RSS Feed

RSS Feed by Calculated Risk on 8/04/2010 02:17:00 PM

Wednesday, August 04, 2010

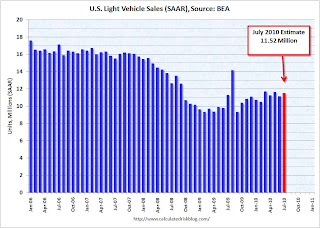

BEA: July light vehicle sales rate 11.5 million SAAR

I usually use the light vehicle estimate from AutoData for the seasonally adjusted annual rate. Their estimate is usually very close, however since the BEA didn't put out the adjustment factors in advance, AutoData estimated sales at 12 million SAAR in July with a notice that this might be revised.

The BEA released the sales numbers this morning, and the sales rate was 11.52 million (below most analyst estimates). This is a significant difference and worth mentioning. Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the historical light vehicle sales (seasonally adjusted annual rate) from the BEA.

This was below most forecasts of around 11.6 to 11.8 million SAAR, and is below the levels of March and May earlier this year.

Fed Research Supports Mortgage Cram Downs

by Calculated Risk on 8/04/2010 12:30:00 PM

Thomas J. Fitzpatrick IV and James B. Thomson at the Cleveland Fed provide new research that supports residential mortgage cram downs: Stripdowns and Bankruptcy: Lessons from Agricultural Bankruptcy Reform . A few excerpts:

[One proposal is] to revise Chapter 13 of the bankruptcy code to allow judges to modify mortgages on primary residences. The type of loan modification under consideration is known as a loan cramdown or loan stripdown because the judge would reduce the balance of the secured claim to the current market value of the house, turning the remaining balance of the mortgage into an unsecured claim (which would receive the same proportionate payout as other unsecured debts included in the bankruptcy petition).And the authors discuss how this worked for farm loans:

The actual negative impact of the farm stripdown legislation was minor. Although the legislation created a special chapter in the Bankruptcy Code for farmers and allowed stripdowns on primary residences, it did not change the cost and availability of farm credit dramatically. In fact, a United States General Accounting Office (1989) survey of a small group of bankers found that none of them raised interest rates to farmers more than 50 basis points. While this rate change may have been a response to the Chapter 12, it is also consistent with increasing premiums due to the economic environment. This suggests that the changes in the cost and availability of farm credit after the bankruptcy reform differed little from what would be expected in that economic environment, absent reform.It appears the cram down legislation was very effective.

What was most interesting about Chapter 12 is that it worked without working. According to studies by Robert Collender (1993) and Jerome Stam and Bruce Dixon (2004), instead of flooding bankruptcy courts, Chapter 12 drove the parties to make private loan modifications. In fact, although the U.S. General Accounting Office reports that more than 30,000 bankruptcy filings were expected the year Chapter 12 went into effect, only 8,500 were filed in the first two years. Since then, Chapter 12 bankruptcy filings have continued to fall.

And residential mortgage cram downs are not new. The law was changed in 1978 and cram downs eliminated in 1993.

In 2007 my former co-blogger and mortgage banker Tanta explained the history of mortgage cram downs and argued they would be helpful now: Just Say Yes To Cram Downs

I am fully in favor of removing restrictions on modifications of mortgage loans in Chapter 13, but not necessarily because that helps current borrowers out of a jam. I'm in favor of it because I think it will be part of a range of regulatory and legal changes that will help prevent future borrowers from getting into a lot of jams, which is to say that it will, contra MBA, actually help "stabilize" the residential mortgage market in the long term. Any industry that wants special treatment under the law because of the socially vital nature of its services needs to offer socially viable services, and since the industry has displayed no ability or willingness to quit partying on its own, then treat it like any other partier under BK law.Looking at the Fed research, it appears Tanta's argument about mortgage cram downs bringing stability and discipline to the residential mortgage market long term would be correct. It is never too late: Say yes to cram downs!

ISM Non-Manufacturing Index shows expansion in July

by Calculated Risk on 8/04/2010 10:00:00 AM

The July ISM Non-manufacturing index was at 54.3%, up from 53.8% in June - and above expectations of 53.7%. The employment index showed expansion in July at 50.9%. Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

The employment index is at the highest level since December 2007.

From the Institute for Supply Management: July 2010 Non-Manufacturing ISM Report On Business®

Economic activity in the non-manufacturing sector grew in July for the seventh consecutive month, say the nation's purchasing and supply executives in the latest Non-Manufacturing ISM Report On Business®.

The report was issued today by Anthony Nieves, C.P.M., CFPM, chair of the Institute for Supply Management™ Non-Manufacturing Business Survey Committee; and senior vice president — supply management for Hilton Worldwide. "The NMI (Non-Manufacturing Index) registered 54.3 percent in July, 0.5 percentage point higher than the 53.8 percent registered in June, indicating continued growth in the non-manufacturing sector at a slightly faster rate. The Non-Manufacturing Business Activity Index decreased 0.7 percentage point to 57.4 percent, reflecting growth for the eighth consecutive month. The New Orders Index increased 2.3 percentage points to 56.7 percent, and the Employment Index increased 1.2 percentage points to 50.9 percent, reflecting growth after one month of contraction. The Prices Index decreased 1.1 percentage points to 52.7 percent in July, indicating that prices are still increasing but at a slower rate than in June. According to the NMI, 13 non-manufacturing industries reported growth in July. Respondents' comments are mixed. They vary by industry and company, with a tilt toward cautious optimism about business conditions."

emphasis added

ADP: Private Employment increases 42,000 in July

by Calculated Risk on 8/04/2010 08:15:00 AM

ADP reports:

Nonfarm private employment increased 42,000 from June to July 2010 on a seasonally adjusted basis, according to the ADP National Employment Report®. The estimated change of employment from May to June was revised up slightly, from the previously reported increase of 13,000 to an increase of 19,000.Note: ADP is private nonfarm employment only (no government jobs).

July’s rise in private employment was the sixth consecutive monthly gain. However, over those six months increases have averaged a modest 37,000, with no evidence of acceleration.

Unlike the estimate of total establishment employment to be released on Friday by the Bureau of Labor Statistics (BLS), today’s figure does not include the effects of federal hiring — and now firing — for the 2010 Census.

The consensus was for ADP to show an increase of about 35,000 private sector jobs in July, so this was slightly above consensus.

The BLS reports on Friday, and the consensus is for a decrease of 70,000 payroll jobs in July, on a seasonally adjusted (SA) basis, with the loss of around 145,000 temporary Census 2010 jobs (+75,000 ex-Census).

MBA: Mortgage Purchase Applications increase slightly last week

by Calculated Risk on 8/04/2010 07:24:00 AM

The MBA reports: Mortgage Applications Increase in Latest MBA Weekly Survey

The Refinance Index increased 1.3 percent from the previous week. The seasonally adjusted Purchase Index increased 1.5 percent from one week earlier. This third straight weekly increase in the Purchase Index was driven by government purchase applications which increased 3.4 percent from last week, while conventional purchase applications were essentially flat.

...

The average contract interest rate for 30-year fixed-rate mortgages decreased to 4.60 percent from 4.69 percent, with points increasing to 0.93 from 0.88 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the MBA Purchase Index and four week moving average since 1990.

The purchase index has increased slightly for three straight weeks - but is still 40% below the level of the last week of April (and about 33% below the last week of April using the 4-week average).

This recent collapse in the purchase index has already shown up as a decline in new home sales (counted when the contract is signed), and will show up in the July and August existing home sales reports (counted at close of escrow).