RSS Feed

RSS Feed by Calculated Risk on 9/18/2024 07:29:00 PM

Wednesday, September 18, 2024

Thursday: Unemployment Claims, Philly Fed Mfg, Existing Home Sales

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 235 thousand initial claims, up from 230 thousand last week.

• Also at 8:30 AM, the Philly Fed manufacturing survey for September. The consensus is for a reading of 2.0, up from -7.0.

• At 10:00 AM, Existing Home Sales for August from the National Association of Realtors (NAR). The consensus is for 3.85 million SAAR, down from 3.95 million in July.

FOMC Projections

by Calculated Risk on 9/18/2024 02:12:00 PM

Statement here.

Fed Chair Powell press conference video here or on YouTube here, starting at 2:30 PM ET.

Here are the projections. Since the last projections were released, economic growth has been above expectations, the unemployment rate is slightly above expectations, and inflation lower than expected (although there are some "base effects" that might push PCE inflation up a little later this year).

In June, the FOMC participants’ midpoint of the target level for the federal funds rate was around 5.125% at the end of 2024. The FOMC participants’ midpoint of the target range is now at 4.5% at the end of 2024.

Market participants expect the target range to be around 4.25% at the end of 2024.

1 Projections of change in real GDP and inflation are from the fourth quarter of the previous year to the fourth quarter of the year indicated.

The unemployment rate was at 4.2% in August and the projections for Q4 2024 were revised up.

2 Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated.

As of July 2024, PCE inflation increased 2.5 percent year-over-year (YoY). The projections for PCE inflation were revised down.

PCE core inflation increased 2.6 percent YoY in July. The projections for core PCE inflation were about the same.

The BEA's second estimate for Q2 GDP showed real growth at 3.0% annualized, following 1.4% annualized real growth in Q1. Early estimates for Q2 GDP are around 3% annualized, however, projections for Q4 2024 were revised down slightly!

| GDP projections of Federal Reserve Governors and Reserve Bank presidents, Change in Real GDP1 | ||||

|---|---|---|---|---|

| Projection Date | 2024 | 2025 | 2026 | 2027 |

| Sept 2024 | 1.9 to 2.1 | 1.8 to 2.2 | 1.9 to 2.3 | 1.8 to 2.1 |

| June 2024 | 1.9 to 2.3 | 1.8 to 2.2 | 1.8 to 2.1 | --- |

The unemployment rate was at 4.2% in August and the projections for Q4 2024 were revised up.

| Unemployment projections of Federal Reserve Governors and Reserve Bank presidents, Unemployment Rate2 | ||||

|---|---|---|---|---|

| Projection Date | 2024 | 2025 | 2026 | 2027 |

| Sept 2024 | 4.3 to 4.4 | 4.2 to 4.5 | 4.0 to 4.4 | 4.0 to 4.4 |

| June 2024 | 3.9 to 4.2 | 3.9 to 4.3 | 3.9 to 4.3 | --- |

As of July 2024, PCE inflation increased 2.5 percent year-over-year (YoY). The projections for PCE inflation were revised down.

| Inflation projections of Federal Reserve Governors and Reserve Bank presidents, PCE Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2024 | 2025 | 2026 | 2027 |

| Sept 2024 | 2.2 to 2.4 | 2.1 to 2.2 | 2.0 | 2.0 |

| June 2024 | 2.5 to 2.9 | 2.2 to 2.4 | 2.0 to 2.1 | --- |

PCE core inflation increased 2.6 percent YoY in July. The projections for core PCE inflation were about the same.

| Core Inflation projections of Federal Reserve Governors and Reserve Bank presidents, Core Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2024 | 2025 | 2026 | 2027 |

| Sept 2024 | 2.6 to 2.7 | 2.1 to 2.3 | 2.0 | 2.0 |

| June 2024 | 2.8 to 3.0 | 2.3 to 2.4 | 2.0 to 2.1 | --- |

FOMC Statement: 50bp Rate Cut

by Calculated Risk on 9/18/2024 02:00:00 PM

Fed Chair Powell press conference video here or on YouTube here, starting at 2:30 PM ET.

FOMC Statement:

Recent indicators suggest that economic activity has continued to expand at a solid pace. Job gains have slowed, and the unemployment rate has moved up but remains low. Inflation has made further progress toward the Committee's 2 percent objective but remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee has gained greater confidence that inflation is moving sustainably toward 2 percent, and judges that the risks to achieving its employment and inflation goals are roughly in balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In light of the progress on inflation and the balance of risks, the Committee decided to lower the target range for the federal funds rate by 1/2 percentage point to 4-3/4 to 5 percent. In considering additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Lisa D. Cook; Mary C. Daly; Beth M. Hammack; Philip N. Jefferson; Adriana D. Kugler; and Christopher J. Waller. Voting against this action was Michelle W. Bowman, who preferred to lower the target range for the federal funds rate by 1/4 percentage point at this meeting.

emphasis added

AIA: Architecture Billings Declined in August; Multi-family Billings Declined for 25th Consecutive Month

by Calculated Risk on 9/18/2024 11:51:00 AM

Note: This index is a leading indicator primarily for new Commercial Real Estate (CRE) investment.

From the AIA: Architecture firm billings remained sluggish in August, as the AIA/Deltek Architecture Billings Index (ABI) score declined to 45.7

It has now been nearly two years since firms saw sustained growth. However, clients are still expressing interest in new projects, as inquiries into work have continued to increase during that period. However, those inquiries remain challenging to convert to actual new projects in the pipeline, as the value of newly signed design contracts declined for the fifth consecutive month in August.• Northeast (48.2); Midwest (46.6); South (46.8); West (45.7)

Business conditions softened in all regions of the country in August, with firms located in the West reporting the softest conditions for the second consecutive month. Billings were flat at firms located in the Northeast for the previous two months but dipped back into negative territory again this month. Firms of all specializations also saw declining billings in August, with conditions remaining particularly soft at firms with a multifamily residential specialization.

...

The ABI score is a leading economic indicator of construction activity, providing an approximately nine-to-twelve-month glimpse into the future of nonresidential construction spending activity. The score is derived from a monthly survey of architecture firms that measures the change in the number of services provided to clients.

emphasis added

• Sector index breakdown: commercial/industrial (46.6); institutional (47.4); multifamily residential (44.0)

Click on graph for larger image.

Click on graph for larger image.This graph shows the Architecture Billings Index since 1996. The index was at 45.7 in August, down from 48.2 in July. Anything below 50 indicates a decrease in demand for architects' services.

This index has indicated contraction for 22 of the last 23 months.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index usually leads CRE investment by 9 to 12 months, so this index suggests a slowdown in CRE investment into 2025.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index usually leads CRE investment by 9 to 12 months, so this index suggests a slowdown in CRE investment into 2025.

Note that multi-family billing turned down in August 2022 and has been negative for twenty-five consecutive months (with revisions). This suggests we will see a further weakness in multi-family starts.

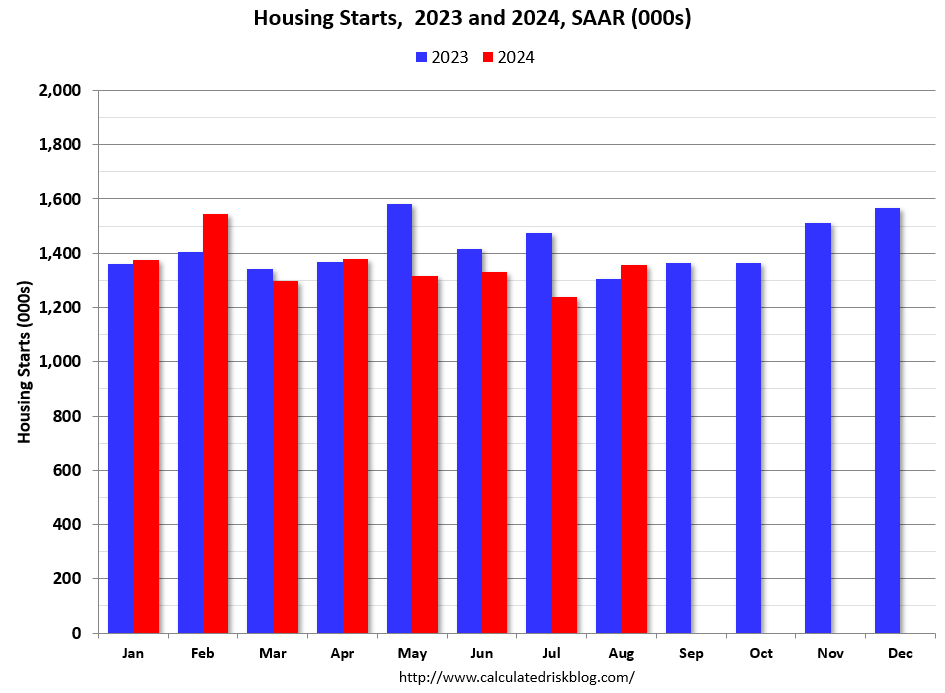

Housing Starts Increased to 1.356 million Annual Rate in August

by Calculated Risk on 9/18/2024 09:27:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Housing Starts Increased to 1.356 million Annual Rate in August

A brief excerpt:

Total housing starts in August were above expectations and starts in June and July were revised slightly. A solid report.There is much more in the article.

The third graph shows the month-to-month comparison for total starts between 2023 (blue) and 2024 (red).

Total starts were up 3.9% in August compared to August 2023.

The YoY increase in August total starts was due to an increase in both multi-family and single-family starts.

Single family starts have been up year-over-year in 12 of the last 14 months, whereas multi-family has been up year-over-year in only 2 of last 14 months. Year-to-date (YTD), total starts are down 4.0% compared to the same period in 2023. Single family starts are up 10.4% YTD, and multi-family down 32.6% YTD.

Housing Starts Increased to 1.356 million Annual Rate in August

by Calculated Risk on 9/18/2024 08:30:00 AM

From the Census Bureau: Permits, Starts and Completions

Housing Starts:

Privately-owned housing starts in August were at a seasonally adjusted annual rate of 1,356,000. This is 9.6 percent above the revised July estimate of 1,237,000 and is 3.9 percent above the August 2023 rate of 1,305,000. Single-family housing starts in August were at a rate of 992,000; this is 15.8 percent above the revised July figure of 857,000. The August rate for units in buildings with five units or more was 333,000.

Building Permits:

Privately-owned housing units authorized by building permits in August were at a seasonally adjusted annual rate of 1,475,000. This is 4.9 percent above the revised July rate of 1,406,000, but is 6.5 percent below the August 2023 rate of 1,578,000. Single-family authorizations in August were at a rate of 967,000; this is 2.8 percent above the revised July figure of 941,000. Authorizations of units in buildings with five units or more were at a rate of 451,000 in August.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows single and multi-family housing starts since 2000.

Multi-family starts (blue, 2+ units) increased in August compared to July. Multi-family starts were up 5.5% year-over-year.

Single-family starts (red) increased in August and were up 5,1% year-over-year.

The second graph shows single and multi-family housing starts since 1968.

The second graph shows single and multi-family housing starts since 1968. This shows the huge collapse following the housing bubble, and then the eventual recovery - and the recent collapse and recovery in single-family starts.

Total housing starts in August were above expectations and starts in June and July were revised slightly.

I'll have more later …

MBA: Mortgage Applications Increased in Weekly Survey

by Calculated Risk on 9/18/2024 07:00:00 AM

From the MBA: Mortgage Applications Increase in Latest MBA Weekly Survey

Mortgage applications increased 14.2 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Applications Survey for the week ending September 13, 2024. Last week’s results included an adjustment for the Labor Day holiday.

The Market Composite Index, a measure of mortgage loan application volume, increased 14.2 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 26 percent compared with the previous week. The Refinance Index increased 24 percent from the previous week and was 127 percent higher than the same week one year ago. The seasonally adjusted Purchase Index increased 5 percent from one week earlier. The unadjusted Purchase Index increased 15 percent compared with the previous week and was 0.4 percent lower than the same week one year ago.

“Application activity was up significantly last week, as market expectations of a rate cut from the Fed pulled mortgage rates lower. The 30-year fixed mortgage rate, at 6.15 percent, is now at its lowest since September 2022 and is more than a full percentage point lower than a year ago,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Refinance applications were up 24 percent – more than double last year’s pace, with both conventional and government activity jumping to the fastest pace of refinancing since 2022.”

Added Kan, “There was also an increase in purchase applications, and it is notable that conventional purchase applications increased to a pace ahead of last year, which also drove overall purchase applications very close to year-ago levels. Homebuyers are seeing improving affordability conditions, sparked by lower rates and slower home-price growth.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 6.15 percent from 6.29 percent, with points increasing to 0.56 from 0.55 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is down 0.4% year-over-year unadjusted (mostly unchanged year-over-year!).

Red is a four-week average (blue is weekly).

Purchase application activity is up about 17% from the lows in late October 2023, but still below the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

With higher mortgage rates, the refinance index declined sharply in 2022 - and mostly flat lined for two years - but has increased recently as mortgage rates declined.

Tuesday, September 17, 2024

Wednesday: Housing Starts, FOMC Announcement

by Calculated Risk on 9/17/2024 07:19:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, Housing Starts for August. The consensus is for 1.250 million SAAR, up from 1.238 million SAAR.

• During the day, The AIA's Architecture Billings Index for August (a leading indicator for commercial real estate).

• At 2:00 PM, FOMC Meeting Announcement. The Fed is expected to cut rates 25bp at this meeting.

• Also at 2:00 PM, FOMC Forecasts This will include the Federal Open Market Committee (FOMC) participants' projections of the appropriate target federal funds rate along with the quarterly economic projections.

• At 2:30 PM, Fed Chair Jerome Powell holds a press briefing following the FOMC announcement.

Lawler: Early Read on Existing Home Sales in August

by Calculated Risk on 9/17/2024 01:00:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Lawler: Early Read on Existing Home Sales in August

A brief excerpt:

From housing economist Tom Lawler:There is more in the article.

Based on publicly-available local realtor/MLS reports released across the country through today, I project that existing home sales as estimated by the National Association of Realtors ran at a seasonally adjusted annual rate of 3.88 million in August, down 1.8% from July’s preliminary pace and down 3.7% from last August’s seasonally adjusted pace. Unadjusted sales should show a slightly larger YOY % decline, as there was one fewer business day this August compared to last August.

Local realtor/MLS reports suggest that the existing single-family home sales price last month was up 3.5% from last August.

CR Note: The National Association of Realtors (NAR) is scheduled to release August Existing Home Sales on Thursday, September 19th at 10 AM ET. The consensus is for 3.85 million SAAR, down from 3.95 million in July.

NAHB: Builder Confidence Increased in September

by Calculated Risk on 9/17/2024 10:00:00 AM

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 41, up from 39 last month. Any number below 50 indicates that more builders view sales conditions as poor than good.

From the NAHB: Builder Sentiment Rises as Rates Fall but Affordability Challenges Persist

With mortgage rates declining by more than one-half of a percentage point from early August through mid-September, per Freddie Mac, builder sentiment edged higher this month even as builders continue to grapple with rising costs.

Builder confidence in the market for newly built single-family homes was 41 in September, up two points from a reading of 39 in August, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) released today. This breaks a string of four consecutive monthly declines.

“Thanks to lower interest rates, builders now have a positive view for future new home sales for the first time since May 2024,” said NAHB Chairman Carl Harris, a custom home builder from Wichita, Kan. “However, the cost of construction remains elevated relative to household budgets, holding back some enthusiasm for current housing market conditions. Moreover, builders will face competition from rising existing home inventory in many markets as the mortgage rate lock-in effect softens with lower mortgage rates.”

“With inflation moderating, the Federal Reserve is expected to begin a cycle of monetary policy easing this week, which will produce downward pressure on mortgage interest rates and also lower the interest rates on land development and home construction business loans,” said NAHB Chief Economist Robert Dietz. “Lowering the cost of construction is critical to confront persistent challenges for housing affordability.”

The latest HMI survey also revealed that the share of builders cutting prices dropped in September for the first time since April, down one point to 32%. Moreover, the average price reduction was 5%, the first time it has been below 6% since July 2022. Meanwhile, the use of sales incentives fell to 61% in September, down from 64% in August.

...

ll three HMI indices were up in September. The index charting current sales conditions rose one point to 45, the component measuring sales expectations in the next six months increased four points to 53 and the gauge charting traffic of prospective buyers posted a two-point gain to 27.

Looking at the three-month moving averages for regional HMI scores, the Northeast fell three points to 49, the Midwest edged one-point higher to 40, the South decreased one point to 41 and the West increased two points to 39.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the NAHB index since Jan 1985.

This was slightly above the consensus forecast.

Industrial Production Increased 0.8% in August

by Calculated Risk on 9/17/2024 09:15:00 AM

From the Fed: Industrial Production and Capacity Utilization

In August, industrial production rose 0.8 percent after falling 0.9 percent in July. Similarly, the output of manufacturing increased 0.9 percent in August after decreasing 0.7 percent during the previous month. This pattern was due in part to a recovery in the index of motor vehicles and parts, which jumped nearly 10 percent in August after dropping roughly 9 percent in July. The index for manufacturing excluding motor vehicles and parts moved up 0.3 percent in August. The index for mining climbed 0.8 percent, while the index for utilities was flat. At 103.1 percent of its 2017 average, total industrial production in August was the same as its year-earlier level. Capacity utilization moved up to 78.0 percent in August, a rate that is 1.7 percentage points below its long-run (1972–2023) average

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and above the level in February 2020 (pre-pandemic).

Capacity utilization at 78.0% is 1.7% below the average from 1972 to 2022. This was above consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production increased to 103.1. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

Retail Sales Increased 0.1% in August

by Calculated Risk on 9/17/2024 08:30:00 AM

On a monthly basis, retail sales increased 0.1% from July to August (seasonally adjusted), and sales were up 2.1 percent from August 2023.

From the Census Bureau report:

Advance estimates of U.S. retail and food services sales for August 2024, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $710.8 billion, an increase of 0.1 percent from the previous month, and up 2.1 percent from August 2023. ... The June 2024 to July 2024 percent change was revised from up 1.0 percent to up 1.1 percent.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline was up 0.1% in August.

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail and Food service sales, ex-gasoline, increased by 3.0% on a YoY basis.

The change in sales in August was slightly below expectations, however sales in June and July were revised up, combined.

The change in sales in August was slightly below expectations, however sales in June and July were revised up, combined.

Monday, September 16, 2024

Tuesday: Retail Sales, Industrial Production, Homebuilder Survey

by Calculated Risk on 9/16/2024 07:01:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Inch Lower to Begin Potentially Wild Week

From Matthew Graham at Mortgage News Daily: Mortgage Rates Inch Lower to Begin Potentially Wild Week

The new week began on a relatively quiet note in terms of mortgage rate movement and the underlying bond market. ... Traders have quickly shifted back to expecting slightly better odds of a 0.50% rate cut versus the minimum 0.25%. That's not even the important part of the announcement, however. Markets will be more focused on the rate trajectory outlined in the Fed's economic projections as well as the guidance offered in the text of the announcement and Fed Chair Powell's press conference. ... Any time an outcome is guaranteed to surprise about half the market, it's pretty much impossible to avoid volatility. [30 year fixed 6.12%]Tuesday:

emphasis added

• At 8:30 AM ET, Retail sales for August will be released. The consensus is for a 0.2% increase in retail sales.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for August. The consensus is for a 0.1% increase in Industrial Production, and for Capacity Utilization to increase to 77.9%.

• At 10:00 AM, The September NAHB homebuilder survey. The consensus is for a reading of 40, up from 39 in August. Any number below 50 indicates that more builders view sales conditions as poor than good.

Part 2: Current State of the Housing Market; Overview for mid-September 2024

by Calculated Risk on 9/16/2024 02:46:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Part 2: Current State of the Housing Market; Overview for mid-September 2024

A brief excerpt:

On Friday, in Part 1: Current State of the Housing Market; Overview for mid-September 2024 I reviewed home inventory, housing starts and sales.There is much more in the article.

In Part 2, I will look at house prices, mortgage rates, rents and more.

...

Other measures of house prices suggest prices will be up less YoY in the July Case-Shiller index than in the June report. The NAR reported median prices were up 4.2% YoY in July, up from 4.1% YoY in June.

ICE reported prices were up 3.6% YoY in July, down from 4.1% YoY in June, and Freddie Mac reported house prices were up 4.4% YoY in July, down from 5.2% YoY in June.

Here is a comparison of year-over-year change in the FMHPI, median house prices from the NAR, and the Case-Shiller National index.

The FMHPI and the NAR median prices appear to be leading indicators for Case-Shiller. Based on recent monthly data, and the FMHPI, the YoY change in the Case-Shiller index will likely be lower YoY in July compared to June.

Update: The Art of the Soft Landing

by Calculated Risk on 9/16/2024 01:06:00 PM

Back in June, I wrote: The Art of the Soft Landing

A few excerpts and an updated graph ...

The "Art of the Soft Landing" requires that the Fed reduce rates quick enough to keep economic growth positive, and slow enough not to reignite inflation. My view is a soft landing is achieved if growth stays positive, inflation returns to target, and the yield curve flattens or reverts to normal (long yields higher than short yields).The good news is growth has stayed positive and inflation has moved closer to the 2% target. However, the yield curve is still inverted, and we are not out of the woods yet.

Here is an updated graph of 10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity from FRED since 1976.

Here is an updated graph of 10-Year Treasury Constant Maturity Minus 2-Year Treasury Constant Maturity from FRED since 1976. The yield curve is no longer inverted. The next 6 months or so will tell the tale if the Fed reduced rates quick enough to accomplish a soft landing. That probably means the Fed Funds rate will need to be down to around 4% or so.

Q2 Update: Delinquencies, Foreclosures and REO

by Calculated Risk on 9/16/2024 11:24:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Q2 Update: Delinquencies, Foreclosures and REO

A brief excerpt:

We will NOT see a surge in foreclosures that would significantly impact house prices (as happened following the housing bubble) for two key reasons: 1) mortgage lending has been solid, and 2) most homeowners have substantial equity in their homes.There is much more in the article.

...

And on mortgage rates, here is some data from the FHFA’s National Mortgage Database showing the distribution of interest rates on closed-end, fixed-rate 1-4 family mortgages outstanding at the end of each quarter since Q1 2013 through Q1 2024 (Q2 2024 data will be released in two weeks).

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 21.9% of loans are under 3%, 57.3% are under 4%, and 76.0% are under 5%.

With substantial equity, and low mortgage rates (mostly at a fixed rates), few homeowners will have financial difficulties.

Housing Sept 16th Weekly Update: Inventory up 1.4% Week-over-week, Up 37.4% Year-over-year

by Calculated Risk on 9/16/2024 08:11:00 AM

Altos reports that active single-family inventory was up 1.4% week-over-week. Inventory is now up 44.5% from the February seasonal bottom.

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of September 13th, inventory was at 714 thousand (7-day average), compared to 704 thousand the prior week.

The second graph shows the seasonal pattern for active single-family inventory since 2015.

The red line is for 2024. The black line is for 2019.

Inventory was up 37.4% compared to the same week in 2023 (last week it was up 38.0%), and down 25.2% compared to the same week in 2019 (last week it was down 25.7%).

Back in June 2023, inventory was down almost 54% compared to 2019, so the gap to more normal inventory levels is slowly closing.

Mike Simonsen discusses this data regularly on Youtube.

Sunday, September 15, 2024

Sunday Night Futures

by Calculated Risk on 9/15/2024 06:52:00 PM

Weekend:

• Schedule for Week of September 15, 2024

• FOMC Preview: Fed to Cut Rates

Monday:

• 8:30 AM ET: The New York Fed Empire State manufacturing survey for September. The consensus is for a reading of -4.0, up from -4.7.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up 5 and DOW futures are up 69 (fair value).

Oil prices were up over the last week with WTI futures at $68.65 per barrel and Brent at $71.61 per barrel. A year ago, WTI was at $91, and Brent was at $96 - so WTI oil prices are down about 25% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.13 per gallon. A year ago, prices were at $3.85 per gallon, so gasoline prices are down $0.72 year-over-year.

FOMC Preview: Fed to Cut Rates

by Calculated Risk on 9/15/2024 10:17:00 AM

Most analysts expect the FOMC will cut the federal funds rate at the meeting this week by 25bp lowering the target range to 5 to 5-1/4 percent. It is possible the FOMC will cut by 50bp.

Currently market participants are split evenly between a 25bp and a 50bp cut this week. Market participants are also pricing in a total of 75bp in cuts by the November meeting, and between 100bp to 125bp in cuts by December.

From BofA:

Next week, the Fed is widely expected to end the longest hold after a hiking cycle in its history (Exhibit 1).

We look for the Fed to cut rates by 25bp, which should kick off a series of 25bp cuts over the next five meetings. Markets still perceive a meaningful risk of a 50bp cut next week, but this week’s data leave us comfortable with our 25bp call. The main message from the meeting should be one of cautious optimism despite greater concerns over downside risks.

emphasis added

Projections will be released at this meeting. For review, here are the June projections.

The BEA's second estimate for Q2 GDP showed real growth at 3.0% annualized, following 1.4% annualized real growth in Q1. Current estimates for Q3 GDP are around 2.5%. That puts real growth in the first 3 quarters at the top end of the June FOMC projections.

| GDP projections of Federal Reserve Governors and Reserve Bank presidents, Change in Real GDP1 | ||||

|---|---|---|---|---|

| Projection Date | 2024 | 2025 | 2026 | |

| June 2024 | 1.9 to 2.3 | 1.8 to 2.2 | 1.8 to 2.1 | |

| Mar 2024 | 2.0 to 2.4 | 1.9 to 2.3 | 1.8 to 2.1 | |

The unemployment rate was at 4.2% in August. This is at the high end of the June projections.

| Unemployment projections of Federal Reserve Governors and Reserve Bank presidents, Unemployment Rate2 | ||||

|---|---|---|---|---|

| Projection Date | 2024 | 2025 | 2026 | |

| June 2024 | 3.9 to 4.2 | 3.9 to 4.3 | 3.9 to 4.3 | |

| Mar 2024 | 3.9 to 4.1 | 3.9 to 4.2 | 3.9 to 4.3 | |

As of July 2024, PCE inflation increased 2.5 percent year-over-year (YoY). This is at the low end of the June projections. Current analyst estimates are that PCE inflation will fall to 2.3% YoY in August.

| Inflation projections of Federal Reserve Governors and Reserve Bank presidents, PCE Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2024 | 2025 | 2026 | |

| June 2024 | 2.5 to 2.9 | 2.2 to 2.4 | 2.0 to 2.1 | |

| Mar 2024 | 2.3 to 2.7 | 2.1 to 2.2 | 2.0 to 2.1 | |

PCE core inflation increased 2.6 percent YoY in July. This is lower than the June FOMC projections for Q4, although analysts expect core PCE inflation to tick up slightly in August.

| Core Inflation projections of Federal Reserve Governors and Reserve Bank presidents, Core Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2024 | 2025 | 2026 | |

| June 2024 | 2.8 to 3.0 | 2.3 to 2.4 | 2.0 to 2.1 | |

| Mar 2024 | 2.5 to 2.8 | 2.1 to 2.3 | 2.0 to 2.1 | |

Saturday, September 14, 2024

Real Estate Newsletter Articles this Week: The "Home ATM" Mostly Closed in Q2

by Calculated Risk on 9/14/2024 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Part 1: Current State of the Housing Market; Overview for mid-September 2024

• The "Home ATM" Mostly Closed in Q2

• 2nd Look at Local Housing Markets in August

• Asking Rents Mostly Unchanged Year-over-year

• ICE Mortgage Monitor: House Price Growth Slows, Inventory Surges in Florida and Texas

• 1st Look at Local Housing Markets in August

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.