RSS Feed

RSS Feed by Calculated Risk on 2/18/2019 09:57:00 PM

Monday, February 18, 2019

Tuesday: NAHB homebuilder survey

Weekend:

• Schedule for Week of February 17, 2019

Tuesday:

• 10:00 AM, The February NAHB homebuilder survey. The consensus is for a reading of 59, up from 58. Any number above 50 indicates that more builders view sales conditions as good than poor.

From CNBC: Pre-Market Data and Bloomberg futures: S&P 500 and DOW futures are mostly unchanged (fair value).

Oil prices were up over the last week with WTI futures at $55.72 per barrel and Brent at $66.06 per barrel. A year ago, WTI was at $62, and Brent was at $65 - so WTI oil prices are down year-over-year, although Brent is essentially unchanged.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.33 per gallon. A year ago prices were at $2.52 per gallon, so gasoline prices are down 19 cents per gallon year-over-year.

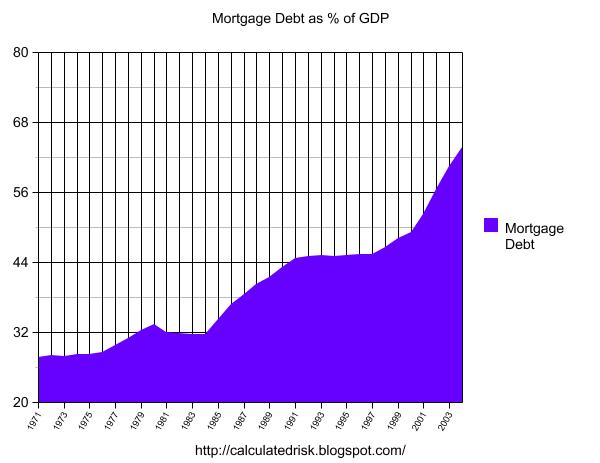

The Housing Bubble, Mortgage Debt as Percent of GDP

by Calculated Risk on 2/18/2019 09:50:00 AM

Two years ago, on Presidents' Day, I excerpted from a post I wrote in February 2005 (yes, 14 years ago).

In that 2005 post, I included a graph of household mortgage debt as a percent of GDP. Several readers asked if I could update the graph.

First, from 2005:

The following chart shows household mortgage debt as a % of GDP. Although mortgage debt has been increasing for years, the last four years have seen a tremendous increase in debt. Last year alone mortgage debt increased close to $800 Billion - almost 7% of GDP. ...CR Note: And a serious problem is what happened!

Many homeowners have refinanced their homes, in essence using their homes as an ATM.

It wouldn't take a RE bust to impact the general economy. Just a slowdown in both volume (to impact employment) and in prices (to slow down borrowing) might push the general economy into recession. An actual bust, especially with all of the extensive sub-prime lending, might cause a serious problem.

The second graph shows household mortgage debt as a percent of GDP through Q3 2018. Hopefully the graphs have improved!

The second graph shows household mortgage debt as a percent of GDP through Q3 2018. Hopefully the graphs have improved!The "bubble" is pretty obvious on this graph, and the sharp increase in mortgage debt was one of the warning signs.

Sunday, February 17, 2019

Oil: Rig Counts Rose Again

by Calculated Risk on 2/17/2019 11:10:00 PM

A few comments from Steven Kopits of Princeton Energy Advisors LLC on February 17, 2019:

• Oil rig counts rose again, +3 to 857. This is not what oil prices would have suggested.

• Horizontal oil rig counts fell modestly, -4 to 754

• After last week’s loss of 3 horizontal oil rigs, the Permian lost an additional 5 this week

• Breakeven to add rigs fell to $54 WTI compared to $55.50 WTI on the screen as of the writing of this report. This is the first time breakeven has been below the posted oil price in months.

Click on graph for larger image.

Click on graph for larger image.CR note: This graph shows the US horizontal rig count by basin.

Graph and comments Courtesy of Steven Kopits of Princeton Energy Advisors LLC.

Hotels: Occupancy Rate Increased Slightly Year-over-year

by Calculated Risk on 2/17/2019 11:24:00 AM

From HotelNewsNow.com: STR: US hotel results for week ending 9 February

The U.S. hotel industry reported positive year-over-year results in the three key performance metrics during the week of 3-9 February 2019, according to data from STR.The following graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

In comparison with the week of 4-10 February 2018, the industry recorded the following:

• Occupancy: +0.2% to 59.9%

• Average daily rate (ADR): +1.5% to US$126.68

• Revenue per available room (RevPAR): +1.7% to US$75.84

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2019, dash light blue is 2018, blue is the median, and black is for 2009 (the worst year probably since the Great Depression for hotels).

A decent start for 2019.

Seasonally, the occupancy rate will increase over the next couple of months.

Data Source: STR, Courtesy of HotelNewsNow.com

Saturday, February 16, 2019

Schedule for Week of February 17, 2019

by Calculated Risk on 2/16/2019 08:11:00 AM

The key report this week is January existing home sales.

For manufacturing, the February Philly Fed manufacturing survey will be released.

All US markets will be closed in observance of Washington's Birthday Holiday.

10:00 AM: The February NAHB homebuilder survey. The consensus is for a reading of 59, up from 58. Any number above 50 indicates that more builders view sales conditions as good than poor.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

During the day: The AIA's Architecture Billings Index for January (a leading indicator for commercial real estate).

2:00 PM: FOMC Minutes, Meeting of January 29-30, 2019

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 230 thousand initial claims, down from 239 thousand the previous week.

8:30 AM: Durable Goods Orders for January from the Census Bureau. The consensus is for a 1.7% increase in durable goods orders.

8:30 AM: the Philly Fed manufacturing survey for February. The consensus is for a reading of 14.5, down from 17.0.

10:00 AM: Existing Home Sales for January from the National Association of Realtors (NAR). The consensus is for 5.00 million SAAR, up from 4.99 million.

10:00 AM: Existing Home Sales for January from the National Association of Realtors (NAR). The consensus is for 5.00 million SAAR, up from 4.99 million.The graph shows existing home sales from 1994 through the report last month.

No major economic releases scheduled.

Friday, February 15, 2019

Q4 GDP Forecasts: High-1s, Low-2s, 2018 Annual GDP around 2.8%

by Calculated Risk on 2/15/2019 11:58:00 AM

The BEA has announced that the Q4 advanced GDP report will be combined with the 2nd estimate of GDP, and will be released on Feb 28th.

From Merrill Lynch:

Weak retail sales data and inventory build caused a 0.8pp decline in our 4Q GDP tracking estimate to 1.5% from 2.3% [Feb 14 estimate]From Goldman Sachs:

emphasis added

The retail sales report indicated a considerably weaker pace of fourth quarter consumption growth than we had previously assumed. Reflecting this and lower-than-expected November business inventories, we lowered our Q4 GDP tracking estimate by five tenths to +2.0% (qoq ar). [Feb 14 estimate]From the NY Fed Nowcasting Report

The New York Fed Staff Nowcast stands at 2.2% for 2018:Q4 and 1.1% for 2019:Q1. [Feb 15 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2018 is 1.5 percent on February 14, down from 2.7 percent on February 6. [Feb 14 estimate]CR Note: These estimates suggest GDP in the high 1s for Q4.

Using the middle of these four forecasts (about 1.8% real GDP growth in Q4), that would put 2018 annual GDP growth at around 2.8%. This would be the best year since 2015, but lower than many forecasts.

MBA: "Mortgage Delinquencies Dropped to 18-Year Low in the Fourth Quarter of 2018"

by Calculated Risk on 2/15/2019 10:44:00 AM

From the MBA: Mortgage Delinquencies Dropped to 18-Year Low in the Fourth Quarter of 2018

The delinquency rate for mortgage loans on one-to-four-unit residential properties decreased to a seasonally adjusted rate of 4.06 percent of all loans outstanding at the end of the fourth quarter of 2018, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey.

The delinquency rate was down 41 basis points from the third quarter of 2018 and 111 basis points from one year ago. The percentage of loans on which foreclosure actions were started in the fourth quarter rose by two basis points to 0.25 percent.

“The overall national mortgage delinquency rate in the fourth quarter was at its lowest level since the first quarter of 2000,” said Marina Walsh, MBA’s Vice President of Industry Analysis. “What’s even more noteworthy, the delinquency rate dropped from the previous quarter and on a year-over-year basis across all loan types and stages of delinquency."

Added Walsh, “With the unemployment rate near a 50-year low, wage growth trending higher and household debt levels relative to disposable incomes at a 35-year low, homeowners are in great shape, and mortgage performance is quite strong.”

...

In relation to the third quarter of 2018, mortgage delinquencies decreased across all stages of delinquency. The 30-day delinquency rate decreased 22 basis points to 2.29 percent, the 60-day delinquency rate decreased three basis points to 0.74 percent, and the 90-day delinquency bucket decreased 15 basis points to 1.03 percent.

...

The delinquency rate includes loans that are at least one payment past due, but does not include loans in the process of foreclosure. The percentage of loans in the foreclosure process at the end of the fourth quarter was 0.95 percent, down four basis points from the third quarter of 2018 and 24 basis points lower than one year ago. This was the lowest foreclosure inventory rate since the first quarter of 1996.

...

The serious delinquency rate, the percentage of loans that are 90 days or more past due or in the process of foreclosure, was 2.06 percent – a decrease of seven basis points from last quarter – and a decrease of 85 basis points from last year.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of loans delinquent by days past due.

The percent of loans delinquent decreased in Q4 and is at the lowest rate since Q1 2000.

The percent of loans in the foreclosure process continues to decline, and is now at the lowest level since 1996.

Industrial Production Decreased 0.6% in January

by Calculated Risk on 2/15/2019 09:20:00 AM

From the Fed: Industrial Production and Capacity Utilization

Industrial production decreased 0.6 percent in January after rising 0.1 percent in December. In January, manufacturing production fell 0.9 percent, primarily as a result of a large drop in motor vehicle assemblies; factory output excluding motor vehicles and parts decreased 0.2 percent. The indexes for mining and utilities moved up 0.1 percent and 0.4 percent, respectively. At 109.4 percent of its 2012 average, total industrial production was 3.8 percent higher in January than it was a year earlier. Capacity utilization for the industrial sector decreased 0.6 percentage point in January to 78.2 percent, a rate that is 1.6 percentage points below its long-run (1972–2018) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up 11.5 percentage points from the record low set in June 2009 (the series starts in 1967).

Capacity utilization at 78.2% is 1.6% below the average from 1972 to 2017 and below the pre-recession level of 80.8% in December 2007.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production decreased in January to 109.4. This is 25.6% above the recession low, and 3.8% above the pre-recession peak.

The decrease in industrial production and capacity utilization were well below consensus.

NY Fed: Manufacturing "Business activity grew modestly in New York State"

by Calculated Risk on 2/15/2019 08:36:00 AM

From the NY Fed: Empire State Manufacturing Survey

Business activity grew modestly in New York State, according to firms responding to the February 2019 Empire State Manufacturing Survey. The headline general business conditions index moved up five points to 8.8. New orders and shipments also increased modestly. Delivery times were slightly longer, and inventories held steady. Labor market indicators pointed to a slight increase in employment and hours worked. The prices paid index moved lower for a third consecutive month, indicating an ongoing deceleration in input price increases, while the prices received index climbed ten points to reach its highest level in several months, indicating a pickup in selling price increases. After slumping last month, indexes assessing the six-month outlook improved noticeably, suggesting firms were fairly optimistic about future conditions.This was close to the consensus forecast.

The index for number of employees fell for a second consecutive month, declining three points to a still-positive 4.1, pointing to a slight increase in employment levels, and the average workweek index moved down to 2.5. emphasis added

Thursday, February 14, 2019

Friday: Industrial Production, NY Fed Mfg Survey

by Calculated Risk on 2/14/2019 07:36:00 PM

Friday:

• At 8:30 AM: The New York Fed Empire State manufacturing survey for February. The consensus is for a reading of 7.0, up from 3.9.

• At 9:15 AM: The Fed will release Industrial Production and Capacity Utilization for January. The consensus is for a 0.2% increase in Industrial Production, and for Capacity Utilization to increase to 78.8%.

• At 10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for February). The consensus is for a reading of 92.5.