RSS Feed

RSS Feed by Calculated Risk on 12/27/2010 06:11:00 PM

Showing posts with label Freddie Mac. Show all posts

Showing posts with label Freddie Mac. Show all posts

Monday, December 27, 2010

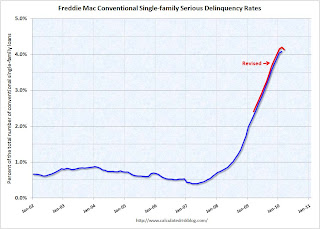

Freddie Mac: 90+ Day Delinquency Rate increases in November

Freddie Mac reported that the serious delinquency rate increased to 3.85% in November from 3.82% in October. The following graph shows the Freddie Mac serious delinquency rate (loans that are "three monthly payments or more past due or in foreclosure"):

Some of the rapid increase last year was probably because of foreclosure moratoriums, and from modification programs because loans in trial mods were considered delinquent until the modifications were made permanent. As modifications have become permanent, they are no longer counted as delinquent.

The increases in October and November are probably related to the new foreclosure moratoriums. The rate will probably start to decrease again in 2011.

Note: Fannie Mae reported the serious delinquency rate declined slightly in October (they are a month behind Freddie Mac).

Monday, August 09, 2010

Fannie, Freddie, FHA REO Inventory Increases 13% in Q2 from Q1 2010

by Calculated Risk on 8/09/2010 11:25:00 AM

The combined REO (Real Estate Owned) inventory for Fannie, Freddie and the FHA increased by 13% in Q2 2010 from Q1 2010. The REO inventory (lender Real Estate Owned) increased 74% compared to Q2 2009 (year-over-year comparison). Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the REO inventory for Fannie, Freddie and FHA through Q2 2010.

The REO inventory for the "Fs" has increased sharply over the last year, from 135,868 at the end of Q2 2009 to 236,338 at the end of Q2 2010.

This is a new record for Fannie and Freddie; the FHA's REO inventory decreased slightly in Q2 2010.

Remember this is just a portion of the total REO inventory. Private label securities and banks and thrifts also hold a substantial number of REOs.

Freddie Mac: $4.7 billion Loss, REO Inventory increases 79% YoY

by Calculated Risk on 8/09/2010 09:40:00 AM

Freddie Mac reported: "a net loss of $4.7 billion for the quarter ended June 30, 2010, compared to a net loss of $6.7 billion for the quarter ended March 31, 2010." and the FHFA requested another $1.8 billion from Treasury. (ht jb)

"We recognize that high unemployment and other factors still pose very real challenges for the housing market" said Freddie Mac Chief Executive Officer Charles E. Haldeman, Jr. Click on graph for larger image in new window.

Click on graph for larger image in new window.

Freddie Mac reported that their REO inventory increased 79% year over year, from 34,699 in Q2 2009 to 62,178 in Q2 2010.

REO: Real Estate Owned.

See page 16 of the Second Quarter 2010 Financial Results Supplement

This graph shows the rapid increase in REO.

Note: last week I posted a graph of the Fannie Mae REO.

Monday, July 12, 2010

FHFA attempting to recoup some losses of Fannie and Freddie

by Calculated Risk on 7/12/2010 02:15:00 PM

From the Federal Housing Finance Agency: FHFA Issues Subpoenas for PLS Documents

FHFA, as Conservator of Fannie Mae and Freddie Mac (the Enterprises), has issued 64 subpoenas to various entities, seeking documents related to private-label mortgage-backed securities (PLS) in which the two Enterprises invested. The documents will enable the FHFA to determine whether PLS issuers and others are liable to the Enterprises for certain losses they have suffered on PLS. If so, the Conservator expects to recoup funds, which would be used to offset payments made to the Enterprises by the U.S. Treasury.Many of the originators of the PLS mortgages are no longer in business (New Century, etc.), however most of the PLS issuers still exist.

...

Before and during conservatorship, the Enterprises sought to assess and enforce their rights as investors in PLS, in an effort to recoup losses suffered in connection with their portfolios. Specifically, the Enterprises have attempted to determine whether misrepresentations, breaches of warranties or other acts or omissions by PLS counterparties would require repurchase of loans underlying the PLS by the counterparties and whether other remedies might be appropriate. However, difficulty in obtaining the loan documents has presented a challenge to the Enterprises’ efforts. FHFA has therefore issued these subpoenas for various loan files and transaction documents pertaining to loans securing the PLS to trustees and servicers controlling or holding that documentation.

Saturday, June 26, 2010

Freddie Mac: 90+ Day Delinquency Rate steady in May

by Calculated Risk on 6/26/2010 09:51:00 PM

Click on graph for larger image in new window.

Click on graph for larger image in new window.

Freddie Mac reported yesterday that the rate of serious delinquencies - at least 90 days behind - for conventional loans in its single-family guarantee business was steady at 4.06% in May, the same rate as April, and up sharply from 2.73% in May 2009.

"Single-family delinquencies are based on the number of mortgages 90 days or more delinquent or in foreclosure as of period end ..."

The "good" news is the delinquency rate has stopped rising rapidly. However some of the earlier increase was because of foreclosure mortatoriums, and distortions from modification programs - loans in trial mods were considered delinquent until the modifications were made permanent.

Even though Freddie Mac has started foreclosing, modifying loans, and accepting short sales, the number of new 90+ day delinquencies has kept pace.

The data from Fannie Mae will be released next week ...

Wednesday, May 05, 2010

Freddie Mac: Q1 Net Loss $6.7 billion, Asks for $10.6 billion

by Calculated Risk on 5/05/2010 05:40:00 PM

"[A]s we have noted for many months now, housing in America remains fragile with historically high delinquency and foreclosure levels, and high unemployment among the key risks."

Freddie Mac Chief Executive Officer Charles E. Haldeman, Jr.

Press Release: Freddie Mac Reports First Quarter 2010 Financial Results

First quarter 2010 net loss was $6.7 billion. ...The first quarter loss in 2009 was $9.97 billion and the Q4 2009 loss was $6.5 billion. The losses keep coming, but last quarter Haldeman warned about "a potential large wave of foreclosures", so it appears he is a little more optimistic.

Net worth deficit was $10.5 billion at March 31, 2010, driven primarily by a significant adverse impact due to the change in accounting principles. ...

The Federal Housing Finance Agency (FHFA), as Conservator, will submit a request on the company’s behalf to Treasury for a draw of $10.6 billion under the Senior Preferred Stock Purchase Agreement (Purchase Agreement).

emphasis added

Saturday, May 01, 2010

Freddie Mac: 90+ Day Delinquency Rate at 4.13% in March

by Calculated Risk on 5/01/2010 11:57:00 AM

Note: Freddie Mac reported the serious delinquency rate decreased in March from February, but that is only after the previous months were revised higher. Also there might be some distortion from the modification program - loans in trial mods were considered delinquent until the modifications were made permanent. Click on graph for larger image in new window.

Click on graph for larger image in new window.

Freddie Mac reported that the rate of serious delinquencies - at least 90 days behind - for conventional loans in its single-family guarantee business decreased to 4.13% in March 2010, down from 4.20% in February - and up from 2.41% in March 2009.

"Single-family delinquencies are based on the number of mortgages 90 days or more delinquent or in foreclosure as of period end ..."

The data from Fannie Mae will be released next week ...

Monday, March 22, 2010

Obama Adminstration to outline changes for Fannie and Freddie

by Calculated Risk on 3/22/2010 08:45:00 PM

There will be hearing tomorrow about Fannie and Freddie, but the Obama administration will only "outline broad principles".

From Jim Puzzanghera at the LA Times: Pressure rises to overhaul Fannie Mae, Freddie Mac

[I]n a hearing Tuesday, lawmakers will start pressing the Obama administration for an exit strategy [for Fannie Mae and Freddie Mac] ...And from Nick Timiraos and Michale Crittenden at the WSJ: New Plan to Reshape Mortgage Market

"It's clear that Fannie and Freddie, as they currently exist, should be put out of existence, which means the important question is what combination of entities public and private will replace them," said Rep. Barney Frank (D-Mass.), chairman of the House Financial Services Committee.

He has called Treasury Secretary Timothy F. Geithner to testify at the hearing before his committee about how to do that.

The administration will outline broad principles for the future of the mortgage market at the hearing, including stronger consumer protections and explicit guarantees for any government backstop of mortgages.Clearly we can't go back to a structure that privatizes profits and socializes losses.

"The housing-finance system cannot continue to operate as it has in the past," Mr. Geithner says in prepared testimony. The administration won't issue a detailed overhaul proposal until later this year.

Friday, February 26, 2010

Freddie Mac: Delinquencies Increase Sharply in January

by Calculated Risk on 2/26/2010 02:24:00 PM

Here is the monthly Freddie Mac hockey stick graph ... Click on graph for larger image in new window.

Click on graph for larger image in new window.

Freddie Mac reported that the rate of serious delinquencies - at least 90 days behind - for conventional loans in its single-family guarantee business increased to 4.03% in January 2010, up from 3.87% in December - and up from 1.98% in January 2009.

"Single-family delinquencies are based on the number of mortgages 90 days or more delinquent or in foreclosure as of period end ..."

Just more evidence of the growing delinquency problem, although some of these loans may be in the trial modification programs and are still included as delinquent until they are converted to a "permanent mod". If the trial is cancelled, the loan stays delinquent (until foreclosure).

The data from Fannie Mae will be released later ...

Wednesday, February 10, 2010

Freddie Mac to Buy Out Seriously Delinquent Loans

by Calculated Risk on 2/10/2010 12:26:00 PM

Press Release: Freddie Mac To Purchase Substantial Number of Seriously Delinquent Loans From PC Securities

Freddie Mac (NYSE: FRE) announced today that it will purchase substantially all 120 days or more delinquent mortgage loans from the company's related fixed-rate and adjustable-rate (ARM) mortgage Participation Certificate (PC) securities.This makes sense (since the costs are lower to buy the nonperforming loans back), and this has been in the works since Treasury increased the GSE portfolio limits in December. Back in December, Credit Suisse analysts argued this would happen (from Bloomberg):

The company's purchases of these loans from related PCs should be reflected in the PC factor report published after the close of business on March 4, 2010, and the corresponding principal payments would be passed through to fixed-rate and ARM PC holders on March 15 and April 15, respectively. The decision to effect these purchases stems from the fact that the cost of guarantee payments to security holders, including advances of interest at the security coupon rate, exceeds the cost of holding the nonperforming loans in the company's mortgage-related investments portfolio as a result of the required adoption of new accounting standards and changing economics. In addition, the delinquent loan purchases will help Freddie Mac preserve capital and reduce the amount of any additional draws from the U.S. Department of the Treasury. The purchases would not affect Freddie Mac's activities under the Making Home Affordable Program.

“This announcement increases the prospect of large-scale voluntary buyouts by removing the portfolio cap hurdle and helping funding by potentially increasing debt-investor confidence,”

Thursday, January 28, 2010

Freddie Mac: Delinquencies Increase Sharply in December

by Calculated Risk on 1/28/2010 11:04:00 AM

Here is the monthly Freddie Mac hockey stick graph ... Click on graph for larger image in new window.

Click on graph for larger image in new window.

Freddie Mac reported that the rate of serious delinquencies - at least 90 days behind - for conventional loans in its single-family guarantee business increased to 3.87% in December 2009, up from 3.72% in November - and up from 1.72% in December 2008.

"Single-family delinquencies are based on the number of mortgages 90 days or more delinquent or in foreclosure as of period end ..."

Just more evidence of the growing delinquency problem, although some of these loans may be in the trial modification programs and are still included as delinquent until they become permanent.

Fannie Mae should report soon ...

Thursday, December 24, 2009

Treasury: More Support for Fannie and Freddie

by Calculated Risk on 12/24/2009 03:14:00 PM

From the WSJ: U.S. Uncaps Support for Fannie, Freddie

The Treasury said it would provide capital as needed to Fannie Mae and Freddie Mac over the next three years, in a move aimed at soothing investors' concerns about the government's continued support of the mortgage giants.A press release before the holiday ... I was wondering what would come out today.

Treasury also will suspend its purchases of the companies' mortgage-backed securities ...

Under the new terms announced Thursday, the cap on Treasury's support would increase according to how much each firm loses in a quarter, beginning the first quarter of next year and through 2012. The cap in place at the end of 2012 would apply thereafter.

Update: Here is the press release: TREASURY ISSUES UPDATE ON STATUS OF SUPPORT FOR HOUSING PROGRAMS (ht Steelhead)

Wednesday, November 11, 2009

Fannie, Freddie, Counterparty Risk and More

by Calculated Risk on 11/11/2009 10:08:00 PM

Yesterday I posted some excerpt from Freddie Mac's 10-Q:

We believe that several of our mortgage insurance counterparties are at risk of falling out of compliance with regulatory capital requirements, which may result in regulatory actions that could threaten our ability to receive future claims payments, and negatively impact our access to mortgage insurance for high LTV loans.The WSJ has more tonight, including the risks to Fannie Mae: Fannie, Freddie Warn on More Losses

Fannie Mae has about $109.5 billion of mortgage-insurance coverage in force ... Freddie Mac had $63.4 billion in mortgage insurance and $12.2 billion in bond insurance.And this a key sentence:

The reduction in private insurance coverage has contributed to the rise in the volume of loans backed by the Federal Housing Administration ...Instead of using private mortgage insurance for loans greater than 80% LTV, low down payment borrowers are now using FHA insurance.

That will probably end well ...

Also - the WSJ has more on the new FDIC "Prudent Commercial Real Estate Loan Workouts" guidance issued Oct 30th: Banks Hasten to Adopt New Loan Rules. Here is the new FDIC guidance that states performing loans "made to creditworthy borrowers" will not require write downs "solely because the value of the underlying collateral declined".

Monday, October 26, 2009

SF Fed: Recent Developments in Mortgage Finance

by Calculated Risk on 10/26/2009 03:30:00 PM

From San Francisco Fed Senior Economist John Krainer: Recent Developments in Mortgage Finance

As the U.S. housing market has moved from boom in the middle of the decade to bust over the past two years, the sources of mortgage funding have changed dramatically. The government-sponsored enterprises—Fannie Mae, Freddie Mac, and Ginnie Mae—now own or guarantee an overwhelming share of originations. At the same time, non-agency mortgage securitization and loans retained in lender portfolios have largely dried up.

Click on graph for slightly larger in new window.

Click on graph for slightly larger in new window.This is figure 3 from the Economic Letter. This shows the surge in non-agency securitized loans, and loans held in bank portfolios, in 2004 through 2006 (the worst loans).

[T]he sources of mortgage finance have shifted as the housing market has gone from boom to bust. Figure 3 plots the evolution of these funding sources over the past decade. Fannie Mae and Freddie Mac combined have consistently been the largest players in the market, owning or guaranteeing about half or more of the mortgages in the sample at any given time. Non-agency securitization peaked in the first quarter of 2006, when it accounted for nearly 40% of new originations. Finally, the share of mortgages retained in the originating institution's portfolio averaged about 15% throughout the boom, but has fallen considerably since.Although Krainer doesn't mention it, notice the increase in bank portfolio loans in early 2007 - that was probably because the banks were stuck with loans when the securitization market seized up.

...

In the present day, when Ginnie Mae's activities are included, the three GSEs are providing unprecedented support to the housing market—owning or guaranteeing almost 95% of the new residential mortgage lending.

Krainer concludes:

With the vast majority of current mortgage lending now intermediated in some form by the GSEs, it will be difficult for the housing market to return to normal.Note: Tanta wrote this last year on the naming of the GSEs: On Maes and Macs. An excerpt:

Trivia buffs will know that once upon a time there were three "agencies": the Government National Mortgage Association, the Federal National Mortgage Association, and the Federal Home Loan Mortgage Corporation. It didn't take all that long for market participants to start coming up with pronunciations for the abbreviations GNMA (Ginnie Mae), FNMA (Fannie Mae), and FHLMC (Freddie Mac, which makes no sense whatsoever except that nobody liked "Filly Mac." ... Old farts whose favorite childhood treat was a box of Pixies will remember the old-time candy company Fannie May, whose name is said to have inspired the whole thing, probably in the throes of a major sugar rush.

Friday, October 23, 2009

Freddie Mac: Delinquency Rate Rises to 3.33 Percent

by Calculated Risk on 10/23/2009 11:59:00 AM

NOTE: I'll have some more thoughts on existing home sales soon. Click on graph for large image.

Click on graph for large image.

This graph shows the Freddie Mac single family delinquency rate since January 2005.

Here is the Freddie Mac portfolio data.

From Reuters: Freddie Mac Sept portfolio up, delinquencies jump (ht Ron at WallStreetPit)

Delinquencies ... jumped to 3.33 percent of its book of business in September from 3.13 percent in August and 1.22 percent in September 2008.

The multifamily delinquency rate accelerated slightly in September to 0.11 percent from 0.10 percent in August. A year earlier it was 0.01 percent..

Monday, August 10, 2009

Freddie Mac: Taylor Bean Losses could be "Significant"

by Calculated Risk on 8/10/2009 12:49:00 PM

From Bloomberg: Freddie Mac Says Its Loss From Taylor Bean May Be 'Significant'

Freddie Mac ... said the collapse of lender Taylor, Bean & Whitaker Mortgage Corp. may cause it “significant” losses.From the SEC filing:

...

The Ocala, Florida-based lender accounted for about 5.2 percent of Freddie Mac’s single-family mortgage purchases last year ... Freddie Mac can force lenders to repurchase defaulted loans that weren’t of the credit quality they represented, a use of its contracts already made harder by the collapses of IndyMac Bancorp., Washington Mutual Inc. and Lehman Brothers Holdings Inc., the company said.

...

Brian Faith, a spokesman for Fannie Mae, Freddie Mac’s Washington-based rival, said last week his company hasn’t done business with Taylor Bean “for some time.”

On August 4, 2009, we notified Taylor, Bean & Whitaker Mortgage Corp., or TBW, that we had terminated its eligibility, for cause, as a seller and servicer for us effective immediately. TBW accounted for approximately 5.2% and 2.7% of our single-family mortgage purchase volume activity for full-year 2008 and the six months ended June 30, 2009, respectively. We are in the process of determining our total exposure to TBW in the event it cannot perform its contractual obligations to us. The amount of our losses in such event could be significant.

Friday, August 07, 2009

Freddie Mac: House Price Improvement "Largely Seasonal"

by Calculated Risk on 8/07/2009 04:22:00 PM

Freddie Mac Press Release:

Freddie Mac had a positive net worth of $8.2 billion at June 30, 2009. As a result, no additional funding was required from Treasury under the terms of the Senior Preferred Stock Purchase Agreement (Purchase Agreement) for the second quarter.No mention of the amount of nonperforming loans.

...

Provision for credit losses was $5.2 billion for the second quarter of 2009, compared to $8.8 billion for the first quarter of 2009. The decrease was driven by a reduced rate of growth in the company's loan loss reserve due to the recent modest national home price improvements, which the company believes to be largely seasonal.

emphasis added

Wednesday, August 05, 2009

WaPo: Good Bank, Bad Bank for Fannie and Freddie?

by Calculated Risk on 8/05/2009 08:09:00 PM

From Zachary A. Goldfarb and David Cho at the WaPo: Administration Considers Splitting Fannie Mae, Freddie Mac

The Obama administration launched a broad government effort this week to overhaul mortgage giants Fannie Mae and Freddie Mac and is considering splitting the companies and putting their troubled assets in a new federally backed corporation, administration officials said.There are no details on a proposed structure.

...

The companies' regulator ... confirmed that the administration is discussing the "good bank bad bank" model.

Thursday, July 30, 2009

Regulator: GSEs Unlikely to Fully Repay Bailout

by Calculated Risk on 7/30/2009 01:51:00 PM

From the WSJ: GSEs Unlikely to Repay U.S. in Full

... "My view is that some assets in the senior preferred will have to be left behind as they come out of conservatorship," Federal Housing Finance Agency Director James B. Lockhart said Thursday in response to a question at a panel discussion in Washington. "That will mean that some of the losses will never be repaid."I'm shocked!

The Treasury has agreed to pump $200 billion into each company in order to keep them solvent. In exchange, the government receives senior preferred stock that pays a 10% dividend. So far, it has injected $85 billion in total into the companies, but Lockhart said that figure was likely to rise in the coming months.

Fannie and Freddie together own or guarantee $5.4 trillion in mortgages. ...

Mr. Lockhart said Fannie and Freddie would likely see their reserves continue to decline next year, but could return to strong profits in two to three years.

Monday, June 29, 2009

Freddie Mac June Investor Presentation

by Calculated Risk on 6/29/2009 08:48:00 AM

Here are a few graphs from the Freddie Mac June Investor Presentation. Click on graph for large image.

Click on graph for large image.

The first graph shows the average LTV of the Freddie Portfolio (graph doesn't start at zero).

The second graph shows the current breakdown by LTV and credit score.

According to Freddie Mac's estimate, 17% of the mortgages in their portfolio have negative equity. Another 11% of the loans have less than 10% equity.

Another 11% of the loans have less than 10% equity.

According to the Census Bureau, 51.6 million U.S. owner occupied homes had mortgages (end of 2007, see data here)

This would suggest that 8.8 million households have negative equity (51.6 million times 17%), and another 5.7 have 10% or less equity. However, the loans from Freddie Mac were better than most, and this is probably the lower bound for homeowners with negative equity. The third graphs show how the LTV breakdown has shifted over time as house prices have fallen.

The third graphs show how the LTV breakdown has shifted over time as house prices have fallen.

I'm surprised that any loans had negative equity in 2004, but just over 10% of the portfolio appeared to have LTV portfolio risk in 2004. Falling house prices has changed the mix!

Note: I'd consider the Zillow estimate of 20.4 million homeowners with negative equity as the upper bound (and I think their estimate is too high).

About 20.4 million of the 93 million houses, condos and co- ops in the U.S. were worth less than their loans as of March 31, according to Seattle-based real estate data service Zillow.com.There is much more in the Freddie Mac presentation.