RSS Feed

RSS Feed by Calculated Risk on 1/31/2008 07:18:00 PM

Thursday, January 31, 2008

Chase: Max HELOC LTV 70% in Certain Areas

From Kathy Kristof and Scott Reckard at the LA Times: Trying to tap into home equity? We'll see

Countrywide Financial Corp. sent letters to 122,000 customers last week telling them they could no longer borrow against their credit lines because the total debt on the home exceeded the market value of the property. ... The move by Countrywide ... is part of a pullback by lenders nationwide on home equity loans ... with new evidence of sinking home values, many lenders are requiring that homeowners maintain a much larger percentage of equity in their homes as a cushion against financial problems.This is an excellent followup to my posts this morning: Advance Q4 MEW Estimate and Lenders Suspending HELOCs

... Chase Home Lending ... will start imposing new guidelines Monday that further restrict who will be granted a home equity line ... This week, California homeowners can tap as much as 90% of the equity in their homes. Starting Monday, however, Chase won't let homeowners in certain parts of the state -- including Los Angeles, Orange and Imperial counties -- borrow more than 70% of the value of their homes.

CR4RE Newsletter: Sign Up Now to Receive February Issue

by Calculated Risk on 1/31/2008 04:35:00 PM

A repeat ...

Tanta and I are starting to write the February CR4RE "Calculated Risk 4 Real Estate". The newsletter should be sent out in a few days.

If you'd like to subscribe, here is the sign up page ($60 for 12 monthly issues).

The January 2008 Newsletter is available free as a sample (858kb PDF file).

We've received some excellent feedback - thanks! - and a number of subscribers commented that we priced the newsletter too low compared to other newsletters. Hey, take advantage of us!

Best Wishes to All.

CRE: Macklowe Cedes Control to Lender

by Calculated Risk on 1/31/2008 04:32:00 PM

Remember this story? Macklowes On a Wire

Mr. Macklowe and his son Billy paid $6.8 billion to buy seven New York buildings from Equity Office Properties Trust. ... Macklowe Properties put in only $50 million of equity and borrowed $7.6 billion, according to the documents. (Mr. Macklowe borrowed more than the purchase price to cover closing costs and other fees.) The deal also had "negative debt service," meaning that the rents from the buildings weren't expected to cover the debt payments for five years ...Macklowe Properties financed nearly $5.1 billion in debt that must be paid back by February...Well, the debt apparently isn't being paid off. Instead, from the WSJ: Macklowe in Deal to Cede Control Of Seven Manhattan Properties

Troubled New York real estate titan Harry Macklowe has reached a tentative agreement with his lender to turn over effective control of seven Manhattan office buildings he triumphantly acquired less than a year ago for $7.2 billion ...Talk about walking away.

S&P Cuts FGIC To AA; MBIA, XLCA On Watch Neg

by Calculated Risk on 1/31/2008 04:14:00 PM

From S&P (no link):

Standard & Poor's Ratings Services today lowered its financial strength, financial enhancement, and issuer credit ratings on Financial Guaranty Insurance Co. to 'AA' from 'AAA' and its senior unsecured and issuer credit ratings on FGIC Corp. to 'A' from 'AA.' Standard & Poor's also placed all the above ratings on CreditWatch with developing implications.Update: And from the WSJ a long time ago (this morning): AAA Rating Will Stand, MBIA Says.

At the same time, Standard & Poor's placed various ratings on MBIA Insurance Corp., XL Capital Assurance Inc., XL Financial Assurance Ltd., and their related entities on CreditWatch with negative implications. The ratings on various related contingent capital facilities were also affected.

Chief Executive Officer Gary Dunton mounted a spirited defense on a conference call, following MBIA's quarterly earnings report, against "fear mongering" and "distortions' that he said have contributed to last year's dramatic stock-price decline. He also said that MBIA's capital plan currently exceeds all stated rating agency requirements.MBIA hasn't been downgraded so far; this is just a move to CreditWatch with negative implications. BTW, I don't think a CEO should ever comment on his company's stock price, only on the performance of the company:

Despite the significant losses posted by the company, Mr. Dunton said, "there is nothing that we can identify that justifies the 80% drop in our stock price since last year."

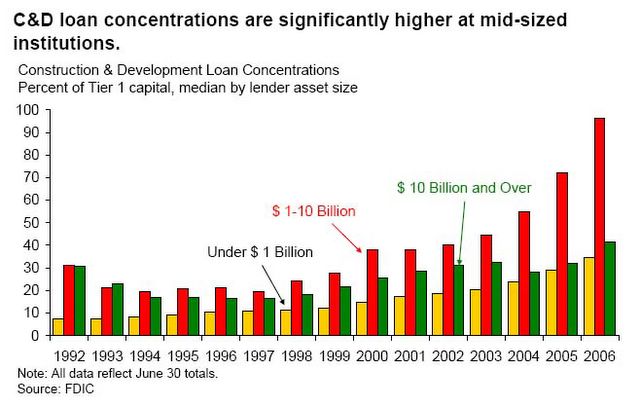

Comptroller Dugan Expresses Concern About CRE Concentrations

by Calculated Risk on 1/31/2008 02:15:00 PM

From the Comptroller of the Currency John C. Dugan: Comptroller Dugan Expresses Concern About Commercial Real Estate Concentrations

Comptroller of the Currency John C. Dugan told a bank conference today that the OCC is focusing increased attention on problems arising from high community bank concentrations in commercial real estate (CRE) at a time of significant market disruptions and declining house and condominium sales and values.As I noted last week, with the failure of Douglass National Bank in Kansas City, the housing bust hasn't hurt most small banks and institutions because the banks didn't hold many of the residential mortgages they originated. Instead the small to mid-sized institutions focused on commercial real estate (CRE) and construction and development (C&D) loans, so rising CRE and C&D defaults will impact community banks much more than rising residential mortgage defaults.

“The combination of these conditions is putting considerable stress on one particular category of commercial real estate lending: residential construction and development – and other categories of CRE loans will feel similar stress if general economic activity slows materially,” Mr. Dugan said in a speech before a meeting of the Florida Bankers Association.

In the area of construction and development (C&D) loans, nonperforming loans in community national banks amounted to 1.96 percent of the total at the end of the third quarter, double the rate of the year before.

“Although starting from an admittedly very low baseline, an increase like this – over 100 percent in a single year – is clearly a trend that we need to monitor closely,” Mr. Dugan said.

...

In recent years, the Comptroller said, banks had become too complacent regarding the potential for significant stresses in these markets, and CRE concentrations rose significantly in many banks. The ratio of commercial real estate loans to capital has nearly doubled in the past six years, he said.

“Even more significant than this overall industry statistic is the number of individual banks that have especially large concentrations,” Mr. Dugan added. “Over a third of the nation’s community banks have commercial real estate concentrations exceeding 300 percent of their capital, and almost 30 percent have construction and development loans exceeding 100 percent of capital.”

...

“In terms of asset quality, our horizontal reviews have indeed confirmed a significant increase in the number of problem residential construction and development loans in community banks across the country,” the Comptroller added.

Note: Dugan was one of the first regulators to express concern about non-traditional mortgages, especially Option ARMs.

Clockwork Mortgages, Again

by Anonymous on 1/31/2008 12:26:00 PM

So far at least a dozen people have emailed me the link to Jonathan Weil's latest egregiousness in Bloomberg. I have no idea how many times it has come up in the comments. My response?

What P.J. said.

Weil's whole argument rests on the original assumption that pools of mortgage loans can be "wind-up toys" or "brain dead" from a servicing perspective. The reality is that they cannot, they are not, and anyone who pretended otherwise was an idiot (I'm lookin' at you, Wall Street). The prohibition on actively managed pools is there to prevent the issuer or servicer from buying and selling loans in and out of the trust and passing through gain-on-sale to investors while calling it "interest income," or securitizing loans with "putback" provisions that mean the issuer can repurchase loans out of the pools whenever it wants to at a price that is below market in order to take advantage of the bondholders. It was never and is not a prohibition on servicing mortgage loans. That is, in fact, what the SEC just said.

There is and has always been the recognition that mortgage loans, unlike, say, Treasury notes, need to be "serviced." There are therefore long and involved servicing agreements and absolutely not trivial servicing fees specified in all these deals. A couple minutes' worth of reflection would lead you to this: perhaps there is a debate about where you cross the line between servicing a pool and managing it. That would be a debate about when "loss mitigation" (working out a loan in order to minimize loss when loss is inevitable) becomes "loss creation" (a servicer creating a loss to the investor in order to increase servicing income or something like that). But to have that debate you'd have to accept that real loss mitigation is acceptable, and you'd have to look at more facts than just the presence of workouts as such. Such a debate doesn't have jack to do with the SEC handing out "accounting favors" to anyone.

I simply hope that someday Weil wants to drop escrows or make a curtailment and get a payment recast or deed off an easement or something on his home mortgage and he calls his servicer and the servicer says, "Sorry, dood. You're brain dead to us. All we do is collect your payment. Have a nice day. Click."

Maybe that has already happened to him, and it's making him bitter. Beats me. All I know is that a bunch of geniuses on Wall Street did, actually, fall for the idea that residential home mortgages were "wind-up toys," just "asset classes" instead of messy complicated things that involve real people (good, bad, and indifferent, lucky and unlucky, high-maintenance and low-maintenance) on the other side of the cash flow, who don't always behave the way your models said they would. And here we are. Demanding that we continue the delusion in order to make the accounting work out is mind-boggling. Demanding that issuers take it all back onto their balance sheets as punishment for trying to mitigate losses to bondholders is beyond perverse.

Bristol-Myers: $275 Million in Mortgage Related Write-Downs

by Calculated Risk on 1/31/2008 11:52:00 AM

From Bloomberg: Bristol-Myers Posts Quarterly Loss on Investments (Hat tip NK)

The company wrote off $275 million in investments in the quarter, which could rise to as much as $417 million, said Rebecca Goldsmith, a spokeswoman for the New York-based drugmaker ...More containment.

``Some of the underlying collateral for the auction rate securities held by the company consists of sub-prime mortgages,'' the company said today in a statement. If credit and capital markets continue to deteriorate, Bristol-Myers said, it ``may incur additional impairments to its investment portfolio, which could negatively affect the company's financial condition, cash flow and reported earnings.''

Lenders Suspending HELOCs

by Calculated Risk on 1/31/2008 10:49:00 AM

In the previous post, I noted that mortgage equity withdrawal (MEW) was apparently still strong in Q4. Unlike previous years, this appears to be the result of homeowners drawing down HELOCs as opposed to cash out refis.

The lenders are starting to be concerned about the risk of homeowners drawing down HELOCs, while at the same time their property value is declining, leaving little or no equity in the home.

The Implode-O-Meter has posted a letter today from Countrywide suspending certain HELOCs.

A portion of HELOC customers have already or will soon be notified by CFC Loan Administration that their HELOC draws have been suspended indefinitely. These HELOCs were identified as candidates for suspensions for various reasons including:Significant decrease in supporting property value – If the customer's current untapped equity (home value minus all mortgage liens) drops by 50% or more from their HELOC opening date, his/her line will be suspended.This is not a one-time event, but an on-going strategy as we continue to manage our lending risk.

HELOC payment delinquency – If the customer's payment is made two or more days after the grace period ends, his/her line will be suspended.

Product Terms/Conditions Violation – In cases where the customer violated terms or conditions of the HELOC Agreement, his/her line will be suspended.

Examples include, but are not limited to: HELOC on property originated as owner occupied, but now believed to be non-owner occupied or unpaid taxes or insurance on the subject property.

Be aware that there may be other actions that could trigger draw suspensions.

Advance Q4 MEW Estimate

by Calculated Risk on 1/31/2008 10:18:00 AM

Based on the Q4 GDP data from the BEA, my advance estimate for Mortgage Equity Withdrawal (MEW) is approximately $145 Billion for Q4 (just under $600 billion on a SAAR) or 5.6% of Disposable Personal Income (DPI). This would be slightly higher than the Q3 estimates, from the Fed's Dr. Kennedy, of $133.0 Billion, or 5.2% of Disposable Personal Income (DPI).

The actual Q3 data for MEW will be released after the Flow of Funds report is available from the Fed (scheduled for March 6, 2008 for Q4).  Click on graph for larger image.

Click on graph for larger image.

This graph compares my advance MEW estimate (as a percent of DPI) with the MEW estimate from Dr. James Kennedy at the Federal Reserve. The correlation is pretty high, but there are differences quarter to quarter. This analysis does suggest that MEW was at about the same level in Q4 2007, as in Q3. We will have to wait until March to know for sure.

MEW had been expected to decline precipitously since mid-summer 2007, with a combination of tighter lending standards and falling house prices. However, in Q3, MEW was supported by homeowners drawing down pre-existing home equity lines of credit (HELOC). The sizable MEW in Q4 was probably related to home equity lines too (as opposed to cash out refis of a couple of years ago).

The impact of less equity extraction on consumer spending is still being debated, but as HELOCs dry up, I believe a slowdown in consumption expenditures is likely.

Another "Significant Discount"

by Anonymous on 1/31/2008 08:34:00 AM

HOUSTON, Jan 31, 2008 (BUSINESS WIRE) -- Oxford Funding Corporation has won the bid and secured financing for the purchase of a portfolio of mortgage loans offered by a national lender which is finalizing its bankruptcy proceedings. The pool of loans carries principal balances of $2.6 million, and consists of a mix of performing, sub-performing and non-performing loans; Oxford is purchasing these assets at a significant discount.90% ROI? Jeepers.

"We have evaluated the real estate securing these loans, and based on current valuations our cost of the portfolio will equate to approximately 30% of the collateral value," said Robert Dunn, President of Oxford. "We think this is another excellent opportunity for a safe and significant return on our investment."

Earlier this week, Oxford announced that its portfolio reflected an annualized return on investment exceeding 90% during 2007.

If the price was 30 cents on the collateral dollar, I'd like to know what it was on the loan balances.

More Fig Leaves

by Anonymous on 1/31/2008 07:43:00 AM

PBS (thanks, ES!):

JEFF YASTINE, NIGHTLY BUSINESS REPORT CORRESPONDENT: You wouldn't call Sandra Sanchez a real estate speculator. The mother of two teaches at a private school. Two years ago, with a daughter headed off to college and the real estate boom in full swing, she purchased this house as an investment property. It seemed like a good idea at the time.I have no idea why I wouldn't call Ms. Sanchez a real estate speculator, since as far as I can tell she was speculating in real estate. I'm sure she's an amateur speculator, but that's rather the point, isn't it?

YASTINE: Sandra Sanchez, struggling now to make payments on two homes, thinks the GOP and Democratic candidates are beginning to pay attention.I'm guessing that we could, certainly, sit back and let things happen to speculators. Hence the fig leaf.

SANCHEZ: I think they're seriously thinking about the matter. And they know that a lot of the votes come from the average people, so you have to focus on the needs of the average people. You cannot sit back and let things happen to people.

YASTINE: With that in mind, Sanchez says she'll vote today and reevaluate come November. She hopes her homes haven't been foreclosed upon by then.

MBIA: $2.3 Billion Loss, Seeks Capital

by Calculated Risk on 1/31/2008 01:16:00 AM

From Bloomberg: MBIA Posts Biggest Loss; Considers New Capital Plans

MBIA Inc., the world's largest bond insurer, posted its biggest-ever quarterly loss and said it is considering new ways to raise capital ...The ratings watch continues.

The fourth-quarter net loss was $2.3 billion ... raising concern the ... company will lose its Aaa rating at Moody's ... Without the Aaa stamp, MBIA would be unable to lend a top rating to new securities, crippling its business and throwing ratings on $652 billion of debt into doubt. ... Bond insurers guarantee $2.4 trillion of debt combined and are sitting on losses of as much as $41 billion, according to JPMorgan Chase & Co. analysts. Their downgrades could force banks to write down $70 billion, Oppenheimer & Co. analyst Meredith Whitney said yesterday in a report.

Wednesday, January 30, 2008

S&P: Financial institution Losses "will reach more than $265 billion"

by Calculated Risk on 1/30/2008 05:29:00 PM

S&P reported today (no link):

Many of the largest global financial institutions have already taken significant losses on their exposures of subprime CDOs and the RMBS that were in the pipeline to be securitized as CDOs. For those institutions, we believe that these ratings actions are not likely to add significantly to the more than $90 billion of losses already reported. However, we believe that total losses for financial institutions will eventually reach more than $265 billion.

In our opinion, the downgrades of mortgage securities could lead to the realization of those losses, especially among some of the smaller players that have yet to feel the full extent of the value impairments on securities held in their available-for-sale securities portfolios. For institutions that hold a substantial portion of their assets in RMBS, we will be reviewing the exposures and the current marks to market on these holdings. In particular, some large European banks have not reported yet, and we currently expect upward revision of losses.

In the U.S., we see losses moving to regional banks, credit unions, and FHLBs. Certain Asian banks are also exposed. There could be rating actions for selected banks, especially for those that are thinly capitalized. ...

Another issue is the potential for a ripple impact on the broader financial markets. It is difficult to predict the magnitude of any such effect, but we believe it will have implications for trading revenues, general business activity, and liquidity for the banks.

S&P: Half Trillion in Mortgage Debt Ratings Cut (or may be cut)

by Calculated Risk on 1/30/2008 05:01:00 PM

From Bloomberg: S&P Lowers or May Cut Ratings on $534 Billion of Mortgage Debt (hat tip Tank, RayOnTheFarm)

Standard & Poor's lowered or may cut ratings on $534 billion of residential mortgage securities and collateralized debt obligations.According to the Fed Flow of Funds report, household have $10.4 trillion in mortgage debt. S&P's announcement today alone is for about 5% of that debt.

Fitch Cuts FGIC Rating

by Calculated Risk on 1/30/2008 04:18:00 PM

From Bloomberg: FGIC Loses AAA Rating at Fitch After Missing Deadline

Financial Guaranty, a unit of New York-based FGIC Corp., was cut two levels to AA, New York-based Fitch said today in a statement. ...FGIC is the fourth largest bond insurer.

``This announcement is based on FGIC's not yet raising new capital, or having executed other risk mitigation measures, to meet Fitch's AAA capital guidelines within a timeframe consistent with Fitch's expectations,'' the ratings company said today.

MBIA and Ambac Watch

by Calculated Risk on 1/30/2008 03:26:00 PM

Still waiting ...

Meanwhile, CNBC reports: MBIA, Ambac Understate Losses: Short Seller

William Ackman, a hedge fund manager and short-seller of MBIA, is submitting data to the Securities and Exchange Commission and insurance regulators in New York State alleging that bond insurers MBIA and Ambac Financial Group are understating their losses.

In his report, Ackman, of Pershing Square Capital, will contend that both bond insurers have said their mark-to-market losses are less than $1.5 billion. According to his analysis, the losses for each firm will be around $12 billion.

Flagstar Bancorp: Concerned About Consumers Walking Away

by Calculated Risk on 1/30/2008 02:56:00 PM

"Another effect we are seeing has been a challenge with the media and consumer groups; and with consumers willingness just to walk away from homes. We haven't seen anything like this since Texas during the oil bust and people just willing to declare bankruptcy and walk away. We are seeing a lot of that similar type social phenomenon occurring, especially in California. And that is concerning to us."Hammond also expressed concern that a larger percentage of homeowners - as compared to previous housing busts - that go delinquent, don't cure. They just "go under" in Hammond's words.

Mark Hammond, CEO, Flagstar Bancorp conference call. (hat tip Scott)

Here is what Hammond means: Say a homeowner misses a payment and becomes delinquent. Historically most homeowners try to make future payments - even if they stay 30 days late. Now, according to Hammond, once they go 30 days late, many homeowners just give up and keep missing all payments; they go 60 days late, 90 days late, and on to foreclosure.

Also, there was some concern expressed about CRE loan concentrations and delinquencies.

Fed Cuts Fed Funds Rate 50bps

by Calculated Risk on 1/30/2008 02:14:00 PM

From the Federal Reserve:

The Federal Open Market Committee decided today to lower its target for the federal funds rate 50 basis points to 3 percent.

Financial markets remain under considerable stress, and credit has tightened further for some businesses and households. Moreover, recent information indicates a deepening of the housing contraction as well as some softening in labor markets.

The Committee expects inflation to moderate in coming quarters, but it will be necessary to continue to monitor inflation developments carefully.

Today’s policy action, combined with those taken earlier, should help to promote moderate growth over time and to mitigate the risks to economic activity. However, downside risks to growth remain. The Committee will continue to assess the effects of financial and other developments on economic prospects and will act in a timely manner as needed to address those risks.

Voting for the FOMC monetary policy action were: Ben S. Bernanke, Chairman; Timothy F. Geithner, Vice Chairman; Donald L. Kohn; Randall S. Kroszner; Frederic S. Mishkin; Sandra Pianalto; Charles I. Plosser; Gary H. Stern; and Kevin M. Warsh. Voting against was Richard W. Fisher, who preferred no change in the target for the federal funds rate at this meeting.

In a related action, the Board of Governors unanimously approved a 50-basis-point decrease in the discount rate to 3-1/2 percent. In taking this action, the Board approved the requests submitted by the Boards of Directors of the Federal Reserve Banks of Boston, New York, Philadelphia, Cleveland, Atlanta, Chicago, St. Louis, Kansas City, and San Francisco.

Non-Residential Investment: The Key?

by Calculated Risk on 1/30/2008 10:15:00 AM

Residential investment, as a percent of GDP, fell to 4.16% in Q4 2007, and is now below the median of the last 50 years (about 4.56%). Click on graph for larger image

Click on graph for larger image

This graph shows Residential Investment (RI) as a percent of GDP since 1960. Based on previous downturns, RI as a percent of GDP will probably bottom in the 3% to 4% range (probably below 3.5% because of the current huge excess supply of housing units).

Simply extrapolating out the current trajectory, RI as a percent of GDP would then bottom in the 2nd half of 2008. Of course, given the magnitude of the boom, RI as a percent of GDP could fall below 3% and not bottom until sometime in 2009.

But we all know housing is getting crushed.

The good economic news in the Q4 GDP report was that non-residential investment was still positive. Investment in non-residential structures increased at a very robust 15.8% annualized real rate. And investment in equipment and software increased at a more modest 3.8% annualized real rate. This non-residential investment is probably the key (along with consumer spending) on how weak the economy will be in 2008.

This following graphs compare residential investment with both of the components of non-residential investment: structures, and equipment and software.

Important Note: On both graphs, residential investment is shifted into the future. Historically investment in non-residential structures follows residential investment by about 5 quarters, and investment in equipment and software follows residential investment by about 3 quarters. For more on these lags, see: Investment Lags.

The second graph shows the YoY change in Residential Investment (shifted 3 quarters into the future) and investment in equipment and software. The normal pattern would be for investment in equipment and software to have turned negative.

Instead investment in equipment and software is still positive.

The third graph shows the YoY change in Residential Investment (shifted 5 quarters into the future) and investment in Non-residential Structures. The normal pattern would be for investment in non-residential structures to turn negative now.

Once again, investment in non-residential structures was still strong in Q4. It is possible that the big investment slump in the early '00s has left many markets with too little supply of commercial and office buildings (and other non-residential structures). If true, then investment in non-residential structures decoupled (at least for a short period) from the typical pattern.

However, there is growing evidence that investment in non-residential structures is now slumping. We will know more when the Fed releases the January Senior Loan Officer Opinion Survey on Bank Lending Practices.

For equipment and software, I think we are still in a technology fueled productivity boom, so it is possible that investment in software and equipment will stay somewhat positive, and not follow residential investment. This is what happened in the '90s (second graph); residential investment slumped somewhat, but investment in equipment and software stayed strong.

Of course, if non-residential investment falters, the U.S. will almost certainly be in a recession.

Slow GDP Growth in Q4

by Calculated Risk on 1/30/2008 09:28:00 AM

From the WSJ: GDP Growth Slowed in 4th Quarter, As Housing Continues Its Drag

Gross domestic product rose at a seasonally adjusted 0.6% annual rate October through December, the Commerce Department said Wednesday in the first estimate of fourth-quarter GDP.We will know more on December consumer spending tomorrow when the monthly Personal Income and Outlays report is released, but ... we know that PCE (personal consumption expenditures) was strong in October and November (see Econbrowser):

...

Aside from the housing slump, slowing consumer spending, inventory liquidation and lower overseas sales restrained the economy.

...

Inflation gauges within Wednesday's GDP data indicated acceleration in prices.

...

The biggest GDP component, consumer spending, decelerated in the fourth quarter, rising 2.0% after increasing 2.8% in the third quarter.

The October and November 2007 data imply an estimate of the growth rate of real consumption spending of 3.2% during the fourth quarter of 2007.Since PCE came in at only 2.0%, clearly there was a sharp slowdown in December, and the growth from the last month of Q3 to last month of Q4 was probably negative - suggesting a recession might have started in December.

Edit: The ADP employment data is also available this morning, showing nonfarm private employment grew by 130,000 in January, and without a downward revision, those numbers are definitely not recessionary.

UBS: $14 Billion in Mortgage Write Downs

by Calculated Risk on 1/30/2008 01:48:00 AM

The WSJ reports:

UBS said it expects a fourth-quarter net loss of $11.4 billion, including around $12 billion of losses linked to subprime debt and $2 billion in other mortgage-related losses.A little late night visit to the confessional.

Tuesday, January 29, 2008

CNBC: Bond Insurer Downgrades Could Come Tomorrow

by Calculated Risk on 1/29/2008 07:42:00 PM

From CNBC: Bond Insurers Face Downgrade Despite Call for Delay

Wall Street bond rating agencies are poised to downgrade two big bond insurers, Ambac Financial Group and MBIA ... the downgrades could come as early as Wednesday.A downgrade would lead to significant write-downs on Wall Street, and more losses for investors, but it's unclear how large the write-downs will be.

WSJ: More Criminal Inquiries into Mortgage Related Companies

by Calculated Risk on 1/29/2008 04:04:00 PM

From the WSJ: U.S. Probes 14 Companies In Subprime Investigation

Federal investigators have opened criminal inquiries into 14 companies as part of a wide-ranging investigation of the subprime mortgage crisis, focusing on accounting fraud, securitization of loans and insider trading ... The FBI wouldn't identify the companies under investigation but said that generally the bureau is looking into allegations of fraud in various stages of mortgage securitization, from those who bundled the loans, to the banks that ended up holding them.This reminds me of Tanta's excellent piece last March: Unwinding the Fraud for Bubbles

There is a tradition in the mortgage business of distinguishing between two major types of mortgage fraud, called “Fraud for Housing” and “Fraud for Profit.” The former is the borrower-initiated fraud—inflating income or assets, lying about employment, etc.—that is motivated by the borrower’s desire to get housing (not the same thing as “real estate”), by means of getting a loan he or she doesn’t actually qualify for.This new investigation is once again going after those involved in "Fraud for Profit", possibly with a new emphasis on those involved in the securtization process. See also this recent NY Times report by Jenny Anderson and Vikas Bajaj: Reviewer of Subprime Loans Agrees to Aid Inquiry

...

Fraud for profit is simply someone trying to extract cash—not housing—out of the transaction somewhere.

Tousa Goes BK

by Calculated Risk on 1/29/2008 11:26:00 AM

From Bloomberg: Tousa, Florida Homebuilder, Files for Bankruptcy

Tousa Inc. ... sought bankruptcy protection from creditors ... Tousa, now the largest builder in bankruptcy and at least the 14th to file since June ...TOUSA was the #13 largest builder in 2006 according to BuilderOnline. I believe the largest home builder previously to go bankrupt was #50 Levitt & Sons. Here is the BuilderOnline top 100.

Options Theory and Mortgage Pricing

by Anonymous on 1/29/2008 11:02:00 AM

One of the hot topics of conversation lately is the idea of a mortgage “put option.” There seem to be more than a few people—including those who don’t exactly use the language of options contracts, like that weird couple featured recently on 60 Minutes—who are slightly confused about what the “optionality” of a mortgage contract is. There are also lots of folks who are wondering what will happen to mortgage pricing in general should a substantial number of folks decide to “exercise the put” on their mortgages. It seems wise to me to try to tease out what’s going on here.

First, mortgage contracts in the U.S. are not, actually, options contracts. You may peruse your note and mortgage at length now, if you didn’t do so when you signed them, and you will not find any “put” or “call” in there. Your note is a promise to pay money you have borrowed, and your mortgage or deed of trust is a pledge of real estate you own (or are buying with the borrowed money) as security for that note. That means, in short, that if you fail to keep your promise to pay the loan in cash, the lender can force you to sell your property at auction (to produce cash with which to pay the loan in full). Because the mortgage instrument gives your lender a “lien,” any sales proceeds are first applied to the mortgage debt before you get any of it.

People get very confused about this because it is often the lender who ends up buying the property at the forced auction. When that happens, it is basically because the lender simply wants to put a “floor” bid in the auction: the lender bids an amount based on what it is willing to lose (if any). Typically, the lender bids its “make whole amount” or the loan amount plus accrued interest and expenses. If someone else bids more than that, the lender is happy to let the property go to the higher bidder.

The lender might bid less than its make-whole amount; it might bid its “probable loss” amount. If the lender is owed $300,000 and doesn’t think it could ever end up recovering more than $200,000, it might bid $200,000 at the FC auction. The lender doesn’t actually want to win the auction; lenders are not really in the business of real estate investment or property management. However, the lender would rather buy the home at the auction and pay itself back eventually by re-selling the property later (as a listed property in a private sale instead of a courthouse auction) than let the property go for $50,000 (meaning the lender would recover only $50,000 on a $300,000 loan instead of $200,000). Nothing ever stops any third party from bidding $1 more than the lender’s bid and winning the auction (except, of course, any third party’s own inclinations).

We need to remember, then, right away, when anyone talks about “giving the house back to the bank” or “mailing in the keys,” we are already in the land of metaphorical language. The only situation in which “giving the house back to the bank” would literally be possible is if you bought the house from the bank (say, it was REO) and the contract explicitly gave you an option to sell it back to the bank, whenever you wanted to, at a price equal to your loan balance. Nobody writes REO sales contracts that way. In most cases, of course, you bought the house from someone other than a bank. You have no option to “put the house back” to the seller. You win only if it's "heads."

A “put option,” in the financial world, is a contract that gives the buyer of the put the right, but not the obligation, to sell something (a commodity, a stock, a bond, etc.) in the future at a predetermined price. On the other side of the deal, the “writer” of the put is obligated to buy the thing in question if the put buyer exercises the option. Some of you may already be a bit confused about “buyer” and “seller” here, but that’s an important point. You don’t get “free puts.” You buy puts. There is a fee or a “premium” that you pay for the option contract. If you do not exercise the option, the put-writer pockets that fee. If you do exercise your option, the put-writer pockets that fee (to offset his loss on the deal) and your gains on the ultimate sale of the thing are net of the option premium.

The point of a put is that you buy them when you want to be protected from falling prices: if you think there is a good chance that the value of something will fall in the future, buying a put that allows you the option of selling it next month at this month’s price might well be worth paying that option premium. But you do always pay an option premium and you do not get it back.

The opposite of the put option is the call option: it is the option to buy something in the future at a predetermined price. You buy calls when you think the value of the thing is likely to rise. You also always pay some premium or fee for a call.

Residential real estate sales and mortgage loans do not, actually, literally, have puts and calls in them. If you buy a home today, you assume the risk that its price may fall in the future. Your contract does not include an option for you to sell the house at the price you paid for it. Nor does the seller of the house have a “call”; the seller cannot force you to sell the house back to him at the original price if its value rises.

Your mortgage loan contract does not give you the right to simply substitute the current value of the house for the current balance of the loan: you do, in fact, risk being “upside down.” (The only time this isn’t true in the U.S. is with a reverse mortgage; those are written explicitly to have this kind of a feature, where the balance due on the loan can never exceed the current market value of the property. But of course reverse mortgages aren’t purchase-money loans.) Nor does the mortgage contract give your lender the right to buy your house from you for the “price” of the loan amount when that is less than its value. Mortgage lenders never do better than paid back. If the real estate securing your loan increases in value, that appreciation belongs to you (as long as you make your loan payments).

So why is it that people keep talking about “puts” and “calls” in terms of mortgage loans? That’s because mortgage contracts have features that can affect their value to the writer of the contract (the lender or investor) in a way that is analytically comparable, in some ways, to classic options. Options theory is applied to mortgages in order to price them as investments. (Strictly speaking, this is a matter of analyzing them so that a price can be determined.) The interest rate, then, that you get on a mortgage loan will depend, in part, on how the lender/investor “priced” the implied options in the contract.

The “implied put” in a mortgage contract is the borrower’s ability to default (walk away, send jingle mail, whatever you want to call it). We do not, generally, consider “distress” (that’s actually the formal term in the literature, for you Googlers) as an “implied put.” Some borrowers will fall on hard times and be unable to fulfill their mortgage contracts. This is a matter of “credit risk” and it is, analytically, a different matter of mortgage contract valuation. The “implied put” analysis is trying to capture the possible cost to the lender/investor of what we call the “ruthless” borrower. “Ruthless” isn’t really intended to be a casual insult; it is in fact the term we use to describe borrowers who can pay their debts but choose not to, because there is a greater financial return to that borrower in defaulting as opposed to not defaulting. It is “ruthless” precisely because there is not a contractual option to do this: the only way you can exercise the “implied put” is to default on your contract.

Many many people are very confused about this. When we talk about the “social acceptability” of jingle mail, what we are talking about is at some level the extent to which there is or ought to be some rhetorical or social “fig leaf” over ruthlessness. It seems to be true, after all, that most people are more likely to behave ruthlessly if they can call it something other than ruthlessness. (There are always people who have no trouble with ruthlessness; they often get the CEO job. Most of us have at least moderately strong inhibitions about ruthless behavior.) There is, therefore, a process in which the ruthless put is re-described in various alternative terms, or has alternative narrative contexts built up around it, such that it no longer “feels” ruthless. The borrower was victimized (by the lender, the original property seller, the media, the Man). The put premium was actually paid (“they charge me so much they can afford this”). The ruthless borrower is actually the distressed borrower (redefining what one can “afford” or what is necessary expense so that a payment you can make becomes a payment you “can’t” make).

Before anyone starts in on me, let me note that these fig leaf mechanisms are effective precisely because victimization, predatory interest rates, and truly distressed household budgets do really exist. They wouldn’t be very convincing otherwise. (Very few ruthless borrowers will claim it’s because of, say, alien abduction or something equally implausible.) I am not, therefore, asserting that all claims of predation or distress are “false.” I am simply pointing out that it is, after all, a hallmark of the not-usually-ruthless person who is nonetheless acting ruthlessly to rationalize his conduct.

I don’t offer that as some startling insight into human psychology. I offer it as an attempt to get some analytic clarity. When CR talks about lenders fearing that jingle mail will become socially acceptable, he’s not exactly saying that lenders fear that society will no longer stigmatize financial failure (“distress”). They are afraid that rationalization mechanisms will become so effective that true ruthlessness (which is historically pretty rare in home mortgage lending) will become a significant additional problem (in addition to true distress). And they fear this because, delusions to the contrary, those loans did not have enough of a “put premium” priced into them to cover widespread “ruthless default.”

In fact, the very language of options theory can function, for a certain class of ruthless borrowers, as the fig leaf. To say “Hey, I’m just exercising my put” is a retroactive reinterpretation of your mortgage contract to “formalize” the “implied put” so that you do not have to describe what you’re doing as “defaulting.” This strategy is apparently popular with folks who have some modest exposure to financial markets jargon and an unwillingness to lump themselves in with the “riffraff”—victims of predators and financially failing households and other “weaklings.” (Sadly, a lot of people who have a very high degree of exposure to financial markets jargon don’t need no steenkin’ rationalization. Like most sociopaths, they don’t understand why “ruthless” would be considered insulting or what this term “social acceptability” might mean. So if you’re hearing the “put” excuse, you are probably in the presence of a relative amateur.)

The other side of the problem in valuation of mortgage loans and mortgage securities is the “implied call.” The “call-like feature” in a mortgage contract is the right to prepay. In the U.S., all mortgage contracts have the right to prepay. (Some, but not all, have a “prepayment penalty” in the early years of the loan, but “penalty” here means a prepayment fee, not an actual legal prohibition on prepayment.) The reason the right to prepay functions like an implied call is that it gives the borrower the right to “buy” the loan from the lender at “par,” even if the value of the loan is much higher than “par.” If you refinance your mortgage, you are required only to pay the unpaid principal balance (plus accrued interest to the payoff date) to the old lender in order to get the old lien released. Unless the loan specifically has a prepayment penalty, you are not required to further compensate the old lender for the loss of a profitable loan. So a loan with a prepayment penalty has an implied call and a real call exercise price. A loan without a prepayment penalty, or past the term of its prepayment penalty, has a “free call.” (In the original lender’s point of view. There is always some price to be paid to get a new refinance loan; the borrower’s calculation of the value of refinancing always has to take that into account. Among other things, this fact results in mortgage “call exercise” being much less “efficient” than it is on actual call contracts, which makes the call much more difficult to value, analytically, for mortgages.)

While ruthless default might, historically, be rare, refinancing has been ubiquitous for decades now. It wasn’t always so easily available; your grandparents might never have refinanced a loan not because their existing interest rates were never above market, but just because there weren’t lenders around offering inexpensive refinances. In fact, refinances have been so ubiquitous for so long now that many people have come to think of the availability of refinancing money as somehow guaranteed. This isn’t just a naïveté about interest rate cycles, although it is that too. It is a belief that credit standards and operating costs of lenders never change, so that if someone thought you were “creditworthy” once, they’ll automatically think of you as creditworthy again, and that lenders can always afford to refinance you without charging you upfront fees.

People who price mortgage-backed securities have always known that the prepayment behavior of mortgage loans is impacted not just by prevailing interest rates, but also by the borrower’s creditworthiness, the lenders’ risk appetites, and the cost (time and money) of the refinance transaction. We were talking the other day about the prepayment characteristics of jumbo loans in comparison to conforming loans; the fact is that people who have the largest loans are the most likely to refinance at any given reduction in interest rate, since a reduction in interest rate produces more dollars-per-month in savings on a larger loan than it does on a smaller loan. Considering these types of things is very important to people who price MBS, because in fact prepayment behavior is both hard to “price” and absolutely critical to “pricing” mortgages as an investment.

MBS, unlike other kinds of bonds, are “negatively convex.” I have been threatening to talk about convexity for a while and I keep chickening out. It’s actually useful to understand it if you want to understand why mortgage rates (and the value of servicing portfolios) behave the way they do. The trouble is that convexity involves a whole bunch of seriously geeky math and computer models and normal people probably don’t want to go there. (I don’t even want to go there.) So as a compromise, this is a very quick and simple explanation of convexity.

The convexity of mortgages is a result of the “implied options” in them. Most people understand intuitively that the higher the interest rate on a loan, the more an investor would pay for that loan: if you had the choice today of buying a bond that paid you 6.00% and one that paid you 6.50%, you would probably not offer the same price for each of them. With a classic “vanilla” bond, the price you would offer would be a matter of looking at the term to maturity, the frequency of payments, the interest rate, and some appropriate discount rate.

The trouble with mortgages is that while they have a maximum legal term to maturity, they have an unpredictable actual loan life, because they have the prepayment “calls” implied in the contracts. The return on a mortgage is uncertain, because you might get repaid early, forcing you to reinvest your funds at a lower rate. On the other hand, the loans might just stay there until legal maturity, at an interest rate that is now below the market rate on a new investment. The problem, obviously, is that borrowers refinance most often when prevailing market rates have dropped (right when the investor might want the loans to be long-lived) and don’t refinance when prevailing rates have risen (right when the investor would like to see you go away). “Vanilla” bonds don’t behave this way. Vanilla bonds, like Treasury bonds and notes, are “positively convex.” Mortgages are “negatively convex.”

Here’s a comparative convexity graph prepared by Mark Adelman of Nomura (do pursue the link if you want more detailed information about MBS valuation). This graph plots three example instruments all with a face value of $1,000 and a price of par ($1,000) at 6.00%. The vertical axis reflects the change in price of the bond. The horizontal axis reflects the change in prevailing market yields. As you move to the left of 6.00%, you see that the price of the bond increases (it has an above-market yield); as you move to the right it decreases.

However, the three instruments do not increase or decrease in price in the same way. The 30-year bond has a steeper curve than the 10-year note, which is a function of the difference in maturities of the two instruments. The MBS isn’t just not as steep; it is a different shape. The 30-year bond and the 10-year note price functions create an upward-curving slope when you plot them against price/yield changes like this, and the MBS price functions create a downward-curving slope. The term “negative convexity” means, exactly, that downward curving slope.

What’s going on here is that when market yields fall (moving to the left in the graph), average loan life in an MBS pool will shorten markedly, as borrowers are “in the money” to refinance. At a relatively modest fall in market yields, the price of the MBS does increase (but the increase is much less than the increase in the other bonds). At a larger drop in market yields, the MBS price gets as high as it will ever get and then stops increasing at all. What happens here is that the underlying mortgage loans have become so “rate sensitive” that any additional decrease in market yield (increase in the spread between the bond’s coupon of 6.00% and current market coupons) is entirely offset by shortened loan life: loans will pay off so fast at this point that this “officially” 30-year bond really returns principal to the investor the way a 1-year or even 6-month Treasury bill would. No investor is going to pay more for the MBS at this point than it would for the very shortest-term alternative.

On the other side of the graph, you see that the MBS price declines more slowly than the vanilla bonds, although its curvature at this point is very like the 10-year. At this side of the chart, average loan life is increasing. (Mortgage bonds never go to zero prepayments or actual average loan life = 30 years.)

What all this implies is that, analytically, mortgages do have some sort of “option price” built in. (There is actually a name for this, the OAS or Option Adjusted Spread, a method of comparing cash flows of a mortgage bond across multiple interest rate and prepayment scenarios. It’s heavy math and modeling.) In the case of voluntary prepayment (refinancing or selling your home, basically), your “call” option has, in fact, been priced—it’s in the interest rate/fees you pay to get a refinanceable mortgage loan. Investors accept the uncertainty of mortgage duration by (attempting to) price it in.

All that, however, is about trying to price the full return of principal (which, in the case of a mortgage loan, is also the point at which interest payments cease). It isn’t trying to model the return of less than outstanding principal, which is what the “put” or ruthless default is. A refinancing borrower pays you back early at par. A defaulting borrower pays you back early at less than par. Standard MBS valuation models that were developed for GSE or Ginnie Mae securities (that are guaranteed against credit loss) do not “worry” about ruthless puts in terms of principal loss, since that loss is covered by the guarantor. What is causing some trouble these days with the “ruthless put” in the prepayment models is simply that this is an unexpected source of prepayment that isn’t correlating with “typical” interest rate scenarios. (We are seeing increased defaults in a very low-rate environment, because of the house price problem, which isn’t built into the prepayment models for guaranteed securities. Historically, prepayment models “expect” non-negligible numbers of ruthless puts only in higher-rate environments.)

It may help you to understand that we have been talking about how an investor might price an MBS coupon, which isn’t the same thing as the interest rate on a loan. In a Fannie Mae or Freddie Mac MBS, the “coupon” or interest rate paid to the investor might be, say, 6.00%. That means that the weighted average interest rate on the underlying loans in the pool is substantially more than 6.00%. There is the bit that has to go to the servicer, and there’s the bit that has to go to the GSE to offset the credit risk. The mortgages must pay a high enough rate of interest to provide 6.00% to the investor after the servicing and guarantee fees come off the top. In essence, then, MBS traders set the “current coupon” or the coupon that trades at par, the GSEs set the guarantee fee and/or loan-level settlement fees that cover the credit risk, the servicer sets the required servicing fee, and all that adds up to the “market rate” for conforming mortgage loans (plus mortgage insurance, if applicable, which is conceptually an offset to the guarantee fee).

One way of describing the situation we’re currently in is that borrowers are continuing the short loan life of the boom (which was made possible by easy refi money and hot RE markets) by substituting jingle mail for refinancing. That increases credit losses to whoever takes the credit loss (the GSEs and the mortgage insurers), decreases servicer cash flow (a refi substitutes a new fee-paying loan for the old loan; a default substitutes a no-fee-paying problem for the old loan), and makes everyone’s prepayment models go whacky-looking. This is one reason why it obviously wasn’t a good time for MBS traders to be told they’d be suddenly getting jumbos in their conforming pools; at some level the response to that could be summed up as “we don’t need one more thing that defies analysis.”

Ultimately, there is no way anyone can mobilize “social acceptability” as a defense against the ruthless put (even if you wanted to). The industry has, in fact, created the conditions in which it’s rational, and as long as it’s rational it will go on. Just as it was rational to buy at 100% LTV. The only possible way to get back to an environment in which ruthless default is rare is to abandon the “innovations” that give rise to them: no-down financing, wish-fulfillment appraisals, underpriced investment property loans, etc. The administration is currently pushing for increasing the FHA loan amounts and the FHA maximum LTV up to 100%. This is not likely to remove the incentive to take another reckless loan on a still-too-high-priced house. If we aren’t going to ration credit with tighter guidelines and loan limits, then it will have to be rationed with pricing: eventually the models will “solve” the problem by increasing the costs of mortgage credit. You cannot simply keep writing “free puts.”

Homeownership Rate: Cliff Diving

by Calculated Risk on 1/29/2008 10:42:00 AM

The Census Bureau reports that the homeownership rate declined to 67.8% in Q4, from 68.2% in Q3 2007. Click on graph for larger image.

Click on graph for larger image.

The homeownership rate has plunged back to the levels of the summer of 2001. Note: graph starts at 60% to better show the change.

This is a huge drag on the U.S. housing market. I'll have more on this later today.

The homeownership vacancy rate increased slight to a record 2.8% (from 2.7% in Q3).

The second graph shows the homeowner vacancy rate since 1956. A normal rate for recent years appears to be about 1.7%. There is some noise in the series, quarter to quarter, but it does appear the vacancy rate has stabilized.

This leaves the homeowner vacancy rate about 1% above normal, or about 825 thousand excess homes.

The rental vacancy rate declined to 9.6% in Q4, from 9.8% in Q3. The rental vacancy rate has been trending down slightly for almost 3 years (with some noise). This was due to a decline in the total number of rental units in 2004, and more recently due to more households choosing renting over owning.

It's hard to define a "normal" rental vacancy rate based on the historical series, but we can probably expect the rate to trend back towards 8%. This would suggest there are about 560 thousand excess rental units in the U.S. that need to be absorbed.

There are also approximately 250K excess new homes above the normal inventory level (for home builders).

This suggests there are about 1.65 million excess housing units in the U.S. that need to be worked off over the next few years. These excess units will keep pressure on housing starts and prices for some time.

S&P Case-Shiller Composite: House Prices Fall 7.7%

by Calculated Risk on 1/29/2008 09:17:00 AM

Correction (hat tip Whiskey): the composite 10 is down 8.4% (ten cities), the composite 20 is down only 7.7%.

Here is the S&P/Case-Shiller data.

Here is the year over year change in both October and November for 20 large U.S. metropolitan areas (not the entire U.S.). Prices are falling in every city in the index (even the three cities with rising year-over-year prices are seeing falling prices on a monthly basis).

| City | YoY Price Change, October | YoY Price Change November |

| Charlotte - NC | 4.3% | 2.9% |

| Seattle - WA | 3.3% | 1.8% |

| Portland - OR | 1.9% | 1.3% |

| Dallas - TX | -0.1% | -1.2% |

| Atlanta - GA | -0.7% | -2.0% |

| Denver | -1.8% | -3.1% |

| Chicago | -3.2% | -3.9% |

| Boston | -3.6% | -3.0% |

| New York | -4.1% | -4.8% |

| Cleveland - OH | -4.5% | -5.8% |

| Minneapolis- MN | -5.5% | -6.6% |

| San Francisco | -6.2% | -8.6% |

| Washington | -7.0% | -7.8% |

| Los Angeles | -8.8% | -11.9% |

| Phoenix - AZ | -10.6% | -12.9% |

| Las Vegas | -10.7% | -13.2% |

| San Diego | -11.1% | -13.4% |

| Detroit - MI | -11.2% | -13.0% |

| Tampa - FL | -11.8% | -12.6% |

| Miami | -12.4% | -15.1% |

| Composite-20 | -6.1% | -7.7% |

Countrywide: One Third of Subprime Loans Delinquent

by Calculated Risk on 1/29/2008 08:34:00 AM

From Reuters: Countrywide--1 in 3 subprime mortgages delinquent

Countrywide said borrowers were delinquent on 33.64 percent of subprime loans it serviced as of Dec. 31, up from 29.08 percent in September.From the WSJ: Countrywide Swings to Loss

Countrywide ... lost $422 million...More to come, Countrywide is still in the Confessional.

Countrywide set aside $924 million for credit losses during the fourth quarter, compared with reserves of $73 million during the final quarter in 2006.

Monday, January 28, 2008

Countrywide Concerned about "Borrowers economic interest to repay"

by Calculated Risk on 1/28/2008 08:50:00 PM

Countrywide sent out a letter on Jan 18th with their new Soft Market policies (hat tip ck).

... 2008 is forecasted to be a challenging year for the mortgage industry, characterized by a declining Housing Price Index in a wide variety of metropolitan markets. In the context of the prominent threat to our industry of collateral values falling below outstanding loan balances, mortgage professionals must strive to ensure that borrowers do not take on loans that they do not have the ability or economic interest to repay.Note that last phrase: "borrowers do not take on loans that they do not have the economic interest to repay". Countrywide is clearly concerned about the new trend of buyers "walking away" from their mortgages.

The policy basically reduced the maximum LTV for various loans based on the county risk level. Countrywide's ranking of risk, by county, is available online Countrywide Soft Market County Index.

AmEx CEO: "Clear signs of a weakening economy and business environment"

by Calculated Risk on 1/28/2008 04:38:00 PM

From American Express:

"... we saw clear signs of a weakening economy and business environment in December,”And from CNBC:

Kenneth I. Chenault, chairman and CEO.

The company also set aside $440 million in the quarter to cover loans that it expects won't be repaid.

Consumers are cutting back on their spending because of many factors that include higher energy and food prices, in addition to weakness in the credit and housing markets.

NY Insurance Department Hires Wall Street Firm for Advice on Monoline Insurers

by Calculated Risk on 1/28/2008 03:22:00 PM

From the WSJ: New York Hires Perella To Advise on Bond Insurers

The New York State Insurance Department has hired the Wall Street firm Perella Weinberg Partners for advice on the financial health of bond insurers.A line of credit or capital infusion from the insured to the insurer is not an answer. I'm not sure how you can protect the policy holders if the insurer can't pay.

...

The Perella Weinberg assignment focuses on protecting policy holders who are customers of so-called monoline insurers, which include Ambac Financial Group Inc. and MBIA Inc., according to people familiar with the assignment.

New Home Sales: Cliff Diving

by Calculated Risk on 1/28/2008 11:22:00 AM

Click on graph for larger image.

Click on graph for larger image.

This graph shows New Home Sales vs. recessions for the last 45 years. New Home sales were falling prior to every recession, with the exception of the business investment led recession of 2001.

Note that the escalation of the Vietnam War in the '60s kept the economy out of recession, even though New Home sales were falling.

This is what we call Cliff Diving!

And this shows why so many economists are concerned about a possible consumer led recession - possibly starting in December (as shown on graph).

December New Home Sales

by Calculated Risk on 1/28/2008 10:00:00 AM

According to the Census Bureau report, New Home Sales in December were at a seasonally adjusted annual rate of 604 thousand. Sales for November were revised down to 634 thousand, from 647 thousand, and numbers for October were revised up slightly.

| Click on Graph for larger image. Sales of new one-family houses in December 2007 were at a seasonally adjusted annual rate of 604,000 ... This is 4.7 percent below the revised November rate of 634,000 and is 40.7 percent below the December 2006 estimate of 1,019,000. |

| The Not Seasonally Adjusted monthly rate was 42,000 New Homes sold. There were 71,000 New Homes sold in December 2006. December '07 sales were the lowest December since 1994 (40,000). |

| The median and average sales prices are generally declining. Caution should be used when analyzing monthly price changes since prices are heavily revised and do not include builder incentives. The median sales price of new houses sold in December 2007 was $219,200; the average sales price was $267,300. |

| The seasonally adjusted estimate of new houses for sale at the end of December was 495,000. The 495,000 units of inventory is slightly below the levels of the last year. Inventory numbers from the Census Bureau do not include cancellations - and cancellations are once again at record levels. Actual New Home inventories are probably much higher than reported - my estimate is about 100K higher. |

| This represents a supply of 9.6 months at the current sales rate. |

This is another VERY weak report for New Home sales. Most revisions continue to be down. This is the fifth report after the start of the credit turmoil, and, as expected, the sales numbers are very poor.

I expect these numbers to be revised down too. More later today on New Home Sales.

Blackstone ADS Deal "Unlikely"

by Calculated Risk on 1/28/2008 09:29:00 AM

From the WSJ: ADS Says Blackstone Deal Unlikely

Alliance Data Systems Corp. ... Blackstone ... likely won't go through with its $6.4 billion acquisition ..."Extraordinary measures" are usually doable during better times. This seems like another way to leave your lover (from Paul Simon):

... Blackstone told the data processor and marketing firm in a letter late Friday it doesn't expect the deal to get the necessary approvals from OCC and that the regulator is demanding "extraordinary measures" which "represent operational and financial burdens ... that cannot be reasonably assumed."

You just slip out the back, Jack

Make a new plan, Stan

You don't need to be coy, Roy

Just get yourself free

Sunday, January 27, 2008

60 Minutes: House of Cards

by Calculated Risk on 1/27/2008 08:36:00 PM

House of Cards (video): "Steve Kroft reports on how the U.S. sub-prime mortgage meltdown, in which risky loans drove a housing boom that went bust, is now roiling capital markets worldwide."

Here is the foreclosure site mentioned in the story. I live in a neighborhood that is "immune" to the housing bust. Oh yeah, that site shows a number of REOs and preforeclosure homes in my neighborhood.

New Trend: "Intentional Foreclosure"

by Calculated Risk on 1/27/2008 12:23:00 PM

From CBS: New Trend In Sacramento: 'Intentional Foreclosure' (hat tip Shawn)

Linda Caoli helps lots of families on the verge of losing their homes, including a single mom working two jobs to pay her mortgage.This is similar to Peter Viles' story in the LA Times: A tipping point? "Foreclose me ... I'll save money".

"She says Linda the house across the street, same model, with more upgrades sold in foreclosure for $315,000!" explains Linda.

Her client isn't the only one thinking about ditching her house to buy the better deal across the street. A number of realtors CBS13 talked to say it's already happening.

Wachovia is seeing this too (from their Jan 22nd conference call):

“... people that have otherwise had the capacity to pay, but have basically just decided not to because they feel like they've lost equity ...”And from BofA CEO Kenneth Lewis in December:

"There's been a change in social attitudes toward default. We're seeing people who are current on their credit cards but are defaulting on their mortgages. I'm astonished that people would walk away from their homes."This change in social attitudes could lead to a flood of foreclosures. The following is from my post last December: Homeowners With Negative Equity

The following graph shows the number of homeowners with no or negative equity, using the most recent First American data, with several different price declines.

At the end of 2006, there were approximately 3.5 million U.S. homeowners with no or negative equity. (approximately 7% of the 51 million household with mortgages).

At the end of 2006, there were approximately 3.5 million U.S. homeowners with no or negative equity. (approximately 7% of the 51 million household with mortgages).By the end of 2007, the number will have risen to about 5.6 million.

If prices decline an additional 10% in 2008, the number of homeowners with no equity will rise to 10.7 million.

The last two categories are based on a 20%, and 30%, peak to trough declines. The 20% decline was suggested by MarketWatch chief economist Irwin Kellner (See How low must housing prices go?) and 30% was suggested by Paul Krugman (see What it takes).

Intentional foreclosure. Jingle Mail. Negative Equity. All terms that could be common in 2008.

Saturday, January 26, 2008

Mortgage Due Diligence Firm Granted Immunity, Cooperating with Prosecutors

by Calculated Risk on 1/26/2008 10:49:00 PM

Jenny Anderson and Vikas Bajaj at the NY Times report: Reviewer of Subprime Loans Agrees to Aid Inquiry (hat tip James)

Clayton Holdings, a company ... that vetted home loans for many investment banks, has agreed to provide important documents and the testimony of its officials to the New York attorney general, Andrew M. Cuomo, in exchange for immunity from civil and criminal prosecution in the state.It seems the key question here is: Did the investment banks adequately disclose the information from Clayton to the investors in the mortgage securities?

... Clayton has told the prosecutors that starting in 2005, it saw a significant deterioration of lending standards and a parallel jump in lending exceptions. In an another sign that the industry was becoming less careful, some investment banks directed Clayton to halve the sample of loans it evaluated in each portfolio, a person familiar with the investigation said.

...

It is unclear how many lending exceptions are contained in the $1 trillion subprime mortgage market, but industry participants cite figures ranging from about 50 percent to 80 percent for some loan portfolios they examined.

Bank and Thrift Failures

by Calculated Risk on 1/26/2008 06:05:00 PM

The FDIC announced the first bank failure of 2008 last night. To put that into context, here is a graph of bank and thrift failures since the FDIC was created in 1934.

| Click on graph for larger image. The huge spike in the '80s was due to the S&L crisis. It's interesting to note that even with the failure of almost 3,000 banks and thrifts during the S&L crisis, the overall economy was healthy. |  |

The second graph includes the 1920s and shows that failures during the S&L crisis were far less than during the '20s (before the FDIC was enacted).

The second graph includes the 1920s and shows that failures during the S&L crisis were far less than during the '20s (before the FDIC was enacted).Note how small the S&L crisis appears on this graph!

During the Roaring '20s, 500 bank failures per year was common - even with a booming economy - with depositors typically losing 30% to 40% of their bank deposits in the failed institutions. The number of bank failures soared to 4000 (estimated) in 1933.

It's important to note that the housing bust hasn't hurt most small banks and institutions, because the banks didn't hold many of the residential mortgages they originated. Instead the small to mid-sized institutions focused on commercial real estate (CRE), construction and development (C&D) and other loans.

From the December 2006 FDIC report: Economic Conditions and Emerging Risks in Banking.

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. ... small and mid-size institutions have been ... assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loan concentrations, especially at institutions with total assets between $1 billion and $10 billion. Four of six Regional Risk Committees expressed some level of concern about CRE lending, in part due to continuing increases in concentrations.Now credit standards are being tightened, and many of these small and mid-sized institutions are seeing rising defaults on their CRE and C&D loans. So 2008 is when we would expect to see more of these small and mid-sized institutions start to fail, but the number of failures will probably be small as compared to the '80s.

Update: Here is an addition from the

Atlanta's residential bust is rapidly becoming a financial disaster on a par with the Savings and Loan Crisis of the 1980s.The article (subscription) reports that at the peak of the S&L crisis, the non-performing loans reached 4.4% for Altanta based banks (compared to 2.2% at the end of Q3 2007). However the article quotes several bankers and industry analysts that believe the percent of non-performing loans increased significantly in Q4, and will rise sharply in 2008.

Commenting

by Anonymous on 1/26/2008 04:08:00 PM

CR and I have discussed going to some kind of registration-based commenting software. There are many good reasons to do that.

The biggest problem I personally have with that is this being a business kind of blog, a lot of our readers are working in offices and cannot access commenting windows other than Haloscan because of network filters and blocks. I am not here to debate the wisdom of employers in the financial, housing, and regulatory sectors keeping their employees from using our blog as a resource. Of course that's stupid. You try telling them that.

But it gets to a point where, if the comment threads get stupid and pointless and Yahooified enough, our employed readers will not want to read them, so there goes that problem. With a registration/moderation system, we could at least assure our loyal employed readers of having something worth reading at night and on the weekends when they have access from home.

I cannot make anyone stop responding to pointless or nuisance comments. You have to want to restrain yourself, because you understand that the only way to get rid of them is to fail to give them the attention they want. A "troll" is not just someone whose comments you disagree with, or even just a nasty or badly-worded comment. A troll is someone who does not, under any possible set of circumstances, care what you think about him or his comments. He merely wants attention. Negative attention will do. The more you disagree with him, the more he is able to tell himself that he is persecuted and victimized or the only voice of reason or one of the elite few who has the God's-eye view of the world or whatever his current delusion is. If he isn't merely a narcissist who thrives on feeling attacked, he's just some putz who enjoys irritating other people. Therefore, you "feed" the troll by paying any attention to him at all. It does not matter what you say in response. Any response to a troll just encourages the troll.

Besides classic trolls, we have a few resident long-winded bores who believe that the rest of us have never been exposed to some trite, shallow, bombastic rant they just heard on the radio or read in Reader's Digest or saw in a vision, and feel compelled to share with the rest of us. These people lack any possible sense of context or audience; they are incapable of noticing that the bulk of our commenting community has been exposed to the world for a while now and is not interested in any comment that starts "there is one simple answer to this the rest of you aren't getting." It does you no good to respond to this type either; they'll just re-write the same comment again, at the same length, saying the same thing, until you "get it." They are bores with no self-awareness. The cool thing about the internet is that you can just scroll down to the next comment without being "rude." So take advantage of the medium.

Absolutely none of this is to say or imply that you are not invited to debate with each other or to correct misstatements of fact. You are also still allowed to make jokes and ramble occasionally and even from time to time introduce a new topic that is relevant. Most of you are grownups who understand intuitively where the line is, and if you cross it now and again you catch yourself and go on mostly behaving yourself. A few of you are those problem children who are not capable of taking only one cookie or talking quietly in the library or waiting until it's your turn and you ruin all group experiences for everyone else. You goad the authorities into instituting draconian rules for everybody in order to prevent you from getting out of control. You are probably going to be like this for the rest of your life, since such behavior patterns that persist past puberty usually don't go away. All I can say to you is that you really will get nowhere asking me personally to validate your feelings or demands. If you worked for me, I would foist you off on another department or just fire you immediately. I learned a long time ago that I can't fix you and I can't function with you and you need me a whole hell of lot more than I need you. Of course you don't recognize yourself in this description. That'd be your big problem. I'm really just writing this to once again remind your fellows that I am not trying to inhibit anyone having a good time in the comments. I am trying to inhibit those of you with no judgment and no ability to control yourselves.

So you tell me, folks. Do we need to ditch Haloscan and go to controlled comments, or is the sane majority willing to help me keep the comment threads readable by starving the trolls?

First Bank Closure of 2008

by Calculated Risk on 1/26/2008 09:06:00 AM

From the FDIC: FDIC Approves the Assumption of all the Deposits of Douglass National Bank, Kansas City, Missouri

The Board of Directors of the Federal Deposit Insurance Corporation (FDIC) today approved the assumption of all the deposits of Douglass National Bank, Kansas City, Missouri, by Liberty Bank and Trust Company, New Orleans, Louisiana.This is a small bank, and by itself this closing is inconsequential. However this might become a trend, with a number of small FDIC-insured banks going under because of bad loans. I suspect the over-under line for bank failures this year has to be much higher this year than in 2007.

Douglass National, with $58.5 million in total assets and $53.8 million in total deposits as of October 22, 2007, was closed today by the Office of the Comptroller of the Currency, and the FDIC was named receiver.

... the FDIC estimates that the cost to its Deposit Insurance Fund is approximately $5.6 million. Douglass National is the first FDIC-insured bank to fail this year, and the first in Missouri since Superior National Bank, Kansas City, was closed on April 14, 1994. Last year, three FDIC-insured institutions failed.

Friday, January 25, 2008

Traders: Don't Put Jumbos in my TBAs

by Anonymous on 1/25/2008 06:06:00 PM

This probably wasn't what Congress had in mind, ya think?

NEW YORK (Reuters) - A key element of the stimulus package aimed at jump-starting the ailing U.S. housing market may have the unintended consequence of raising mortgage rates, said analysts studying the plan.TBA works the way it does precisely because "agency" loans are basically interchangeable: the normal variation just isn't wide enough to prevent traders from pricing deals before seeing the exact loan composition.