RSS Feed

RSS Feed by Calculated Risk on 10/31/2005 01:40:00 AM

Monday, October 31, 2005

Housing and More

My Angry Bear post is up: GDP and Housing.

Dr. Thoma excerpts Krugman's Ending the Fraudulence. I would like to echo Dr. Thoma's comments on the media.

Journalists need to ... ask themselves how to do a better job of presenting objective analysis on economic matters rather than the opinions of pundits from both sides. That’s a lot harder than grabbing the usual talking heads who say the usual things, it will require digging in and doing research, seeking out and talking to the real experts in the field, and understanding the issues before reporting on them.Of course the media tries to be "fair" and report both sides. When one side is spouting nonsense, reporting both sides equally is absurd. Dr. Krugman once joked that if President Bush said that the Earth was flat, the headlines of news articles would read, "Opinions Differ on Shape of the Earth."

And finally, I have suggested that the UK's current economic problems might be an example of what will happen in the US, after the housing market slows, since the BoE started raising rates sooner than the FED. Australia is another country to watch: Home sales stall on slowdown

SALES of new homes and units plummeted 16 per cent in September with no sight of a recovery in the housing market, figures released today show.Dilbert (Scott Adams) has started blogging: Enjoy!

The sale of new houses fell by 20 per cent while the sale of multi-units rose 9.4 per cent over the month, the Housing Industry Association (HIA) said.

New home sales are less than half their level two years ago before the property market had started to cool with higher interest rates.

Australia's peak building industry body said there was no sight of recovery in housing demand.

Friday, October 28, 2005

UCLA's Dr. Thornberg: California Housing 35% overvalued

by Calculated Risk on 10/28/2005 08:48:00 PM

The Economic Alliance for Business (EDAB) just released their October 2005 East Bay Quarterly Forecast, authored by Christopher Thornberg, Senior Economist for UCLA Anderson Forecast (thanks to Robert Sakai). The report is fairly positive on the economy over the next few quarters, but is cautionary on real estate. Dr. Thornberg writes:

The good news is likely to continue for the next few quarters. Katrina and Rita may have monopolized the newspapers, but they will have little impact positive or negative on the California economy. Gas prices are already on their way back down. Demand is softening as the year moves into the winter season and refining capacity is coming back online. With pockets flush again, expect a solid holiday season for retailers in the area.From the section on Real Estate: Is the party coming to an end?

But there are storm clouds on the horizon that are being generated by yet another low-pressure system building up -- our housing markets. Prices have continued their truly meteoric rise, as has the pace of building. But there are signs the market is starting to lose its oomph. Market activity in the Bay Area has started to slow sharply, and inventories are on the rise.

As has been discussed in this and past reports, the primary driver of the California economy, including the Bay Area and the East Bay, has been the residential real estate boom. ... All this new construction has been creating many of the new jobs in the state including those in finance companies working to extend credit. And while we lack direct evidence, it appears that consumer spending is being fueled largely by the wealth being generated within the economy by the massive rate of appreciation.After a discussion of housing fundamentals, Thornberg states:

... housing prices should have basically gone flat as of Q4 2002, and instead they have grown at an unprecedented pace. While there is some room for debate on this issue, I put the starting date of the downturn in ‘per worker income’ at Q4 2002. On this basis, we can guesstimate that property in California is now overvalued by something close to 35 or 40%.(emphasis added)Thornberg concludes:

The market is still red hot of course. Price appreciation and market activity continue at a record pace. Nevertheless, right now the bubble is clearly starting to lose steam.

...

The best indicator that the party is starting to end will be a decline in overall market activity—slowing of total unit sales and build up of inventories. When inventories rise and sales start to fall this will spill over into price appreciation and construction within three to six quarters, and this is when the overall economy will begin to feel the pinch. Right now the market appears to be at a crossroads. According to the latest numbers available, market inventories in the state have almost doubled over the past six months and overall market activity has been flat albeit at a very high pace.

...

... things are clearly at a tipping point. And remember, while it is unlikely that nominal home prices will fall rapidly, that does not mean a cooling market will do little damage to the economy. A cooling market is characterized by a large drop in new building units, market activity, and refinancing activity, not to mention heightened foreclosure activity. A lot of the new jobs in those areas will suddenly start to disappear. And don’t forget those wealth effects. When consumers realize they can no longer expect that appreciation bonus to subsidize their consumption habits, they will very likely pull back on spending. Keep an eye out.

Krugman on Bernanke

by Calculated Risk on 10/28/2005 01:27:00 AM

Dr. Thoma excerpts from Dr. Krugman's most recent column: New Fed Chairman Bernanke and the Bubble

Krugman on Bernanke's recent comments: "...soothing words are expected from a Fed chairman. He must know that he may be wrong."

Excerpt (italics Krugman, other Dr. Thoma):

... my main concern is that the economy may well face a day of reckoning soon after Mr. Bernanke takes office. And ... coping with that day of reckoning without some nasty shocks may be beyond anyone's talents. The fact is that the U.S. economy's growth over the past few years has depended on two unsustainable trends: a huge surge in house prices and a vast inflow of funds from Asia. Sooner or later, both trends will end, possibly abruptly.

But hasn't Bernanke said there is no housing bubble, and that the global savings glut explains the international trade imbalance and the dangers there aren't as large as many believe?

...Well, soothing words are expected from a Fed chairman. He must know that he may be wrong.

If he is wrong, what should he do? Does he have what it takes to handle such events?

If he is, the U.S. economy will find itself in need of the "Rooseveltian resolve" Mr. Bernanke advocated for Japan. We can safely predict that Mr. Bernanke will show that resolve. ...

It's reassuring to hear such praise for Bernanke. It sounds like monetary policy is in good hands.

But that may not be enough. When all is said and done, the Fed controls only one thing: the short-term interest rate. And it will be a long time before we have competent, public-spirited people controlling taxes, spending and other instruments of economic policy."

That's not quite as reassuring.

Thursday, October 27, 2005

MBA: Increased use of 'creative' mortgages

by Calculated Risk on 10/27/2005 04:57:00 PM

IBD reports: Data confirm increased use of 'creative' mortgages

Faced with rising interest rates, more U.S. home buyers sought savings by opting for riskier nontraditional mortgages in the early part of this year compared with late last year, more evidence of a trend that has caught the attention of regulators and the mortgage industry at large, Mortgage Bankers Association data released Tuesday showed.Here is the MBA release: Mortgage Originations Rise in First Half of 2005; Demand for Interest Only, Option ARM and Alt-A Products Increases

...

Mortgage activity overall expanded in the early part of this year: the dollar volume of first-mortgage originations on single-family homes increased 10%, while volume for second mortgages rose 12%, the trade group said as part of its annual conference, held in Orlando, Fla.

...

"With the difference in ARM rates and fixed rates narrowing, consumers have shifted from traditional ARMs to nontraditional products," said Doug Duncan, MBA's chief economist.

...

The increase in nontraditional lending prompted the Federal Reserve earlier this year to urge greater vigilance on the part of mortgage lenders too.

The Fed's attention highlighted the growing risk in this area, although some of that risk is countered by the large amount, more than half, of loans locked in at fixed interest rates.

The most popular of the "creative" financing now being undertaken by some households include interest-only loans and option ARMs, a relatively new product that allows borrowers to choose each month to pay interest only, interest plus some principal, or even less than the interest due, with the remaining portion of the interest payment tacked on to the principal.

A Wells Fargo survey released this week showed most holders of these loans were paying toward principal. But some experts said the real test will come in just over a year, when higher interest rates kick in for these loans. See related story.

Interest-only loans increased to a 23% share in the first part of this year from a 17% share late last year, the MBA poll showed.

Option ARM originations rose to 7% of the dollar value of originations and 4% of the loan count during the first half of 2005.

"These percentages are likely understated as many survey respondents did not report their option ARM volume," the group said.

Originations of loans to consumers with riskier credit ratings also increased, the survey found. The share of originations that were so-called Alt-A loans, or those that fall somewhere on the risk spectrum between prime and subprime, increased to 11% from 8%.

The survey also found that the majority of loans, 88% in the first half, were for owner-occupied homes. But a rising share was taken up by loans for non-owner-occupied properties, at a "significant" 12%, MBA said.

Some market observers have said that mortgage risk overall has risen in step with an increase of mortgages on investment property. Traditionally, homeowners are viewed as more likely to keep up with payments on their own residence, less so on the roof not over their head.

*More than 9 of 10 interest only loans originated during the first half of 2005 are adjustable rate products, the remaining loans were fixed rate products.

*Among all survey respondents, option ARM originations were 7 percent of dollar originations and 4 percent of the loan count during the first half of 2005. These percentages are likely understated as many survey respondents did not report their option ARM volume. Among survey respondents that did report option ARM data, option ARM loans comprised 16 percent of their dollar originations and 10 percent of their loan count.

*The vast majority of loans (88 percent) in the first half were for owner occupied homes, but the percentage of loans for non-owner occupied properties was significant (12 percent). This finding is consistent with the 2004 Home Mortgage Disclosure Act data which revealed that more than 11 percent of 2004 originations were for non-owner occupied properties.

*While nearly half (48 percent) of all loans originated were agency eligible, they represented only 38 percent of the origination dollar volume. Agency eligible loans are mortgage loans which conform to the size and credit quality guidelines and would be available for sale to Fannie Mae and Freddie Mac under any of their loan programs.

*From the second half of 2004 to the first half of 2005, reverse mortgage originations increased 28 percent, with FHA’s Home Equity Conversion Mortgages (HECMs) increasing by 31 percent and other reverse mortgages up 8 percent.

*Compared with the last half of 2004, the first half of 2005 origination volume of all second mortgages increased 12 percent, closed-end seconds increased 37 percent and open-end seconds or home equity lines of credit (HELOCs) increased 20 percent (based on companies submitting data for both time periods).

*In the first half of 2005, 82 percent of second mortgage originations were HELOC loans compared with 18 percent for closed-end loans. HELOC origination volume refers to the size of the line, not the drawn amount.

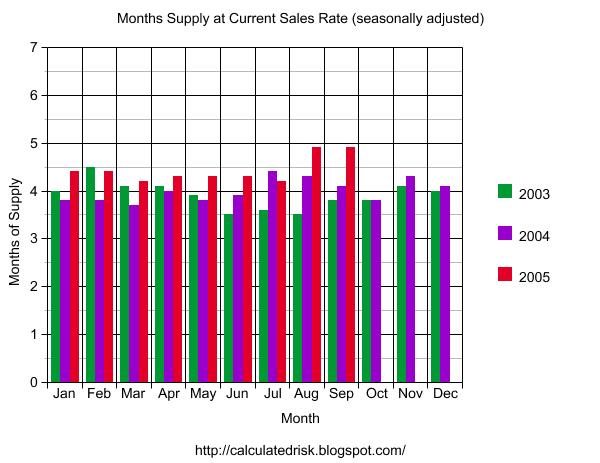

September New Home Sales: 1.222 Million

by Calculated Risk on 10/27/2005 09:58:00 AM

According to the Census Bureau report, New Home Sales in September were at a seasonally adjusted annual rate of 1.222 million vs. market expectations of 1.25 million. August sales were revised down to 1.197 million from 1.237 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

Sales of new one-family houses in September 2005 were at a seasonally adjusted annual rate of 1,222,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development.

The Not Seasonally Adjusted monthly rate was 97,000 New Homes sold, down from a revised 103,000 in August.

On a year over year basis, September 2005 sales are still higher than September 2004.

The median sales price continued to fall.

The median sales price of new houses sold in September 2005 was $215,700; the average sales price was $285,700.

The seasonally adjusted estimate of new houses for sale at the end of September was 493,000. This represents a supply of 4.9 months at the current sales rate.

The 493,000 units of inventory is the all time record for new houses for sale. On a months of supply basis, this is the highest inventory since December 1996 - the end of the previous housing slowdown.

The downturn observed in August has continued into September. This report shows a significant downturn in the New Home Sales market. Sales were off. Inventories were up. Revisions were negative.

It appears the housing market is slowing.

Wednesday, October 26, 2005

Housing and UK Update

by Calculated Risk on 10/26/2005 12:10:00 PM

Just some stories ...

MBA: Mortgage Application Volume Down in Latest Survey

"The seasonally-adjusted Purchase Index decreased by 7.4 percent ... from ... the previous week whereas the Refinance Index decreased by 8.5 percent..."Denver: October housing market still soft

Sellers are having to make more concessions, having to adjust their prices downward," said Steve McGuire with Re/Max Professionals in Highlands Ranch. "Maybe we are seeing a little bit of a trend."Florida: More houses in region hitting the market, tempering prices

A report by the Sarasota Association of Realtors due out this week shows listings in Sarasota County more than doubled in September to 1,331 compared with the same month last year.More Mass. articles: Mass. home prices fall in September and Mass. housing market showing signs of fatigue

In Manatee, listings for August jumped a whopping 157 percent compared with the same month last year.

The increase is mostly because of the longer time listings are remaining on the market.

And on the possible Canary in the Coal mine (The UK, thanks to Joshua):

More homeowners in debt trouble

Mortgage repossession orders during the past three months in England and Wales were up 66% on a year ago to nearly 20,000, official figures have shown.Job losses will accelerate, predicts CBI

Repossession orders have been on the increase since early 2004.

...

The Department for Constitutional Affairs figures will add to concerns about debt and the housing market.

"The increase in mortgage possessions fits with the slowdown in house price inflation," Alan Clarke, UK economist at BNP Paribas, said.

"The conclusion is there are still signs of financial stress among homeowners," he added.

A gloomy picture of British manufacturing industry emerged from the latest CBI survey which predicts the loss of thousands more manufacturing jobs. ... The October survey of business by the Confederation of British Industry tells a sorry tale of declining order books and falling optimism brought on mainly by the tough conditions on the shopping high streets.

...

The CBI said: "Rising raw material and energy prices have continued to push up costs and hit profits. Against this background, firms are cutting back on their investment plans and expect the rate of job losses to increase."

Massachusetts: Housing Prices Weaken, Record Inventories

by Calculated Risk on 10/26/2005 05:23:00 AM

The Boston Herald reports: Housing prices weaken

...median house and condo sale prices also fell – something not directly affected by seasonal issues.In Boston, CPI less Shelter has increased 8.7% over the last 12 months. Therefore, in real terms and using the 4% YoY nominal increase reported in the story, house prices have fallen in Massachusetts by almost 5%.

Additionally, the number of unsold houses and condos on the market rose to 56,016 last month – apparently the highest inventory ever recorded.

John Bitner, chief economist at Eastern Bank, said the latest data "very well may confirm that (the market has) passed the peak."

He said that as housing booms die, prices rise year over year for a time, but fall month over month – exactly what yesterday's report showed.

I believe Bitner is correct, the market has passed the peak.

Tuesday, October 25, 2005

Existing Homes: Sales Strong, Inventories Rise Seasonally

by Calculated Risk on 10/25/2005 10:40:00 AM

UPDATE: Add Graph of Year over Year inventory increase.

Click on graph for larger image.

Inventories were up slightly from August to 2.849 million units. This represents an increase of 19.6% over last September. Usually inventories decline in September after the summer selling season. For comparison, August was up 12.2% Year over year, so seasonally this indicates a significant increase in inventories.

Reuters reports: Sept existing home sales flat

Sales of existing U.S. homes were unchanged in September at a 7.28 million unit pace, as strong post-Katrina sales in the U.S. South helped offset weaker activity elsewhere, a trade group said on Tuesday.Median prices declined to $212K, the lowest since May, probably because of the strong activity in the South. Average prices also decreased to $260K, the lowest since May.

Sales of the previously owned homes were flat compared with August's downwardly revised 7.28 million unit pace, the National Association of Realtors said. That figure includes both single-family homes and condominiums.

Analysts had expected overall sales to decline to a 7.20 million unit pace from the originally reported 7.29 million unit pace in August.

Sales would have been lower in September without the strong purchase activity reported for areas around the hurricane-hit zone, the Realtors' chief economist said. For example, while sales dropped 85 percent in New Orleans, Baton Rouge reported a 150 percent increase, the group said.

Monday, October 24, 2005

Prediction for September Petroleum Trade Deficit

by Calculated Risk on 10/24/2005 09:01:00 PM

Here is my forecast for September petroleum import and exports using the same model (described here).

The ERPP (Energy Related Petroleum Products) trade numbers for September are forecast to be:

Forecast: Total NSA ERPP Imports: $23.0 Billion

Total SA ERPP FORECAST:

Imports SA: $23.1 Billion (seasonal factor estimated at 1.003 for Sept)

Exports SA: $2.0 Billion

SA Balance ERPP: $21.1 Billion

This compares to the record $20.6 Billion SA petroleum trade deficit for August.

I am forecasting a record average price per barrel of $56.47 compared to the August record of $52.65.

Imports SA and NSA will be close to the records set in August. Although unit prices were substantially higher in September, imported quantities were lower. A new record depends on the quantity of refined products imported in September.