RSS Feed

RSS Feed by Calculated Risk on 3/19/2007 01:05:00 PM

Monday, March 19, 2007

Builder Confidence Declines in March

Click on graph for larger image.

Click on graph for larger image.

UPDATE: NABH Press Release: Builder Confidence Slips In March

Builder confidence in the market for new single-family homes receded in March, largely on concerns about deepening problems in the subprime mortgage arena, according to the National Association of Home Builders/Wells Fargo Housing Market Index (HMI), released today. After rising fairly steadily since its recent low last September, the HMI declined three points from a downwardly revised 39 reading in February to 36 in March.

“Builders are uncertain about the consequences of tightening mortgage lending standards for their home sales down the line, and some are already seeing effects of the subprime shakeout on current sales activity,” said NAHB Chief Economist David Seiders. “The fundamentals of today’s housing market still are relatively strong, including a favorable interest-rate structure, solid growth in employment and household income, lower energy prices and improving affordability in much of the single-family market – due in part to price cuts and non-price sales incentives offered by builders. NAHB continues to forecast modest improvements in home sales during the balance of 2007, although the problems in the mortgage market increase the degree of uncertainty surrounding our baseline (i.e., most probable) forecast.”

Derived from a monthly survey that NAHB has been conducting for 20 years, the NAHB/Wells Fargo HMI gauges builder perceptions of current single-family home sales and sales expectations for the next six months as either “good,” “fair” or “poor.” The survey also asks builders to rate traffic of prospective buyers as either “high to very high,” “average” or “low to very low.” Scores for each component are then used to calculate a seasonally adjusted index where any number over 50 indicates that more builders view sales conditions as good than poor.

All three component indexes registered declines in March after having risen in the previous month. The index gauging current single-family home sales and the index gauging sales expectations for the next six months each declined three points, to 37 and 50, respectively. Meanwhile, the index gauging traffic of prospective buyers declined a single point, to 28.

Regionally, the HMI results were somewhat mixed. In the Midwest and West, the index gained one point to 28 and 36, respectively. In the Northeast, the HMI declined two points to 41, and in the South, it fell four points to 40.

Fremont General Gives Notice to Mortgage Staff

by Calculated Risk on 3/19/2007 12:26:00 PM

From Bloomberg (hat tip Brian): Fremont General Gives Mortgage Staff Two-Month Dismissal Notice

Fremont General Corp., the California thrift trying to sell its home-lending business, told the unit's staff they may be dismissed in two months.

...

"The company has aggressively been pursuing its options," Walker said. "Such efforts continue, although the company cannot provide more definitive information today."

...

California requires employers to give workers 60 days notice before "a plant closing or mass layoff," according to the state Employment Development Department's Web site.

First American Study on Foreclosures

by Calculated Risk on 3/19/2007 11:54:00 AM

From the OC Register: Homeowners face foreclosure

The United States likely will see 1.1 million foreclosures during the next six to seven years on adjustable-rate mortgages issued when home prices were at or near the peak of the market, a study released today by First American Corp. of Santa Ana says.Compare this to the Center for Responsible Lending report: Losing Ground: Foreclosures in the Subprime Market and Their Cost to Homeowners.

As a result, lenders will end up losing about $112.5 billion.

But that probably won't have a significant impact on the economy or the mortgage industry since the loss equals less than 1 percent of the $12 trillion in home loans projected for the next six years, the study said.

"This is not going to break the economy," said study author Christopher Cagen, director of research and analytics at First American CoreLogic, a First American company. "It's less than the price of alcohol. It's less than the price of gasoline going up to $3.25 a gallon. ... It's part of the business cycle and it's not going to be dominant."

"... foreclosure rates will increase significantly in many markets as housing appreciation slows or reverses. As a result, we project that 2.2 million borrowers will lose their homes ...I'm trying to find the First American study.

...

We project that one out of five (19 percent) subprime mortgages originated during the past two years will end in foreclosure. This rate is nearly double the projected rate of subprime loans made in 2002, and it exceeds the worst foreclosure experience in the modern mortgage market, which occurred during the “Oil Patch” disaster of the 1980s."

Sunday, March 18, 2007

Commercial Bank Exposure to Real Estate

by Calculated Risk on 3/18/2007 04:18:00 PM

Professor Kash had an interesting post on Friday: Bad Loans, Banks, and the Coming Credit Crunch Kash is trying to look at the incipient credit crunch from the bank's perspective.

"I've been thinking about the health of the banking sector of the US economy, and pulled together a couple of charts that have gotten me thinking. And worried."Check out Kash's post and graphs.

Kash presented the loan amounts in real terms. The following graph shows the loan amounts as a percent of GDP (Q1 2007 estimated).

Click on graph for larger image.

Click on graph for larger image.This graph shows the rapid increase in real estate loans. This category includes all loans collateralized by real estate, and includes residential, commercial and real estate construction and development loans.

The banking sector is clearly exposed to real estate, although the breakdown between residential and commercial isn't available.

Note: Commercial and industry (C&I) bank borrowing has risen recently as a percent of GDP, but the level is still low compared to historical norms. However this is bank loans only, and doesn't include any bonds. I'll have more on consumer borrowing soon.

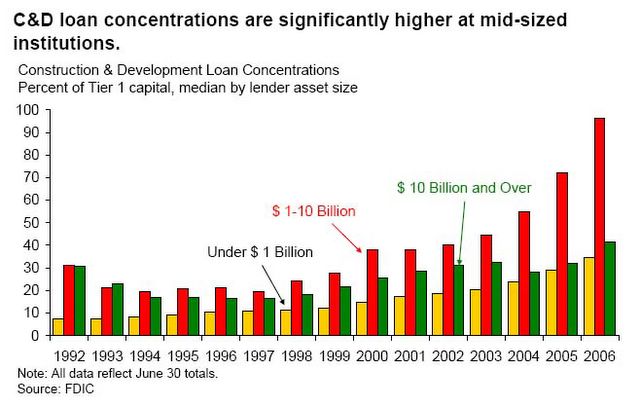

We know, from the FDIC Semiannual Report that the concentration of CRE and C&D loans has increased:

Small and mid-size institutions have been increasing their concentrations in riskier assets, such as CRE loans and construction and development (C&D) loans. This suggests that, although small and mid-size institutions have been more successful in limiting the erosion of their nominal NIMs, they have achieved this success in part by assuming higher levels of credit risk.

... continued increases in concentrations and reports of loosened underwriting standards at FDIC-insured institutions signal the potential for future credit quality deterioration. In addition, regulators have noted increasing C&D and overall CRE loanThe housing crisis is now front page news, but there is little discussion about U.S. bank exposure to CRE loans. If a CRE slump follows the residential real estate bust (the typical historical pattern), then the U.S. commercial banks might have a serious problem.

concentrations, especially at institutions with total assets between $1 billion and $10 billion.

Currently delinquency rates are very low for CRE loans. But when times are tough, CRE loans usually have the highest overall delinquency rates.

Currently delinquency rates are very low for CRE loans. But when times are tough, CRE loans usually have the highest overall delinquency rates.I understand why Kash is thinking about this issue ... and why he is worried.

Tanta on FICO "Inflation"

by Calculated Risk on 3/18/2007 02:47:00 AM

From CR: At the OC Register, Mathew Padilla interviews Glenn Stearns of Stearns Lending. Here is an excerpt:

Stearns also said there has been an inflation in credit scores, known as FICO scores. He said some consumers with a maximum of $3,000 in credit had a FICO of 700, which generally is considered a good score. Such a first-time buyer had no proven history of making a house payment, he said. In his own business, he said customers that went into default tended to have credit scores greater than 700.This makes it sound like FICO scores are undergoing a process like “grade inflation” in college. Tanta explains that the problem isn't with the FICO score itself, but that using the FICO score alone is insufficient for first time homebuyers.

“Everyone is having to rethink credit scores,” he said.

The following is from Tanta:

Some of us (OldFart Mortgage, LTD) used to require a first-time homebuyer to have a 24-month rental history, and to verify that with a direct verification from the landlord or property management company. First, we would make sure that the borrower had a history of making housing (not “house”) payments on time. Then, we would calculate the borrower’s current housing expense as a ratio to gross monthly income, and compare it to the borrower’s proposed monthly housing expense (including taxes and insurance). The result of this comparison is actually what old-timers mean by the term “payment shock.” (The term for potential future issues on an ARM was “rate shock”; the press has completely muddled the terms now so much that it’s hopeless.) Anyway, the traditional rule of thumb was that a first-time homebuyer was limited to a proposed house payment no more than 150% of the current housing (rental) payment. That extra 50% allowed owning to be more expensive than rent, but also was conservative enough to allow for things like maintenance and other expenses that renters aren’t often in the habit of paying for. If you let them double their monthly housing payments, they can get into terrible trouble the first time they have to call a plumber. The theory is that second-time homebuyers have already learned this awful lesson and so they can be allowed more “shock” (as long as they still meet the total DTI max).

In any case, this verification of the rental payment history and “payment shock” test was on top of the required minimum FICO. So those borrowers described in the article—a nice pretty 700 FICO derived from one $3000 card balance—would not get the loan if they didn’t meet the other two tests. For instance, this old rule eliminated FTBs who were going straight from mom & dad’s place (or the dormitory) to a mortgage: they were ineligible because they couldn’t show a 24-month history of being responsible for their own housing costs. Ditto for someone “renting” a condo owned by the parents but not actually paying anything near a real housing cost burden. I used to get those “kiddie condo” deals a lot when I worked for a lender with branches in a college town.

In my view, it is among the most irresponsible of the irresponsible lending we’ve seen lately that FTB rules were relaxed to allow either 1) no history of making one’s own rental payments required or 2) not counting late rental payments as a reduction to FICO (they won’t affect the FICO if the landlord doesn’t report to the credit bureau, and small-time property owners don’t) or 3) the payment shock limit was increased to 200% or more.

That said, it’s not so much that FICOs get “inflated,” it’s that their importance to the loan qualification process is inflated. For anyone who has already owned a home, the mortgage payment history is already taken into account in the FICO (because mortgage servicers report to the bureaus). But first-timers present a cautionary tale in not letting the FICO bear more weight in your decision than it should.

I’m sure that’s probably what the guy in the newspaper meant, but as usual, the newspaper only deals in sound bites, so my version is just the one that shows the work as well as the answer, as it were. There are some other issues a lot of us have with FICOs; they can in some cases “reward” heavy debt users over limited debt users. That’s why a sane underwriter (yeah, right) reads the credit report instead of just looking at the FICO. The other side of this, you see, is that the borrower with $3000 on the cards might have a FICO of 700, but the borrower with $8000 on the cards might have a FICO of 750 (because that person’s credit record is older, or has more tradelines—the $8000 is split over three cards instead of one, and the more trades you have, generally, the higher your score until you get to the point where you’re maxed out). So just having stricter FICO rules for FTBs would end up setting the very perverse incentive of encouraging them to get into a lot of consumer debt so they can prove they’re good enough to get a home. I would rather go back to the (“inefficient”) old days where we used FICOs, but only as a guideline that had to be backed up with other considerations, positive and negative. I certainly don’t want to see young borrowers locked out of mortgage credit because they don’t have enough plastic in their wallets or because they bought an old beater for cash instead of taking out a car loan or lease for something new, for the love of Peat. But I fear that’s the message some of them have gotten.

And that gets us back to my long-standing problem with subprime lending becoming predatory lending. A lot of folk end up in subprime because they don’t have access to the kind of credit that would improve their FICOs enough to get them into prime. If you come from the side of town where the available credit is mostly payday lenders or rent-to-own stores—who don’t report to the bureaus—you are not only getting screwed on whatever borrowing you’re currently doing, because the rates are just usurious, you’re also screwed because paying those cruddy rates in a timely fashion doesn’t offer the reward of a good FICO score. My solution to a lot of the predatory lending problem is to make sure that depositories are offering “entry level” credit to low-to-moderate income people, including young people. If the banks get ahold of them before the sleazy credit card mailers or the local loan sharks do, they can get some debt experience in a safer and sounder manner. But some banks seem to have taken the position that they’ll let Providian or the local loan shark take the risk on entry level borrowers, and then they’ll pick out the few survivors for their prime loans, while putting the others into those high-yield subprime loans. When we focus exclusively on borrower behavior, without looking at lender behavior, we get a skewed view of how you “create” a subprime borrower in the first place.