RSS Feed

RSS Feed by Calculated Risk on 10/31/2022 08:57:00 PM

Monday, October 31, 2022

Tuesday: ISM Mfg, Construction Spending, Vehicle Sales

From Matthew Graham at Mortgage News Daily: Mortgage Rates Slightly Higher To Start The Week. More Volatility Ahead

From Matthew Graham at Mortgage News Daily: Mortgage Rates Slightly Higher To Start The Week. More Volatility Ahead

Mortgage rates are fresh off their best week since at least July and their best winning streak (in terms of consecutive days moving lower) in well over a year. The price of admission happened to be the highest rates in more than 20 years, so the recent improvements were really nothing more than a balancing act. ... [30 year fixed 7.13%]Tuesday:

emphasis added

• At 8:00 AM ET, Corelogic House Price index for September.

• At 10:00 AM, ISM Manufacturing Index for October. The consensus is for 49.9, down from 50.9.

• Also at 10:00 AM, Construction Spending for September. The consensus is for 0.5% decrease in spending.

• Late, Light vehicle sales for October. The consensus is for sales of 14.3 million SAAR, up from 13.5 million SAAR in September (Seasonally Adjusted Annual Rate).

Fannie Mae: Mortgage Serious Delinquency Rate Decreased in September

by Calculated Risk on 10/31/2022 04:47:00 PM

Fannie Mae reported that the Single-Family Serious Delinquency decreased to 0.69% in September from 0.72% in August. The serious delinquency rate is down from 1.62% in September 2021. This is close to pre-pandemic levels.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59% following the housing bubble and peaked at 3.32% in August 2020 during the pandemic.

Click on graph for larger image

Click on graph for larger image

By vintage, for loans made in 2004 or earlier (1% of portfolio), 2.41% are seriously delinquent (down from 2.48% in August).

For loans made in 2005 through 2008 (1% of portfolio), 3.83% are seriously delinquent (down from 3.95%),

For recent loans, originated in 2009 through 2021 (98% of portfolio), 0.55% are seriously delinquent (down from 0.57%). So, Fannie is still working through a few poor performing loans from the bubble years.

Mortgages in forbearance were counted as delinquent in this monthly report, but they were not reported to the credit bureaus.

Freddie Mac reported earlier.

Mortgages in forbearance were counted as delinquent in this monthly report, but they were not reported to the credit bureaus.

Freddie Mac reported earlier.

Q3 2022 GDP Details on Residential and Commercial Real Estate

by Calculated Risk on 10/31/2022 02:46:00 PM

The BEA released the underlying details for the Q3 advance GDP report on Friday.

The BEA reported that investment in non-residential structures increased at a 3.7% annual pace in Q3. Investment in petroleum and natural gas structures increased in Q3 compared to Q2 and was up 22% year-over-year.

The first graph shows investment in offices, malls and lodging as a percent of GDP.

Investment in offices (blue) increased slightly in Q3 and was down 1.3% year-over-year. And still declining as a percent of GDP.

Investment in multimerchandise shopping structures (malls) peaked in 2007 and was up about 16% year-over-year in Q3 - from a very low level. The vacancy rate for malls is still very high, so investment will probably stay low for some time.

Lodging investment increased in Q3 compared to Q2, and lodging investment was up 6% year-over-year.

All three sectors - offices, malls, and hotels - were hurt significantly by the pandemic.

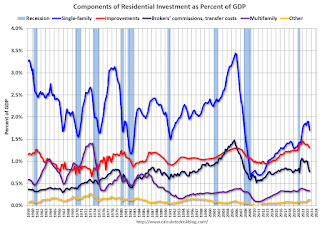

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single-family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single-family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

Investment in single family structures was $438 billion (SAAR) (about 1.7% of GDP) and was unchanged year-over-year.

Investment in multi-family structures was up in Q3 from Q2.

Investment in home improvement was at a $335 billion Seasonally Adjusted Annual Rate (SAAR) in Q3 (about 1.3% of GDP). Home improvement spending was strong during the pandemic but has declined as a percent of GDP recently.

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single-family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).

The second graph is for Residential investment components as a percent of GDP. According to the Bureau of Economic Analysis, RI includes new single-family structures, multifamily structures, home improvement, Brokers’ commissions and other ownership transfer costs, and a few minor categories (dormitories, manufactured homes).Investment in single family structures was $438 billion (SAAR) (about 1.7% of GDP) and was unchanged year-over-year.

Investment in multi-family structures was up in Q3 from Q2.

Investment in home improvement was at a $335 billion Seasonally Adjusted Annual Rate (SAAR) in Q3 (about 1.3% of GDP). Home improvement spending was strong during the pandemic but has declined as a percent of GDP recently.

Note that Brokers' commissions (black) increased sharply as existing home sales increased in the second half of 2020 but was down in Q3 2022. Brokers' commissions were down 15% year-over-year in Q3 (and down sharply as a percent of GDP).

Year-over-year Pace of Rent Increases Continues to Slow

by Calculated Risk on 10/31/2022 09:52:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Year-over-year Pace of Rent Increases Continues to Slow

A brief excerpt:

Here is a graph of the year-over-year (YoY) change for these measures since January 2015. All of these measures are through September 2022 (Apartment List through October 2022).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Note that new lease measures (Zillow, Apartment List) dipped early in the pandemic, whereas the BLS measures were steady. Then new leases took off, and the BLS measures are picking up.

...

The Zillow measure is up 10.8% YoY in September, down from 12.3% YoY in August. This is down from a peak of 17.2% YoY in February.

The ApartmentList measure is up 5.9% YoY as of October, down from 7.5% in September. This is down from the peak of 18.0% YoY last November.

Rents are still increasing YoY, and we should expect this to continue to spill over into measures of inflation. The Owners’ Equivalent Rent (OER) was up 6.7% YoY in September, from 6.3% YoY in August - and will likely increase further in the coming months even as rents slow sharply.

...

My suspicion is rent increases will slow further over the coming months as the pace of household formation slows, and more supply comes on the market. Housing economist Tom Lawler recently wrote: "An actual decline in rents next year would be a reasonable base case"

Housing October 31st Weekly Update: Inventory Increased, New High for 2022

by Calculated Risk on 10/31/2022 08:42:00 AM

Active inventory increased again, hitting another new peak for the year. Here are the same week inventory changes for the last four years (usually inventory is declining at this time of year):

2022: +5.2K (still increasing!)

2021: -9.1K

2020: -6.6K

2019: -9.9K

Inventory bottomed seasonally at the beginning of March 2022 and is now up 139% since then. Altos reports inventory is up 0.9% week-over-week.

Click on graph for larger image.

Click on graph for larger image.

This inventory graph is courtesy of Altos Research.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of October 28th, inventory was at 577 thousand (7-day average), compared to 572 thousand the prior week.

Compared to the same week in 2021, inventory is up 39.5% from 414 thousand, and compared to the same week in 2020 inventory is up 6.3% from 543 thousand. Compared to 3 years ago, inventory is down 37.2% from 919 thousand.

Here are the inventory milestones I’ve been watching for with the Altos data:

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 37.2%).

1. The seasonal bottom (happened on March 4, 2022, for Altos) ✅

2. Inventory up year-over-year (happened on May 20, 2022, for Altos) ✅

3. Inventory up compared to 2020 (happened on October 7, 2022, for Altos) ✅

4. Inventory up compared to 2019 (currently down 37.2%).

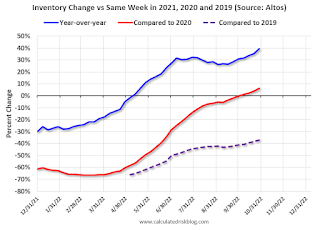

Here is a graph of the inventory change vs 2021 (milestone 2 above), 2020 (milestone 3) and 2019 (milestone 4).

The blue line is the year-over-year data, the red line is compared to two years ago, and dashed purple is compared to 2019.

A key will be if inventory continues to increase in the Fall.

Mike Simonsen discusses this data regularly on Youtube.

Four High Frequency Indicators for the Economy

by Calculated Risk on 10/31/2022 08:29:00 AM

These indicators are mostly for travel and entertainment. It is interesting to watch these sectors recover as the pandemic subsides.

The TSA is providing daily travel numbers.

This data is as of October 30th.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Black), 2021 (Blue) and 2022 (Red).

The dashed line is the percent of 2019 for the seven-day average.

The 7-day average is about at the same level as in 2019 (100.3% of 2019). (Dashed line)

Air travel - as a percent of 2019 - has picked up recently.

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Black is 2020, Blue is 2021 and Red is 2022.

The data is from BoxOfficeMojo through October 27th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $147 million last week, down about 7% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $147 million last week, down about 7% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four-week average. The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

This data is through Oct 22nd. The occupancy rate was down 0.5% compared to the same week in 2019.

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue).

Notes: Y-axis doesn't start at zero to better show the seasonal change.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Purple is for 2021, and Red is for 2022.

As of October 21st, gasoline supplied was down 6.9% compared to the same week in 2019.

Recently gasoline supplied has been running below 2019 and 2021 levels - and sometimes below 2020.

Sunday, October 30, 2022

Sunday Night Futures

by Calculated Risk on 10/30/2022 07:15:00 PM

Weekend:

• Schedule for Week of October 30, 2022

Monday:

• At 9:45 AM ET, Chicago Purchasing Managers Index for October. The consensus is for a reading of 47.2, up from 45.7 in September.

• At 10:00 AM, The Q3 Housing Vacancies and Homeownership report from the Census Bureau.

• At 10:30 AM, Dallas Fed Survey of Manufacturing Activity for October. This is the last regional Fed survey for October.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are down slightly (fair value).

Oil prices were up over the last week with WTI futures at $87.90 per barrel and Brent at $95.77 per barrel. A year ago, WTI was at $84, and Brent was at $84 - so WTI oil prices are up 5% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.72 per gallon. A year ago, prices were at $3.39 per gallon, so gasoline prices are up $0.33 per gallon year-over-year.

FOMC Preview: 75bp Hike

by Calculated Risk on 10/30/2022 10:28:00 AM

Expectations are the FOMC will announce a 75bp rate increase in the federal funds rate at the meeting this week.

From Merrill Lynch:

1 Projections of change in real GDP and inflation are from the fourth quarter of the previous year to the fourth quarter of the year indicated.

The unemployment rate was at 3.5% in September. So far, the economic slowdown has not pushed up the unemployment rate.

2 Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated.

As of September 2022, PCE inflation was up 6.2% from September 2021. This was below the cycle high of 7.0% YoY in June. There was a surge of inflation in Q4 2021, so with less inflation in Q4 this year, it is possible inflation will decline to the projected year-over-year range in Q4.

PCE core inflation was up 5.1% in September year-over-year. This was below the cycle high of 5.4% YoY in February. Core inflation has picked up more than expected and will likely be above the Q4 projected range.

"We expect the Fed to raise its target range for the federal funds rate by 75bp in November ... In our view, based on the median policy rate path as expressed in the September SEPs and communication from some FOMC participants like San Francisco Fed President Mary Daly, the committee is likely to engage in a debate on the appropriateness of slowing the pace of policy rate hikes beginning in December.From Goldman Sachs:

Communicating that the discussion took place should be enough to open the door for a step down to a 50bp rate hike in December, as we currently expect. That said, we expect Chair Powell to say that no decision was taken and the committee remains data dependent. With two employment reports and one CPI report between the November FOMC meeting and the December blackout period, the Fed will be reluctant to pre- commit to a smaller rate hike this far in advance. Data still need to cooperate.

By reaffirming the September median policy rate path, repeating consensus FOMC views that risks to the outlook for inflation still reside to the upside, and emphasizing a willingness to err on the side of tightening to much over tightening too little, we think the Fed can be successful in pushing back against any interpretation that a slower pace of rate hikes implies a lower terminal rate or a quicker pivot to rate cuts. In other words, it is now about the destination, not the journey."

"The FOMC is set to deliver a fourth 75bp hike at its November meeting next week, raising the target range for the fed funds rate to 3.75-4%. The focus will be on what comes next, and we expect Chair Powell to hint that the FOMC will likely slow the pace to 50bp in December ... We expect the FOMC to eventually pair that slowdown to 50bp in December with a somewhat higher projected peak funds rate in the December dot plot. We are adding another 25bp hike to our own forecast—which now calls for hikes of 75bp in November, 50bp in December, 25bp in February, and 25bp in March—and now see the funds rate peaking at 4.75-5%."

Analysts will be looking for comments on the size of future rate hikes.

Projections will NOT be released at this meeting. For review, here are the September projections.

In September, most participants expected seventeen 25bp rate hikes in 2022. The FOMC raised rates 25 bp in March, 50 bp in May, 75 bp in June, 75 bp in July and 75 bp in September. That is twelve 25 bp increases so far, and the Fed expects rates to raise rates 75 bp at this meeting and 50 bp in December.

Current Wall Street forecasts are for GDP to increase slightly in 2022 Q4 over Q4 in line with FOMC projections. For example, BofA is projecting:

Current Wall Street forecasts are for GDP to increase slightly in 2022 Q4 over Q4 in line with FOMC projections. For example, BofA is projecting:

We now forecast GDP growth to slow to 0.2% in 2022 (4Q/4Q) and expect growth to slow to -0.9% in 2023 (4Q/4Q) as the lagged effects of tighter monetary policy and financial conditions cool the economy.

Goldman is tracking real Q4 GDP at a 0.8% annualized rate, that would put Q4/Q4 at 0.3% in 2022.

| GDP projections of Federal Reserve Governors and Reserve Bank presidents, Change in Real GDP1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Sept 2022 | 0.1 to 0.3 | 0.5 to 1.5 | 1.4 to 2.0 | |

| June 2022 | 1.5 to 1.9 | 1.3 to 2.0 | 1.5 to 2.0 | |

The unemployment rate was at 3.5% in September. So far, the economic slowdown has not pushed up the unemployment rate.

| Unemployment projections of Federal Reserve Governors and Reserve Bank presidents, Unemployment Rate2 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Sept 2022 | 3.8 to 3.9 | 4.1 to 4.5 | 4.0 to 4.6 | |

| June 2022 | 3.6 to 3.8 | 3.8 to 4.1 | 3.9 to 4.1 | |

As of September 2022, PCE inflation was up 6.2% from September 2021. This was below the cycle high of 7.0% YoY in June. There was a surge of inflation in Q4 2021, so with less inflation in Q4 this year, it is possible inflation will decline to the projected year-over-year range in Q4.

| Inflation projections of Federal Reserve Governors and Reserve Bank presidents, PCE Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Sept 2022 | 5.3 to 5.7 | 2.6 to 3.5 | 2.1 to 2.6 | |

| June 2022 | 5.0 to 5.3 | 2.4 to 3.0 | 2.0 to 2.5 | |

PCE core inflation was up 5.1% in September year-over-year. This was below the cycle high of 5.4% YoY in February. Core inflation has picked up more than expected and will likely be above the Q4 projected range.

| Core Inflation projections of Federal Reserve Governors and Reserve Bank presidents, Core Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2022 | 2023 | 2024 | |

| Sept 2022 | 4.4 to 4.6 | 3.0 to 3.4 | 2.2 to 2.5 | |

| June 2022 | 4.2 to 4.5 | 2.5 to 3.2 | 2.1 to 2.5 | |

Saturday, October 29, 2022

Real Estate Newsletter Articles this Week: National House Price Index "Continued to Decelerate"

by Calculated Risk on 10/29/2022 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• Case-Shiller: National House Price Index "Continued to Decelerate" to 13.0% year-over-year increase in August

• New Home Sales Decreased in September; Completed Inventory Increased

• Lawler: Update on the Household “Conundrum”

• Inflation Adjusted House Prices 2.3% Below Peak

• Final Look at Local Housing Markets in September

• Lawler: Selected Operating Results, Large Home Builders

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of October 30, 2022

by Calculated Risk on 10/29/2022 08:11:00 AM

Boo!

The key report this week is the October employment report on Friday.

Other key indicators include the October ISM manufacturing and services indexes, October vehicle sales, and the September trade deficit.

The FOMC meets this week and is expected to raise rates 75 bp.

9:45 AM: Chicago Purchasing Managers Index for October. The consensus is for a reading of 47.2, up from 45.7 in September.

10:00 AM: The Q3 Housing Vacancies and Homeownership report from the Census Bureau.

10:30 AM: Dallas Fed Survey of Manufacturing Activity for October. This is the last regional Fed survey for October.

8:00 AM ET: Corelogic House Price index for September.

10:00 AM: ISM Manufacturing Index for October. The consensus is for 49.9, down from 50.9.

10:00 AM: Construction Spending for September. The consensus is for 0.5% decrease in spending.

All day: Light vehicle sales for October.

All day: Light vehicle sales for October.The consensus is for sales of 14.3 million SAAR, up from 13.5 million SAAR in September (Seasonally Adjusted Annual Rate).

This graph shows light vehicle sales since the BEA started keeping data in 1967. The dashed line is the current sales rate.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:15 AM: The ADP Employment Report for October. This report is for private payrolls only (no government). The consensus is for 200,000 jobs added, down from 208,000 in September.

2:00 PM: FOMC Meeting Announcement. The FOMC is expected to raise rates 75bp at this meeting.

2:30 PM: Fed Chair Jerome Powell holds a press briefing following the FOMC announcement.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for an increase to 222 thousand from 217 thousand last week.

8:30 AM: Trade Balance report for September from the Census Bureau. The consensus is for the deficit to be $72.1 billion in September, from $67.4 billion in August.

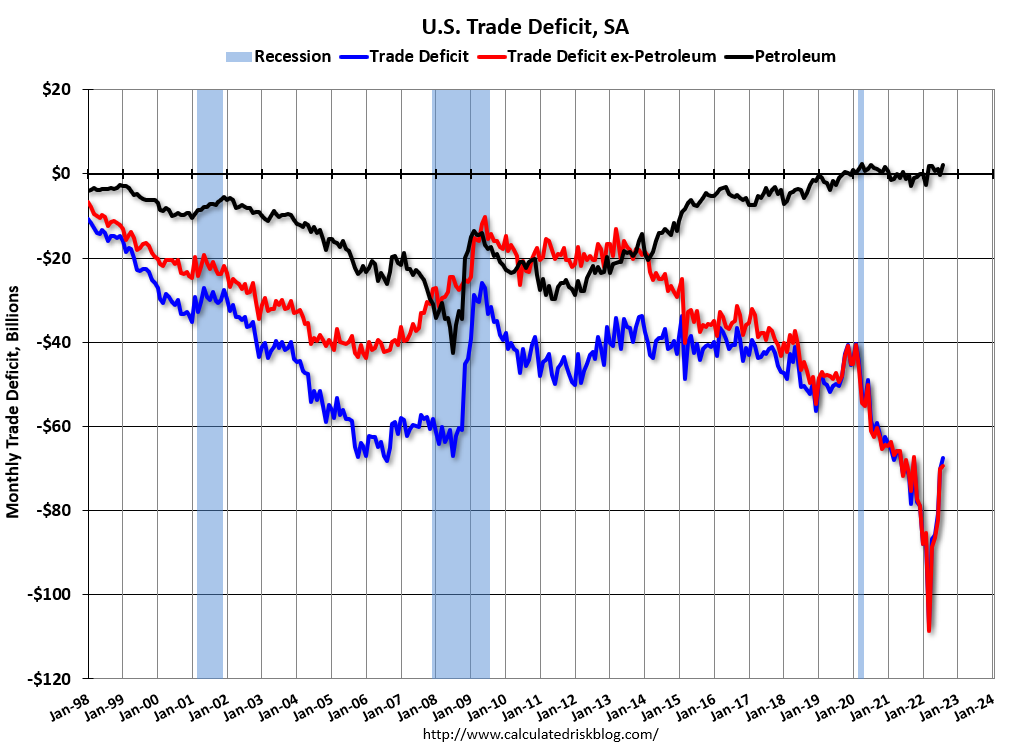

8:30 AM: Trade Balance report for September from the Census Bureau. The consensus is for the deficit to be $72.1 billion in September, from $67.4 billion in August.This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

10:00 AM: the ISM Services Index for October. The consensus is for a decrease to 55.5 from 56.7.

8:30 AM: Employment Report for October. The consensus is for 200,000 jobs added, and for the unemployment rate to increase to 3.6%.

8:30 AM: Employment Report for October. The consensus is for 200,000 jobs added, and for the unemployment rate to increase to 3.6%.There were 263,000 jobs added in September, and the unemployment rate was at 3.5%.

This graph shows the job losses from the start of the employment recession, in percentage terms.

The current employment recession was by far the worst recession since WWII in percentage terms. However, all of the jobs have returned.

Friday, October 28, 2022

COVID Oct 28, 2022: Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 10/28/2022 09:12:00 PM

30-year mortgage rates are close to a 20 year high.

30-year mortgage rates are close to a 20 year high.

NOTE: COVID stats are updated on Fridays.

On COVID (focus on hospitalizations and deaths). Data has switched to weekly.

Weekly deaths bottomed in July 2021 at 1,666.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Week2🚩 | 265,893 | 261,315 | ≤35,0001 | |

| Hospitalized2 | 20,938 | 21,078 | ≤3,0001 | |

| Deaths per Week2🚩 | 2,649 | 2,591 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Cases, Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

Hotels: Occupancy Rate Down 0.5% Compared to Same Week in 2019

by Calculated Risk on 10/28/2022 05:28:00 PM

U.S. hotel performance decreased slightly from the previous week but showed improved comparisons with 2019, according to STR‘s latest data through Oct. 22.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

Oct. 16-22, 2022 (percentage change from comparable week in 2019*):

• Occupancy: 69.9% (-0.5%)

• Average daily rate (ADR): $157.43 (+16.7%)

• Revenue per available room (RevPAR): $110.11 (+16.1%)

Among the Top 25 Markets, Tampa reported the largest increases over 2019 in occupancy (+7.4% to 75.9%) and RevPAR (+39.2% to $117.28). Tampa has been one of the markets in Florida that have seen a performance lift associated with post-Hurricane Ian demand. ...

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019.

emphasis added

Click on graph for larger image.The red line is for 2022, black is 2020, blue is the median, and dashed light blue is for 2021. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is above the median rate for the previous 20 years (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will decline into the Winter.

Lawler: Selected Operating Results, Large Home Builders; Cancellation Rates Increasing Sharply

by Calculated Risk on 10/28/2022 01:42:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Lawler: Selected Operating Results, Large Home Builders

Excerpt:

Below are some selected operating results from some large home builders for last quarter. Note that the sales cancellations number are derived from reported sales cancellations rates and may be off by a bit due to rounding.

Deliveries and Average Sales Price

...

One of the more striking statistics on orders and cancellations was from MDC Holdings, where gross orders totaled 1,569 while sales cancellations totaled 1,270!!!! And in its “Mountain” division (Colorado, Idaho, and Utah), net orders were NEGATIVE 3 homes!

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

NMHC: Survey shows "Apartment Market Softens" in October

by Calculated Risk on 10/28/2022 11:42:00 AM

From the National Multifamily Housing Council (NMHC): Apartment Market Softens, Sales Put on Hold Amidst Rising Rates and Economic Uncertainty

Rising interest rates caused by the Federal Reserve’s ongoing efforts to combat inflation continue to impact the multifamily business. However, it is worth noting that the overall apartment market has begun to revert to pre-pandemic trends as rent growth is decreasing.

Apartment market conditions weakened in the National Multifamily Housing Council (NMHC) Quarterly Survey of Apartment Market Conditions for October 2022, as the Market Tightness (20), Sales Volume (6), Equity Financing (13), and Debt Financing (5) indices all came in well below the breakeven level (50).

“The Fed’s continued interest rate hikes have resulted in higher costs of both debt and equity and a higher degree of economic uncertainty," noted NMHC’s Chief Economist Mark Obrinsky. “This has caused the market for apartment transactions to come to a virtual standstill, as buyers seek a higher rate of return that sellers are unwilling to accommodate via lower prices.”

“The physical apartment market is also starting to normalize after six consecutive quarters of tightening conditions, with a majority of survey respondents reporting higher vacancy and lower rent growth compared to the three months prior.”

...

• Market Tightness Index came in at 20 this quarter — well below the breakeven level (50) — indicating looser market conditions for the first time in six quarters. The majority of respondents (66%) reported markets to be looser than three months ago, while only 5% thought markets have become tighter. The remaining 29% of respondents thought that market conditions were unchanged over the past three months, a considerable decline from the 56% of respondents who said the same in July.

...

It is important to remember that the index does not measure the magnitude of change but, rather, the degree to which respondents agree on the direction of change. For instance, an index value of 0 in market tightness would indicate that all respondents believe market conditions have become looser, but this does not tell us how much looser markets have become.

Click on graph for larger image.

This graph shows the quarterly Apartment Tightness Index. Any reading below 50 indicates looser conditions from the previous quarter.

The quarterly index plunged to 20 in October, from 51 in July.

This index has been an excellent leading indicator for rents and vacancy rates, and this suggests higher vacancy rates and slower rent growth.

NAR: Pending Home Sales Decreased 10.2% in September, Year-over-year Down 31%

by Calculated Risk on 10/28/2022 10:03:00 AM

From the NAR: Pending Home Sales Waned 10.2% in September

Pending home sales trailed off for the fourth consecutive month in September, according to the National Association of REALTORS®. All four major regions recorded month-over-month and year-over-year declines in transactions.This was a much larger decline than expected for this index. Note: Contract signings usually lead sales by about 45 to 60 days, so this would usually be for closed sales in October and November.

The Pending Home Sales Index (PHSI), a forward-looking indicator of home sales based on contract signings, slumped 10.2% to 79.5 in September. Year-over-year, pending transactions slid by 31.0%. An index of 100 is equal to the level of contract activity in 2001.

"Persistent inflation has proven quite harmful to the housing market," said NAR Chief Economist Lawrence Yun. "The Federal Reserve has had to drastically raise interest rates to quell inflation, which has resulted in far fewer buyers and even fewer sellers."

...

The Northeast PHSI descended 16.2% from last month to 64.2, a decline of 30.1% from September 2021. The Midwest index retracted 8.8% to 80.7 in September, down 26.7% from one year ago.

The South PHSI faded 8.1% to 97.0 in September, a drop of 30.0% from the prior year. The West index slipped by 11.7% in September to 62.7, down 38.7% from September 2021.

emphasis added

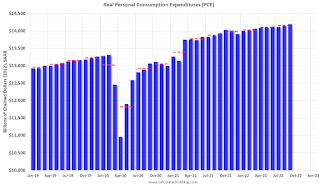

Personal Income increased 0.4% in September; Spending increased 0.6%

by Calculated Risk on 10/28/2022 08:38:00 AM

The BEA released the Personal Income and Outlays report for June:

Personal income increased $78.9 billion (0.4 percent) in September, according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) increased $71.3 billion (0.4 percent) and personal consumption expenditures (PCE) increased $113.0 billion (0.6 percent).The September PCE price index increased 6.2 percent year-over-year (YoY), unchanged 6.2 percent YoY in August, and down from 7.0 percent in June.

The PCE price index increased 0.3 percent. Excluding food and energy, the PCE price index increased 0.5 percent. Real DPI increased less than 0.1 percent in September and Real PCE increased 0.3 percent; goods increased 0.4 percent and services increased 0.3 percent.

emphasis added

The PCE price index, excluding food and energy, increased 5.1 percent YoY, up from 4.9 percent in August.

The following graph shows real Personal Consumption Expenditures (PCE) through September 2022 (2012 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.

The dashed red lines are the quarterly levels for real PCE.

Personal income and the increase in PCE were both above expectations.

The following graph shows real Personal Consumption Expenditures (PCE) through September 2022 (2012 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.The dashed red lines are the quarterly levels for real PCE.

Personal income and the increase in PCE were both above expectations.

Inflation was close to expectations.

Thursday, October 27, 2022

Friday: Personal Income and Outlays, Pending Home Sales

by Calculated Risk on 10/27/2022 08:59:00 PM

From Matthew Graham at MortgageNewsDaily Lowest Mortgage Rates in 3 Weeks

From Matthew Graham at MortgageNewsDaily Lowest Mortgage Rates in 3 Weeks

Friday:

• At 8:30 AM ET, Personal Income and Outlays for September. The consensus is for a 0.3% increase in personal income, and for a 0.4% increase in personal spending. And for the Core PCE price index to increase 0.5%. PCE prices are expected to be up 6.2% YoY, and core PCE prices up 5.2% YoY.

• At 10:00 AM, Pending Home Sales Index for September. The consensus is 5.0% decrease in the index.

• Also at 10:00 AM, University of Michigan's Consumer sentiment index (Final for October). The consensus is for a reading of 59.8.

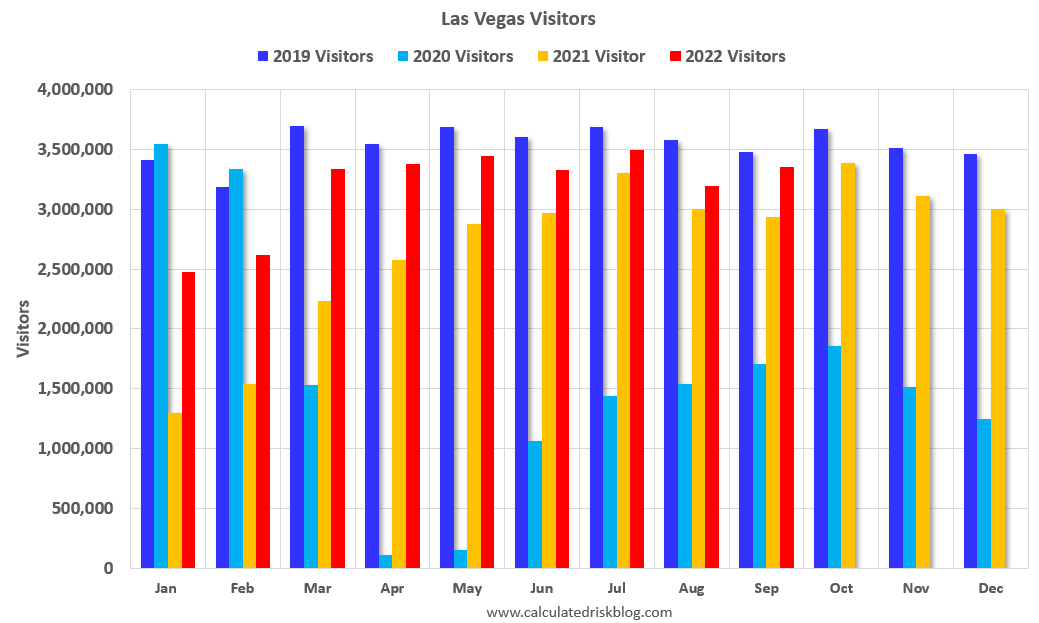

Las Vegas September 2022: Visitor Traffic Down Just 3.5% Compared to 2019

by Calculated Risk on 10/27/2022 02:25:00 PM

Note: I like using Las Vegas as a measure of recovery for both leisure (visitors) and business (conventions).

From the Las Vegas Visitor Authority: August 2022 Las Vegas Visitor Statistics

September saw strong visitation of 3.35M visitors, just ‐3.5% behind September 2019, with notable weekend holidays and events from Labor Day to the Life Is Beautiful festival, the Canelo/GGG fight, Mexican Independence Day, the Raiders/Cardinals home game, Bad Bunny World's Hottest Tour and the iHeartRadio Music festival.

Overall hotel occupancy reached 83.1%, +10.1 pts ahead of last September but down ‐5.2 pts vs. September 2019. Weekend occupancy reached 92.1% (up +3.0 pts YoY but down ‐3.5 pts vs. September 2019), while Midweek occupancy reached 78.6% (up +12.5 pts YoY but down ‐6.5 pts vs. September 2019).

Strong weekend demand supported by major events translated to record monthly ADR levels as September ADR approached $187, +20.1% YoY and +36.5% ahead of September 2019 while RevPAR neared $156 for the month, +36.8% YoY and +28.5% over September 2019

Click on graph for larger image.

Click on graph for larger image. The first graph shows visitor traffic for 2019 (dark blue), 2020 (light blue), 2021 (yellow) and 2022 (red)

Visitor traffic was down 3.5% compared to the same month in 2019.

Visitor traffic was up 14.3% compared to last September.

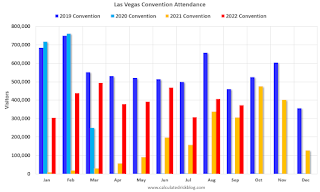

The second graph shows convention traffic.

Convention traffic was down 18.9% compared to August 2019.The second graph shows convention traffic.

Note: There was almost no convention traffic from April 2020 through May 2021.

Realtor.com Reports Weekly Active Inventory Up 36% Year-over-year; New Listings Down 13%

by Calculated Risk on 10/27/2022 12:33:00 PM

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report released today from Chief Economist Danielle Hale: Weekly Housing Trends View — Data Week Ending Oct 22, 2022. Note: They have data on list prices, new listings and more, but this focus is on inventory.

• Active inventory continued to grow, increasing 36% above one year ago. In last week’s Housing Trends View, which marked the first big increase in the active inventory trend since July, we gave a helpful summary of the historical context and timing of recent inventory developments. This week we saw another sizable step up in the active inventory trend (from 34% last week to 36% this week), even as new listings remain low, and the driving factor is the same: climbing mortgage rates, which were very near 7% last week and are likely to top that mark this week.

...

• New listings–a measure of sellers putting homes up for sale–were again down, dropping 13% from one year ago. This week marks the sixteenth straight week of year over year declines in the number of new listings coming up for sale. This week’s decline was somewhat smaller than last week’s, but still means fewer fresh options for home shoppers in the market. Seasonally, fewer homeowners contemplate a home sale as the temperature cools and the holidays approach, but this kind of change in the year over year trend signals a cooling that’s more than just seasonal.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Note the rapid increase in the YoY change earlier this year, from down 30% at the beginning of the year, to up 29% YoY at the beginning of July.

Then the Realtor.com data was stuck at up around 26% to 30% YoY for 14 weeks in a row. This was due to the slowdown in new listings, even as sales had fallen sharply.

Now YoY inventory is increasing again with even higher mortgage rates, suggesting sales are off more than new listings.

Inflation Adjusted House Prices 2.3% Below Peak

by Calculated Risk on 10/27/2022 10:12:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 2.3% Below Peak

Excerpt:

It has been over 16 years since the bubble peak. In the Case-Shiller release Tuesday, the seasonally adjusted National Index (SA), was reported as being 64% above the bubble peak in 2006. However, in real terms, the National index (SA) is about 13% above the bubble peak (and historically there has been an upward slope to real house prices). The composite 20, in real terms, is about 4% above the bubble peak.

Both indexes have declined for three consecutive months in real terms (inflation adjusted).

People usually graph nominal house prices, but it is also important to look at prices in real terms. As an example, if a house price was $200,000 in January 2000, the price would be almost $338,000 today adjusted for inflation (69% increase). That is why the second graph below is important - this shows "real" prices. ...

The second graph shows the same two indexes in real terms (adjusted for inflation using CPI less Shelter). Note: some people use other inflation measures to adjust for real prices. In real terms, the National index is 2.3% below the recent peak, and the Composite 20 index is 3.0% below the recent peak in early 2006.

In real terms, house prices are still above the bubble peak levels. There is an upward slope to real house prices, and it has been over 16 years since the previous peak, but real prices are historically high.

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Weekly Initial Unemployment Claims increase to 217,000

by Calculated Risk on 10/27/2022 08:39:00 AM

The DOL reported:

In the week ending October 22, the advance figure for seasonally adjusted initial claims was 217,000, an increase of 3,000 from the previous week's unrevised level of 214,000. The 4-week moving average was 219,000, an increase of 6,750 from the previous week's unrevised average of 212,250.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 219,000.

The previous week was unrevised.

Weekly claims were lower than the consensus forecast.

BEA: Real GDP increased at 2.6% Annualized Rate in Q3

by Calculated Risk on 10/27/2022 08:34:00 AM

From the BEA: Gross Domestic Product, Third Quarter 2022 (Advance Estimate)

Real gross domestic product (GDP) increased at an annual rate of 2.6 percent in the third quarter of 2022, according to the "advance" estimate released by the Bureau of Economic Analysis. In the second quarter, real GDP decreased 0.6 percent. ...PCE increased at a 1.4% rate, and residential investment decreased at a 26.4% rate. The advance Q3 GDP report, with 2.6% annualized increase, was above expectations.

The increase in real GDP reflected increases in exports, consumer spending, nonresidential fixed investment, federal government spending, and state and local government spending, that were partly offset by decreases in residential fixed investment and private inventory investment. Imports, which are a subtraction in the calculation of GDP, decreased.

The increase in exports reflected increases in both goods and services. Within exports of goods, the leading contributors to the increase were industrial supplies and materials (notably petroleum and products as well as other nondurable goods), and nonautomotive capital goods. Within exports of services, the increase was led by travel and "other" business services (mainly financial services). Within consumer spending, an increase in services (led by health care and "other" services) was partly offset by a decrease in goods (led by motor vehicles and parts as well as food and beverages). Within nonresidential fixed investment, increases in equipment and intellectual property products were partly offset by a decrease in structures. The increase in federal government spending was led by defense spending. The increase in state and local government spending primarily reflected an increase in compensation of state and local government employees.

Within residential fixed investment, the leading contributors to the decrease were new single-family construction and brokers' commissions. The decrease in private inventory investment primarily reflected a decrease in retail trade (led by "other" retailers). Within imports, a decrease in imports of goods (notably consumer goods) was partly offset by an increase in imports of services (mainly travel).

Real GDP turned up in the third quarter, increasing 2.6 percent after decreasing 0.6 percent in the second quarter. The upturn primarily reflected a smaller decrease in private inventory investment, an acceleration in nonresidential fixed investment, and an upturn in federal government spending that were partly offset by a larger decrease in residential fixed investment and a deceleration in consumer spending. Imports turned down.

emphasis added

I'll have more later ...

Wednesday, October 26, 2022

Thursday: GDP, Unemployment Claims, Durable Goods

by Calculated Risk on 10/26/2022 08:29:00 PM

On Q3 GDP from Goldman: "The September new home sales and inventory data were slightly better than our previous assumptions on net, and we boosted our Q3 GDP tracking estimate by one tenth to +2.5% (qoq ar) ahead of tomorrow’s report."

From BofA: "The trade and inventory data lowered our 3Q GDP tracking estimate from 2.5% q/q saar to 2.0% q/q saar."

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, the initial weekly unemployment claims report will be released. The consensus is for an increase to 225 thousand from 214 thousand last week.

• Also, at 8:30 AM, Gross Domestic Product, 3rd quarter 2022 (advance estimate). The consensus is that real GDP increased 2.4% annualized in Q3, up from -0.6% in Q2.

• Also, at 8:30 AM, Durable Goods Orders for September from the Census Bureau. The consensus is for a 0.5% increase in durable goods orders.

• At 11:00 AM: Kansas City Fed Survey of Manufacturing Activity for October.

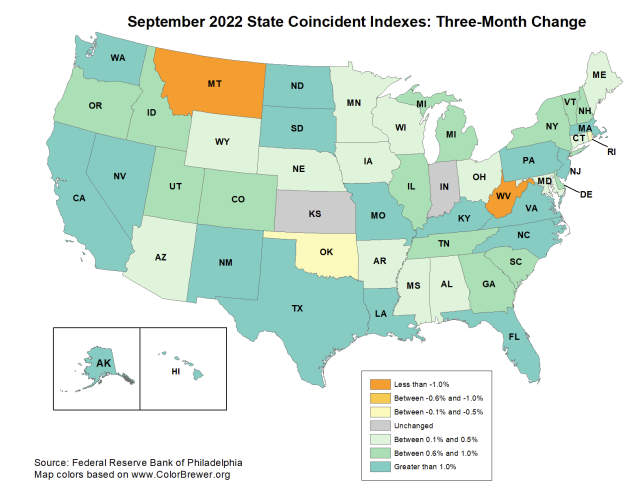

Philly Fed: State Coincident Indexes Increased in 38 States in September

by Calculated Risk on 10/26/2022 01:48:00 PM

From the Philly Fed:

The Federal Reserve Bank of Philadelphia has released the coincident indexes for the 50 states for September 2022. Over the past three months, the indexes increased in 44 states, decreased in four states, and remained stable in two, for a three-month diffusion index of 80. Additionally, in the past month, the indexes increased in 38 states, decreased in 10 states, and remained stable in two, for a one-month diffusion index of 56. For comparison purposes, the Philadelphia Fed has also developed a similar coincident index for the entire United States. The Philadelphia Fed’s U.S. index increased 1.0 percent over the past three months and 0.4 percent in September.Note: These are coincident indexes constructed from state employment data. An explanation from the Philly Fed:

emphasis added

The coincident indexes combine four state-level indicators to summarize current economic conditions in a single statistic. The four state-level variables in each coincident index are nonfarm payroll employment, average hours worked in manufacturing by production workers, the unemployment rate, and wage and salary disbursements deflated by the consumer price index (U.S. city average). The trend for each state’s index is set to the trend of its gross domestic product (GDP), so long-term growth in the state’s index matches long-term growth in its GDP.

Click on map for larger image.

Click on map for larger image.Here is a map of the three-month change in the Philly Fed state coincident indicators. This map was all red during the worst of the Pandemic and also at the worst of the Great Recession.

The map is mostly positive on a three-month basis.

Source: Philly Fed.

And here is a graph is of the number of states with one month increasing activity according to the Philly Fed.

And here is a graph is of the number of states with one month increasing activity according to the Philly Fed. This graph includes states with minor increases (the Philly Fed lists as unchanged).

In September 39 states had increasing activity including minor increases.

In September 39 states had increasing activity including minor increases.

New Home Sales Decreased in September; Completed Inventory Increased

by Calculated Risk on 10/26/2022 10:52:00 AM

Today, in the Calculated Risk Real Estate Newsletter: New Home Sales Decreased in September; Completed Inventory Increased

Brief excerpt:

The next graph shows the months of supply by stage of construction. “Months of supply” is inventory at each stage, divided by the sales rate.You can subscribe at https://calculatedrisk.substack.com/.

There are 1.1 months of completed supply (red line). This is about two-thirds of the normal level.

The inventory of new homes under construction is at 6.0 months (blue line). This elevated level of homes under construction is due to supply chain constraints.

And a record 105 thousand homes have not been started - about 2.1 months of supply (grey line) - about double the normal level. Homebuilders are probably waiting to start some homes until they have a firmer grasp on prices and demand.

...

First, as I discussed last month, the Census Bureau overestimates sales, and underestimates inventory when cancellation rates are rising, see: New Home Sales and Cancellations: Net vs Gross Sales. So, take the headline sales number with a large grain of salt - the actual negative impact on the homebuilders is greater than the headline number suggests!

...

There are a large number of homes under construction, and this suggests we will see a sharp increase in completed inventory over the next several months - and that will put pressure on new home prices.

New Home Sales Decrease to 603,000 Annual Rate in September

by Calculated Risk on 10/26/2022 10:09:00 AM

The Census Bureau reports New Home Sales in September were at a seasonally adjusted annual rate (SAAR) of 603 thousand.

The previous three months were revised down, combined.

Sales of new single‐family houses in September 2022 were at a seasonally adjusted annual rate of 603,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 10.9 percent below the revised August rate of 677,000 and is 17.6 percent below the September 2021 estimate of 732,000.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

New home sales are below pre-pandemic levels.

The second graph shows New Home Months of Supply.

The months of supply increased in September to 9.2 months from 8.1 months in August.

The months of supply increased in September to 9.2 months from 8.1 months in August. The all-time record high was 12.1 months of supply in January 2009. The all-time record low was 3.5 months, most recently in October 2020.

This is well above the top of the normal range (about 4 to 6 months of supply is normal).

"The seasonally‐adjusted estimate of new houses for sale at the end of September was 462,000. This represents a supply of 9.2 months at the current sales rate."

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).In September 2022 (red column), 49 thousand new homes were sold (NSA). Last year, 58 thousand homes were sold in September.

The all-time high for September was 99 thousand in 2005, and the all-time low for September was 24 thousand in 2011.

This was slightly above expectations, however sales in the three previous months were revised down, combined. I'll have more later today.

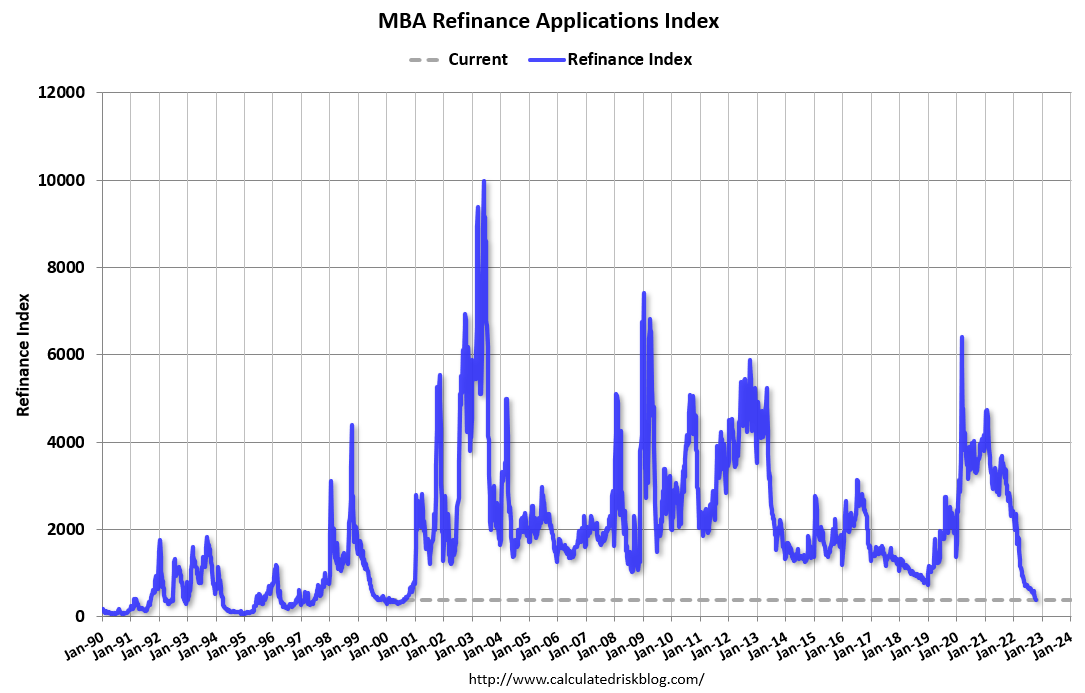

MBA: Mortgage Applications Decrease in Latest Weekly Survey; Lowest Level Since 1997

by Calculated Risk on 10/26/2022 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 1.7 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending October 21, 2022.

... The Refinance Index increased 0.1 percent from the previous week and was 86 percent lower than the same week one year ago. The seasonally adjusted Purchase Index decreased 2 percent from one week earlier. The unadjusted Purchase Index decreased 3 percent compared with the previous week and was 42 percent lower than the same week one year ago.

“Mortgage rates increased for the 10th consecutive week, with the 30-year fixed rate reaching 7.16 percent, the highest rate since 2001. The ongoing trend of rising mortgage rates continues to depress mortgage application activity, which remained at its slowest pace since 1997,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Refinance applications were ess entially unchanged, but purchase applications declined 2 percent to the slowest pace since 2015 – over 40 percent behind last year’s pace. Despite higher rates and lower overall application activity, there was a slight increase in FHA purchase applications, as FHA rates remained lower than conventional loan rates.”

Added Kan, “MBA’s forecast expects both economic and housing market weakness in 2023 to drive a 3 percent decline in purchase originations, while refinance volume is anticipated to decline by 24 percent.

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 7.16 percent from 6.94 percent, with points decreasing to 0.88 from 0.95 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index has declined sharply this year.

The refinance index is at the lowest level since the year 2000.

The second graph shows the MBA mortgage purchase index

According to the MBA, purchase activity is down 42% year-over-year unadjusted.

According to the MBA, purchase activity is down 42% year-over-year unadjusted.The purchase index is 12% below the pandemic low and at the lowest level since 2015.

Note: Red is a four-week average (blue is weekly).

Note: Red is a four-week average (blue is weekly).

Tuesday, October 25, 2022

Wednesday: New Home Sales

by Calculated Risk on 10/25/2022 09:01:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 10:00 AM, New Home Sales for September from the Census Bureau. The consensus is for 590 thousand SAAR, down from 685 thousand in August.

Freddie Mac: Mortgage Serious Delinquency Rate decreased in September

by Calculated Risk on 10/25/2022 04:42:00 PM

Freddie Mac reported that the Single-Family serious delinquency rate in September was 0.67%, down from 0.70% August. Freddie's rate is down year-over-year from 1.46% in September 2021.

Freddie's serious delinquency rate peaked in February 2010 at 4.20% following the housing bubble and peaked at 3.17% in August 2020 during the pandemic.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

Click on graph for larger image

Click on graph for larger image

Mortgages in forbearance are being counted as delinquent in this monthly report but are not reported to the credit bureaus.

The serious delinquency rate was at 0.60% just prior to the pandemic - almost back to that level.

Note that multi-family delinquencies have been increasing and were at 0.13% in September.

Lawler: Update on the Household “Conundrum”

by Calculated Risk on 10/25/2022 02:25:00 PM

Today, in the Real Estate Newsletter: Lawler: Update on the Household “Conundrum”

Excerpt:

This is from housing economist Tom Lawler:There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

The pandemic wreaked havoc on some of the government surveys designed to measure the number of and characteristics of US households (though there were measurement issues before the pandemic), making it difficult for analysts how much of the extraordinary strength in the housing market during 2021 and early 2022 was related to “demographics” as opposed to behavioral and preference changes. (Here is the November 2021 piece on this issue). Nevertheless, it may still be useful to see what these reports are showing.

...

What is striking about the estimated household gain is that it is significantly above – in fact, about double -- what one would have projected if one had assumed that so-called “headship rates” in each age group (the number of householders in an age group divided by the total population of that age group) had remained the same over this period. Moreover, headship rate increases were concentrated in the 15–34-year-old categories.

If in fact over the 12-month period ending March of this year the number of households increased by almost two million, then household growth significantly outpaced housing production, as total housing completions plus manufactured housing shipments totaled only about 1.44 million.

In terms of household growth, there are several reasons to expect that household growth has slowed sharply since the beginning of this year ...

...

If in fact this dynamic shift between household growth and housing production is taking place, then it, combined with (1) the unprecedented increase in housing prices over a 2-year period from mid-2020 to mid-2022, and (2) the unprecedented surge in mortgage rates this year, would suggest that a non-trivial decline in home prices from the middle of this year to at least the middle of next year would be a logical “base case.” This shift, combined with (1) the unprecedented increase in rents from late 2020 to the middle of this year and (2) the significant increase in rental units coming to market over the next year, suggest not only that rent growth should soon decelerate sharply (in fact, some indicators suggest that it already has), but that an actual decline in rents next year would be a reasonable base case.

Comments on August Case-Shiller and FHFA House Prices

by Calculated Risk on 10/25/2022 10:02:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Case-Shiller: National House Price Index "Continued to Decelerate" to 13.0% year-over-year increase in August

Excerpt:

Both the Case-Shiller House Price Index (HPI) and the Federal Housing Finance Agency (FHFA) HPI for August were released today. Here is a graph of the month-over-month (MoM) change in the Case-Shiller National Index Seasonally Adjusted (SA).

The Case-Shiller Home Price Indices for “August” is a 3-month average of June, July and August closing prices. June closing prices include some contracts signed in April, so there is a significant lag to this data.

The MoM decrease in Case-Shiller was at -0.86% seasonally adjusted. This was the second consecutive MoM decrease, and the largest MoM since February 2010. Since this includes closings in June and July, this suggests prices fell sharply for August closings.

On a seasonally adjusted basis, prices declined in all of the Case-Shiller cities on a month-to-month basis. The largest monthly declines seasonally adjusted were in San Francisco (-3.7%), Seattle (-2.9%), and San Diego (-2.5%). San Francisco has fallen 8.2% from the peak in May 2022.

...

The August Case-Shiller report is mostly for contracts signed in the April through July period when 30-year mortgage rates were in the low-to-mid 5% range. The September report will mostly be for contracts signed in the May through August period - when rates were also in the low-to-mid 5% range.

The impact from higher rates in September and October will not show up for several more months.

There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

Case-Shiller: National House Price Index "Continued to Decelerate" to 13.0% year-over-year increase in August

by Calculated Risk on 10/25/2022 09:12:00 AM

S&P/Case-Shiller released the monthly Home Price Indices for August ("August" is a 3-month average of June, July and August closing prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

From S&P: S&P Corelogic Case-Shiller Index Continued to Decelerate in August

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 13.0% annual gain in August, down from 15.6% in the previous month. The 10- City Composite annual increase came in at 12.1%, down from 14.9% in the previous month. The 20- City Composite posted a 13.1% year-over-year gain, down from 16.0% in the previous month.

Miami, Tampa, and Charlotte reported the highest year-over-year gains among the 20 cities in August. Miami led the way with a 28.6% year-over-year price increase, followed by Tampa in second with a 28.0% increase, and Charlotte in third with a 21.3% increase. All 20 cities reported lower price increases in the year ending August 2022 versus the year ending July 2022.

...

Before seasonal adjustment, the U.S. National Index posted a -1.1% month-over-month decrease in August, while the 10-City and 20-City Composites both posted decreases of -1.6%.

After seasonal adjustment, the U.S. National Index posted a month-over-month decrease of -0.9%, and the 10-City and 20-City Composites both posted decreases of -1.3%.

In August, all 20 cities reported declines before and after seasonal adjustments.

“The forceful deceleration in U.S. housing prices that we noted a month ago continued in our report for August 2022,” says Craig J. Lazzara, Managing Director at S&P DJI. “For example, the National Composite Index rose by 13.0% for the 12 months ended in August, down from its 15.6% year-over-year growth in July. The -2.6% difference between those two monthly rates of change is the largest deceleration in the history of the index (with July’s deceleration now ranking as the second largest). We see similar patterns in our 10-City Composite (up 12.1% in August vs. 14.9% in July) and our 20-City Composite (up 13.1% in August vs. 16.0% in July). Further, price gains decelerated in every one of our 20 cities. These data show clearly that the growth rate of housing prices peaked in the spring of 2022 and has been declining ever since.

“Month-over-month comparisons are consistent with these observations. All three composites declined in July, as did prices in every one of our 20 cities. On a month-over-month basis, the biggest declines occurred on the west coast, with San Francisco (-4.3%), Seattle (-3.9%), and San Diego (-2.8%) falling the most.

emphasis added

Click on graph for larger image.

Click on graph for larger image. The first graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index is down 1.3% in August (SA).

The Composite 20 index is down 1.3% (SA) in August.

The National index is 64% above the bubble peak (SA), and down 0.9% (SA) in August. The National index is up 121% from the post-bubble low set in February 2012 (SA).

The second graph shows the year-over-year change in all three indices.

The second graph shows the year-over-year change in all three indices.The Composite 10 SA is up 12.1% year-over-year. The Composite 20 SA is up 13.1% year-over-year.

The National index SA is up 13.0% year-over-year.

Price increases were lower than expectations. I'll have more later.

Monday, October 24, 2022

Tuesday: Case-Shiller and FHFA House Prices, Richmond Fed Mfg

by Calculated Risk on 10/24/2022 08:54:00 PM

From Matthew Graham at Mortgage News Daily: A Rare Winning Streak For Rates, But Don't Get Excited

From Matthew Graham at Mortgage News Daily: A Rare Winning Streak For Rates, But Don't Get Excited

Now here's a rare thing! Mortgage rates managed to move lower, on average, for the 2nd consecutive business day on Monday. That hasn't happened for roughly 3 weeks, and you'd need to go back another 3 weeks to see the previous example. ... [30 year fixed 7.29%]Tuesday:

emphasis added

• At 9:00 AM ET, S&P/Case-Shiller House Price Index for August. The consensus is for the Composite 20 index to be up 16.1% year-over-year.

• Also at 9:00 AM, FHFA House Price Index for August. This was originally a GSE only repeat sales, however there is also an expanded index.

• At 10:00 AM, Richmond Fed Survey of Manufacturing Activity for October.

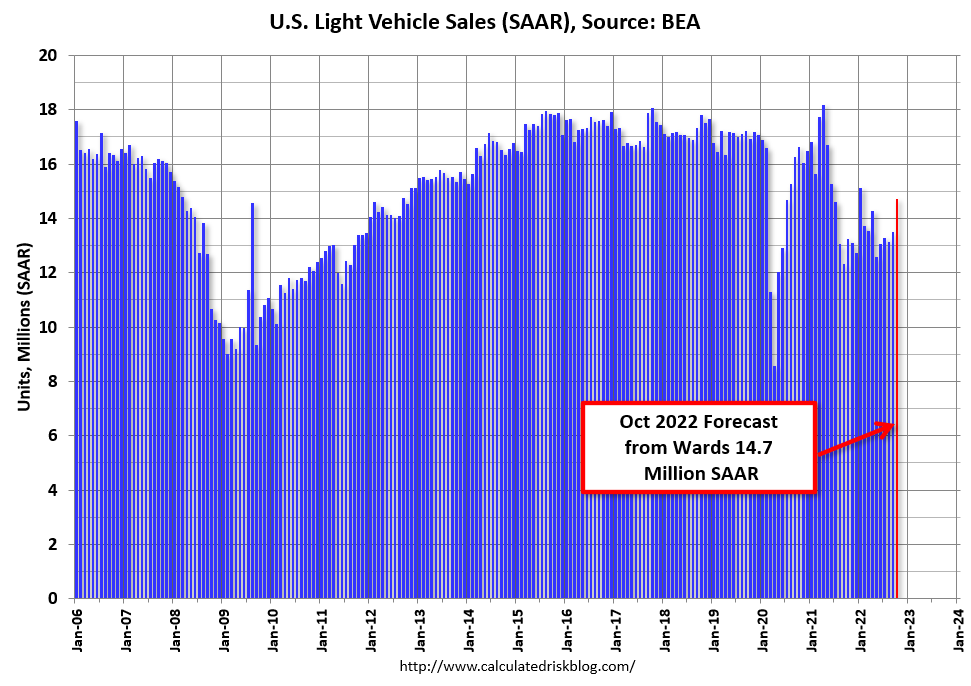

October Vehicle Sales Forecast: "Signs of Life"

by Calculated Risk on 10/24/2022 01:54:00 PM

From WardsAuto: October U.S. Light-Vehicle Sales Show Signs of Life (pay content). Brief excerpt:

"The fourth-quarter SAAR is pegged at 14.2 million units, an improvement on Q2’s 13.3 million and Q3’s 13.4 million, but also meaning November-December results will weaken from October, with the primary reason being stiffer economic headwinds expected. Still, inventory will continue rising through the end of November, creating upside to the outlook"

Click on graph for larger image.

Click on graph for larger image.This graph shows actual sales from the BEA (Blue), and Wards forecast for October (Red).

The Wards forecast of 14.7 million SAAR, would be up 9% from last month, and up 11% from a year ago (sales weakened in the second half of 2021, due to supply chain issues).

Vehicle sales are usually a transmission mechanism for Federal Open Market Committee (FOMC) policy, far behind housing. However, this time, vehicle sales have been suppressed by supply chain issues, and sales will probably not be significantly impacted by higher interest rates.

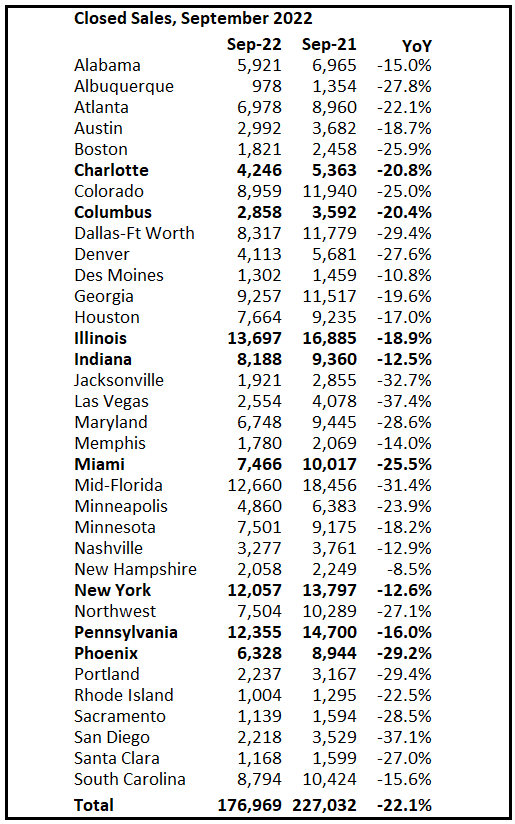

Final Look at Local Housing Markets in September

by Calculated Risk on 10/24/2022 11:36:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Final Look at Local Housing Markets in September

A brief excerpt:

The big story for September existing home sales was the sharp year-over-year (YoY) decline in sales. Another key story was that new listings were down YoY in September as many potential sellers are locked into their current home (low mortgage rate).There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/

This is the final look at local markets in September. I’m tracking about 35 local housing markets in the US. Some of the 35 markets are states, and some are metropolitan areas. I update these tables throughout the month as additional data is released.

Important: Closed sales in September were mostly for contracts signed in July and August when 30-year mortgage rates averaged about 5.3%. Rates increased to around 6% in September and that will impact closed sales in October and November. In October 30-year mortgage rates have jumped to over 7%, negatively impacting closed sales in November and December.

...

And a table of September sales. In September, sales were down 22.1% YoY Not Seasonally Adjusted (NSA) for these markets. The NAR reported sales were down 21.6% NSA YoY.

Sales in some of the hottest markets are down around 30% YoY (all of California was down 30%), whereas in other markets, sales are only down in the teens YoY.

More local data coming in November for activity in October! We should expect even larger YoY declines in the next few months due to the recent increase in mortgage rates.

{kind=link}