RSS Feed

RSS Feed by Calculated Risk on 6/21/2010 11:30:00 AM

Monday, June 21, 2010

Housing Tax Credit Extension Update

David Rosenberg, chief economist at Gluskin Sheff + Associates, wrote this morning:

"We heard from Ivy Zelman (top-rated real estate research) on Friday that the bill that included an extension for the closing date of the homebuyer tax credit fell two votes short of passing in the Senate. This virtually assures that it will not become law prior to the June 30th deadline. Ivy says that while it is difficult to quantify the impact, the fact that as of yet there is no extension, which was widely expected in this bailout nation, it could trigger a jump in cancellations beginning in July if a sizeable number of sales are not closed in time."Rosenberg is referring to H.R.4213 the "American Jobs and Closing Tax Loopholes Act of 2010".

The amendment (S.AMDT.4344) to extend the closing date for the tax credit passed last week on a vote of 60 to 37.

The Senate is still debating the other tax extenders, and was unable to obtain cloture (this is what Zelman was referring to). This bill also includes the extension of the date (not duration) of unemployment benefits and other provisions. One of the sticking points is the extension of the COBRA benefit.

China's Yuan Rises against Dollar

by Calculated Risk on 6/21/2010 08:38:00 AM

From Reuters: China's Yuan Jumps After Flexibility Pledge

The yuan closed at 6.7976 against the dollar, up 0.42 percent from Friday's close ...The yuan has been essentially pegged at 6.83 since July 2008.

On Saturday China announced more exchange rate flexibility ... here are some excerpts from the statement (via WSJ):

In view of the recent economic situation and financial market developments at home and abroad, and the balance of payments (BOP) situation in China, the People´s Bank of China has decided to proceed further with reform of the RMB exchange rate regime and to enhance the RMB exchange rate flexibility.

...

The global economy is gradually recovering. The recovery and upturn of the Chinese economy has become more solid with the enhanced economic stability. It is desirable to proceed further with reform of the RMB exchange rate regime and increase the RMB exchange rate flexibility.

Sunday, June 20, 2010

Apartment owner on rental market: "Worst ever", Charge-offs triple

by Calculated Risk on 6/20/2010 09:42:00 PM

Some landlords think rents have bottomed ... other are not so optimistic ...

From Jon Lansner at the O.C. Register: ‘Worst ever’ market hits O.C. landlords

Veteran Orange County apartment owner and manager Ray Maggi says this the current rental market “is the worst I’ve ever seen” for landlords.

...

Last year, landlords usually offered free months of rent as lures for new tenants. This year, Maggi says, more landlords have simply slashed rents to meet tight-fisted renters who have plenty of choice.

Making matters worse for property owners is that a growing number of tenants aren’t keeping up with payments. Charge-offs have roughly tripled to nearly 3 percent of rents due.

Look Ahead to FOMC Statement on Wednesday

by Calculated Risk on 6/20/2010 05:17:00 PM

The previous post was the Weekly Summary and a Look Ahead.

The FOMC statement to be released on Wednesday will be interesting. This is the first scheduled FOMC meeting since the EU / ECB rescue package was announced on May 9th. In addition, some of the economic data since the last FOMC meeting has been somewhat disappointing.

Two things are nearly certain: 1) the FOMC will not increase the Fed Funds rate at this meeting, and 2) the key language about "exceptionally low levels of the federal funds rate for an extended period" will remain.

Here are a few excerpts from the last FOMC statement to see some possible changes:

Information received since the Federal Open Market Committee met in March suggests that economic activity has continued to strengthen and that the labor market is beginning to improve. Growth in household spending has picked up recently ...Since the April meeting, growth appears to have slowed, the labor market has stumbled, and retail spending was weak. The first sentence will be less positive this meeting.

Housing starts have edged up but remain at a depressed level.Housing starts plummeted in May.

With substantial resource slack continuing to restrain cost pressures and longer-term inflation expectations stable, inflation is likely to be subdued for some time.It is possible that the Fed will mention the downside risk to prices (deflation). The Fed might also mention the European situation.

Last week, Jon Hilsenrath at the WSJ wrote "Federal Reserve officials are beginning to debate quietly what steps they might take if the recovery surprisingly falters or if the inflation rate falls much more". These discussions are probably part of the agenda, but I doubt there will be any mention in the FOMC statement.

Weekly Summary and a Look Ahead

by Calculated Risk on 6/20/2010 11:59:00 AM

Two key housing reports will be released this week: existing home sales on Tuesday, and new home sales on Wednesday.

On Tuesday at 10 AM, the National Association for Realtors (NAR) will release the May existing home sales report. The consensus is for an increase to 6.2 million sales in May, at a seasonally adjusted annual rate (SAAR), from 5.77 million in April (SAAR). I'll take the under because I think there will be a larger than normal fallout from pending home sales. A key number in the release will be existing home inventory. Inventory surged in April, to over 4 million homes for sale, as sellers tried to take advantage of the homebuyer tax credit. I expect inventory to decline in May.

Also on Tuesday, the FHFA house price index, and the Richmond Fed survey will be released.

On Wednesday at 10 AM, the Census Bureau will release the May New Home sales report. The consensus is for a sharp decrease in sales to around 400K (SAAR), down from 504K in April. Since new home sales are reported when a contract is signed, April was the last month that reported sales will be positively impacted by the tax credit. The May AIA's Architecture Billings Index will also be released on Wednesday (a leading indicator for commercial real estate).

Also on Wednesday, the FOMC statement will be released at 2:15 PM ET (conclusion of 2 day meeting).

On Thursday, the May Durable Goods Orders will be released at 8:30 AM. The consensus is for a 1.2% decrease. Also on Thursday, the closely watched initial weekly unemployment claims will be released. Consensus is for a decline to 465K from 472K last week.

On Friday, the third estimate of the Q1 GDP report will be released at 8:30 AM. The consensus is for no significant change (3.0% annualized growth rate). And of course the FDIC will probably have another busy Friday afternoon ...

Note: Other reports that will probably be released this week include the Moodys/REAL Commercial Property Price Index (for April) and the HAMP May report.

And a summary of last week:

Click on graph for larger image in new window.

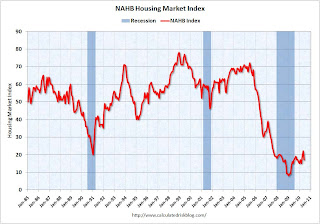

Click on graph for larger image in new window.This graph shows the builder confidence index from the National Association of Home Builders (NAHB).

The housing market index (HMI) was at 17 in June. This was a sharp decline from 22 in May.

Note: any number under 50 indicates that more builders view sales conditions as poor than good.

Total housing starts were at 593 thousand (SAAR) in May, down 10% from the revised April rate of 659,000 (revised down from 672 thousand), and up 24% from the all time record low in April 2009 of 477 thousand (the lowest level since the Census Bureau began tracking housing starts in 1959).

Total housing starts were at 593 thousand (SAAR) in May, down 10% from the revised April rate of 659,000 (revised down from 672 thousand), and up 24% from the all time record low in April 2009 of 477 thousand (the lowest level since the Census Bureau began tracking housing starts in 1959). Single-family starts collapsed 17.2% to 468,000 in May. This is 30% above the record low in January 2009 (360 thousand).

This was way below expectations (I took the under!), and is good news for the housing market longer term (there are too many housing units already), but bad news for the economy and employment short term.

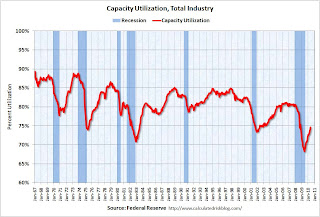

From the Fed: Industrial production and Capacity Utilization

This graph shows Capacity Utilization. This series is up 9.4% from the record low set in June 2009 (the series starts in 1967).

This graph shows Capacity Utilization. This series is up 9.4% from the record low set in June 2009 (the series starts in 1967). Capacity utilization at 73.7% is still far below normal - and 7.2% below the the pre-recession levels of 80.5% in November 2007.

Note: y-axis doesn't start at zero to better show the change.

Here is the Philadelphia Fed Index released this week: Business Outlook Survey.

This graph shows the Philly index for the last 40 years.

This graph shows the Philly index for the last 40 years.The index has been positive for ten months now, but turned down "notably" in June.

This might suggest that growth in the manufacturing sector is slowing. Especially concerning is the slightly negative employment index.

From the NAHB, framing lumber prices have collapsed since the end of April.

From the NAHB, framing lumber prices have collapsed since the end of April.This graph shows two measures of lumber prices: 1) from Random Lengths (via NAHB), and 2) CME futures.

With so many mills shut down during the bust, the supply of lumber was way down - and prices surged early this year with a slight increase in construction activity. Now that construction has slowed - at the same time mills were coming back online (more supply) - prices have collapsed.

Note: the oil gusher continues ...

Best wishes to all.