RSS Feed

RSS Feed by Calculated Risk on 3/20/2007 02:32:00 PM

Tuesday, March 20, 2007

People's Choice Home Loan BK, LoanCity Closes Shop

Tiffany Kary at Bloomberg reports: People's Choice Home Loan Files for Bankruptcy

People's Choice Home Loan Inc., ... filed for bankruptcy protection.And apparently LoanCity is finished (hat tip Anthony):

The Chapter 11 filing today in U.S. Bankruptcy Court in Santa Ana, California, comes as delinquency rates on so-called subprime home mortgages hit a four-year high. ...

People's Choice, based in Irvine, California, is the fourth subprime lender to file for bankruptcy since December, joining Ownit Mortgage Solutions LLC, Mortgage Lenders Network USA Inc. and ResMae Mortgage Corp.

...

Filing the same day as People's Choice Home Loan was People's Choice Funding Inc. The companies are subsidiaries of People's Choice Financial Corp., a real estate investment trust.

LoanCity is closed for business. Today March 20, 2007 is the last day we will be funding loans.LoanCity closed seven branches in February, so this must be the remaining five branches.

Mortgage lender LoanCity closed seven branches recently, leaving it with five nationally, BankNet360 has learned.The Mortgage Lender Implode-O-Meter is going to be busy.

The San Jose, Calif.-based lender closed offices due to a “softer market and improved technology, which allows for better load balancing among branches,” according to a company spokesman.

LoanCity originated about $5 billion of loans last year, which includes prime, alt-A and jumbo mortgages.

BofA See 15% Drop in New Home demand, Citigroup Remains Bullish

by Calculated Risk on 3/20/2007 10:29:00 AM

In a research note this morning, Bank of America Securities analyst Daniel Oppenheim wrote that mortgage lending problems go "well beyond subprime" are "likely to cut 15% of demand" for New Homes.

"Our view is that the excess inventory of homes for sale (the primary issue) and the reduced demand from tighter lending will lead to lower prices and likely exacerbate mortgage delinquencies and foreclosures," wrote Oppenheim.

See MarketWatch: Stricter loans seen draining new-home demand for more.

Meanwhile, MarketWatch reports that Citigroup remains bullish: Bullish home-builder analyst sticking to guns

One of most consistently bullish Wall Street analysts covering home builders during the housing downturn argues that the hand-wringing over the subprime-mortgage market and its potential impact on the already beaten-down group may be exaggerated.

"The threat from the subprime issue on home builders is obviously large, but somewhat indirect," wrote Citigroup analyst Stephen Kim in a research note this weekend. "It is also widely discussed and prone to hyperbole."

Housing Starts and Completions

by Calculated Risk on 3/20/2007 08:41:00 AM

The Census Bureau reports on housing Permits, Starts and Completions. Seasonally adjusted permits declined:

Privately-owned housing units authorized by building permits in February were at a seasonally adjusted annual rate of 1,532,000. This is 2.5 percent below the revised January rate of 1,571,000 and is 28.6 percent below the February 2006 estimate of 2,147,000.Starts rebounded:

Privately-owned housing starts in February were at a seasonally adjusted annual rate of 1,525,000. This is 9.0 percent above the revised January estimate of 1,399,000, but is 28.5 percent below the February 2006 rate of 2,132,000.And Completions declined significantly:

Privately-owned housing completions in February were at a seasonally adjusted annual rate of 1,664,000. This is 9.4 percent below the revised January estimate of 1,836,000 and is 18.4 percent below the February 2006 rate of 2,038,000.

Click on graph for larger image.

Click on graph for larger image.The first graph shows Starts vs. Completions.

As expected, Completions are now following Starts "off the cliff". Completions are the key number in this release, since employment follows completions.

This graph shows starts, completions and residential construction employment. (starts are shifted 6 months into the future). Completions and residential construction employment are highly correlated, and Completions lag Starts by about 6 months.

Based on historical correlations, it is reasonable to expect residential construction employment to follow Starts and Completions "off the cliff". It is reasonable to expect significant residential construction job losses over the next several months.

Monday, March 19, 2007

More on Bank Exposure to Real Estate

by Calculated Risk on 3/19/2007 04:13:00 PM

Professor Kash has a followup: How Exposed Are Banks to Real Estate?

My earlier post: Commercial Bank Exposure to Real Estate

FICOs and AUS: We Will Add Your Distinctiveness to Our Collective

by Calculated Risk on 3/19/2007 01:13:00 PM

From Tanta:

Brian asked, in the comments to an earlier post regarding FICO scores, why mortgage lenders have not developed a “mortgage score” that would address the deficiencies in FICO when it comes specifically to mortgage underwriting. In fact, such attempts have been made and have never really gotten off the ground. It’s a very good question, though, and since the last time I launched onto a giant long Nerdish explanation of some dorky mortgage matter, some serious coin dropped into the CR tip jar, it occurs to me that you all deserve another one. This is, my dears, by way of thanking you all for the tips. It goes straight to my coffee-and-chocolate budget, which just then produces more lengthy posts. My story is that that’s a virtuous cycle, and I’m sticking to it.

The main reason that mortgage scores never got far, in my view, is the development of automated underwriting systems (AUS). The earliest attempts at building an AUS, in the late 80s and early 90s, used some sort of internal credit scorecard. By the mid-to-late 90s, when Freddie Mac and then Fannie Mae were perfecting their AUS, FICO scores had become an easily and widely available “credit scorecard,” and so the development path of these AUS changed, from the idea of creating a new credit scoring method for mortgages to creating the additional rule sets and algorithms needed, beyond the analysis of a borrower’s consumer credit history, to fully analyze mortgage loans. In other words, the AUS were intended to be automated “holistic” analysis, not just more computerized credit scoring.

The history and development of AUS is fascinating (really, it is, my UberNerds). It is, however, beyond today’s scope. Let me just note that a few years ago, the general situation in the industry was that the systems of the GSEs (Freddie Mac’s Loan Prospector (LP) and Fannie Mae’s Desktop Underwriter (DU), both of which could also handle FHA loans via additional technology called FHA TOTAL Scorecard), were the gold standard for AUS in the conforming-balance prime loan world. But they were never designed to underwrite loans that are not eligible for delivery to the GSEs, including jumbos, no docs, subprime (outside of the A- stuff the agencies have special AUS capabilities for), and a lot of exotic product structures (like the Option ARM). So there was parallel development by large private investors of their own AUS, the two best-known and most reliable of which are Countrywide’s CLUES and GMAC-RFC’s AssetWise, both of which specialize in jumbo loan balances, Alt-A and subprime.

But while just about every lender, correspondent, and broker in the country could have access to LP or DU for very low cost, and needed to anyway for its GSE loans, you had to be a correspondent of Countrywide or RFC to get access to CLUES or AssetWise, and like anyone else Countrywide and RFC tended to expect you to sell them the loan if you used their systems to underwrite it. Other buyers of jumbo and Alt-A whole loans might appeal to these smaller loan originators, but those other buyers didn’t offer an AUS, which are very expensive to develop. There became a habit of originators using the ones everyone had access to and were familiar with, LP and DU, to underwrite loans that neither system was designed to accommodate. What happened is that the whole-loan buyers would create an “overlay” of rules that a jumbo or Alt loan had to meet, in addition to approval of the loan by LP or DU. A very odd hybrid of traditional and automated underwriting was born; Star Trek fans are free to imagine Borg drones (half organic, half machine creatures) invading the mortgage world. Resistance sure seemed futile there for a while.

I mentioned this on an earlier post about the new subprime mortgage guidance, but let me touch on it again: you can offer “reduced documentation” loans in two general ways, lender-directed or borrower-directed. Lender-directed means that the lender first looks at the loan as a whole, including the proposed loan amount, sales price and appraised value, borrower credit history, and the income, assets, and liabilities that are indicated (still just “stated” at this point) on the loan application, plus the treasure-trove of other information that is on a loan application (where you work, how long you’ve worked there, what other real estate you own, whether you have supplemental assets like retirement accounts or cash-value life insurance, etc.). If all of that looks good enough—or it all looks low-risk enough—the lender might decide that the income or assets can be verified with less documentation than is usually required, or perhaps even no documentation. For instance, what is “usually required” to count a loan as full-doc is that the borrower verify income for the last two years, as well as currently. For a salaried borrower, that would mean submitting the last two years’ W-2s, plus a current year-to-date pay stub. (If your pay stub doesn’t show year-to-date, you have to scrounge up enough of them to prove that your current pay is not just this week’s fluke, which can happen for hourly employees who might just have worked more hours than usual this week, or for borrowers who receive a bonus. The lender doesn’t want to know what you made in your best month ever, but what can count as “stable monthly income.”) After a review of the file, the lender might require the borrower to submit only the last pay stub, and allow him or her to skip hunting down the W-2s.

This isn’t really just “documentation relief,” to use an actual industry phrase that might well drive you nuts. (Relief? Like having to prove your income is some giant burden?) It is also often a way to allow a loan to be underwritten at a marginally higher income figure than would have been calculated with true “full doc,” because, as in the examples I listed above, a true full-doc loan might involve some income “averaging” to arrive at the “stable monthly income.” Your average monthly income over the last two years can, clearly, be higher or lower than your last month’s income. Traditionally, underwriters considered an upward trend to be favorable, as long as there were any reason to think it would continue, and a downward trend to be worrisome, generally requiring some good offsetting factor like a higher than usual down payment or a perfect rather than just acceptable credit record. You can see, then, that when you don’t get the two years’ W-2s, just the current pay stub, you aren’t doing any averaging; you are taking the additional risk that the current pay stub is distorting a trend. For most salaried borrowers, that’s not a huge risk. It can be a major risk when we get to commissioned borrowers, contract workers, and so on, who are not, we notice, getting to be smaller rather than larger percentages of the workforce pool. (It was a big problem in the NASDAQ bubble, when you’d get all these folks wanting to count recently exercised stock options as “stable monthly income.” Underwriters can be crankier than usual—in need of regular chocolate infusions—in January of any given year, because they see more than usual numbers of borrowers wanting to count the annual bonus as current monthy income.)

In any case, this kind of “lender-directed” program of doc relief is different from a borrower-directed program, in which the borrower comes to you and requests a low-doc or no-doc loan up front. The specific term for that is “adverse self-selection,” and it is much riskier than a lender-directed program. It also creates one of the big problems of using an AUS like LP or DU to underwrite these loans. LP and DU were designed to be lender-directed programs; they might allow some doc relief after the initial analysis is done, but they always start with the “assumption” that any number you type in for income or assets is verifiable if not initially verified. That’s a huge, important difference. The initial analysis can “give more weight” to things like DTI and reserves after closing if it can consider those things as potentially verified fact rather than quite possibly unverifiable smoke. It might “decide” to let those things remain unverified, or only partially verified, but it does so, if I can put it this way, because it knew it had the right to demand otherwise. A “borrower-directed” low doc loan simply messes up the whole underlying assumption of verifiability. And, of course, a borrower-directed low or no doc loan is, as we’ve seen, probably (although not necessarily, of course) already “gaming” the system: inflating the income or assets so that the DTI or reserve calculations come up with better results than they would have using verifiable numbers. The huge joke is that you can get the AUS offering “relief” to a borrower who qualified for that “relief” by lying to the system up front.

(It is possible, of course, to get around that problem by building in some algorithm that selects a certain number of loans to be forced into full doc, regardless of whether they might otherwise have been eligible for doc relief, to create some disincentive for gaming. I won’t say the GSEs aren’t doing that; I honestly don’t know, although I don’t see any signs that it’s working if it is happening. The problem, though, is making sure that such an instant-feedback fear of getting caught lying is applied enough for any individual user of the AUS to create the right Pavlovian behavior. Remember that the GSEs buy loans at the top of the food chain, mostly, from big seller/servicers and “aggregators,” who in turn buy their loans from smaller correspondents and fund loans for little brokers. The AUS gets used at the top of the chain and also at the bottom (the borrower entry level). So your algorithm would have to work by selecting a big enough percent of those little bottom-level pipelines of loans to scare any individual originator, as well as by selecting enough of the aggregator’s pipeline to scare the aggregator. This is by way of saying that we’re dealing with second- and third- and fourth-order effects of how the business structure, in “disintermediating” the process, finds a way to create a problem that the original software engineers didn’t have in their sights. You have to keep re-modulating your phasers, because the Borg adapts.)

In large part, that’s where this “hybrid” or Borg approach comes in: whole-loan investors did (mostly) realize that LP and DU were not designed to accommodate borrower-directed low doc or no doc loans. They’re also not designed to accommodate jumbos in a very important sense. Since LP and DU are designed to analyze loans the GSEs actually buy, their internal logic was designed, for instance, to weigh the proposed down payment on the loan with the assumption that the loan amount isn’t going to be higher than $417,000 (currently). A 20% down payment on a $471,000 loan is generally considered a compensating factor for other possible weaknesses (like tight ratios or a few minor credit dings). But a 20% down payment on a $1,000,000 loan? That might not even meet basic program guidelines; it might be possible, but it stops being a compensating factor and becomes a weakness that needs compensation elsewhere. In other words, a traditional view of things indicates that an 80% $1MM loan is the equivalent of a 90% or so conforming loan: possible, but definitely in the higher-risk bucket. But in a real sense LP and DU didn’t “know” that, because they weren’t designed to handle the problem. Ergo, you had the investor accepting these loans underwritten by the AUS, as long as it met a separate “overlay” or second hurdle of requirements to get around this problem.

Eventually Fannie Mae came up with the idea of “Custom DU,” which is a way a lender can access DU for loans that aren’t Fannie Mae-eligible by “customizing” its product eligibility features to take things like jumbo balances and borrower-directed documentation reduction into account. (You may ask why a GSE is putting such investment in technology to accommodate loans it is in no way chartered to buy. You may be asking about something like the concept of “corporate welfare,” where the private sector gets the quasi-government sector to subsidize its technology costs. But that’s another day’s problem.) This is still a fairly new development and, as far as I’m concerned, the results aren’t in yet (someone else might tell you different, of course). But we here at CR have now become quite wary of these things without a long enough performance history. And it’s not just history I want; there’s also the problem with the level of possible “customization.” The short version, for now at least, is that I am concerned that investors don’t know enough about the core logic of the system (the “black box” part) to know if the things that can be customized (product eligibility rules like maximum loan amount, documentation type, and so on) are 1) customized correctly and 2) sufficiently compatible with the core logic. The customization is done by the lender, and so it’s only as good as the lender’s inputs (there are competence issues here as well as potentially abuse and failure-to-test issues). Furthermore, you get back to the whole logic problem behind the lender-vs-borrower directed issue: at what level does too much customization defeat the purposes of the machine’s approach?

On an earlier post I talked about conforming loans as the vanilla ice cream of the mortgage business; I’ve also used the term “commodity” to describe them. The development of GSE AUS was spurred as much by the desire to keep its book of business uniform and homogeneous as much as to use technology to speed up and increase productivity of the loan approval process. The whole idea was that the AUS could sort out the vanilla ice cream from the mocha java praline mango. It is in no way clear to me that the eventual use of GSE AUS for nonconforming loans, with an overlay or with customization, was motivated largely by anyone’s desire to impose uniformity and homogeneity on the jumbo and Alt production. I personally believe that it was motivated more by two things, one more respectable and one less so: first, it was a desire to capture the speed and productivity increases of technology. Second, it was an attempt by at least some people to get the “seal of approval” of LP or DU on exotic loans—in other words, the “core logic” incompatibility was a feature, not a bug, to some folks. I’d start seeing that a lot in due diligence. I’d find some god-awful loan I’d throw on my problem loan list, only to have the originator come back and say, “Yeah, but we got a DU approve on that one.” My response was something on the order of “Yes, but you threw a loan at DU that was ‘over its head,’ as it were.” They did that for a reason.

So how do we get back to FICO? Well, the AUS out there—at least LP and DU—do not use FICO scores as such. The GSEs still require lenders to get them and report them on the loans, but the AUS do their own internal credit analysis based on raw data imports from an electronic credit report. That’s what I meant above by indicating that the development shifted away from creating a free-standing “mortgage score” to replace FICO. AUS do not need another “free-standing” score, because they’re designed to do the holistic underwriting themselves. They’re an attempt to automate what a traditional underwriter before FICOs did.

That’s what I meant in the comment section of this post when I indicated that, for mortgage people, FICOs traditionally were useful less as a predictive tool than a communication tool: it’s not so much that traditional lenders like the GSEs ever depended on FICO’s analytics to substitute for their own default estimates; it’s that FICO score became a handy, consistent, easily-available “shorthand” designation of a loan’s credit quality, insofar as over time they were “calibrated” to GSE loan performance, and the GSEs could then set the actual FICO “bucketing” guidelines (over 720, under 620, etc.). What that means, in essence, is that they were less important to traditional underwriters (people or machines) than they were to investors in traditional loans. As I suggested in this post, the giant MBS market works “efficiently” insofar as end-investors can really just make a lot of reliable assumptions about what’s going on in the details of processing the underlying mortgage loans (the “sausage factory”). By reporting such indications of credit quality as FICO, LTV, DTI, doc type, etc., a lender can “indicate” to a bond buyer what the general quality of the loans is, and the bond buyer can have a sort of “reality check.” The exact methods I use to get into the weeds with individual loans might be a matter of “rep and warranty,” but you, the end investor, can glance at the general stratification of the pool I supply you with, the FICO, LTV, etc., and you can check the plausibility of those reps and warranties. If I’m claiming to use “traditional” underwriting methods but I produce these pools with these low average FICOs, you might wonder what the hell I mean by “traditional.” You might be right to do so.

From using FICOs as a short-hand indication of credit quality, it was a short step to using them to price things. By price, I mean more than just setting the interest rate and points for an individual loan, or even the price of a security or tranche thereof. FICOs are involved in setting the required credit enhancement levels of a security (such as overcollateralization), the MI premium required, the due diligence level required, and any number of things that, basically, come out of the yield of a loan. I, actually, worry as much if not more about this issue than I do in using FICOs as part of the initial underwriting. We’ve had occasional discussions here on the blog about “guideline rationing” versus “price rationing” as mechanisms of credit crunching. That whole issue is about whether available credit is reduced as much by making it too expensive as by re-writing the guidelines so that people don’t qualify for certain kinds of loans. It’s a true chicken-and-egg problem, though. Suffice it to say, for now, that a large distortion may have entered the market during the boom because FICO (a kind of derivative or simplification of a complex credit analysis) drove a lot of pricing decisions. That, in short, is the “Alt-A” problem in a nutshell: not only did the FICO of those loans make them look like “prime,” it made people willing to price them at tiny risk premiums over prime. So pricing models have to get as complex as AUS models, and they have to be applied to the right kind of product, or else you have the same problem as I’ve indicated above with using LP or DU to underwrite a “nontraditional” loan. Borg pricing is as scary as Borg underwriting.

The rating agencies do have their own software—S&P’s Levels is generally the standard—that are supposed to account for pricing/credit enhancement levels on nontraditional product. I still think those models over-weight FICO, and that that’s a large part of why it seems that “Alt-A” is deteriorating “so fast.” There’s a whole issue out there about why, then, people aren’t using more AUS like CLUES or AssetWise, which were designed to handle Alt-A, but that kind of gets complicated by what we’re hearing from Countrywide and RFC about their own little Alt problems. Perhaps building an Alt AUS is harder than everyone thought? Perhaps speed and efficiency are more “expensive” than we thought? Perhaps you don’t have to be an outright Luddite to conclude that, maybe, we should give this tech fetish another thought? I have observed before now that I very often think we fail to consider certain kinds of tech in the mortgage business at its “true cost,” and that once you do that, you often find the vaunted cost savings and productivity increases kind of evaporating on you when your business adapts, like the Borg does, to whatever high-tech weapon you can fire at it. But I am known as an unassimilated thinker.

Tanta

Builder Confidence Declines in March

by Calculated Risk on 3/19/2007 01:05:00 PM

Click on graph for larger image.

Click on graph for larger image.

UPDATE: NABH Press Release: Builder Confidence Slips In March

Builder confidence in the market for new single-family homes receded in March, largely on concerns about deepening problems in the subprime mortgage arena, according to the National Association of Home Builders/Wells Fargo Housing Market Index (HMI), released today. After rising fairly steadily since its recent low last September, the HMI declined three points from a downwardly revised 39 reading in February to 36 in March.

“Builders are uncertain about the consequences of tightening mortgage lending standards for their home sales down the line, and some are already seeing effects of the subprime shakeout on current sales activity,” said NAHB Chief Economist David Seiders. “The fundamentals of today’s housing market still are relatively strong, including a favorable interest-rate structure, solid growth in employment and household income, lower energy prices and improving affordability in much of the single-family market – due in part to price cuts and non-price sales incentives offered by builders. NAHB continues to forecast modest improvements in home sales during the balance of 2007, although the problems in the mortgage market increase the degree of uncertainty surrounding our baseline (i.e., most probable) forecast.”

Derived from a monthly survey that NAHB has been conducting for 20 years, the NAHB/Wells Fargo HMI gauges builder perceptions of current single-family home sales and sales expectations for the next six months as either “good,” “fair” or “poor.” The survey also asks builders to rate traffic of prospective buyers as either “high to very high,” “average” or “low to very low.” Scores for each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view sales conditions as good than poor.

All three component indexes registered declines in March after having risen in the previous month. The index gauging current single-family home sales and the index gauging sales expectations for the next six months each declined three points, to 37 and 50, respectively. Meanwhile, the index gauging traffic of prospective buyers declined a single point, to 28.

Regionally, the HMI results were somewhat mixed. In the Midwest and West, the index gained one point to 28 and 36, respectively. In the Northeast, the HMI declined two points to 41, and in the South, it fell four points to 40.

Fremont General Gives Notice to Mortgage Staff

by Calculated Risk on 3/19/2007 12:26:00 PM

From Bloomberg (hat tip Brian): Fremont General Gives Mortgage Staff Two-Month Dismissal Notice

Fremont General Corp., the California thrift trying to sell its home-lending business, told the unit's staff they may be dismissed in two months.

...

"The company has aggressively been pursuing its options," Walker said. "Such efforts continue, although the company cannot provide more definitive information today."

...

California requires employers to give workers 60 days notice before "a plant closing or mass layoff," according to the state Employment Development Department's Web site.

First American Study on Foreclosures

by Calculated Risk on 3/19/2007 11:54:00 AM

From the OC Register: Homeowners face foreclosure

The United States likely will see 1.1 million foreclosures during the next six to seven years on adjustable-rate mortgages issued when home prices were at or near the peak of the market, a study released today by First American Corp. of Santa Ana says.Compare this to the Center for Responsible Lending report: Losing Ground: Foreclosures in the Subprime Market and Their Cost to Homeowners.

As a result, lenders will end up losing about $112.5 billion.

But that probably won't have a significant impact on the economy or the mortgage industry since the loss equals less than 1 percent of the $12 trillion in home loans projected for the next six years, the study said.

"This is not going to break the economy," said study author Christopher Cagen, director of research and analytics at First American CoreLogic, a First American company. "It's less than the price of alcohol. It's less than the price of gasoline going up to $3.25 a gallon. ... It's part of the business cycle and it's not going to be dominant."

"... foreclosure rates will increase significantly in many markets as housing appreciation slows or reverses. As a result, we project that 2.2 million borrowers will lose their homes ...I'm trying to find the First American study.

...

We project that one out of five (19 percent) subprime mortgages originated during the past two years will end in foreclosure. This rate is nearly double the projected rate of subprime loans made in 2002, and it exceeds the worst foreclosure experience in the modern mortgage market, which occurred during the “Oil Patch” disaster of the 1980s."

Sunday, March 18, 2007

Commercial Bank Exposure to Real Estate

by Calculated Risk on 3/18/2007 04:18:00 PM

Professor Kash had an interesting post on Friday: Bad Loans, Banks, and the Coming Credit Crunch Kash is trying to look at the incipient credit crunch from the bank's perspective.

"I've been thinking about the health of the banking sector of the US economy, and pulled together a couple of charts that have gotten me thinking. And worried."Check out Kash's post and graphs.

Kash presented the loan amounts in real terms. The following graph shows the loan amounts as a percent of GDP (Q1 2007 estimated).

Click on graph for larger image.

Click on graph for larger image.This graph shows the rapid increase in real estate loans. This category includes all loans collateralized by real estate, and includes residential, commercial and real estate construction and development loans.

The banking sector is clearly exposed to real estate, although the breakdown between residential and commercial isn't available.

Note: Commercial and industry (C&I) bank borrowing has risen recently as a percent of GDP, but the level is still low compared to historical norms. However this is bank loans only, and doesn't include any bonds. I'll have more on consumer borrowing soon.

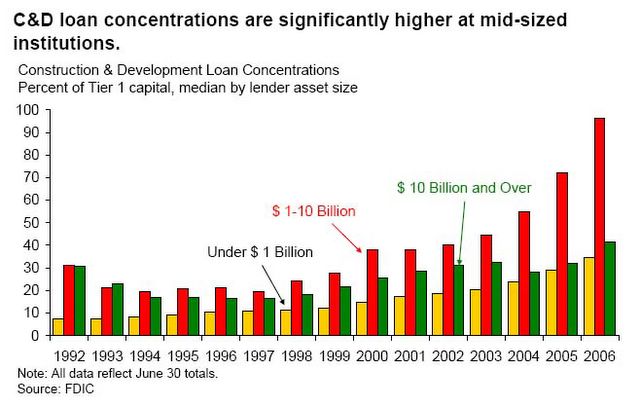

We know, from the FDIC Semiannual Report that the concentration of CRE and C&D loans has increased:

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. This suggests that, although small and mid-size institutions have been more successful in limiting the erosion of their nominal NIMs, they have achieved this success in part by assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loanThe housing crisis is now front page news, but there is little discussion about U.S. bank exposure to CRE loans. If a CRE slump follows the residential real estate bust (the typical historical pattern), then the U.S. commercial banks might have a serious problem.

concentrations, especially at institutions with total assets between $1 billion and $10 billion.

Currently delinquency rates are very low for CRE loans. But when times are tough, CRE loans usually have the highest overall delinquency rates.

Currently delinquency rates are very low for CRE loans. But when times are tough, CRE loans usually have the highest overall delinquency rates.I understand why Kash is thinking about this issue ... and why he is worried.

Tanta on FICO "Inflation"

by Calculated Risk on 3/18/2007 02:47:00 AM

From CR: At the OC Register, Mathew Padilla interviews Glenn Stearns of Stearns Lending. Here is an excerpt:

Stearns also said there has been an inflation in credit scores, known as FICO scores. He said some consumers with a maximum of $3,000 in credit had a FICO of 700, which generally is considered a good score. Such a first-time buyer had no proven history of making a house payment, he said. In his own business, he said customers that went into default tended to have credit scores greater than 700.This makes it sound like FICO scores are undergoing a process like “grade inflation” in college. Tanta explains that the problem isn't with the FICO score itself, but that using the FICO score alone is insufficient for first time homebuyers.

“Everyone is having to rethink credit scores,” he said.

The following is from Tanta:

Some of us (OldFart Mortgage, LTD) used to require a first-time homebuyer to have a 24-month rental history, and to verify that with a direct verification from the landlord or property management company. First, we would make sure that the borrower had a history of making housing (not “house”) payments on time. Then, we would calculate the borrower’s current housing expense as a ratio to gross monthly income, and compare it to the borrower’s proposed monthly housing expense (including taxes and insurance). The result of this comparison is actually what old-timers mean by the term “payment shock.” (The term for potential future issues on an ARM was “rate shock”; the press has completely muddled the terms now so much that it’s hopeless.) Anyway, the traditional rule of thumb was that a first-time homebuyer was limited to a proposed house payment no more than 150% of the current housing (rental) payment. That extra 50% allowed owning to be more expensive than rent, but also was conservative enough to allow for things like maintenance and other expenses that renters aren’t often in the habit of paying for. If you let them double their monthly housing payments, they can get into terrible trouble the first time they have to call a plumber. The theory is that second-time homebuyers have already learned this awful lesson and so they can be allowed more “shock” (as long as they still meet the total DTI max).

In any case, this verification of the rental payment history and “payment shock” test was on top of the required minimum FICO. So those borrowers described in the article—a nice pretty 700 FICO derived from one $3000 card balance—would not get the loan if they didn’t meet the other two tests. For instance, this old rule eliminated FTBs who were going straight from mom & dad’s place (or the dormitory) to a mortgage: they were ineligible because they couldn’t show a 24-month history of being responsible for their own housing costs. Ditto for someone “renting” a condo owned by the parents but not actually paying anything near a real housing cost burden. I used to get those “kiddie condo” deals a lot when I worked for a lender with branches in a college town.

In my view, it is among the most irresponsible of the irresponsible lending we’ve seen lately that FTB rules were relaxed to allow either 1) no history of making one’s own rental payments required or 2) not counting late rental payments as a reduction to FICO (they won’t affect the FICO if the landlord doesn’t report to the credit bureau, and small-time property owners don’t) or 3) the payment shock limit was increased to 200% or more.

That said, it’s not so much that FICOs get “inflated,” it’s that their importance to the loan qualification process is inflated. For anyone who has already owned a home, the mortgage payment history is already taken into account in the FICO (because mortgage servicers report to the bureaus). But first-timers present a cautionary tale in not letting the FICO bear more weight in your decision than it should.

I’m sure that’s probably what the guy in the newspaper meant, but as usual, the newspaper only deals in sound bites, so my version is just the one that shows the work as well as the answer, as it were. There are some other issues a lot of us have with FICOs; they can in some cases “reward” heavy debt users over limited debt users. That’s why a sane underwriter (yeah, right) reads the credit report instead of just looking at the FICO. The other side of this, you see, is that the borrower with $3000 on the cards might have a FICO of 700, but the borrower with $8000 on the cards might have a FICO of 750 (because that person’s credit record is older, or has more tradelines—the $8000 is split over three cards instead of one, and the more trades you have, generally, the higher your score until you get to the point where you’re maxed out). So just having stricter FICO rules for FTBs would end up setting the very perverse incentive of encouraging them to get into a lot of consumer debt so they can prove they’re good enough to get a home. I would rather go back to the (“inefficient”) old days where we used FICOs, but only as a guideline that had to be backed up with other considerations, positive and negative. I certainly don’t want to see young borrowers locked out of mortgage credit because they don’t have enough plastic in their wallets or because they bought an old beater for cash instead of taking out a car loan or lease for something new, for the love of Peat. But I fear that’s the message some of them have gotten.

And that gets us back to my long-standing problem with subprime lending becoming predatory lending. A lot of folk end up in subprime because they don’t have access to the kind of credit that would improve their FICOs enough to get them into prime. If you come from the side of town where the available credit is mostly payday lenders or rent-to-own stores—who don’t report to the bureaus—you are not only getting screwed on whatever borrowing you’re currently doing, because the rates are just usurious, you’re also screwed because paying those cruddy rates in a timely fashion doesn’t offer the reward of a good FICO score. My solution to a lot of the predatory lending problem is to make sure that depositories are offering “entry level” credit to low-to-moderate income people, including young people. If the banks get ahold of them before the sleazy credit card mailers or the local loan sharks do, they can get some debt experience in a safer and sounder manner. But some banks seem to have taken the position that they’ll let Providian or the local loan shark take the risk on entry level borrowers, and then they’ll pick out the few survivors for their prime loans, while putting the others into those high-yield subprime loans. When we focus exclusively on borrower behavior, without looking at lender behavior, we get a skewed view of how you “create” a subprime borrower in the first place.