RSS Feed

RSS Feed by Calculated Risk on 8/30/2016 09:04:00 PM

Tuesday, August 30, 2016

Wednesday: ADP employment, Pending Home Sales, Chicago PMI

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:15 AM, The ADP Employment Report for August. This report is for private payrolls only (no government). The consensus is for 175,000 payroll jobs added in August, down from 179,000 added in July.

• At 9:45 AM, Chicago Purchasing Managers Index for August. The consensus is for a reading of 55.2, down from 55.8 in July.

• At 10:00 AM, Pending Home Sales Index for July. The consensus is for a 0.6% increase in the index.

Fannie Mae: Mortgage Serious Delinquency rate declined in July, Lowest since May 2008

by Calculated Risk on 8/30/2016 05:09:00 PM

Fannie Mae reported today that the Single-Family Serious Delinquency rate declined in July to 1.30%, down from 1.32% in June. The serious delinquency rate is down from 1.63% in July 2015.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

This is the lowest rate since May 2008.

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59%.

Click on graph for larger image

Click on graph for larger image

Although the rate is generally declining, the "normal" serious delinquency rate is under 1%.

The Fannie Mae serious delinquency rate has fallen 0.33 percentage points over the last year, and at that rate of improvement, the serious delinquency rate will not be below 1% until next summer.

Note: Freddie Mac reported last week.

FDIC: Fewer Problem banks, Residential REO Declined in Q2

by Calculated Risk on 8/30/2016 02:11:00 PM

The FDIC released the Quarterly Banking Profile for Q2 today:

Commercial banks and savings institutions insured by the Federal Deposit Insurance Corporation (FDIC) reported aggregate net income of $43.6 billion in the second quarter of 2016, up $584 million (1.4 percent) from a year earlier. The increase in earnings was mainly attributable to a $5.2 billion (4.8 percent) increase in net interest income and a $981 million decline in expenses for litigation reserves at a few large banks. Banks increased their loan-loss provisions by $3.6 billion (44.2 percent) compared to a year ago, partly in response to rising levels of troubled loans to commercial and industrial borrowers, particularly in the energy sector.

...

“Income and revenue both increased from a year ago, loan growth remained strong, the number of unprofitable banks was at an 18-year low, and there were fewer banks on the problem list. Community banks reported strong net income, revenue, and loan growth,” Chairman Gruenberg said.

“However, challenges continue,” he said. “Revenue growth remains sluggish as a prolonged period of low interest rates has put downward pressure on net interest margins. This has led some institutions to reach for yield, increasing their exposure to interest-rate risk.

“More recently, persistent stress in the energy sector has resulted in asset quality deterioration at banks that lend to oil and gas producers. We likely have not yet seen the full impact of low energy prices on the banking industry, particularly for consumer and commercial and industrial loans in energy-producing regions of the country.

“We will continue to closely monitor the environment in which banks operate, and we will remain vigilant as we conduct our supervision of the industry.”

...

“Problem List” Continues to Shrink: The number of banks on the FDIC’s Problem List fell from 165 to 147 during the second quarter. This is the smallest number of problem banks in more than seven years and is down significantly from the peak of 888 in the first quarter of 2011. Total assets of problem banks fell from $30.9 billion to $29.0 billion during the second quarter. Two banks failed during the quarter.

Deposit Insurance Fund’s Reserve Ratio Surpasses 1.15 Percent Benchmark: The DIF increased $2.8 billion during the second quarter, from $75.1 billion at the end of March to $77.9 billion at the end of June, largely driven by $2.3 billion in assessment income. The DIF reserve ratio rose from 1.13 percent to 1.17 percent during the quarter. Under previously approved FDIC regulations, once the reserve ratio exceeds 1.15 percent, lower regular assessment rates will go into effect. As a result of lower rates, the FDIC estimates that regular assessments paid by banks to the FDIC will decline by about one-third.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The FDIC reported the number of problem banks declined (Note: graph shows problem banks for Q1 and Q2 2016, and year end prior to 2016):

The number of FDIC-insured commercial banks and savings institutions reporting quarterly financial results declined to 6,058 from 6,122 in the second quarter. During the quarter, mergers absorbed 57 insured institutions, two banks failed, and no new charters were added. The number of banks on the FDIC’s “Problem List” declined from 165 to 147, and total assets of problem banks fell from $30.9 billion to $29 billion. This is the smallest number of problem banks in eight years

The dollar value of 1-4 family residential Real Estate Owned (REOs, foreclosure houses) declined from $4.38 billion in Q1 2016 to $4.12 billion in Q2. This is the lowest level of REOs since Q1 2007.

The dollar value of 1-4 family residential Real Estate Owned (REOs, foreclosure houses) declined from $4.38 billion in Q1 2016 to $4.12 billion in Q2. This is the lowest level of REOs since Q1 2007.This graph shows the nominal dollar value of Residential REO for FDIC insured institutions. Note: The FDIC reports the dollar value and not the total number of REOs.

Real Prices and Price-to-Rent Ratio in June

by Calculated Risk on 8/30/2016 11:40:00 AM

Here is the earlier post on Case-Shiller: Case-Shiller: National House Price Index increased 5.1% year-over-year in June

The year-over-year increase in prices is mostly moving sideways now around 5%. In June, the index was up 5.1% YoY.

In the earlier post, I graphed nominal house prices, but it is also important to look at prices in real terms (inflation adjusted). Case-Shiller, CoreLogic and others report nominal house prices. As an example, if a house price was $200,000 in January 2000, the price would be close to $275,000 today adjusted for inflation (37%). That is why the second graph below is important - this shows "real" prices (adjusted for inflation).

It has been almost ten years since the bubble peak. In the Case-Shiller release this morning, the National Index was reported as being 2.6% below the bubble peak. However, in real terms, the National index is still about 17.0% below the bubble peak.

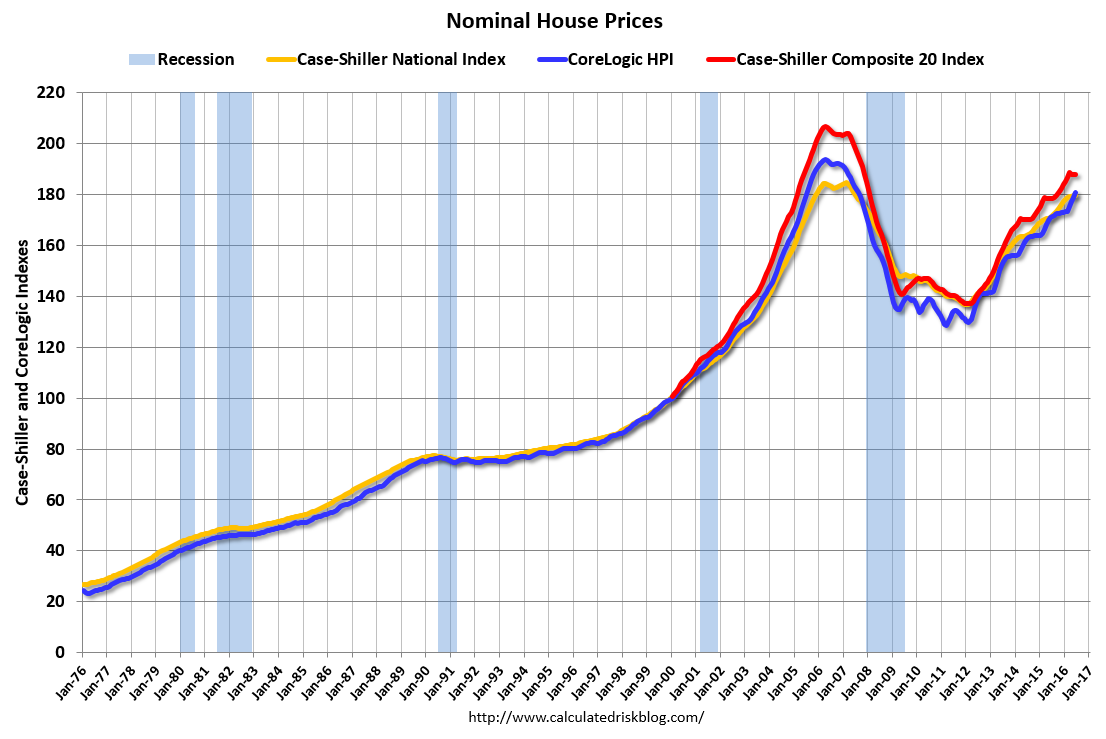

Nominal House Prices

The first graph shows the monthly Case-Shiller National Index SA, the monthly Case-Shiller Composite 20 SA, and the CoreLogic House Price Indexes (through June) in nominal terms as reported.

The first graph shows the monthly Case-Shiller National Index SA, the monthly Case-Shiller Composite 20 SA, and the CoreLogic House Price Indexes (through June) in nominal terms as reported.

In nominal terms, the Case-Shiller National index (SA) is back to November 2005 levels, and the Case-Shiller Composite 20 Index (SA) is back to June 2005 levels, and the CoreLogic index (NSA) is back to July 2005.

Real House Prices

The second graph shows the same three indexes in real terms (adjusted for inflation using CPI less Shelter). Note: some people use other inflation measures to adjust for real prices.

The second graph shows the same three indexes in real terms (adjusted for inflation using CPI less Shelter). Note: some people use other inflation measures to adjust for real prices.

CPI less Shelter has declined over the last two years pushing up real house prices.

In real terms, the National index is back to January 2004 levels, the Composite 20 index is back to October 2003, and the CoreLogic index back to November 2003.

In real terms, house prices are back to late 2003 levels.

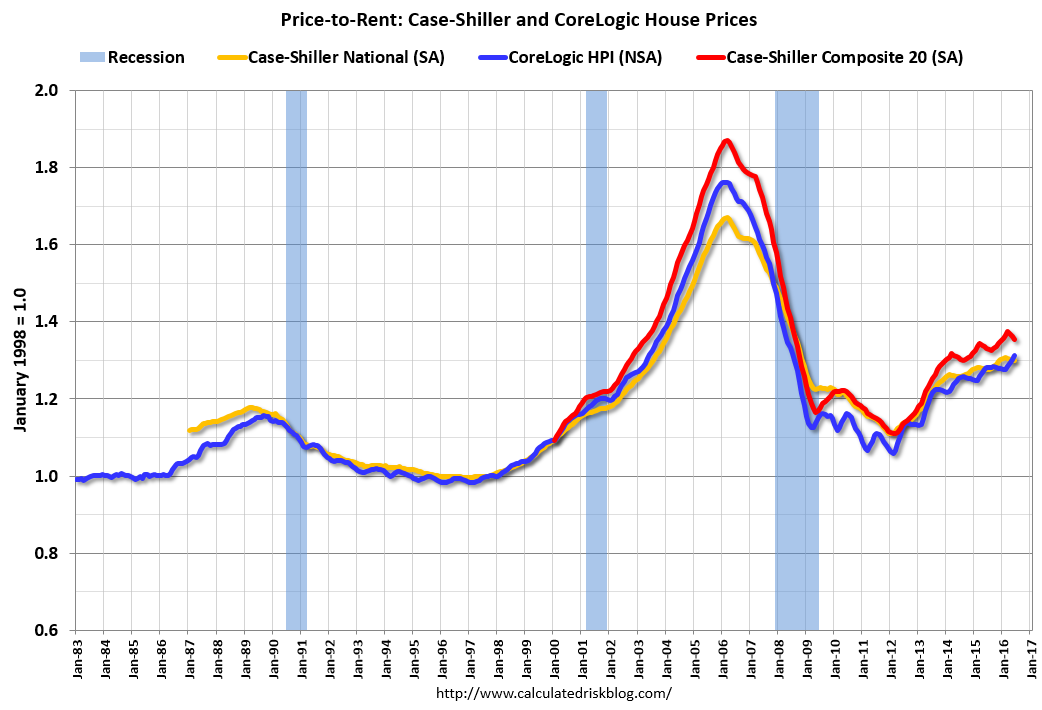

Price-to-Rent

In October 2004, Fed economist John Krainer and researcher Chishen Wei wrote a Fed letter on price to rent ratios: House Prices and Fundamental Value. Kainer and Wei presented a price-to-rent ratio using the OFHEO house price index and the Owners' Equivalent Rent (OER) from the BLS.

Here is a similar graph using the Case-Shiller National, Composite 20 and CoreLogic House Price Indexes.

Here is a similar graph using the Case-Shiller National, Composite 20 and CoreLogic House Price Indexes.

This graph shows the price to rent ratio (January 1998 = 1.0).

On a price-to-rent basis, the Case-Shiller National index is back to July 2003 levels, the Composite 20 index is back to April 2003 levels, and the CoreLogic index is back to June 2003.

In real terms, and as a price-to-rent ratio, prices are back to late 2003 - and the price-to-rent ratio maybe moving a little more sideways now.

Case-Shiller: National House Price Index increased 5.1% year-over-year in June

by Calculated Risk on 8/30/2016 09:13:00 AM

S&P/Case-Shiller released the monthly Home Price Indices for June ("June" is a 3 month average of April, May and June prices).

This release includes prices for 20 individual cities, two composite indices (for 10 cities and 20 cities) and the monthly National index.

Note: Case-Shiller reports Not Seasonally Adjusted (NSA), I use the SA data for the graphs.

From S&P: Home Price Gains in June Concentrated in South and West According to the S&P CoreLogic Case-Shiller Indices

The S&P CoreLogic Case-Shiller U.S. National Home Price NSA Index, covering all nine U.S. census divisions, reported a 5.1% annual gain in June, unchanged from last month. The 10-City Composite posted a 4.3% annual increase, down from 4.4% the previous month.The 20-City Composite reported a year-over-year gain of 5.1%, down from 5.3% in May.

...

Before seasonal adjustment, the National Index posted a month-over-month gain of 1.0% while both the 10-City Composite and the 20-City Composite posted a 0.8% increase in June. After seasonal adjustment, the National Index recorded a 0.2% month-over-month increase, and both the 10-City Composite and 20-City Composite posted 0.1% month-over-month decreases. After seasonal adjustment, nine cities saw prices rise, two cities were unchanged, and nine cities experienced negative monthly prices changes.

emphasis added

Click on graph for larger image.

Click on graph for larger image. The first graph shows the nominal seasonally adjusted Composite 10, Composite 20 and National indices (the Composite 20 was started in January 2000).

The Composite 10 index is off 11.1% from the peak, and down 0.1% in June (SA).

The Composite 20 index is off 9.1% from the peak, and down 0.1% (SA) in June.

The National index is off 2.6% from the peak, and up 0.2% (SA) in June. The National index is up 31.6% from the post-bubble low set in December 2011 (SA).

The second graph shows the Year over year change in all three indices.

The second graph shows the Year over year change in all three indices.The Composite 10 SA is up 4.3% compared to June 2015.

The Composite 20 SA is up 5.1% year-over-year.

The National index SA is up 5.1% year-over-year.

Note: According to the data, prices increased in 10 of 20 cities month-over-month seasonally adjusted.

I'll have more later.

Tuesday: Case-Shiller House Prices

by Calculated Risk on 8/30/2016 01:00:00 AM

Tuesday:

• At 9:00 AM ET, b>S&P/Case-Shiller House Price Index for June. Although this is the June report, it is really a 3 month average of April, May and June prices. The consensus is for a 5.2% year-over-year increase in the Comp 20 index for June. The Zillow forecast is for the National Index to increase 5.1% year-over-year in June.

From Matthew Graham at Mortgage News Daily: Mortgage Rates Battle Back From Recent Highs

Mortgage Rates were briefly at their highest levels in several weeks on Friday afternoon. This followed comments from the Fed's Jackson Hole symposium. Markets interpreted those comments as the Fed being more likely to hike rates in 2016--possibly even twice! While mortgage rates are based on MBS (mortgage-backed-securities), as opposed to the Fed Funds Rate (the thing the Fed is talking about hiking), if investors think the Fed is more likely to hike, MBS tend to lose some ground.

emphasis added

Monday, August 29, 2016

Lawler: Table of Distressed Sales and All Cash Sales for Selected Cities in July

by Calculated Risk on 8/29/2016 03:11:00 PM

Economist Tom Lawler sent me the table below of short sales, foreclosures and all cash sales for selected cities in July.

On distressed: Total "distressed" share is down year-over-year in all of these markets (except Springfield).

Short sales and foreclosures are down in all of these areas.

The All Cash Share (last two columns) is mostly declining year-over-year. As investors continue to pull back, the share of all cash buyers continues to decline.

| Short Sales Share | Foreclosure Sales Share | Total "Distressed" Share | All Cash Share | |||||

|---|---|---|---|---|---|---|---|---|

| July- 2016 | July- 2015 | July- 2016 | July- 2015 | July- 2016 | July- 2015 | July- 2016 | July- 2015 | |

| Las Vegas | 5.7% | 7.1% | 5.9% | 7.7% | 11.6% | 14.8% | 25.8% | 27.1% |

| Reno** | 3.0% | 3.0% | 1.0% | 2.0% | 4.0% | 5.0% | ||

| Phoenix | 1.6% | 2.8% | 2.2% | 3.4% | 3.8% | 6.3% | 19.7% | 21.9% |

| Sacramento | 2.6% | 4.7% | 2.1% | 4.6% | 4.7% | 9.3% | 14.4% | 18.1% |

| Minneapolis | 1.0% | 2.0% | 3.6% | 5.5% | 4.6% | 7.5% | 11.3% | 11.7% |

| Mid-Atlantic | 2.7% | 3.4% | 7.6% | 9.4% | 10.4% | 12.8% | 15.0% | 15.8% |

| So. California* | 4.9% | 7.1% | 19.6% | 21.6% | ||||

| Bay Area CA* | 3.2% | 4.7% | 18.6% | 20.1% | ||||

| Florida SF | 2.4% | 3.4% | 8.0% | 16.3% | 10.4% | 19.7% | 26.6% | 32.6% |

| Florida C/TH | 1.6% | 2.4% | 7.0% | 15.2% | 8.6% | 17.6% | 53.7% | 59.1% |

| Miami MSA SF | 3.8% | 5.1% | 9.5% | 16.5% | 13.4% | 21.6% | 27.9% | 31.8% |

| Miami MSA C/TH | 1.7% | 3.5% | 9.5% | 18.8% | 11.2% | 22.2% | 56.7% | 61.9% |

| Tampa MSA SF | 2.8% | 3.6% | 8.3% | 16.4% | 11.1% | 20.0% | 25.7% | 33.9% |

| Tampa MSA C/TH | 1.6% | 2.0% | 6.7% | 14.8% | 8.3% | 16.8% | 50.2% | 56.1% |

| Chicago (city) | 10.5% | 13.5% | ||||||

| Northeast Florida | 12.8% | 26.3% | ||||||

| Spokane | 5.7% | 9.1% | ||||||

| Tucson | 21.6% | 23.7% | ||||||

| Orlando | 28.4% | 34.5% | ||||||

| Toledo | 24.3% | 27.0% | ||||||

| S.C. Wisconsin | 14.4% | 15.2% | ||||||

| Knoxville | 20.6% | 21.8% | ||||||

| Peoria | 22.7% | 15.6% | ||||||

| Georgia*** | 18.5% | 20.3% | ||||||

| Omaha | 13.0% | 13.2% | ||||||

| Pensacola | 28.0% | 28.5% | ||||||

| Rhode Island | 7.8% | 8.8% | ||||||

| Richmond VA | 6.0% | 8.4% | 15.9% | 18.1% | ||||

| Memphis | 8.1% | 12.8% | ||||||

| Springfield IL** | 6.3% | 4.7% | ||||||

| *share of existing home sales, based on property records **Single Family Only ***GAMLS | ||||||||

Black Knight: House Price Index up 0.8% in June, Up 5.3% year-over-year

by Calculated Risk on 8/29/2016 12:53:00 PM

Note: I follow several house price indexes (Case-Shiller, CoreLogic, Black Knight, Zillow, FHFA, FNC and more). Note: Black Knight uses the current month closings only (not a three month average like Case-Shiller or a weighted average like CoreLogic), excludes short sales and REOs, and is not seasonally adjusted.

From Black Knight: Black Knight Home Price Index Report: June 2016 Transaction

• U.S. Home Prices Up 0.8 Percent for the Month; Up 5.3 Percent Year-Over-YearThe year-over-year increase in this index has been about the same for the last year.

• At $265K, the U.S. HPI is up 32.6 percent from the market's bottom and is within just 1.1 percent of a new national peak

• Home prices in six of the nation's 20 largest states and 14 of the 40 largest metros hit new peaks in June

Note that house prices are close to the bubble peak in nominal terms, but not adjusted for inflation.

Dallas Fed: Regional Manufacturing Activity Increases in August

by Calculated Risk on 8/29/2016 10:41:00 AM

From the Dallas Fed: Texas Manufacturing Activity Increases

Texas factory activity increased in August, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, came in at 4.5 after a near-zero reading in July, suggesting output picked up this month.The impact of lower oil prices is still impacting manufacturing.

Other measures of current manufacturing activity also reflected expansion. Demand bounced back, with the new orders index rising from -8.0 to 5.3 in August and the growth rate of orders index pushing up to 2.1, its first positive reading in nearly two years. The capacity utilization index remained only barely positive at 0.9, while the shipments index rose nearly 10 points to 9.9, with nearly a third of manufacturers reporting higher volumes of shipments this month.

Perceptions of broader business conditions remained fairly pessimistic. The general business activity index was negative for a 20th month in a row and moved down from -1.3 to -6.2. The company outlook index was largely unchanged at -2.8.

Labor market measures indicated slight employment declines and shorter workweek length. The employment index came in at -5.0, down from -2.6 last month. ...

emphasis added

This was the last of the regional Fed surveys for August.

Here is a graph comparing the regional Fed surveys and the ISM manufacturing index:

Click on graph for larger image.

Click on graph for larger image.The New York and Philly Fed surveys are averaged together (yellow, through August), and five Fed surveys are averaged (blue, through August) including New York, Philly, Richmond, Dallas and Kansas City. The Institute for Supply Management (ISM) PMI (red) is through July (right axis).

It seems likely the ISM manufacturing index will be lower in August than in July.

Personal Income increased 0.4% in July, Spending increased 0.3%

by Calculated Risk on 8/29/2016 08:41:00 AM

The BEA released the Personal Income and Outlays report for July:

Personal income increased $71.6 billion (0.4 percent) in July according to estimates released today by the Bureau of Economic Analysis ... personal consumption expenditures (PCE) increased $42.0 billion (0.3 percent).The July PCE price index increased 0.8 percent year-over-year and the July PCE price index, excluding food and energy, increased 1.6 percent year-over-year.

...

Real PCE increased 0.3 percent. The PCE price index was unchanged from June. Excluding food and energy, the PCE price index increased 0.1 percent in July.

The following graph shows real Personal Consumption Expenditures (PCE) through July 2016 (2009 dollars). Note that the y-axis doesn't start at zero to better show the change.

Click on graph for larger image.

Click on graph for larger image.The dashed red lines are the quarterly levels for real PCE.

Both the increase in personal income and the increase in PCE was at consensus expectations.

A solid start for Q3.