RSS Feed

RSS Feed by Calculated Risk on 8/24/2021 01:02:00 PM

Tuesday, August 24, 2021

New Home Prices

As part of the new home sales report released this morning, the Census Bureau reported the number of homes sold by price and the average and median prices.

From the Census Bureau: "The median sales price of new houses sold in July 2021 was $390,500. The average sales price was $446,000."

The following graph shows the median and average new home prices.

Click on graph for larger image.

Click on graph for larger image.

During the housing bust, the builders had to build smaller and less expensive homes to compete with all the distressed sales. When housing started to recovery - with limited finished lots in recovering areas - builders moved to higher price points to maximize profits.

Then the average and median house prices mostly moved sideways since 2017 due to home builders offering more lower priced homes. Prices picked up during the pandemic, and really picked up recently.

The average price in July 2021 was a record $446,00, up 18% year-over-year. The median price was a record $390,500, up 18% year-over-year.

The second graph shows the percent of new homes sold by price.

Very few new homes sold were under $200K in July 2021 (about 1.6% of all homes). This is down from 56% in 2002. In general, the under $200K bracket is going away.

Very few new homes sold were under $200K in July 2021 (about 1.6% of all homes). This is down from 56% in 2002. In general, the under $200K bracket is going away.

The $400K and greater than $500K+ brackets increased significantly over the last decade.

The average price in July 2021 was a record $446,00, up 18% year-over-year. The median price was a record $390,500, up 18% year-over-year.

The second graph shows the percent of new homes sold by price.

Very few new homes sold were under $200K in July 2021 (about 1.6% of all homes). This is down from 56% in 2002. In general, the under $200K bracket is going away.

Very few new homes sold were under $200K in July 2021 (about 1.6% of all homes). This is down from 56% in 2002. In general, the under $200K bracket is going away. The $400K and greater than $500K+ brackets increased significantly over the last decade.

Half of new homes (about 50% in July) in the U.S., are in the $200K to $400K range. The fastest growing price segment over the last 2 years has been the $400K to $500K range.

A few Comments on July New Home Sales

by Calculated Risk on 8/24/2021 11:13:00 AM

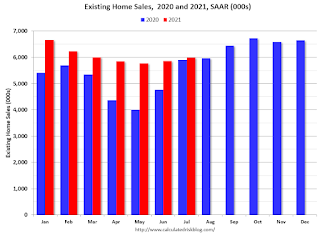

New home sales for July were reported at 708,000 on a seasonally adjusted annual rate basis (SAAR). Sales for the previous three months were revised up, combined.

This was somewhat above consensus expectations for July, but still down 27.2% year-over-year - since sales increased sharply following the early months of the pandemic. The new home sales rate is now slightly below the pre-pandemic level of around 740 thousand (the three months previous to pandemic).

Click on graph for larger image.

Click on graph for larger image.This graph shows new home sales for 2020 and 2021 by month (Seasonally Adjusted Annual Rate).

The year-over-year comparisons were easy in the first half of 2021 - especially in March and April.

However, sales will likely be down year-over-year for the remainder of 2021 - since the selling season was delayed in 2020.

And on inventory: note that completed inventory (3rd graph in previous post) is near record lows, but inventory under construction is closer to normal.

This graph shows the months of supply by stage of construction.

This graph shows the months of supply by stage of construction.The inventory of completed homes for sale was at 36 thousand in July, just above the record low of 33 thousand in March, April and May 2021. That is about 0.6 months of completed supply (just above the record low).

The inventory of new homes under construction is at 3.8 months - slightly above the normal level.

However, a record 105 thousand homes have not been started - about 1.8 months of supply - about double the normal level.

New Home Sales Increase to 708,000 Annual Rate in July

by Calculated Risk on 8/24/2021 10:12:00 AM

The Census Bureau reports New Home Sales in July were at a seasonally adjusted annual rate (SAAR) of 708 thousand.

The previous three months were revised up, combined.

Sales of new single‐family houses in July 2021 were at a seasonally adjusted annual rate of 708,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 1.0 percent above the revised June rate of 701,000, but is 27.2 percent below the July 2020 estimate of 972,000.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

New home sales are now declining year-over-year since sales soared following the first few months of the pandemic.

The second graph shows New Home Months of Supply.

The months of supply increased in July to 6.2 months from 6.0 months in June.

The months of supply increased in July to 6.2 months from 6.0 months in June. The all time record high was 12.1 months of supply in January 2009. The all time record low was 3.5 months, most recently in October 2020.

This is above the normal range (about 4 to 6 months supply is normal).

"The seasonally‐adjusted estimate of new houses for sale at the end of July was 367,000. This represents a supply of 6.2 months at the current sales rate."

On inventory, according to the Census Bureau:

On inventory, according to the Census Bureau: "A house is considered for sale when a permit to build has been issued in permit-issuing places or work has begun on the footings or foundation in nonpermit areas and a sales contract has not been signed nor a deposit accepted."Starting in 1973 the Census Bureau broke this down into three categories: Not Started, Under Construction, and Completed.

The third graph shows the three categories of inventory starting in 1973.

The inventory of completed homes for sale is just above the record low, but the combined total of completed and under construction is close to normal.

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).In July 2021 (red column), 63 thousand new homes were sold (NSA). Last year, 85 thousand homes were sold in July.

The all time high for July was 117 thousand in 2005, and the all time low for July was 26 thousand in 2010.

This was above expectations of 690 thousand sales SAAR, and sales in the three previous months were revised up, combined. I'll have more later today.

New York State Real Estate in July: Sales Up 22% YoY, Inventory Down 46% YoY

by Calculated Risk on 8/24/2021 08:05:00 AM

Note: I'm tracking data for many local markets around the U.S. I think it is especially important to watch inventory this year.

For New York State:

Closed sales in July 2021 were 13,765, up 32.6% from 10,384 in July 2020.

Active Listings in July 2021 were 44,025, down 19.5% from 54,700 in July 2020.

Inventory in July was up 1.4% from last month, and up 13.5% from the record low in March 2021.

South Florida Real Estate in July: Sales Up 22% YoY, Inventory Down 46% YoY

by Calculated Risk on 8/24/2021 07:54:00 AM

Note: I'm tracking data for many local markets around the U.S. I think it is especially important to watch inventory this year.

For the South Florida area:

Closed sales (house and condos) in July 2021 were 11,792, up 21.8% from 9,685 in July 2020.

Active Listings in July 2021 were 23,724, down 45.6% from 43,586 in July 2020.

Inventory in July was down 7.4% from last month and was at a record low.

Monday, August 23, 2021

Tuesday: New Home Sales, Richmond Fed Mfg

by Calculated Risk on 8/23/2021 09:00:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Start Higher, But Improve in The Afternoon

By abstaining on Friday, the average lender was forced to adjust today's rates slightly higher to account for the bond market weakness. In other words, this morning's rates were higher than Friday morning's.Tuesday:

As the day progressed, mortgage bonds improved enough for a friendly mid-day reprice. A majority of lenders pulled the trigger, thus helping rates close the gap with Friday's rates. Simply put, rates started the day moderately higher versus Friday morning, but are now only marginally higher (assuming the lender in question offered a mid-day price improvement). ... [30 year fixed 2.94%]

emphasis added

• At 10:00 AM ET, New Home Sales for July from the Census Bureau. The consensus is for 690 thousand SAAR, up from 676 thousand in June.

• Also at 10:00 AM, Richmond Fed Survey of Manufacturing Activity for August.

August 23rd COVID-19: Data reported on Monday is always low, and will be revised up as data is received

by Calculated Risk on 8/23/2021 07:47:00 PM

The CDC is the source for all data.

According to the CDC, on Vaccinations. Total doses administered: 363,267,789, as of a week ago 357,292,057. Average doses last week: 0.85 million per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Yesterday | Week Ago | Goal | |

| Percent fully Vaccinated | 51.5% | 51.5% | 50.8% | ≥70.0%1 |

| Fully Vaccinated (millions) | 171.1 | 170.8 | 168.7 | ≥2321 |

| New Cases per Day3 | 124,383 | 133,517 | 130,165 | ≤5,0002 |

| Hospitalized3🚩 | 77,727 | 80,362 | 71,466 | ≤3,0002 |

| Deaths per Day3🚩 | 691 | 725 | 664 | ≤502 |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37 day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

IMPORTANT: For "herd immunity" most experts believe we need 70% to 85% of the total population fully vaccinated (or already had COVID).

KUDOS to the residents of the 7 states that have achieved 60% of total population fully vaccinated: Vermont at 67.5%, Massachusetts, Maine, Connecticut, Rhode Island, Maryland and New Jersey at 60.5%.

The following 17 states and D.C. have between 50% and 59.9% fully vaccinated: Washington at 59.5%, New Hampshire, New York State, New Mexico, Oregon, District of Columbia, Virginia, Colorado, Minnesota, California, Hawaii, Delaware, Pennsylvania, Wisconsin, Florida, Nebraska, Iowa, Illinois, and Michigan at 50.0%.

Next up (total population, fully vaccinated according to CDC) are South Dakota at 48.4%, Ohio at 47.8%, Kentucky at 47.6%, Kansas at 47.3%, Arizona at 47.1%, Nevada at 46.8%, Utah at 46.7%, and Alaska at 46.6%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

MBA Survey: "Share of Mortgage Loans in Forbearance Slightly Decreases to 3.25%"

by Calculated Risk on 8/23/2021 04:00:00 PM

Note: This is as of August 15th.

From the MBA: Share of Mortgage Loans in Forbearance Slightly Decreases to 3.25%

The Mortgage Bankers Association’s (MBA) latest Forbearance and Call Volume Survey revealed that the total number of loans now in forbearance decreased by 1 basis point from 3.26% of servicers’ portfolio volume in the prior week to 3.25% as of August 15, 2021. According to MBA’s estimate, 1.6 million homeowners are in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance decreased 3 basis points to 1.66%. Ginnie Mae loans in forbearance decreased 3 basis points to 3.92%, while the forbearance share for portfolio loans and private-label securities (PLS) increased 10 basis points to 7.15%. The percentage of loans in forbearance for independent mortgage bank (IMB) servicers increased 2 basis points to 3.48%, and the percentage of loans in forbearance for depository servicers decreased 1 basis point to 3.35%.

“The share of loans in forbearance was little changed, as both new requests and exits were at a slower pace compared to the prior week. In fact, exits were at their slowest pace in over a year,” said Mike Fratantoni, MBA’s Senior Vice President and Chief Economist. “There were more new forbearance requests and re-entries for portfolio and PLS loans, leading to a 10-basis-point increase in their share. Portfolio and PLS loans now account for almost 50% of all depository servicer loans in forbearance and almost 40% of IMB servicer loans in forbearance, which highlights the importance of this investor category.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time. Most of the increase was in late March and early April 2020, and has trended down since then.

The MBA notes: "Total weekly forbearance requests as a percent of servicing portfolio volume (#) decreased relative to the prior week: from 0.06% to 0.05%.%"

Comments on July Existing Home Sales

by Calculated Risk on 8/23/2021 01:11:00 PM

Earlier: NAR: Existing-Home Sales Increased to 5.99 million in July

Two key points:

1) Existing home sales are somewhat above pre-pandemic levels rate of around 5.5 million SAAR (average six months prior to pandemic). Seasonally adjusted (SA) sales for July 2021 were also the highest since 2006 - about 2% above July 2020.

Some of the increase in sales over the previous year was probably related to record low mortgage rates, strong second home buying, a strong stock market and favorable demographics.

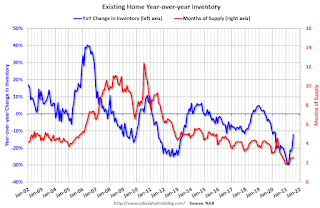

2) Inventory is very low, and was down 12.0% year-over-year (YoY) in July. Also, as housing economist Tom Lawler has noted, the local MLS data shows even a larger decline in active inventory (the NAR appears to include some pending sales in inventory). Lawler noted:

Months-of-supply at 2.6 months is still very low, but above the record low of 1.9 months set in December 2020 and January 2021. Inventory will be important to watch in 2021, see: Some thoughts on Housing Inventory

Click on graph for larger image.

Click on graph for larger image.

This graph shows existing home sales by month for 2020 and 2021.

The year-over-year comparison will be more difficult in the second half of the year.

The second graph shows existing home sales for each month, Not Seasonally Adjusted (NSA), since 2005.

Sales NSA in July (584,000) were 2.2% below sales in July 2020 (597,000).

Sales NSA in July (584,000) were 2.2% below sales in July 2020 (597,000).

Also, the delay in the 2020 buying season pushed the seasonally adjusted number to very high levels over the winter. This means there are going to be some difficult comparisons in the second half of 2021!

2) Inventory is very low, and was down 12.0% year-over-year (YoY) in July. Also, as housing economist Tom Lawler has noted, the local MLS data shows even a larger decline in active inventory (the NAR appears to include some pending sales in inventory). Lawler noted:

"As I’ve noted before, the inventory measure in most publicly-released local realtor/MLS reports excludes listings with pending contracts, but that is not the case for many of the reports sent to the NAR (referred to as the “NAR Report!”), Since the middle of last Spring inventory measures excluding pending listings have fallen much more sharply than inventory measures including such listings, and this latter inventory measure understates the decline in the effective inventory of homes for sale over the last several months."

It seems likely that active inventory is down close to 30% year-over-year.

Click on graph for larger image.

Click on graph for larger image.This graph shows existing home sales by month for 2020 and 2021.

The year-over-year comparison will be more difficult in the second half of the year.

The second graph shows existing home sales for each month, Not Seasonally Adjusted (NSA), since 2005.

Sales NSA in July (584,000) were 2.2% below sales in July 2020 (597,000).

Sales NSA in July (584,000) were 2.2% below sales in July 2020 (597,000). There were fewer selling days in July 2021 than in July 2020, so the SA numbers were higher than last year, even though the NSA numbers were lower.

This was the second highest sales for July, NSA, since 2006.

This was the second highest sales for July, NSA, since 2006.

Housing Inventory August 23rd Update: Inventory Increased Week-over-week, Up 41% from Low in early April

by Calculated Risk on 8/23/2021 11:50:00 AM

Tracking existing home inventory will be very important this year.

Click on graph for larger image in graph gallery.

Click on graph for larger image in graph gallery.

This inventory graph is courtesy of Altos Research.

As of August 20th, inventory was at 432 thousand (7 day average), compared to 594 thousand for the same week a year ago. That is a decline of 27.3%.

Compared to the same week in 2019, inventory is down 55%.

A week ago, inventory was at 422 thousand, and was down 29.8% YoY.

Seasonally, inventory has bottomed. Inventory was about 40.8% above the record low in early April.

A couple of interesting points from 2019: In 2019, inventory bottomed at 814 thousand in February (so inventory is still very low compared to normal levels). And, in 2019, inventory peaked at 972 thousand in early August (an increase of about 19% from the low). So inventory is less than half of what we'd normally expect, however inventory has increased (as a percentage) more than normal.

Key question: Usually inventory peaks in the Summer, and then declines into the Fall. Will inventory follow the normal seasonal pattern, or will inventory continue to increase over the coming months? This will be important to watch for house prices and housing activity.

Mike Simonsen discusses this data regularly on Youtube.

Altos Research has also seen a significant pickup in price decreases - back to the level of a year ago - but still well below a normal rate for August.

NAR: Existing-Home Sales Increased to 5.99 million in July

by Calculated Risk on 8/23/2021 10:11:00 AM

From the NAR: Existing-Home Sales Climb 2.0% in July

Existing-home sales rose in July, marking two consecutive months of increases, according to the National Association of Realtors®. Three of the four major U.S. regions recorded modest month-over-month gains, and the fourth remained level. Figures varied from a year-over-year perspective as two regions saw gains, one witnessed a decline and one was unchanged.

Total existing-home sales, completed transactions that include single-family homes, townhomes, condominiums and co-ops, grew 2.0% from June to a seasonally adjusted annual rate of 5.99 million in July. Sales inched up year-over-year, increasing 1.5% from a year ago (5.90 million in July 2020).

...

Total housing inventory at the end of July totaled 1.32 million units, up 7.3% from June's supply and down 12.0% from one year ago (1.50 million). Unsold inventory sits at a 2.6-month supply at the present sales pace, up slightly from the 2.5-month figure recorded in June but down from 3.1 months in July 2020.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1993.

Sales in July (5.99 million SAAR) were up 2.0% from last month, and were 1.5% above the July 2020 sales rate.

The second graph shows nationwide inventory for existing homes.

According to the NAR, inventory increased to 1.32 million in July from 1.23 million in June.

According to the NAR, inventory increased to 1.32 million in July from 1.23 million in June.Headline inventory is not seasonally adjusted, and inventory usually decreases to the seasonal lows in December and January, and peaks in mid-to-late summer.

The last graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Since inventory is not seasonally adjusted, it really helps to look at the YoY change. Note: Months-of-supply is based on the seasonally adjusted sales and not seasonally adjusted inventory.

Inventory was down 12.0% year-over-year in July compared to July 2020.

Inventory was down 12.0% year-over-year in July compared to July 2020.

Months of supply increased to 2.6 months in July from 2.5 months in June.

This was slightly above the consensus forecast. I'll have more later.

The last graph shows the year-over-year (YoY) change in reported existing home inventory and months-of-supply. Since inventory is not seasonally adjusted, it really helps to look at the YoY change. Note: Months-of-supply is based on the seasonally adjusted sales and not seasonally adjusted inventory.

Inventory was down 12.0% year-over-year in July compared to July 2020.

Inventory was down 12.0% year-over-year in July compared to July 2020. Months of supply increased to 2.6 months in July from 2.5 months in June.

This was slightly above the consensus forecast. I'll have more later.

Seven High Frequency Indicators for the Economy

by Calculated Risk on 8/23/2021 08:27:00 AM

These indicators are mostly for travel and entertainment. It will interesting to watch these sectors recover as the pandemic subsides.

The TSA is providing daily travel numbers.

This data is as of August 22nd.

Click on graph for larger image.

Click on graph for larger image.This data shows the 7-day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Blue) and 2021 (Red).

The dashed line is the percent of 2019 for the seven day average.

The 7-day average is down 23.3% from the same day in 2019 (76.7% of 2019). (Dashed line)

There was a slow increase from the bottom starting in May 2020 - and then TSA data picked up in 2021 - but the dashed line was moving sideways, and has moved down recently.

The second graph shows the 7-day average of the year-over-year change in diners as tabulated by OpenTable for the US and several selected cities.

IMPORTANT: OpenTable notes: "we’ve updated the data including downloadable dataset from January 1, 2021 onward to compare seated diners from 2021 to 2019, as opposed to year over year." Thanks!

Thanks to OpenTable for providing this restaurant data:

Thanks to OpenTable for providing this restaurant data:

This data is updated through August 21, 2021.

This data is "a sample of restaurants on the OpenTable network across all channels: online reservations, phone reservations, and walk-ins. For year-over-year comparisons by day, we compare to the same day of the week from the same week in the previous year."

Note that this data is for "only the restaurants that have chosen to reopen in a given market". Since some restaurants have not reopened, the actual year-over-year decline is worse than shown.

Dining picked up during the holidays, then slumped with the huge winter surge in cases. Dining was generally picking up, but has moved down recently - especially in Florida and Texas. The 7-day average for the US is down 10% compared to 2019.

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

Thanks to OpenTable for providing this restaurant data:

Thanks to OpenTable for providing this restaurant data:This data is updated through August 21, 2021.

This data is "a sample of restaurants on the OpenTable network across all channels: online reservations, phone reservations, and walk-ins. For year-over-year comparisons by day, we compare to the same day of the week from the same week in the previous year."

Note that this data is for "only the restaurants that have chosen to reopen in a given market". Since some restaurants have not reopened, the actual year-over-year decline is worse than shown.

Dining picked up during the holidays, then slumped with the huge winter surge in cases. Dining was generally picking up, but has moved down recently - especially in Florida and Texas. The 7-day average for the US is down 10% compared to 2019.

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Blue is 2020 and Red is 2021.

The data is from BoxOfficeMojo through August 19th.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $107 million last week, down about 43% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $107 million last week, down about 43% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average. The red line is for 2021, black is 2020, blue is the median, dashed purple is 2019, and dashed light blue is for 2009 (the worst year on record for hotels prior to 2020).

Occupancy is above the horrible 2009 levels. With solid leisure travel, the Summer months had decent occupancy - but it is uncertain what will happen in the Fall with business travel - especially with the sharp increase in COVID pandemic cases and hospitalizations.

This data is through August 14th. The occupancy rate is down 8.4% compared to the same week in 2019. Note: Occupancy was up year-over-year, since occupancy declined sharply at the onset of the pandemic.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.Blue is for 2020. Red is for 2021.

As of August 13th, gasoline supplied was down 3.0% compared to the same week in 2019.

There have been four weeks so far this year when gasoline supplied was up compared to the same week in 2019.

This graph is from Apple mobility. From Apple: "This data is generated by counting the number of requests made to Apple Maps for directions in select countries/regions, sub-regions, and cities." This is just a general guide - people that regularly commute probably don't ask for directions.

There is also some great data on mobility from the Dallas Fed Mobility and Engagement Index. However the index is set "relative to its weekday-specific average over January–February", and is not seasonally adjusted, so we can't tell if an increase in mobility is due to recovery or just the normal increase in the Spring and Summer.

This data is through August 14th for the United States and several selected cities.

This data is through August 14th for the United States and several selected cities.The graph is the running 7-day average to remove the impact of weekends.

IMPORTANT: All data is relative to January 13, 2020. This data is NOT Seasonally Adjusted. People walk and drive more when the weather is nice, so I'm just using the transit data.

According to the Apple data directions requests, public transit in the 7 day average for the US is at 105% of the January 2020 level.

New York City is doing well by this metric, but subway usage in NYC is down sharply (next graph).

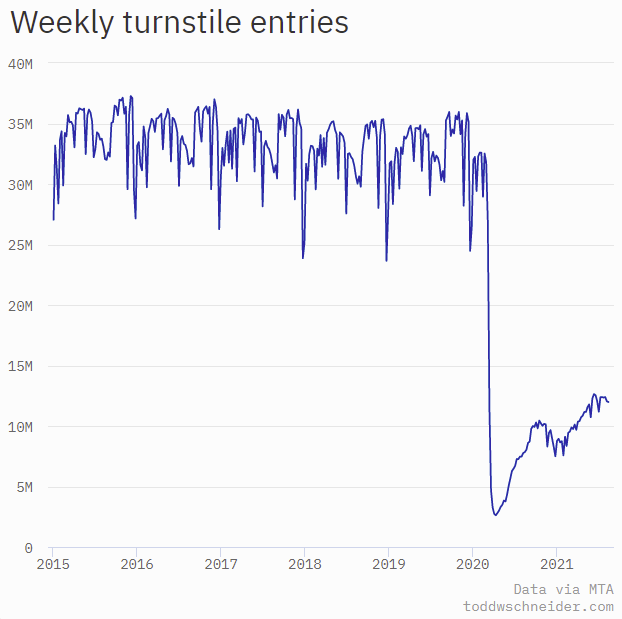

----- New York City Subway Usage -----

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider. This is weekly data since 2015.

This graph is from Todd W Schneider. This is weekly data since 2015.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider. This is weekly data since 2015.

This graph is from Todd W Schneider. This is weekly data since 2015. Most weeks are between 30 and 35 million entries, and currently there are over 12 million subway turnstile entries per week - and generally increasing.

This data is through Friday, August 20th.

Schneider has graphs for each borough, and links to all the data sources.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

This data is through Friday, August 20th.

Schneider has graphs for each borough, and links to all the data sources.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, August 22, 2021

Monday: Existing Home Sales

by Calculated Risk on 8/22/2021 07:29:00 PM

Weekend:

• Schedule for Week of August 22, 2021

Monday:

• At 8:30 AM ET, Chicago Fed National Activity Index for July. This is a composite index of other data.

• At 10:00 AM, Existing Home Sales for July from the National Association of Realtors (NAR). The consensus is for 5.81 million SAAR, down slightly from 5.86 million last month.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up 4 and DOW futures are up 30 (fair value).

Oil prices were down over the last week with WTI futures at $62.38 per barrel and Brent at $65.49 per barrel. A year ago, WTI was at $42, and Brent was at $44 - so WTI oil prices are UP about 50% year-over-year (oil prices collapsed at the beginning of the pandemic).

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.14 per gallon. A year ago prices were at $2.18 per gallon, so gasoline prices are up $0.96 per gallon year-over-year.

August 22nd COVID-19: Averaging Over 1 Million Doses Administered Last 4 Days

by Calculated Risk on 8/22/2021 04:33:00 PM

Note: Cases and Deaths are not updated on Sundays.

The CDC is the source for all data.

According to the CDC, on Vaccinations.

Total doses administered: 362,657,771, as of a week ago 356,433,665. Average doses last week: 0.89 million per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Yesterday | Week Ago | Goal | |

| Percent fully Vaccinated | 51.5% | 51.3% | 50.6% | ≥70.0%1 |

| Fully Vaccinated (millions) | 170.8 | 170.4 | 168.1 | ≥2321 |

| New Cases per Day3🚩 | 137,188 | 134,859 | 122,769 | ≤5,0002 |

| Hospitalized3🚩 | 79,310 | 80,298 | 69,269 | ≤3,0002 |

| Deaths per Day3🚩 | 738 | 688 | 600 | ≤502 |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37 day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

IMPORTANT: For "herd immunity" most experts believe we need 70% to 85% of the total population fully vaccinated (or already had COVID).

KUDOS to the residents of the 7 states that have achieved 60% of total population fully vaccinated: Vermont at 67.4%, Massachusetts, Maine, Connecticut, Rhode Island, Maryland and New Jersey at 60.4%.

The following 17 states and D.C. have between 50% and 59.9% fully vaccinated: Washington at 59.4%, New Hampshire, New York State, New Mexico, Oregon, District of Columbia, Virginia, Colorado, Minnesota, California, Hawaii, Delaware, Pennsylvania, Wisconsin, Florida, Nebraska, Iowa, Illinois, and Michigan at 50.0%.

Next up (total population, fully vaccinated according to CDC) are South Dakota at 48.4%, Ohio at 47.8%, Kentucky at 47.6%, Kansas at 47.2%, Arizona at 47.0%, Utah at 46.7%, Alaska at 46.6%, and Nevada at 46.6%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of hospitalizations reported.

Note that the shaded area will be revised up.

Columbus Real Estate in July: Sales Up 3% YoY, Inventory UP 4% YoY

by Calculated Risk on 8/22/2021 03:23:00 PM

The is only the second local market that I track that saw a year-over-year increase in active inventory in July.

Note: I'm tracking data for many local markets around the U.S. I think it is especially important to watch inventory this year.

Here is a summary post for many markets: Existing Home Inventory in July: Local Markets

For for the Columbus, Ohio area:

Closed sales in July 2021 were 3,630, up 2.7% from 3,536 in July 2020.

Active Listings in July 2021 were 3,079, up 4.2% from 2,955 in July 2020.

Months of Supply was 1.0 Months in July 2021, compared to 1.1 Months in July 2020.

Inventory in July was up 27.0% from last month, and up 87.9% from the all time low in March 2021.

30 Year Mortgage Rates "Stuck in the Middle" at 2.93%

by Calculated Risk on 8/22/2021 08:58:00 AM

From Matthew Graham at Mortgage News Daily: Rates Stuck in The Middle

Rates are on hold until the next chapter is written in the complex saga of covid versus the market. This isn't to say rates perfectly flat--simply that the prevailing momentum has been sideways for the past few weeks.

Since mortgage rates only change once or twice a day, we can use 10yr Treasury yields to see finer detail. This entire week took place in the fairly narrow range of 1.29 to 1.21, and it ended with yields precisely in the middle at 1.25%.

...

What does all this mean in plain English? Rates are low--much lower than most anyone expected at this point in the year. The key reason is "delta" and Fed's patient approach to changing rate-friendly policies. The lingering concerns about the nature of the post-covid economy also make the list. [30 year fixed 2.93%]

emphasis added

Click on graph for larger image.

Click on graph for larger image.This is a graph from Mortgage News Daily (MND) showing 30 year fixed rates from three sources (MND, MBA, Freddie Mac).

Go to MND and you can adjust the graph for different time periods.

30 year mortgage rates are just above the record lows in 2020.

Saturday, August 21, 2021

Indiana Real Estate in July: Sales Down 7% YoY, Inventory Down 25% YoY

by Calculated Risk on 8/21/2021 04:50:00 PM

Note: I'm tracking data for many local markets around the U.S. I think it is especially important to watch inventory this year.

Here is a summary post for many markets: Existing Home Inventory in July: Local Markets

For for the entire state Indiana:

Closed sales in July 2021 were 9,585, down 6.5% from 10,256 in July 2020.

Active Listings in July 2021 were 8,874, down 24.6% from 11,762 in July 2020.

Months of Supply was 1.1 Months in July 2021, compared to 1.6 Months in July 2020.

Inventory in July was up 14.6% from last month, and up 50.5% from the all time low in March 2021.

August 21st COVID-19: Hospitalizations over 80,000, Cases and Deaths Increasing

by Calculated Risk on 8/21/2021 04:46:00 PM

This is the 3rd consecutive day with over 1 million doses administered.

The 7-day average cases is the highest since February 1st.

The 7-day average hospitalizations is the highest since February 7th.

The 7-day average deaths is the highest since March 25th.

According to the CDC, on Vaccinations.

Total doses administered: 361,684,564, as of a week ago 355,768,825. Average doses last week: 0.85 million per day.

Total doses administered: 361,684,564, as of a week ago 355,768,825. Average doses last week: 0.85 million per day.

| COVID Metrics | ||||

|---|---|---|---|---|

| Today | Yesterday | Week Ago | Goal | |

| Percent fully Vaccinated | 51.3% | 51.2% | 50.6% | ≥70.0%1 |

| Fully Vaccinated (millions) | 170.4 | 170.0 | 168.1 | ≥2321 |

| New Cases per Day3🚩 | 137,188 | 134,859 | 122,769 | ≤5,0002 |

| Hospitalized3🚩 | 80,101 | 78,944 | 66,996 | ≤3,0002 |

| Deaths per Day3🚩 | 738 | 688 | 600 | ≤502 |

| 1 Minimum to achieve "herd immunity" (estimated between 70% and 85%). 2my goals to stop daily posts, 37 day average for Cases, Currently Hospitalized, and Deaths 🚩 Increasing 7 day average week-over-week for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

IMPORTANT: For "herd immunity" most experts believe we need 70% to 85% of the total population fully vaccinated (or already had COVID).

KUDOS to the residents of the 7 states that have achieved 60% of total population fully vaccinated: Vermont at 67.3%, Massachusetts, Maine, Connecticut, Rhode Island, Maryland and New Jersey at 60.3%.

The following 17 states and D.C. have between 50% and 59.9% fully vaccinated: Washington at 59.3%, New Hampshire, New York State, New Mexico, Oregon, District of Columbia, Virginia, Colorado, Minnesota, California, Hawaii, Delaware, Pennsylvania, Wisconsin, Florida, Nebraska, Iowa and Illinois at 50.3%.

Next up (total population, fully vaccinated according to CDC) are Michigan at 49.9%, South Dakota at 48.4%, Ohio at 47.7%, Kentucky at 47.5%, Kansas at 47.0%, Arizona at 46.9%, Utah at 46.7%, Alaska at 46.6%, and Nevada at 46.5%.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) and 7 day average (line) of positive tests reported.

Schedule for Week of August 22, 2021

by Calculated Risk on 8/21/2021 08:11:00 AM

The key reports this week are the second estimate of Q2 GDP, July New and Existing Home sales, and Personal Income and Outlays for July.

For manufacturing, the August Richmond and Kansas City Fed surveys will be released.

Fed Chair Jerome Powell will speak on "The Economic Outlook" at the Jackson Hole Symposium on Friday.

8:30 AM ET: Chicago Fed National Activity Index for July. This is a composite index of other data.

10:00 AM: Existing Home Sales for July from the National Association of Realtors (NAR). The consensus is for 5.81 million SAAR, down slightly from 5.86 million last month.

10:00 AM: Existing Home Sales for July from the National Association of Realtors (NAR). The consensus is for 5.81 million SAAR, down slightly from 5.86 million last month.The graph shows existing home sales from 1994 through the report last month.

Housing economist Tom Lawler expects the NAR to report 5.86 million SAAR.

10:00 AM: New Home Sales for July from the Census Bureau.

10:00 AM: New Home Sales for July from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 690 thousand SAAR, up from 676 thousand in June.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for August.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Durable Goods Orders for July from the Census Bureau. The consensus is for a 0.2% decrease in durable goods orders.

8:30 AM: Gross Domestic Product, 2nd quarter 2021 (second estimate). The consensus is that real GDP increased 6.7% annualized in Q2, up from the advance estimate of 6.5% in Q2.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for a increase slightly to 350 thousand from 348 thousand last week.

11:00 AM: the Kansas City Fed manufacturing survey for August.

Thursday through Saturday: Jackson Hole Economic Policy Symposium, Macroeconomic Policy in an Uneven Economy

8:30 AM ET: Personal Income and Outlays, July 2021. The consensus is for a 0.2% increase in personal income, and for a 0.3% increase in personal spending. And for the Core PCE price index to increase 0.3%.

10:00 AM: Speech, Fed Chair Jerome Powell, The Economic Outlook, At the Jackson Hole Economic Policy Symposium

10:00 AM: University of Michigan's Consumer sentiment index (Final for August). The consensus is for a reading of 70.9.

Friday, August 20, 2021

California July Housing: Sales down 2% YoY, "Home sales and prices curb in July"

by Calculated Risk on 8/20/2021 03:46:00 PM

The CAR reported: California housing market continues to normalize as home sales and prices curb in July, C.A.R. reports

California’s housing market moderated for the third straight month in July with both home sales and prices tempering from the heated market conditions seen over the past year, while still staying above pre-pandemic levels, the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.) said today.Note that inventory was up 15.4% from June to July, similar to the increase the previous month. Although the CAR doesn't report inventory, it appears inventory is down about 12% year-over-year.

Closed escrow sales of existing, single-family detached homes in California totaled a seasonally adjusted annualized rate of 428,980 in July, according to information collected by C.A.R. from more than 90 local REALTOR® associations and MLSs statewide. The statewide annualized sales figure represents what would be the total number of homes sold during 2021 if sales maintained the July pace throughout the year. It is adjusted to account for seasonal factors that typically influence home sales.

July home sales dipped 1.6 percent on a monthly basis from 436,020 in June and were down 2 percent from a year ago, when 437,890 homes were sold on an annualized basis. July’s sales level was the second highest level in a July in the past six years. Despite the downward trend, California home sales maintained a solid year-to-date increase of 27.3 percent.

“The California housing market continues to normalize from the white-hot conditions we experienced at the height of the pandemic with both sales and prices moderating as we slowly transition from the peak home-buying season into the fall,” said C.A.R. President Dave Walsh. “The market remains solid, however, as sales were still the second highest level for a July in the last six years, and the statewide median price continues to perform above last year’s level by double-digits. Housing supply, while improved, remains tight and market competition is still heated with homes flying off the market in record time.”

...

The state housing supply condition continued to improve with active listings reaching the highest level since last October. The number of for-sale properties increased 15.4 percent in July from the prior month as more homes were being listed on the market. Despite an increase in total active listings in July, new listings added in the month dipped slightly for the first time after gaining year-over-year for four straight months.

emphasis added