RSS Feed

RSS Feed by Calculated Risk on 3/18/2007 04:18:00 PM

Sunday, March 18, 2007

Commercial Bank Exposure to Real Estate

Professor Kash had an interesting post on Friday: Bad Loans, Banks, and the Coming Credit Crunch Kash is trying to look at the incipient credit crunch from the bank's perspective.

"I've been thinking about the health of the banking sector of the US economy, and pulled together a couple of charts that have gotten me thinking. And worried."Check out Kash's post and graphs.

Kash presented the loan amounts in real terms. The following graph shows the loan amounts as a percent of GDP (Q1 2007 estimated).

Click on graph for larger image.

Click on graph for larger image.This graph shows the rapid increase in real estate loans. This category includes all loans collateralized by real estate, and includes residential, commercial and real estate construction and development loans.

The banking sector is clearly exposed to real estate, although the breakdown between residential and commercial isn't available.

Note: Commercial and industry (C&I) bank borrowing has risen recently as a percent of GDP, but the level is still low compared to historical norms. However this is bank loans only, and doesn't include any bonds. I'll have more on consumer borrowing soon.

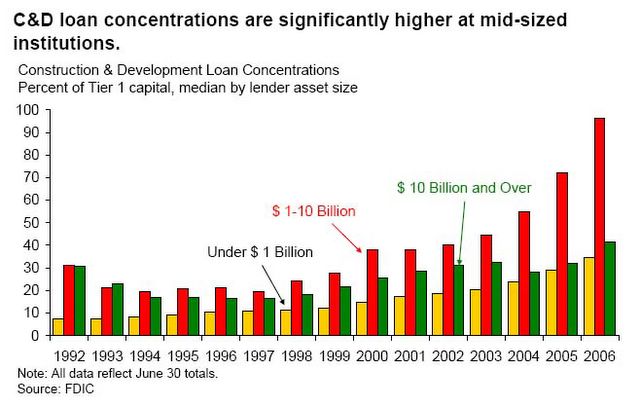

We know, from the FDIC Semiannual Report that the concentration of CRE and C&D loans has increased:

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. This suggests that, although small and mid-size institutions have been more successful in limiting the erosion of their nominal NIMs, they have achieved this success in part by assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loanThe housing crisis is now front page news, but there is little discussion about U.S. bank exposure to CRE loans. If a CRE slump follows the residential real estate bust (the typical historical pattern), then the U.S. commercial banks might have a serious problem.

concentrations, especially at institutions with total assets between $1 billion and $10 billion.

Currently delinquency rates are very low for CRE loans. But when times are tough, CRE loans usually have the highest overall delinquency rates.

Currently delinquency rates are very low for CRE loans. But when times are tough, CRE loans usually have the highest overall delinquency rates.I understand why Kash is thinking about this issue ... and why he is worried.