RSS Feed

RSS Feed by Calculated Risk on 12/04/2015 04:26:00 PM

Friday, December 04, 2015

Public and Private Sector Payroll Jobs: Carter, Reagan, Bush, Clinton, Bush, Obama

By request, here is another update of an earlier post through the November employment report.

NOTE: Several readers have asked if I could add a lag to these graphs (obviously a new President has zero impact on employment for the month they are elected). But that would open a debate on the proper length of the lag, so I'll just stick to the beginning of each term.

Note: We frequently use Presidential terms as time markers - we could use Speaker of the House, or any other marker.

Important: There are many differences between these periods. Overall employment was smaller in the '80s, however the participation rate was increasing in the '80s (younger population and women joining the labor force), and the participation rate is generally declining now. But these graphs give an overview of employment changes.

First, here is a table for private sector jobs. The top two private sector terms were both under President Clinton. Reagan's 2nd term saw about the same job growth as during Carter's term. Note: There was a severe recession at the beginning of Reagan's first term (when Volcker raised rates to slow inflation) and a recession near the end of Carter's term (gas prices increased sharply and there was an oil embargo).

| Term | Private Sector Jobs Added (000s) |

|---|---|

| Carter | 9,041 |

| Reagan 1 | 5,360 |

| Reagan 2 | 9,357 |

| GHW Bush | 1,510 |

| Clinton 1 | 10,884 |

| Clinton 2 | 10,073 |

| GW Bush 1 | -844 |

| GW Bush 2 | 381 |

| Obama 1 | 2,018 |

| Obama 2 | 7,4991 |

| 134 months into 2nd term: 10,587 pace. | |

The first graph shows the change in private sector payroll jobs from when each president took office until the end of their term(s). President George H.W. Bush only served one term, and President Obama is in the third year of his second term.

Mr. G.W. Bush (red) took office following the bursting of the stock market bubble, and left during the bursting of the housing bubble. Mr. Obama (blue) took office during the financial crisis and great recession. There was also a significant recession in the early '80s right after Mr. Reagan (yellow) took office.

There was a recession towards the end of President G.H.W. Bush (purple) term, and Mr Clinton (light blue) served for eight years without a recession.

Click on graph for larger image.

Click on graph for larger image.The first graph is for private employment only.

The employment recovery during Mr. G.W. Bush's (red) first term was sluggish, and private employment was down 844,000 jobs at the end of his first term. At the end of Mr. Bush's second term, private employment was collapsing, and there were net 463,000 private sector jobs lost during Mr. Bush's two terms.

Private sector employment increased slightly under President G.H.W. Bush (purple), with 1,510,000 private sector jobs added.

Private sector employment increased by 20,955,000 under President Clinton (light blue), by 14,717,000 under President Reagan (yellow), and 9,041,000 under President Carter (dashed green).

There were only 2,018,000 more private sector jobs at the end of Mr. Obama's first term. Thirty four months into Mr. Obama's second term, there are now 9,517,000 more private sector jobs than when he initially took office.

A big difference between the presidencies has been public sector employment. Note the bumps in public sector employment due to the decennial Census in 1980, 1990, 2000, and 2010.

A big difference between the presidencies has been public sector employment. Note the bumps in public sector employment due to the decennial Census in 1980, 1990, 2000, and 2010. The public sector grew during Mr. Carter's term (up 1,304,000), during Mr. Reagan's terms (up 1,414,000), during Mr. G.H.W. Bush's term (up 1,127,000), during Mr. Clinton's terms (up 1,934,000), and during Mr. G.W. Bush's terms (up 1,744,000 jobs).

However the public sector has declined significantly since Mr. Obama took office (down 594,000 jobs). These job losses have mostly been at the state and local level, but more recently at the Federal level. This has been a significant drag on overall employment.

And a table for public sector jobs. Public sector jobs declined the most during Obama's first term, and increased the most during Reagan's 2nd term.

| Term | Public Sector Jobs Added (000s) |

|---|---|

| Carter | 1,304 |

| Reagan 1 | -24 |

| Reagan 2 | 1,438 |

| GHW Bush | 1,127 |

| Clinton 1 | 692 |

| Clinton 2 | 1,242 |

| GW Bush 1 | 900 |

| GW Bush 2 | 844 |

| Obama 1 | -702 |

| Obama 2 | 1081 |

| 134 months into 2nd term, 152 pace | |

Looking forward, I expect the economy to continue to expand through 2016 (at least), so I don't expect a sharp decline in private employment as happened at the end of Mr. Bush's 2nd term (In 2005 and 2006 I was warning of a coming recession due to the bursting of the housing bubble).

For the public sector, the cutbacks are clearly over at the state and local levels, and it appears cutbacks at the Federal level are over. Right now I'm expecting some increase in public employment during Obama's 2nd term, but nothing like what happened during Reagan's second term.

Below is a table of the top three presidential terms for private job creation (they also happen to be the three best terms for total non-farm job creation).

Clinton's two terms were the best for both private and total non-farm job creation, followed by Reagan's 2nd term.

Currently Obama's 2nd term is on pace to be the 2nd best ever for private job creation. However, with very few public sector jobs added, Obama's 2nd term is only on pace to be the fourth best for total job creation.

Note: Only 108 thousand public sector jobs have been added during the first thirty four months of Obama's 2nd term (following a record loss of 702 thousand public sector jobs during Obama's 1st term). This is less than 8% of the public sector jobs added during Reagan's 2nd term!

| Top Employment Gains per Presidential Terms (000s) | ||||

|---|---|---|---|---|

| Rank | Term | Private | Public | Total Non-Farm |

| 1 | Clinton 1 | 10,884 | 692 | 11,576 |

| 2 | Clinton 2 | 10,073 | 1,242 | 11,315 |

| 3 | Reagan 2 | 9,357 | 1,438 | 10,795 |

| Obama 21 | 7,499 | 108 | 7,607 | |

| Pace2 | 10,587 | 152 | 10,739 | |

| 134 Months into 2nd Term 2Current Pace for Obama's 2nd Term | ||||

The last table shows the jobs needed per month for Obama's 2nd term to be in the top three presidential terms.

| Average Jobs needed per month (000s) for remainder of Obama's 2nd Term | ||||

|---|---|---|---|---|

| to Rank | Private | Total | ||

| #1 | 242 | 284 | ||

| #2 | 184 | 265 | ||

| #3 | 133 | 228 | ||

Comments: Solid November Employment Report

by Calculated Risk on 12/04/2015 12:23:00 PM

This was a solid employment report with 211,000 jobs added, and employment gains for September and October were revised up.

Also wages increased, from the BLS: "In November, average hourly earnings for all employees on private nonfarm payrolls rose by 4 cents to $25.25, following a 9-cent gain in October. Over the year, average hourly earnings have risen by 2.3 percent."

Earlier: November Employment Report: 211,000 Jobs, 5.0% Unemployment Rate

A few more numbers: Total employment is now 4.5 million above the previous peak. Total employment is up 13.3 million from the employment recession low.

Private payroll employment increased 197,000 in November, and private employment is now 4.9 million above the previous peak. Private employment is up 13.7 million from the recession low.

In November, the year-over-year change was 2.64 million jobs.

Seasonal Retail Hiring

Click on graph for larger image.

Click on graph for larger image.

Typically retail companies start hiring for the holiday season in October, and really increase hiring in November. Here is a graph that shows the historical net retail jobs added for October, November and December by year.

This graph really shows the collapse in retail hiring in 2008. Since then seasonal hiring has increased back close to more normal levels. Note: I expect the long term trend will be down with more and more internet holiday shopping.

Retailers hired 604.5 thousand workers (NSA) net in October and November. Note: this is NSA (Not Seasonally Adjusted).

This is the same pace as last year, and suggests retailers are reasonably optimistic about sales.

Employment-Population Ratio, 25 to 54 years old

Since the overall participation rate declined recently due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate declined recently due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

In the earlier period the participation rate for this group was trending up as women joined the labor force. Since the early '90s, the participation rate moved more sideways, with a downward drift starting around '00 - and with ups and downs related to the business cycle.

The 25 to 54 participation rate increased in October to 80.8%, and the 25 to 54 employment population ratio increased to 77.4%. The participation rate for this group might increase a little more (or at least stabilize for a couple of years) - although the participation rate has been trending down for this group since the late '90s.

Average Hourly Earnings

This graph is based on “Average Hourly Earnings” from the Current Employment Statistics (CES) (aka "Establishment") monthly employment report. Note: There are also two quarterly sources for earnings data: 1) “Hourly Compensation,” from the BLS’s Productivity and Costs; and 2) the Employment Cost Index which includes wage/salary and benefit compensation.

This graph is based on “Average Hourly Earnings” from the Current Employment Statistics (CES) (aka "Establishment") monthly employment report. Note: There are also two quarterly sources for earnings data: 1) “Hourly Compensation,” from the BLS’s Productivity and Costs; and 2) the Employment Cost Index which includes wage/salary and benefit compensation.

The graph shows the nominal year-over-year change in "Average Hourly Earnings" for all private employees. Nominal wage growth was at 2.3% YoY in November - and although the series is noisy - it does appear wage growth is trending up.

Note: CPI has been running under 2%, so there has been some real wage growth.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:

The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) increased by 319,000 to 6.1 million in November, following declines in September and October. These individuals, who would have preferred full-time employment, were working part time because their hours had been cut back or because they were unable to find a full-time job. Over the past 12 months, the number of persons employed part time for economic reasons is down by 765,000.The number of persons working part time for economic reasons increased in November to 6.09 million from 5.77 million from in October. This level suggests slack still in the labor market.

These workers are included in the alternate measure of labor underutilization (U-6) that increased to 9.9% in November.

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 2.05 million workers who have been unemployed for more than 26 weeks and still want a job. This was down from 2.14 million in October.

This is generally trending down, but is still high.

State and Local Government

This graph shows total state and government payroll employment since January 2007. (Note: Scale doesn't start at zero to better show the change.)

This graph shows total state and government payroll employment since January 2007. (Note: Scale doesn't start at zero to better show the change.) In November 2015, state and local governments added 8 thousand jobs. State and local government employment is now up 197,000 from the bottom, but still 561,000 below the peak.

State and local employment is now increasing. And Federal government layoffs appear to have ended and, with the recent budget deal, Federal employment will probably increase in 2016. (Federal payrolls increased by 6,000 in November, and Federal employment is up 11,000 year-to-date).

Overall this was a solid employment report for November.

Trade Deficit increased in October to $43.9 Billion

by Calculated Risk on 12/04/2015 10:04:00 AM

The Department of Commerce reported:

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis, through the Department of Commerce, announced today that the goods and services deficit was $43.9 billion in October, up $1.4 billion from $42.5 billion in September, revised. October exports were $184.1 billion, $2.7 billion less than September exports. October imports were $228.0 billion, $1.3 billion less than September imports.The trade deficit was larger than the consensus forecast of $40.6 billion.

The first graph shows the monthly U.S. exports and imports in dollars through October 2015.

Click on graph for larger image.

Click on graph for larger image.Imports and exports decreased in October.

Exports are 11% above the pre-recession peak and down 7% compared to October 2014; imports are 2% below the pre-recession peak, and down 5% compared to October 2014.

The second graph shows the U.S. trade deficit, with and without petroleum.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products (wild swings earlier this year were due to West Coast port slowdown).

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products (wild swings earlier this year were due to West Coast port slowdown).Oil imports averaged $40.12 in October, down from $42.72 in September, and down from $88.47 in October 2014. The petroleum deficit has generally been declining and is the major reason the overall deficit has declined since early 2012.

The trade deficit with China increased to $33.0 billion in October, from $32.5 billion in October 2014. The deficit with China is a substantial portion of the overall deficit.

November Employment Report: 211,000 Jobs, 5.0% Unemployment Rate

by Calculated Risk on 12/04/2015 08:34:00 AM

From the BLS:

Total nonfarm payroll employment increased by 211,000 in November, and the unemployment rate was unchanged at 5.0 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in construction, professional and technical services, and health care. Mining and information lost jobs.

...

The change in total nonfarm payroll employment for September was revised from +137,000 to +145,000, and the change from October was revised from +271,000 to +298,000. With these revisions, employment gains in September and October combined were 35,000 more than previously reported.

...

In November, average hourly earnings for all employees on private nonfarm payrolls rose by 4 cents to $25.25, following a 9-cent gain in October. Over the year, average hourly earnings have risen by 2.3 percent.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the monthly change in payroll jobs, ex-Census (meaning the impact of the decennial Census temporary hires and layoffs is removed - mostly in 2010 - to show the underlying payroll changes).

Total payrolls increased by 211 thousand in November (private payrolls increased 197 thousand).

Payrolls for September and October were revised up by a combined 35 thousand.

This graph shows the year-over-year change in total non-farm employment since 1968.

This graph shows the year-over-year change in total non-farm employment since 1968.In November, the year-over-year change was 2.64 million jobs.

That is a solid year-over-year gain.

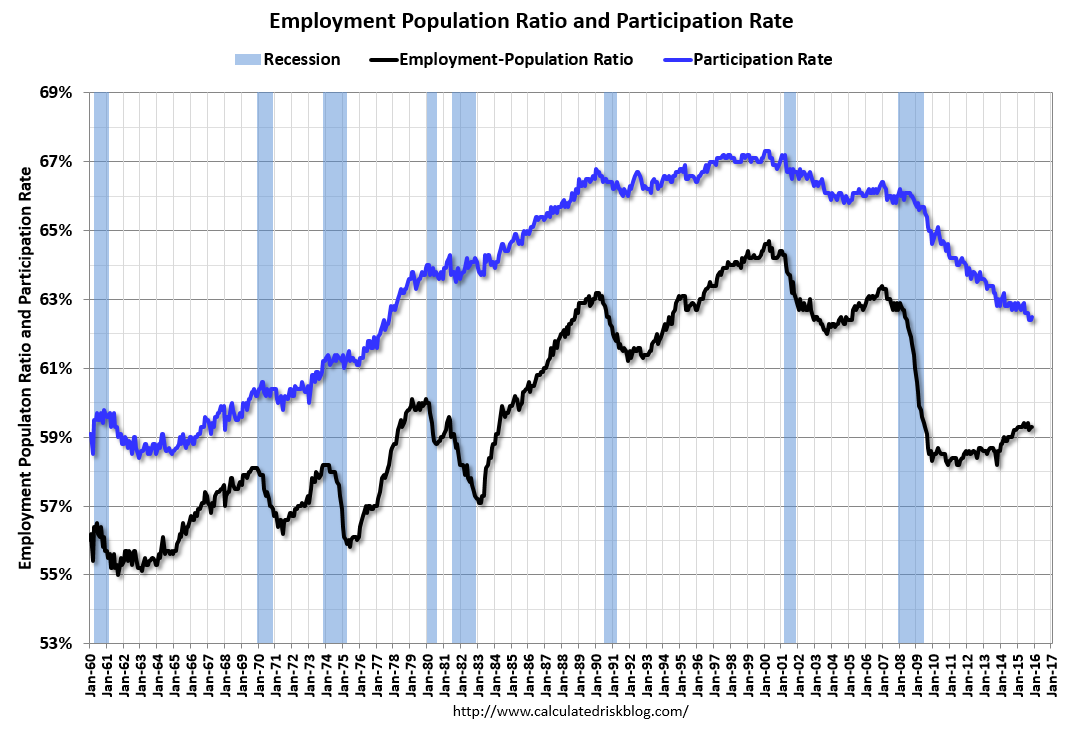

The third graph shows the employment population ratio and the participation rate.

The third graph shows the employment population ratio and the participation rate.The Labor Force Participation Rate increased in November to 62,5%. This is the percentage of the working age population in the labor force. A large portion of the recent decline in the participation rate is due to demographics.

The Employment-Population ratio was unchanged at 59.3% (black line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate was unchanged in November at 5.0%.

This was above expectations of 190,000 jobs, and revisions were up ... a solid report.

I'll have much more later ...

Thursday, December 03, 2015

Friday: Employment Report, Trade Deficit

by Calculated Risk on 12/03/2015 07:58:00 PM

Fed Chair Janet Yellen was asked today about Citi's research suggesting a 65% chance of a recession in 2016. Yellen said she thought the odds of a recession were much lower than 65%.

This is just an historical statistical approach based on elapsed time.

Looking at the economic data, the odds of a recession in 2016 are very low (extremely unlikely). I'm not even on recession watch. No worries.

Friday:

• At 8:30 AM ET, the Employment Report for November. The consensus is for an increase of 190,000 non-farm payroll jobs added in November, down from the 271,000 non-farm payroll jobs added in October. The consensus is for the unemployment rate to be unchanged at 5.0%.

• Also at 8:30 AM, Trade Balance report for October from the Census Bureau. The consensus is for the U.S. trade deficit to be at $40.6 billion in October from $40.8 billion in September.

Freddie Mac: Mortgage Serious Delinquency rate declined in October, Lowest since October 2008

by Calculated Risk on 12/03/2015 06:07:00 PM

Freddie Mac reported that the Single-Family serious delinquency rate declined in October to 1.38%, down from 1.41% in September. Freddie's rate is down from 1.91% in October 2014, and the rate in October was the lowest level since October 2008.

Freddie's serious delinquency rate peaked in February 2010 at 4.20%.

These are mortgage loans that are "three monthly payments or more past due or in foreclosure".

Note: Fannie Mae reported earlier.

Click on graph for larger image

Click on graph for larger image

Although the rate is declining, the "normal" serious delinquency rate is under 1%.

The serious delinquency rate has fallen 0.53 percentage points over the last year, and at that rate of improvement, the serious delinquency rate will not be below 1% until the second half of 2016.

So even though delinquencies and distressed sales are declining, I expect an above normal level of Fannie and Freddie distressed sales through 2016 (mostly in judicial foreclosure states).

Preview: Employment Report for November

by Calculated Risk on 12/03/2015 02:11:00 PM

On Friday at 8:30 AM ET, the BLS will release the employment report for November. The consensus, according to Bloomberg, is for an increase of 190,000 non-farm payroll jobs in November (with a range of estimates between 160,000 to 219,000), and for the unemployment rate to be unchanged at 5.0%.

The BLS reported 271,000 jobs added in October.

Here is a summary of recent data:

• The ADP employment report showed an increase of 217,000 private sector payroll jobs in November. This was above expectations of 183,000 private sector payroll jobs added. The ADP report hasn't been very useful in predicting the BLS report for any one month, but in general, this suggests employment growth above expectations.

• The ISM manufacturing employment index increased in November to 51.3%. A historical correlation between the ISM manufacturing employment index and the BLS employment report for manufacturing, suggests that private sector BLS manufacturing payroll jobs decreased about 10,000 in November. The ADP report indicated a 6,000 increase for manufacturing jobs.

The ISM non-manufacturing employment index decreased in November to 55.0%. A historical correlation between the ISM non-manufacturing employment index and the BLS employment report for non-manufacturing, suggests that private sector BLS non-manufacturing payroll jobs increased about 205,000 in September.

Combined, the ISM indexes suggests employment gains of 195,000. This suggests employment growth close to expectations.

• Initial weekly unemployment claims averaged close to 270,000 in November, up from 260,000 in October. For the BLS reference week (includes the 12th of the month), initial claims were at 272,000, up from 259,000 during the reference week in October.

The increase during the reference suggests a slightly higher level of layoffs in November - but still very low.

• The final November University of Michigan consumer sentiment index increased to 91.3 from the October reading of 90.0. Sentiment is frequently coincident with changes in the labor market, but there are other factors too - like gasoline prices.

• Trim Tabs reported that the U.S. economy added 168,000 jobs in November, down from their estimate of 178,000 jobs in October. Note: "TrimTabs’ employment estimates are based on analysis of daily income tax deposits to the U.S. Treasury from the paychecks of the 142 million U.S. workers subject to withholding."

• Conclusion: Unfortunately none of the indicators above is very good at predicting the initial BLS employment report. Based on these indicators, it appears job gains should be around 200 thousand in November.

Goldman: November Employment Preview

by Calculated Risk on 12/03/2015 12:10:00 PM

A few excerpts from a piece by Goldman Sachs economist David Mericle:

We expect a 200k gain in nonfarm payroll employment in November, in line with consensus expectations. ... Labor market data were mixed in November. ADP employment growth surprised on the upside and the employment components of manufacturing surveys were somewhat stronger on balance, but the Conference Board’s measure of reported job availability declined, jobless claims rose slightly, and the ISM non-manufacturing index’s employment component declined. While a gain of 200k would be a bit softer than the recent average, it would still be well above our estimate of the “breakeven” rate of 85k per month.

We expect the unemployment rate to remain unchanged at 5.0% in November on a rounded basis following a decline last month to 5.036%. However, we see some risk that the unemployment rate will round up to 5.1% given the high unrounded level and the possibility of a slight rebound in participation, which appears a bit low after unexpectedly sharp declines earlier this year. ...

Finally, we expect average hourly earnings for all workers to rise 0.2% in November following a larger-than-expected 0.4% gain in October, implying a two-tenths decline in the year-on-year rate to 2.3%. ... Our wage tracker—which also now includes the Atlanta Fed wage measure—stands at 2.6%. Apart from a technical blip in late 2012, this is the highest reading of the recovery, although it is still somewhat below our 3-3.5% estimate of the full-employment equilibrium rate.

ISM Non-Manufacturing Index Decreased to 55.9% in November

by Calculated Risk on 12/03/2015 10:06:00 AM

The November ISM Non-manufacturing index was at 55.9%, down from 59.1% in October. The employment index decreased in November to 55.0%, down from 59.2% in October. Note: Above 50 indicates expansion, below 50 contraction.

From the Institute for Supply Management: November 2015 Non-Manufacturing ISM Report On Business®

Economic activity in the non-manufacturing sector grew in November for the 70th consecutive month, say the nation’s purchasing and supply executives in the latest Non-Manufacturing ISM® Report On Business®.

The report was issued today by Anthony Nieves, CPSM, C.P.M., CFPM, chair of the Institute for Supply Management® (ISM®) Non-Manufacturing Business Survey Committee. "The NMI® registered 55.9 percent in November, 3.2 percentage points lower than the October reading of 59.1 percent. This represents continued growth in the non-manufacturing sector at a slower rate. The Non-Manufacturing Business Activity Index decreased to 58.2 percent, which is 4.8 percentage points lower than the October reading of 63 percent, reflecting growth for the 76th consecutive month at a slower rate. The New Orders Index registered 57.5 percent, 4.5 percentage points lower than the reading of 62 percent in October. The Employment Index decreased 4.2 percentage points to 55 percent from the October reading of 59.2 percent and indicates growth for the 21st consecutive month. The Prices Index increased 1.2 percentage points from the October reading of 49.1 percent to 50.3 percent, indicating prices increased in November after two consecutive months of decreasing. According to the NMI®, 12 non-manufacturing industries reported growth in November. After a strong month of growth in October, the non-manufacturing sector’s rate of growth slowed in November. Most respondents are still positive about business conditions."

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

This was below the consensus forecast of 58.2 and suggests slower expansion in November than in October. Still a solid report.

Weekly Initial Unemployment Claims at 269,000

by Calculated Risk on 12/03/2015 08:34:00 AM

The DOL reported:

In the week ending November 28, the advance figure for seasonally adjusted initial claims was 269,000, an increase of 9,000 from the previous week's unrevised level of 260,000. The 4-week moving average was 269,250, a decrease of 1,750 from the previous week's unrevised average of 271,000.The previous week was unrevised at 260,000.

There were no special factors impacting this week's initial claims.

The following graph shows the 4-week moving average of weekly claims since 1971.

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims declined to 269,250.

This was at the consensus forecast of 270,000, and the low level of the 4-week average suggests few layoffs.