RSS Feed

RSS Feed by Calculated Risk on 1/12/2026 08:21:00 AM

Monday, January 12, 2026

This is the End and a New Beginning

I've been thinking about this for some time.

After 21 years of writing this blog almost daily, I've decided to stop writing the daily updates on the blog.

However, the economic data "IV" is still in my arm, and I'll be writing a weekly economic summary at the end of each week (via a newsletter - see below). This will have three parts: the Schedule of economic data for the following week, a Review of data for the previous week, and a Commentary on a current topic.

And I'll be writing the Real Estate Newsletter usually 4 to 6 times per week (this remains my main focus).

Thanks for reading the blog all these years! I hope it has been useful and informative.

Thanks for reading the blog all these years! I hope it has been useful and informative.

Thanks to all the people who have helped me over the years. And a special thanks to my friend Tanta; I miss her dearly. Best to all.

Sunday, January 11, 2026

Sunday Night Futures

by Calculated Risk on 1/11/2026 07:50:00 PM

Weekend:

• Schedule for Week of January 11, 2026

Monday:

• No major economic releases scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 futures are down 16 and DOW futures are down 104 (fair value).

Oil prices were up over the last week with WTI futures at $59.37 per barrel and Brent at $63.60 per barrel. A year ago, WTI was at $77, and Brent was at $80 - so WTI oil prices are down about 24% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.74 per gallon. A year ago, prices were at $3.03 per gallon, so gasoline prices are down $0.29 year-over-year.

Hotels: Occupancy Rate Increased 4.4% Year-over-year

by Calculated Risk on 1/11/2026 08:12:00 AM

Hotel occupancy was weak in 2025. It is difficult to tell early in the year because travel is always weak in early January.

From STR: U.S. hotel results for week ending 3 January

Click on graph for larger image.

Click on graph for larger image.

The red line is for 2026, blue is the median, and dashed light blue is for 2025. Dashed black is for 2018, the record year for hotel occupancy.

The U.S. hotel industry reported positive year-over-year comparisons, according to CoStar’s latest data through 3 January. ...The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

28 December 2025 through 3 January 2026 (percentage change from comparable week in 2024 and 2025):

• Occupancy: 50.5% (+4.4%)

• Average daily rate (ADR): US$175.47 (+3.4%)

• Revenue per available room (RevPAR): US$88.65 (+7.9%)

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2026, blue is the median, and dashed light blue is for 2025. Dashed black is for 2018, the record year for hotel occupancy.

It is difficult to judge performance early in the year.

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average will increase seasonally for the next few months.

Saturday, January 10, 2026

Real Estate Newsletter Articles this Week:Housing Starts Decreased to 1.246 million Annual Rate

by Calculated Risk on 1/10/2026 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Housing Starts Decreased to 1.246 million Annual Rate in October

• The "Home ATM" Mostly Closed in Q3

• 1st Look at Local Housing Markets in December

• Asking Rents Decline Year-over-year

• Update: The Housing Bubble and Mortgage Debt as a Percent of GDP

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of January 11, 2026

by Calculated Risk on 1/10/2026 08:11:00 AM

The key reports this week are December CPI, Existing Home Sales and November Retail Sales. Also, New Home Sales for September and October will be released.

For manufacturing, the December Industrial Production report and the January New York and Philly Fed manufacturing surveys will be released.

No major economic releases scheduled.

6:00 AM: NFIB Small Business Optimism Index for December.

8:30 AM: The Consumer Price Index for December from the BLS. The consensus is for 0.3% increase in CPI, and a 0.3% increase in core CPI. The consensus is for CPI to be up 2.7% year-over-year and core CPI to be up 2.7% YoY.

10:00 AM: New Home Sales for September and October from the Census Bureau.

10:00 AM: New Home Sales for September and October from the Census Bureau. This graph shows New Home Sales since 1963 through August 2025.

The dashed line is the sales rate for August.

The consensus is for 714 thousand SAAR for October.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index. This will be two weeks of data.

8:30 AM ET: The Producer Price Index for December from the BLS. The consensus is for a 0.3% increase in PPI, and a 0.2% increase in core PPI.

8:30 AM: Retail sales for November is scheduled to be released.

8:30 AM: Retail sales for November is scheduled to be released. The consensus is for a 0.4% increase in retail sales.

This graph shows retail sales since 1992.

This graph shows retail sales since 1992.

This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

December retail sales for December have not been scheduled yet.

10:00 AM: Existing Home Sales for December from the National Association of Realtors (NAR). The consensus is for 4.23 million SAAR, up from 4.13 million.

10:00 AM: Existing Home Sales for December from the National Association of Realtors (NAR). The consensus is for 4.23 million SAAR, up from 4.13 million.The graph shows existing home sales from 1994 through the report last month.

2:00 PM: the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 208K, unchanged from 208K.

8:30 AM: The New York Fed Empire State manufacturing survey for January. The consensus is for a reading of 1.0, down from -3.9.

8:30 AM: the Philly Fed manufacturing survey for January. The consensus is for a reading of -5.0, up from -10.2.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for December.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for December.This graph shows industrial production since 1967.

The consensus is for a 0.2% increase in Industrial Production, and for Capacity Utilization to be unchanged at 76.0%.

10:00 AM: The January NAHB homebuilder survey.

The consensus is for a reading of 40, up from 39 the previous month. Any number below 50 indicates that more builders view sales conditions as poor than good.

Friday, January 09, 2026

The "Home ATM" Mostly Closed in Q3

by Calculated Risk on 1/09/2026 02:15:00 PM

Today, in the Calculated Risk Real Estate Newsletter: The "Home ATM" Mostly Closed in Q3

A brief excerpt:

During the housing bubble, many homeowners borrowed heavily against their perceived home equity - jokingly calling it the “Home ATM” - and this contributed to the subsequent housing bust, since so many homeowners had negative equity in their homes when house prices declined.

...

Here is the quarterly increase in mortgage debt from the Federal Reserve’s Financial Accounts of the United States - Z.1 (sometimes called the Flow of Funds report) released today. In the mid ‘00s, there was a large increase in mortgage debt associated with the housing bubble.

In Q3 2025, mortgage debt increased $108 billion, unchanged from $108 billion in Q2. Note the almost 7 years of declining mortgage debt as distressed sales (foreclosures and short sales) wiped out a significant amount of debt.

However, some of this debt is being used to increase the housing stock (purchase new homes), so this isn’t all Mortgage Equity Withdrawal (MEW).

Fed's Flow of Funds: Household Net Worth Increased $6.1 Trillion in Q3

by Calculated Risk on 1/09/2026 01:12:00 PM

The Federal Reserve released the Q3 2025 Flow of Funds report today: Financial Accounts of the United States.

The net worth of households and nonprofits rose to $181.6 trillion during the third quarter of 2025. The value of directly and indirectly held corporate equities increased $5.5 trillion and the value of real estate decreased $0.3 trillion.

...

Household debt increased 4.1 percent at an annual rate in the third quarter of 2025. Consumer credit grew at an annual rate of 2.3 percent, while mortgage debt (excluding charge-offs) grew at an annual rate of 3.2 percent.

Click on graph for larger image.

Click on graph for larger image.The first graph shows Households and Nonprofit net worth as a percent of GDP.

Net worth increased $6.1 trillion in Q3. As a percent of GDP, net worth increased in Q3 but is still below the peak in 2021.

This includes real estate and financial assets (stocks, bonds, pension reserves, deposits, etc.) net of liabilities (mostly mortgages). Note that this does NOT include public debt obligations.

The second graph shows homeowner percent equity since 1952.

The second graph shows homeowner percent equity since 1952.

Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008.

In Q3 2025, household percent equity (of household real estate) was at 71.6% - down from 72.0% in Q2, 2025

Note: This includes households with no mortgage debt.

The third graph shows household real estate assets and mortgage debt as a percent of GDP.

The third graph shows household real estate assets and mortgage debt as a percent of GDP.

Mortgage debt increased by $108 billion in Q3.

Mortgage debt is up $2.99 trillion from the peak during the housing bubble, but, as a percent of GDP is at 43.9% - down from Q2 - and down from a peak of 73.1% of GDP during the housing bust.

The value of real estate, as a percent of GDP, decreased in Q3 and is below the recent peak in Q2 2022, but is well above the median of the last 30 years.

The second graph shows homeowner percent equity since 1952.

The second graph shows homeowner percent equity since 1952. Household percent equity (as measured by the Fed) collapsed when house prices fell sharply in 2007 and 2008.

In Q3 2025, household percent equity (of household real estate) was at 71.6% - down from 72.0% in Q2, 2025

Note: This includes households with no mortgage debt.

The third graph shows household real estate assets and mortgage debt as a percent of GDP.

The third graph shows household real estate assets and mortgage debt as a percent of GDP. Mortgage debt increased by $108 billion in Q3.

Mortgage debt is up $2.99 trillion from the peak during the housing bubble, but, as a percent of GDP is at 43.9% - down from Q2 - and down from a peak of 73.1% of GDP during the housing bust.

The value of real estate, as a percent of GDP, decreased in Q3 and is below the recent peak in Q2 2022, but is well above the median of the last 30 years.

Newsletter: Housing Starts Decreased to 1.246 million Annual Rate in October

by Calculated Risk on 1/09/2026 10:34:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Housing Starts Decreased to 1.246 million Annual Rate in October

A brief excerpt:

Note: The Census Bureau is still catching up. They released Start data for September and October today, but we are still missing November data.There is much more in the article.

...

The third graph shows the month-to-month comparison for total starts between 2024 (blue) and 2025 (red).

Total starts were down 7.8% in October compared to October 2024.

Year-to-date (YTD) starts are down 0.7% compared to the same period in 2024. Single family starts are down 7.0% YTD and multi-family up 18.0% YTD.

Housing Starts Decreased to 1.246 million Annual Rate in October

by Calculated Risk on 1/09/2026 09:59:00 AM

From the Census Bureau: Permits, Starts and Completions

Housing Starts:

Privately-owned housing starts in October were at a seasonally adjusted annual rate of 1,246,000. This is 4.6 percent below the revised September estimate of 1,306,000 and is 7.8 percent below the October 2024 rate of 1,352,000. Single-family housing starts in October were at a rate of 874,000; this is 5.4 percent above the revised September figure of 829,000. The October rate for units in buildings with five units or more was 347,000.

Building Permits:

Privately-owned housing units authorized by building permits in October were at a seasonally adjusted annual rate of 1,412,000. This is 0.2 percent below the revised September rate of 1,415,000 and is 1.1 percent below the October 2024 rate of 1,428,000. Single-family authorizations in October were at a rate of 876,000; this is 0.5 percent below the revised September figure of 880,000. Authorizations of units in buildings with five units or more were at a rate of 481,000 in October.

emphasis added

Click on graph for larger image.The first graph shows single and multi-family housing starts since 2000.

Multi-family starts (blue, 2+ units) decreased month-over-month in October. Multi-family starts were down 7.9% year-over-year.

Single-family starts (red) increased in October and were down 7.8% year-over-year.

The second graph shows single and multi-family housing starts since 1968.

The second graph shows single and multi-family housing starts since 1968. Total housing starts in October were well below expectations. We are still missing data for November due to the government shutdown.

I'll have more later …

Comments on December Employment Report

by Calculated Risk on 1/09/2026 09:20:00 AM

The headline jobs number in the December employment report was slightly below expectations, however October and November were revised down by 76,000. The unemployment rate decreased to 4.4%.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate is impacted by both cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The 25 to 54 years old participation rate was unchanged in December at 83.8%% from 83.8% in November.

The 25 to 54 employment population ratio increased to 80.7% from 80.6% the previous month.

Both are down slightly from the recent peaks, but still near the highest level this millennium.

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

Average Hourly Wages

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES).

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees from the Current Employment Statistics (CES). There was a huge increase at the beginning of the pandemic as lower paid employees were let go, and then the pandemic related spike reversed a year later.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 3.8% YoY in December, up from 3.6% YoY in November.

Wage growth has trended down after peaking at 5.9% YoY in March 2022 and was at 3.8% YoY in December, up from 3.6% YoY in November.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of people employed part time for economic reasons, at 5.3 million, changed little in December but is up by 980,000 over the year. These individuals would have preferred full-time employment but were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons decreased in December to 5.34 million from 5.49 million in November. This is well above the pre-pandemic levels and near the highest levels since mid-2021.

These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 8.4% from 8.7% in November. This is down from the record high in April 2020 of 22.9% and up from the lowest level on record (seasonally adjusted) in December 2022 (6.6%). (This series started in 1994). This measure is well above the 7.0% level in February 2020 (pre-pandemic).

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 1.95 million workers who have been unemployed for more than 26 weeks and still want a job, up from 1.91 million in November.

This is down from post-pandemic high of 4.171 million, and up from the recent low of 1.056 million.

This is above pre-pandemic levels.

Summary:

The headline jobs number in the December employment report was slightly below expectations, however October and November were revised down by 76,000. The unemployment rate decreased to 4.4%.

This is above pre-pandemic levels.

Summary:

The headline jobs number in the December employment report was slightly below expectations, however October and November were revised down by 76,000. The unemployment rate decreased to 4.4%.

This was another weak employment report.

December Employment Report: 50 thousand Jobs, 4.4% Unemployment Rate

by Calculated Risk on 1/09/2026 08:30:00 AM

From the BLS: Employment Situation

Both total nonfarm payroll employment (+50,000) and the unemployment rate (4.4 percent) changed little in December, the U.S. Bureau of Labor Statistics reported today. Employment continued to trend up in food services and drinking places, health care, and social assistance. Retail trade lost jobs.

...

The change in total nonfarm payroll employment for October was revised down by 68,000, from -105,000 to -173,000, and the change for November was revised down by 8,000, from +64,000 to +56,000. With these revisions, employment in October and November combined is 76,000 lower than previously reported.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the jobs added per month since January 2021.

Total payrolls increased by 50 thousand in December. Private payrolls increased by37 thousand, and public payrolls increased 13 thousand.

Payrolls for October and November were revised down by 76 thousand, combined. The economy has only added 93 thousand jobs since April (8 months).

Payrolls for October and November were revised down by 76 thousand, combined. The economy has only added 93 thousand jobs since April (8 months).

The second graph shows the year-over-year change in total non-farm employment since 1968.

The second graph shows the year-over-year change in total non-farm employment since 1968.In December, the year-over-year change was 0.594 million jobs.

Year-over-year employment growth has slowed sharply.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate decreased to 62.4% in December, from 62.5% in November. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate decreased to 62.4% in December, from 62.5% in November. This is the percentage of the working age population in the labor force.

The Employment-Population ratio increased to 59.7% from 59.6% in November (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate.

The unemployment rate was decreased to 4.4% in December from 4.5% in November.

This was slightly below consensus expectations, however, October and November payrolls were revised down by 76,000 combined.

I'll have more later ...

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate decreased to 62.4% in December, from 62.5% in November. This is the percentage of the working age population in the labor force.

The Labor Force Participation Rate decreased to 62.4% in December, from 62.5% in November. This is the percentage of the working age population in the labor force. The Employment-Population ratio increased to 59.7% from 59.6% in November (blue line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate was decreased to 4.4% in December from 4.5% in November.

This was slightly below consensus expectations, however, October and November payrolls were revised down by 76,000 combined.

Overall another weak report.

Thursday, January 08, 2026

Friday: Employment Report, Housing Starts, Flow of Funds

by Calculated Risk on 1/08/2026 08:03:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Friday:

• At 8:30 AM ET,: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.

• At 10:00 AM: Housing Starts for September and October.

• At 10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for January)

• At 12:00 PM: Q3 Flow of Funds Accounts of the United States from the Federal Reserve.

December Employment Preview

by Calculated Risk on 1/08/2026 02:16:00 PM

On Friday at 8:30 AM ET, the BLS will release the employment report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decrease to 4.5%. There were 64,000 jobs added in November, and the unemployment rate was at 4.6%.

From Goldman Sachs:

We forecast that payrolls rose 70k (vs. 55k consensus) in December and the unemployment rate fell to 4.5% (vs. 4.5% consensus). ... We expect the unemployment rate to edge down to 4.5% because the increase to 4.6% in November largely reflected the impact of furloughed federal government workers during the shutdown.From BofA:

emphasis added

Dec NFP are likely to tick up to a stable 70k (private: 75k) print, higher than consensus expectations. Initial claims remain low and continuing claims have trended lower since Oct. Education & health jobs should remain the driver of payroll growth. Given the strength in air travel and holiday spending, we project a rise in leisure & hospitality jobs. After the u-rate jumping to 4.6% in Nov, in part due to shutdown-related distortions, we expect a decline to 4.5%. It is likely that the worst is behind us in the labor market.• ADP Report: The ADP employment report showed 41,000 private sector jobs were added in December. This was slightly below consensus forecasts. However, in general, ADP hasn't been very useful in forecasting the BLS report.

• ISM Surveys: Note that the ISM indexes are diffusion indexes based on the number of firms hiring (not the number of hires). The ISM® manufacturing employment index increased to 44.9%, up from 44.0% the previous month. This suggests manufacturing jobs lost in December. The ADP report indicated 5,000 manufacturing jobs lost in December.

The ISM® services employment index increased to 52.0%, up from 48.9%. This suggests job gains in December.

• Unemployment Claims: The weekly claims report showed about the same number of initial unemployment claims during the reference week at 224,000 in December compared to 222,000 in November. This suggests about the same number of layoffs in December as in November.

• Conclusion: Over the last 6 months, employment gains averaged 17 thousand per month. The ADP report, the ISM Surveys, and unemployment claims suggest similar gains in December compared to November. I'll take the over for December - but still weak hiring.

Wholesale Used Car Prices Increased Slightly in December; Up 0.4% Year-over-year

by Calculated Risk on 1/08/2026 10:52:00 AM

From Manheim Consulting today: Manheim Used Vehicle Value Index: December 2025 Trends

The Manheim Used Vehicle Value Index (MUVVI) rose to 205.5, reflecting a 0.4% increase for wholesale used-vehicle prices (adjusted for mix, mileage, and seasonality) compared to December 2024. The December index is up 0.1% month over month.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This index from Manheim Consulting is based on all completed sales transactions at Manheim’s U.S. auctions.

The Manheim index suggests used car prices increased in December (seasonally adjusted) and were up 0.4% YoY.

Trade Deficit Decreased to $29.4 Billion in October

by Calculated Risk on 1/08/2026 08:48:00 AM

The Census Bureau and the Bureau of Economic Analysis reported:

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis announced today that the goods and services deficit was $29.4 billion in October, down $18.8 billion from $48.1 billion in September, revised.

October exports were $302.0 billion, $7.8 billion more than September exports. October imports were $331.4 billion, $11.0 billion less than September imports.

emphasis added

Click on graph for larger image.

Click on graph for larger image.Exports increased and imports decreased in October.

Exports were up 12% year-over-year; imports were down 4% year-over-year.

Imports increased sharply earlier this year as importers rushed to beat tariffs.

The second graph shows the U.S. trade deficit, with and without petroleum.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.Note that net, exports of petroleum products are positive and have been increasing.

The trade deficit with China decreased to $14.9 billion from $28.1 billion a year ago.

Weekly Initial Unemployment Claims Increase to 208,000

by Calculated Risk on 1/08/2026 08:30:00 AM

The DOL reported:

In the week ending January 3, the advance figure for seasonally adjusted initial claims was 208,000, an increase of 8,000 from the previous week's revised level. The previous week's level was revised up by 1,000 from 199,000 to 200,000. The 4-week moving average was 211,750, a decrease of 7,250 from the previous week's revised average. This is the lowest level for this average since April 27, 2024 when it was 210,250. The previous week's average was revised up by 250 from 218,750 to 219,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 211,750.

This was slightly above the consensus estimate.

Wednesday, January 07, 2026

Thursday: Trade Deficit, Unemployment Claims

by Calculated Risk on 1/07/2026 07:48:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 A ET, Trade Balance report for November from the Census Bureau. The consensus is the trade deficit to be $59.4 billion. The U.S. trade deficit was at $52.8 billion in September.

• Also at 8:30 AM, The initial weekly unemployment claims report will be released. The consensus is for 205K, up from 199K.

1st Look at Local Housing Markets in December

by Calculated Risk on 1/07/2026 12:37:00 PM

Today, in the Calculated Risk Real Estate Newsletter: 1st Look at Local Housing Markets in December

A brief excerpt:

Last year (2025) might have seen the lowest number of existing home sales since 1995. It will be close! Even if sales beat 2024 sales, these will be the two lowest sales years since 1995. Sales will be worse than any year during the housing bust.There is much more in the article.

Most readers probably don’t remember 1995, but I do! If I went to an open house ‘95, I was frequently the only person to visit all day. Just me and the crickets.

December sales will be mostly for contracts signed in October and November, and mortgage rates averaged 6.25% in October and 6.24% in November (lower than for closed sales in November). ...

In December, sales in these early reporting markets were up 2.5% YoY. Last month, in November, these same markets were down 10.8% year-over-year Not Seasonally Adjusted (NSA).

Important: There was one more working days in December 2025 (22) as in December 2024 (21). So, the year-over-year change in the headline SA data will be less than the change in NSA data (there are other seasonal factors).

...

This was just several early reporting markets. Many more local markets to come!

ISM® Services Index Increased to 54.4% in December

by Calculated Risk on 1/07/2026 10:12:00 AM

(Posted with permission). The ISM® Services index was at 54.4%, up from 52.6% the previous month. The employment index increased to 52.0%, up from 48.9%. Note: Above 50 indicates expansion, below 50 in contraction.

From the Institute for Supply Management: Services PMI® at 54.4% December 2025 ISM® Services PMI® Report

Economic activity in the services sector continued to expand in December, say the nation’s purchasing and supply executives in the latest ISM® Services PMI® Report. The Services PMI® registered at 54.4 percent, finishing 2025 on a positive note with its 10th month in expansion territory — and its highest reading — of the year.Employment expanded following six consecutive month of contraction.

The report was issued today by Steve Miller, CPSM, CSCP, Chair of the Institute for Supply Management® (ISM®) Services Business Survey Committee:

“In December, the Services PMI® registered a reading of 54.4 percent, 1.8 percentage points higher than the November figure of 52.6 percent and a third consecutive month of expansion. The Business Activity Index continued in expansion territory in December, registering 56 percent, 1.5 percentage points higher than the reading of 54.5 percent recorded in November. The New Orders Index also remained in expansion in December, with a reading of 57.9 percent, 5 percentage points above November’s figure of 52.9 percent. The Employment Index expanded for the first time in seven months with a reading of 52 percent, a 3.1-percentage point improvement from the 48.9 percent recorded in November — the fifth consecutive monthly increase since a reading of 46.4 percent in July.

“The Supplier Deliveries Index registered 51.8 percent, 2.3 percentage points lower than the 54.1 percent recorded in November. This is the 13th consecutive month that the index has been in expansion territory, indicating slower supplier delivery performance. (Supplier Deliveries is the only ISM® PMI® Reports index that is inversed; a reading of above 50 percent indicates slower deliveries, which is typical as the economy improves and customer demand increases.)

“The Prices Index registered 64.3 percent in December, its lowest level since a reading of 60.9 percent in March 2025. The December figure was a 1.1-percentage point drop from November’s reading of 65.4 percent. The index has exceeded 60 percent for 13 straight months.br /> emphasis added

BLS: Job Openings Declined to 7.1 million in November

by Calculated Risk on 1/07/2026 10:00:00 AM

From the BLS: Job Openings and Labor Turnover Summary

The number of job openings was little changed at 7.1 million in November, the U.S. Bureau of Labor Statistics reported today. Over the month, hires were little changed and total separations were unchanged at 5.1 million each. Within separations, both quits (3.2 million) and layoffs and discharges (1.7 million) were little changed.The following graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

emphasis added

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for November; the employment report to be released on Friday will be for December.

Click on graph for larger image.

Click on graph for larger image.Note that hires (dark blue) and total separations (red and light blue columns stacked) are usually pretty close each month. This is a measure of labor market turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

The spike in layoffs and discharges in March 2020 is labeled, but off the chart to better show the usual data.

Jobs openings decreased in November to 7.15 million from 7.45 million in October.

The number of job openings (black) were down 11% year-over-year.

Quits were up 4% year-over-year. These are voluntary separations. (See light blue columns at bottom of graph for trend for "quits").

ADP: Private Employment Increased 41,000 in December

by Calculated Risk on 1/07/2026 08:15:00 AM

“Small establishments recovered from November job losses with positive end-of-year hiring, even as large employers pulled back,” said Dr. Nela Richardson, chief economist, ADP.This was below the consensus forecast of 50,000 jobs added. The BLS will report on Friday, and the consensus is for 55,000 jobs added.

emphasis added

MBA: Mortgage Applications Decreased Over a Two-Week Period

by Calculated Risk on 1/07/2026 07:00:00 AM

From the MBA: MMortgage Applications Decreased Over a Two-Week Period in Latest MBA Weekly Survey

Mortgage applications decreased 9.7 percent from two weeks earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending January 2, 2026. The results include an adjustment for the holidays.

The Market Composite Index, a measure of mortgage loan application volume, decreased 9.7 percent on a seasonally adjusted basis from two weeks earlier. On an unadjusted basis, the Index decreased 28 percent compared with two weeks ago. The holiday adjusted Refinance Index decreased 14 percent from two weeks ago and was 133 percent higher than the same week one year ago. The unadjusted Refinance Index decreased 31 percent from two weeks ago and was 108 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 6 percent from two weeks earlier. The unadjusted Purchase Index decreased 23 percent compared with two weeks ago and was 10 percent higher than the same week one year ago.

“Mortgage rates started the New Year with a decline to 6.25 percent, the lowest level since September 2024. Refinance applications were up 7 percent for the week but were at a slower pace than in the weeks leading up to the holidays,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “FHA refinance applications saw a 19 percent increase, although that was a partial rebound from a drop the week before. MBA continues to expect mortgage rates to stay around current levels, with spells of refinance opportunities in the weeks when rates move lower.”

Added Kan, “Purchase applications were 10 percent higher than the same week a year ago but were down over the week following decreases in conventional and FHA applications. The average loan size was $408,700, the smallest in a year, driven by lower average loan sizes across both conventional and government loan types.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) decreased to 6.25 percent from 6.32 percent, with points decreasing to 0.57 from 0.59 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is up 10% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is still depressed, but solidly above the lows of 2023 and above the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

The refinance index increased from the bottom as mortgage rates declined, but is down from the recent peak in September as rates moved sideways.

Tuesday, January 06, 2026

Wednesday: ADP Employment, Job Openings, ISM Services

by Calculated Risk on 1/06/2026 08:04:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index. This will be two weeks of data.

• At 8:15 AM, The ADP Employment Report for December. This report is for private payrolls only (no government). The consensus is for 50,000, up from -32,000 jobs added in November.

• At 10:00 AM, Job Openings and Labor Turnover Survey for November from the BLS.

• At 10:00 AM, the ISM Services Index for December.

Light Vehicle Sales Increased to 16.0 Million SAAR in December

by Calculated Risk on 1/06/2026 01:21:00 PM

The BEA reported that light vehicle sales were at 16.0 million in December on a seasonally adjusted annual basis (SAAR). This was up 1.9% from the sales rate in November, and down 4.9% from December 2024.

Click on graph for larger image.

Click on graph for larger image.

This graph shows light vehicle sales since 2006 from the BEA (blue) through December.

Vehicle sales were over 17 million SAAR in March and April as consumers rushed to "beat the tariffs".

Then sales were depressed in May and June.

Sales were boosted in August and September due to the termination of the EV credit at the end of September.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

Sales in Decvember were slightly above the consensus forecast.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.Sales in Decvember were slightly above the consensus forecast.

Light vehicle sales were up 2.4% in 2025 compared to 2024.

Heavy Truck Sales Collapsed in Q4; Down 32.5% Year-over-year in December

by Calculated Risk on 1/06/2026 10:54:00 AM

This graph shows heavy truck sales since 1967 using data from the BEA. The dashed line is the December 2025 seasonally adjusted annual sales rate (SAAR) of 311 thousand.

Note: "Heavy trucks - trucks more than 14,000 pounds gross vehicle weight."

Click on graph for larger image.

Click on graph for larger image.

Heavy truck sales were at 311 thousand SAAR in December, down from 336 thousand in November, and down 32.5% from 461 thousand SAAR in December 2024.

Sales were down 15.3% in 2025 compared to annual sales in 2024.

Usually, heavy truck sales decline sharply prior to a recession, and sales have collapsed recently.

Asking Rents Decline Year-over-year

by Calculated Risk on 1/06/2026 10:14:00 AM

Today, in the Real Estate Newsletter: Asking Rents Decline Year-over-year

Brief excerpt:

Another monthly update on rents.There is much more in the article.

Tracking rents is important for understanding the dynamics of the housing market. Slower household formation and increased supply (more multi-family completions) has kept asking rents under pressure.

More recently, immigration policy has become a negative for rentals.

Apartment List: Asking Rent Growth -1.3% Year-over-year ...

The national median rent fell 0.8% in December, and now stands at $1,356. This closes the book on 2025, with five consecutive months of rent declines. Based on recent years, we expect another 1-2 months of rent drops before the market turns a corner in early Spring.Realtor.com: 28th Consecutive Month with Year-over-year Decline in RentsAcross the 50 largest metropolitan areas in the United States, median asking rent for 0-2 bedroom units fell for the 28th consecutive month on a year-over-year basis.

ICE: "Annual home price growth ended 2025 at just +0.7%"

by Calculated Risk on 1/06/2026 08:11:00 AM

The ICE Home Price Index (HPI) is a repeat sales index. ICE reports the median price change of the repeat sales.

From ICE (Intercontinental Exchange):

Annual home price growth ended 2025 at just +0.7% — the smallest calendar-year increase since 2011, when prices fell by 2.9%.As ICE mentioned, "regional trends ... show significant variation". The Northeast and Midwest are saw solid house price gains in 2025, whereas cities in the South and West have been leading the way in inventory increases and price declines (especially Florida and Texas).

With income growth outpacing home price gains and 30-year mortgage rates starting 2026 at 6.15%, housing affordability is at its best level in nearly four years.

At current prices and rates, purchasing an average-priced home with 20% down and a 30-year loan requires a monthly payment of $2,093 — 27.8% of median household income. That’s down from $2,256 (31.1%) at the start of 2025.

According to Andy Walden, Head of Mortgage and Housing Market Research for Intercontinental Exchange:

“Improved affordability and income growth have provided a much-needed boost to housing market dynamics, even as regional trends and property types show significant variation. The Northeast and Midwest have emerged as clear leaders, while condos continue to face headwinds in most markets.”

Drilling down into regional and property type specifics:

• Regional Standouts: New Haven, CT led all markets with an impressive 8.6% price growth, followed by Syracuse, NY (+6.8%) and Hartford, CT (+6.25%). Notably, 24 of the 25 fastest-appreciating markets were in the Northeast and Midwest.

• Price Declines: On the flip side, 35 of the 100 largest U.S. markets saw home prices decline in 2025 — up from just 10 in 2024 and marking the largest share of declines since 2011.

• Property Type Trends: Single-family homes outperformed condos, with prices rising 1.0% compared to a 1.7% decline for condos. Condos underperformed in 90% of markets nationwide.

Monday, January 05, 2026

"Mortgage Rates Holding at 2-Month Low"

by Calculated Risk on 1/05/2026 07:53:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Holding at 2-Month Low Excerpt:

From Matthew Graham at Mortgage News Daily: Mortgage Rates Holding at 2-Month Low Excerpt:

Bottom line: at current levels, any day that rates spend holding steady or moving microscopically lower will technically result in the lowest rates since October 28th. It would take a more noticeable improvement to break below that floor. When and if that happens, rates will be the lowest since early 2023.[30 year fixed 6.19%]Tuesday:

emphasis added

• No major economic releases scheduled.

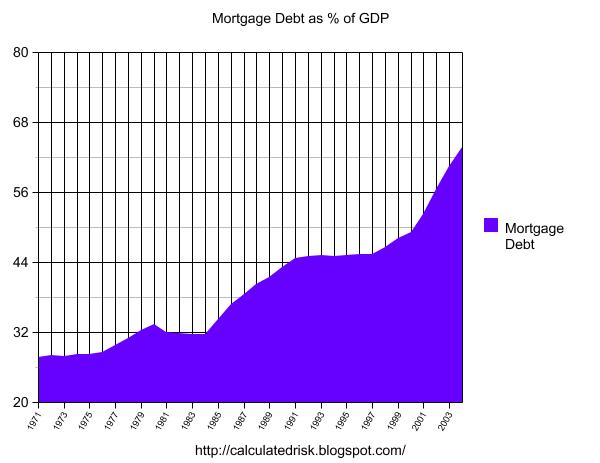

Update: The Housing Bubble and Mortgage Debt as a Percent of GDP

by Calculated Risk on 1/05/2026 02:51:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Update: The Housing Bubble and Mortgage Debt as a Percent of GDP

A brief excerpt:

Three years ago, I wrote The Housing Bubble and Mortgage Debt as a Percent of GDP. Here is an update to a couple of graphs. The bottom line remains the same: There will not be cascading price declines in this cycle due to distressed sales.There is much more in the article.

In a 2005 post, I included a graph of household mortgage debt as a percent of GDP. Several readers asked if I could update the graph.

First, from February 2005 (21 years ago!):The following chart shows household mortgage debt as a % of GDP. Although mortgage debt has been increasing for years, the last four years have seen a tremendous increase in debt. Last year alone mortgage debt increased close to $800 Billion - almost 7% of GDP. ...And a serious problem is what happened!

Many homeowners have refinanced their homes, in essence using their homes as an ATM.

It wouldn't take a RE bust to impact the general economy. Just a slowdown in both volume (to impact employment) and in prices (to slow down borrowing) might push the general economy into recession. An actual bust, especially with all of the extensive sub-prime lending, might cause a serious problem.

ISM® Manufacturing index Decreased to 47.9% in December; "Lowest Reading of 2025"

by Calculated Risk on 1/05/2026 10:00:00 AM

(Posted with permission). The ISM manufacturing index indicated contraction. The PMI® was at 47.9% in December, down from 48.2% in November. The employment index was at 44.9%, up from 44.0% the previous month, and the new orders index was at 47.7%, up from 47.4%.

From ISM: Manufacturing PMI® at 47.9%

December 2025 ISM® Manufacturing PMI® Report

Economic activity in the manufacturing sector contracted in December for the 10th consecutive month, following a two-month expansion preceded by 26 straight months of contraction, say the nation’s supply executives in the latest ISM® Manufacturing PMI® Report.This suggests manufacturing contracted for the tenth consecutive month in December. This was below the consensus forecast, and employment was very weak and prices very strong.

The report was issued today by Susan Spence, MBA, Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee.

“The Manufacturing PMI® registered 47.9 percent in December, a 0.3-percentage point decrease compared to the reading of 48.2 percent in November and the lowest reading of 2025. The overall economy continued in expansion for the 68th month after one month of contraction in April 2020. (A Manufacturing PMI® above 42.3 percent, over a period of time, generally indicates an expansion of the overall economy.) The New Orders Index contracted for a fourth straight month in December following one month of growth; the figure of 47.7 percent is 0.3 percentage point higher than the 47.4 percent recorded in November. The December reading of the Production Index (51 percent) is 0.4 percentage point lower than November’s figure of 51.4 percent. The Prices Index remained in expansion (or ‘increasing’ territory), registering 58.5 percent, the same as November’s reading. The Backlog of Orders Index registered 45.8 percent, up 1.8 percentage points compared to the 44 percent recorded in November. The Employment Index registered 44.9 percent, up 0.9 percentage point from November’s figure of 44 percent.

emphasis added

Housing January 5th Weekly Update: Inventory Down 2.2% Week-over-week

by Calculated Risk on 1/05/2026 08:11:00 AM

Altos reports that active single-family inventory was down 2.2% week-over-week.

Note that Inventory usually bottoms seasonally in January or February.

The first graph shows the seasonal pattern for active single-family inventory since 2015.

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025. The black line is for 2019.

Inventory was up 13.3% compared to the same week in 2025 (last week it was up 13.1%), and down 6.0% compared to the same week in 2019 (last week it was down 11.8%).

Inventory started 2026 down almost 12% compared to 2019.

This second inventory graph is courtesy of Altos Research.

This second inventory graph is courtesy of Altos Research.

As of January 2nd, inventory was at 720 thousand (7-day average), compared to 736 thousand the prior week.

Mike Simonsen discusses this data and much more regularly on YouTube

Sunday, January 04, 2026

Sunday Night Futures

by Calculated Risk on 1/04/2026 06:13:00 PM

Weekend:

• Schedule for Week of January 4, 2026

Monday:

• Early, Light vehicle sales for December. The consensus is for 15.5 million SAAR in December, down from 15.6 million SAAR in November (Seasonally Adjusted Annual Rate).

• At 10:00 AM ET, ISM Manufacturing Index for December. The consensus is for 48.3%, up from 48.2%.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are mostly unchanged (fair value).

Oil prices were moxed over the last week with WTI futures at $57.32 per barrel and Brent at $60.75 per barrel. A year ago, WTI was at $75, and Brent was at $77 - so WTI oil prices are down about 24% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.77 per gallon. A year ago, prices were at $3.04 per gallon, so gasoline prices are down $0.27 year-over-year.

Update: Lumber Prices Mostly Unchanged Year-over-year

by Calculated Risk on 1/04/2026 08:12:00 AM

Here is another update on lumber prices.

NOTE: The CME group discontinued the Random Length Lumber Futures contract on May 16, 2023. I switched to a physically-delivered Lumber Futures contract that was started in August 2022. Unfortunately, this impacts long term price comparisons since the new contract was priced about 24% higher than the old random length contract for the period when both contracts were available.

This graph shows CME random length framing futures through August 2022 (blue), and the new physically-delivered Lumber Futures (LBR) contract starting in August 2022 (Red).

On January 2, 2026, LBR was at $534.00 per 1,000 board feet, down 1.6% from a year ago.

Click on graph for larger image.

Click on graph for larger image.There is somewhat of a seasonal demand for lumber, and lumber prices frequently peak in the first half of the year.

The pickup in early 2018 was due to the Trump lumber tariffs in 2017. There were huge increases during the pandemic due to a combination of supply constraints and a pickup in housing starts.

Now, even with the tariffs, prices are mostly unchanged year-over-year suggesting weak demand for framing lumber.

Saturday, January 03, 2026

Real Estate Newsletter Articles this Week: Case-Shiller House Prices up 1.4% YoY

by Calculated Risk on 1/03/2026 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Case-Shiller: National House Price Index Up 1.4% year-over-year in October

• FHFA’s Q3 National Mortgage Database: Outstanding Mortgage Rates, LTV and Credit Scores

• Freddie Mac House Price Index Up 1.0% Year-over-Year in November

• Inflation Adjusted House Prices 2.7% Below 2022 Peak

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of January 4, 2026

by Calculated Risk on 1/03/2026 08:11:00 AM

The key reports this week are the December employment report and Housing Starts for September and October.

Other key indicators include the November Trade Deficit, November Job Openings, December ISM Manufacturing and December Vehicle Sales.

Early: Light vehicle sales for December.

Early: Light vehicle sales for December.The consensus is for 15.5 million SAAR in December, down from 15.6 million SAAR in November (Seasonally Adjusted Annual Rate).

This graph shows light vehicle sales since the BEA started keeping data in 1967.

The dashed line is the current sales rate.

10:00 AM: ISM Manufacturing Index for December. The consensus is for 48.3%, up from 48.2%.

----- Tuesday, January 6th -----

No major economic releases scheduled.

----- Wednesday, January 7th -----

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index. This will be two weeks of data.

8:15 AM: The ADP Employment Report for December. This report is for private payrolls only (no government). The consensus is for 50,000, up from -32,000 jobs added in November.

10:00 AM ET: Job Openings and Labor Turnover Survey for November from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for November from the BLS.

This graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings increased in October to 7.67 million from 7.66 million in September.

10:00 AM: the ISM Services Index for December.

----- Thursday, January 8th -----

8:30 AM: Trade Balance report for November from the Census Bureau.

8:30 AM: Trade Balance report for November from the Census Bureau.

This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $59.4 billion. The U.S. trade deficit was at $52.8 billion in September.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 205K, up from 199K.

----- Friday, January 9th -----

8:30 AM: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.

8:30 AM: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.

There were 64,000 jobs added in November, and the unemployment rate was at 4.6%.

This graph shows the jobs added per month since January 2021.

10:00 AM: Housing Starts for September and October.

10:00 AM: Housing Starts for September and October.

This graph shows single and total housing starts since 2000.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for January)

12:00 PM: Q3 Flow of Funds Accounts of the United States from the Federal Reserve.

10:00 AM: ISM Manufacturing Index for December. The consensus is for 48.3%, up from 48.2%.

No major economic releases scheduled.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index. This will be two weeks of data.

8:15 AM: The ADP Employment Report for December. This report is for private payrolls only (no government). The consensus is for 50,000, up from -32,000 jobs added in November.

10:00 AM ET: Job Openings and Labor Turnover Survey for November from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for November from the BLS. This graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings increased in October to 7.67 million from 7.66 million in September.

10:00 AM: the ISM Services Index for December.

8:30 AM: Trade Balance report for November from the Census Bureau.

8:30 AM: Trade Balance report for November from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $59.4 billion. The U.S. trade deficit was at $52.8 billion in September.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 205K, up from 199K.

8:30 AM: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.

8:30 AM: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.There were 64,000 jobs added in November, and the unemployment rate was at 4.6%.

This graph shows the jobs added per month since January 2021.

10:00 AM: Housing Starts for September and October.

10:00 AM: Housing Starts for September and October. This graph shows single and total housing starts since 2000.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for January)

12:00 PM: Q3 Flow of Funds Accounts of the United States from the Federal Reserve.

Friday, January 02, 2026

Inflation Adjusted House Prices 2.7% Below 2022 Peak

by Calculated Risk on 1/02/2026 11:12:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 2.7% Below 2022 Peak

Excerpt:

It has almost 20 years since the housing bubble peak, ancient history for many readers!There is much more in the article!

In the October Case-Shiller house price index released Tuesday, the seasonally adjusted National Index (SA), was reported as being 78% above the bubble peak. However, in real terms, the National index (SA) is about 9.7% above the bubble peak (and historically there has been an upward slope to real house prices). The composite 20, in real terms, is 1.1% above the bubble peak.

...

People usually graph nominal house prices, but it is also important to look at prices in real terms. As an example, if a house price was $300,000 in January 2010, the price would be $448,000 today adjusted for inflation (49% increase). That is why the second graph below is important - this shows "real" prices.br />

The third graph shows the price-to-rent ratio, and the fourth graph is the affordability index. The last graph shows the 5-year real return based on the Case-Shiller National Index.

...

The second graph shows the same two indexes in real terms (adjusted for inflation using CPI).

In real terms (using CPI), the National index is 2.7% below the recent peak, and the Composite 20 index is 3.0% below the recent peak in 2022.

Both the real National index and the Comp-20 index increased in October. This was the first increase in the real National index has in 10 months.

It has now been 41 months since the real peak in house prices. Typically, after a sharp increase in prices, it takes a number of years for real prices to reach new highs (see House Prices: 7 Years in Purgatory)

Question #1 for 2026: How much will the economy grow in 2026? Will there be a recession in 2026?

by Calculated Risk on 1/02/2026 08:11:00 AM

Earlier I posted some questions on my blog for next year: Ten Economic Questions for 2026. Some of these questions concern real estate (inventory, house prices, housing starts, new home sales), and I posted thoughts on those in the newsletter (others like GDP and employment will be on this blog).

I'm adding some thoughts and predictions for each question.

Here is a review of the Ten Economic Questions for 2025.

1) Economic growth: Economic growth was probably close to 2% Q4-over-Q4 in 2025. The FOMC is expecting growth of 2.1% to 2.5% Q4-over-Q4 in 2026. How much will the economy grow in 2026? Will there be a recession in 2026?

A year ago, I argued that "Looking at 2025, a recession is mostly off the table." I did go on recession watch during 2025 due to the tariffs, but I noted I wasn't forecasting a recession.

Even though job growth will likely be sluggish in 2026, fiscal policy will be supportive of economic growth and there will be some boost from a rebound from the government shutdown. So, I think a recession in 2026 is very unlikely. Of course there are always exogenous events such as another pandemic, super volcanoes, a major meteor strike or even nuclear war.

It is possible that we will see a pull back in AI and data center investing, and that might negatively impact growth, but that would likely be a 2027 story. It is very likely that many of the tariffs will be ruled illegal (they clearly are illegal), but the Administration has other tools to enact tariffs (more economic uncertainty).

I've expressed concern about unregulated or poorly regulated areas of finance leading to another financial crisis, but that takes a few years to happen.

Here is a table of the annual change in real GDP since 2005. Note: This table includes both annual change and Q4 over the previous Q4 (two slightly different measures).

| Real GDP Growth | ||

|---|---|---|

| Year | Annual GDP | Q4 / Q4 |

| 2005 | 3.5% | 3.0% |

| 2006 | 2.8% | 2.6% |

| 2007 | 2.0% | 2.1% |

| 2008 | 0.1% | -2.5% |

| 2009 | -2.6% | 0.1% |

| 2010 | 2.7% | 2.8% |

| 2011 | 1.6% | 1.5% |

| 2012 | 2.3% | 1.6% |

| 2013 | 2.1% | 3.0% |

| 2014 | 2.5% | 2.7% |

| 2015 | 2.9% | 2.1% |

| 2016 | 1.8% | 2.2% |

| 2017 | 2.5% | 3.0% |

| 2018 | 3.0% | 2.1% |

| 2019 | 2.6% | 3.4% |

| 2020 | -2.1% | -0.9% |

| 2021 | 6.2% | 5.8% |

| 2022 | 2.5% | 1.3% |

| 2023 | 2.9% | 3.4% |

| 2024 | 2.8% | 2.4% |

| 20251 | 2.1% | 2.1% |

| 1 2025 estimate | ||

Real GDP growth is a combination of labor force growth and productivity.

Productivity varies and is difficult to predict, but the labor force growth will likely be sluggish in 2026. So, my guess is that real annual GDP growth will be less than the FOMC expects, perhaps close to 2%.

• Question #1 for 2026: How much will the economy grow in 2026? Will there be a recession in 2026?

• Question #2 for 2026: How much will job growth slow in 2026? Or will the economy lose jobs?

• Question #3 for 2026: What will the unemployment rate be in December 2026?

• Question #4 for 2026: What will the participation rate be in December 2026?

• Question #5 for 2026: What will the YoY core inflation rate be in December 2026?

• Question #6 for 2026: What will the Fed Funds rate be in December 2026?

• Question #7 for 2026: How much will wages increase in 2026?

• Question #8 for 2026: How much will Residential investment change in 2026? How about housing starts and new home sales in 2026?

• Question #9 for 2026: What will happen with house prices in 2026?

• Question #10 for 2026: Will inventory increase further in 2026?