

In the week ending April 23, the advance figure for seasonally adjusted initial claims was 429,000, an increase of 25,000 from the previous week's revised figure of 404,000. The 4-week moving average was 408,500, an increase of 9,250 from the previous week's revised average of 399,250.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.This graph shows the 4-week moving average of weekly claims for the last 40 years. The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased this week to 408,250.

Weekly claims have increased over the last few weeks, and this is the first time the four-week average was above 400,000 in two months.

Wednesday, April 27, 2011

Tim Duy: Very High Bar for QE3

by Calculated Risk on 4/27/2011 10:14:00 PM

From Professor Tim Duy: Very High Bar for QE3

...The Fed's forecasts for inflation and the unemployment rate would seem to suggest more QE, but I think Tim Duy's assessment is correct: Bernanke has set the bar very high for QE3. And the odds of more fiscal policy aimed at the unemployed are zero.

Apparently the threat of headline deflation off the table, Bernanke is not inclined to pursue sustained easing despite low core inflation and high unemployment. Again, I am not entirely surprised, except that Bernanke appear to suggest we are much closer to an inflation tipping point than I would expect. He could have tempered these comments with a more forceful discussion of labor costs, but did not. It seems clear these comments were intended to calm the non-existent bond market vigilantes, but is it consistent with the outlook? Arguably, no. For what it’s worth, I think Bernanke appeared most uncomfortable during this portion of the conference.

Bottom Line: When I look at the revisions to the Fed’s outlook and listen to Bernanke, I get the sense that the basic Fed policy is summarized as follows: “The economic situation continues to fall short of that consistent with the dual mandate, we have the tools to address that deviation, but will take no additional action because some people in the Middle East are seeking democracy.”

Earlier:

• A few takeaways from Bernanke Press Briefing

• Q1 2011: Homeownership Rate at 1998 Levels