RSS Feed

RSS Feed by Calculated Risk on 7/07/2010 04:53:00 PM

Wednesday, July 07, 2010

European Bank Stress Test: 91 Banks, results on July 23rd

From the Committee of European Banking Supervisors (CEBS) Key Features of the extended EU-wide Stress Test

The objective of the extended stress test exercise is to assess the overall resilience of the EU banking sector and the banks’ ability to absorb further possible shocks on credit and market risks, including sovereign risks, and to assess the current dependence on public support measures.The document has a list of the 91 banks.

The exercise is being conducted on a bank-by-bank basis using commonly agreed macro-economic scenarios (baseline and adverse) for 2010 and 2011, developed in close cooperation with the ECB and the European Commission.

...

On aggregate, the adverse scenario assumes a 3 percentage point deviation of GDP for the EU compared to the European Commission’s forecasts over the two-year time horizon. The sovereign risk shock in the EU represents a deterioration of market conditions as compared to the situation observed in early May 2010.

...

The results of the stress test will be disclosed, both on an aggregated and on a bank-by-bank basis, on 23 July 2010.

More from Bloomberg: EU Stress Tests Will Cover 91 Banks, Assume Bond Drop

Real Estate Sign of the Times: "Price Reduced"

by Calculated Risk on 7/07/2010 01:25:00 PM

I see "Priced Reduced" on many For Sale signs these days ...

From Thomas Grillo at the Boston Herald: Boston sellers cut prices (ht StickyDownside)

There’s a silver lining for would-be home buyers who missed the April 30 deadline for the $8,000 federal tax credit: Sellers are dropping prices.Also these price reductions are one of the key reasons why a number of deals didn't close by June 30th - the deals just wouldn't appraise at the agreed upon price because identical units are now being offered for less.

The average price reduction for a single-family home or condominium in the Bay State last month was 8 percent, or $38,883 off the original asking price, according to real estate search engine Trulia.com.

In Suffolk County, which includes the cities of Boston, Chelsea, Revere and Winthrop, the price reduction was $43,288, or 7 percent off the listing price.

Falling Mortgage Rates and Refi Mini-Boom

by Calculated Risk on 7/07/2010 09:50:00 AM

The Mortgage Bankers Association reported this morning that refinance activity increased again:

The Refinance Index increased 9.2 percent from the previous week and is the highest Refinance Index observed in the survey since the week ending May 15, 2009.

...

The refinance share of mortgage activity increased to 78.7 percent of total applications from 76.8 percent the previous week, which is the highest refinance share observed in the survey since April 2009.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the monthly MBA refinance index (Blue) and mortgage rates from the Freddie Mac Primary Mortgage Market Survey - and the Fed Funds target rate since Jan 1990.

Even with the recent decline in mortgage rates, refinance activity is still well below the peak in 2009. The reason is the 30 year mortgage rate is only slightly below the rates of April and May 2010 (4.6% now compared to just over 4.8% in 2009), so for those who refinanced last year there isn't much incentive to refinance now (considering the cost to refinance).

Of course many homeowners can't refinance because they owe more than their homes are worth, or their incomes have declined and they can't qualify.

MBA: Mortgage Purchase Applications Decrease, Refis increase

by Calculated Risk on 7/07/2010 07:21:00 AM

The MBA reports: Mortgage Refinance Applications Increase in Latest MBA Weekly Survey

The Refinance Index increased 9.2 percent from the previous week and is the highest Refinance Index observed in the survey since the week ending May 15, 2009. The seasonally adjusted Purchase Index decreased 2.0 percent from one week earlier. The Purchase Index has decreased eight of the last nine weeks.

...

“Mortgage rates remained near record lows last week, as incoming data on the job and housing markets were weaker than anticipated. As more homeowners locked in to these low rates, the level of refinance applications increased to a new 13-month high,” said Michael Fratantoni, MBA’s Vice President of Research and Economics. “For the month of June, purchase applications declined almost 15 percent relative to the prior month, and were down more than 30 percent compared to April, the last month in which buyers were eligible for the tax credit.”

...

The average contract interest rate for 30-year fixed-rate mortgages increased to 4.68 percent from 4.67 percent, with points decreasing to 0.86 from 0.96 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the MBA Purchase Index and four week moving average since 1990.

There has been a mini-refi boom because of the low mortgage rates, but the purchase index has fallen sharply to the levels of 1996.

Tuesday, July 06, 2010

Reis: Mall Vacancy Rate rises in Q2

by Calculated Risk on 7/06/2010 11:59:00 PM

Click on graph for larger image in new window.

Click on graph for larger image in new window.

From Reuters: US shopping center vacancy rates rose in 2nd qtr

For U.S. strip centers, the vacancy rate in the second quarter rose ... to 10.9 percent, slightly below the 11 percent in 1991 during the prior real estate bust ...At regional malls, the vacancy rate rose to 9.0% - the highest since Reis starts tracking regional malls in 2000. The record vacancy rate for strip malls was in 1990 at 11.1%.

"Until we see stabilization and recovery take root in both consumer spending and business spending and employment, we do not foresee a recovery in the retail sector until late 2012 at the earliest," said Victor Calanog, Reis director of research.

Update on FHA Seller Concessions

by Calculated Risk on 7/06/2010 06:53:00 PM

Early this year, the FHA announced a proposal to reduce allowable seller concessions from 6% to 3%.

David H. Stevens, Assistant Secretary of Housing and FHA Commissioner, discussed the reasons for this proposal in May:

We are also proposing a third policy measure to reduce the maximum permissible seller concession from its current 6 percent level to 3 percent, which is in line with industry norms. The current level exposes the FHA to excess risk by creating incentives to inflate appraised value. ... FHA's experience shows that loans with high levels of seller concessions are significantly more likely to go to claim. Experience to-date on loans insured from FY 2003 to FY 2008 suggests that claim rates on high-concession loans are 50 percent higher or more than those on low-concession loans.I was told by the FHA today that a notice for public comment would be announced "VERY shortly". (I'm guessing that means in the next few weeks - if not this week).

The notice will be posted in the Federal Register, and will go into effect after a 30-day comment period.

LPS: Mortgage Delinquencies and Foreclosures increase to 12.38% in May

by Calculated Risk on 7/06/2010 03:19:00 PM

From Lender Processing Services: LPS' May Mortgage Monitor Report: Increase in Rate of New Delinquencies; Decline in Number of Delinquent Loans Becoming Current

The May Mortgage Monitor report released today by Lender Processing Services, Inc. ... shows a 2.3 percent month-over-month increase in the nation's home loan delinquency rate to 9.2 percent in May 2010, and that early-stage delinquencies are increasing as normal seasonal improvements taper off. This report includes data as of May 31, 2010.LPS shows 9.2% delinquent and another 3.18% in foreclosure for a total of 12.38%. I'm not sure about the days to foreclosure numbers (other sources show fewer), but they have steadily increased. For delinquency rates I usually use the quarterly report from the MBA.

According to the Mortgage Monitor report, the percentage of mortgage loans in default beyond 90 days increased slightly, while both delinquency and foreclosure rates continue to remain relatively stable at historically high levels. There are currently more than 7.3 million loans currently in some stage of delinquency or REO.

The report also shows that the average number of days for a loan to move from 30-days delinquent to foreclosure sale continues to increase, and is now at an all-time high of 449 days, resulting in an increase in "shadow" foreclosure inventory.

Here is the LPS monthly report. The increase in early stage delinquencies might be seasonal, but it is definitely bad news. And what happens when house prices start falling again later this year as I expect?

For more, from Diana Golobay at HousingWire: National Mortgage Delinquency Rate Swells to 9.2% in May: LPS

And from Diana Olick at CNBC: New Loan Delinquencies on the Rise Again

Older, more educated workers, have highest length of unemployment

by Calculated Risk on 7/06/2010 12:37:00 PM

Reader Ann (retired lawyer with economics degree) has obtained some publicly available raw data on the long term unemployed from the BLS Current Population Survey. Ann was able to break down the long term unemployed into two age cohorts, 1) 25 to 45, and 2) 45+.

She also broke down the data by four levels of education: 1) no high school degree, 2) high school only, 3) some college or Associates degree, and 4) BA degree or higher.

The following table summarizes the data (click on link to see table - it doesn't fit here):

Table Long Term Unemployed

(1) This includes all who have some college classes but no degree or certificate, those with certificates and those with an associates. Only 30%+/- of the “some college” group has an associates. There is not statistically significant difference in their average length of unemployment as between the ‘few classes’ or ‘certificate’ and an associates..

(2) I do not have the breakdown of all the unemployed by age combined with education. I only have that data for the long-term unemployed.

The first finding is not too surprising for the longer term unemployed:

The 2nd finding is a more surprising:

For the long term unemployed, it is better to be younger - and have less education.

Ann adds these comments:

More education = longer unemployment if the job is lost. The upside is the more educated the worker, the less likely they are to lose their job, but the downside of being more educated is that once they hit 45 if they lose their job, they are toast.It is tough to find a job, especially if you are older and better educated.

So what does one do with the over-45s with a BA or higher? ... The current mantra is 'more education is good for you' but this shows that it can, in the long run, hurt you.

ISM Non-Manufacturing Index shows slower expansion in June

by Calculated Risk on 7/06/2010 10:00:00 AM

The June ISM Non-manufacturing index was at 53.8%, down from 55.4% in May - and below expectations of 55. The employment index showed contraction in June at 49.7%. Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

The employment index is showing contraction again after one month of expansion.

From the Institute for Supply Management: June 2010 Non-Manufacturing ISM Report On Business®

Economic activity in the non-manufacturing sector grew in June for the sixth consecutive month, say the nation's purchasing and supply executives in the latest Non-Manufacturing ISM Report On Business®.

The report was issued today by Anthony Nieves, C.P.M., CFPM, chair of the Institute for Supply Management™ Non-Manufacturing Business Survey Committee; and senior vice president — supply management for Hilton Worldwide. "The NMI (Non-Manufacturing Index) registered 53.8 percent in June, 1.6 percentage points lower than the 55.4 percent registered in May, indicating continued growth in the non-manufacturing sector, but at a slightly slower rate. The Non-Manufacturing Business Activity Index decreased 3 percentage points to 58.1 percent, reflecting growth for the seventh consecutive month. The New Orders Index decreased 2.7 percentage points to 54.4 percent, and the Employment Index decreased 0.7 percentage point to 49.7 percent, reflecting contraction after one month of growth. The Prices Index decreased 6.8 percentage points to 53.8 percent in June, indicating that prices are still increasing but at a slower rate than in May. According to the NMI, 15 non-manufacturing industries reported growth in June. Respondents' comments are mostly positive about business conditions; however, there is concern about the effect of employment on the economic recovery."

emphasis added

Reis: U.S. Office Vacancy Rate at 17 year high

by Calculated Risk on 7/06/2010 08:23:00 AM

Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the office vacancy rate starting 1991.

Reis is reporting the vacancy rate rose to 17.4% in Q1 2010, up from a revised 17.3% in Q1 (revised up from 17.2%), and up from 16.0% in Q2 2009. The peak following the previous recession was 16.9%.

From Bloomberg Office Vacancy Rate in U.S. Climbs to 17-Year High, Reis Says

The vacancy rate climbed to 17.4 percent from 16 percent a year earlier and 17.3 percent in the first quarter, the New York-based research company said today in a statement. Effective rents, the amount tenants actually pay landlords, fell 5.7 percent from a year earlier and 0.9 percent from the previous three months, according to Reis.It appears the rate of increases has slowed.

Reis should release the Mall and Apartment vacancy rates over the next few days, and those will probably be at record levels.

Monday, July 05, 2010

Rogoff sees "Collapse" in China's Property Market

by Calculated Risk on 7/05/2010 08:29:00 PM

From Bloomberg: China Property Market Beginning Collapse That May Hit Banks, Rogoff Says (ht jb)

“You’re starting to see that collapse in property and it’s going to hit the banking system,” [Kenneth Rogoff, Harvard University professor and former chief economist of the IMF] said today [in an interview with Bloomberg Television in Hong Kong].It appears Rogoff is talking about a "collapse" in sales, but price frequently follows volume in real estate - so perhaps he is also talking about a steep decline in prices.

...

He also said that while recoveries across the global economy are “very slow,” the danger of a return to recession isn’t “elevated.”

Note: Here is the weekly summary and a look ahead (with plenty of graphs from last week).

The Nikkei is off about 1.5% in early trading.

And from CNBC: Pre-Market Data shows the S&P 500 off over 1% (close to breaking under 1000) and Dow futures are off about 110 points.

Best to all.

More on the slowdown in China

by Calculated Risk on 7/05/2010 03:58:00 PM

Just a follow up to the previous posts on oil prices and the 2nd half slowdown ...

From Bloomberg: China Car Sales Grow at Slower Pace; Services Index Slides to 15-Month Low (ht Paulo)

China’s auto sales grew at a slower pace in June and a services-industry index slid to a 15-month low, adding to signs that the economy leading the world recovery is cooling.Slowing in China is just one of the 2nd half stories - there is also less stimulus spending, state and local government cutbacks, more household saving impacting consumption, another downturn in housing, and a slowdown and financial issues in Europe.

Passenger-car purchases rose 10.9 percent from a year earlier, down from May’s 25 percent gain, the China Automotive Technology & Research Center said today. The services-industry measure fell to 55.6 from 56.4, HSBC Holdings Plc and Markit Economics said in an e-mailed statement.

On the flip side, Yahoo had a headline this morning: 8 Problems That Could Trigger a Double-Dip Recession (ht Brian). Brian joked that this might be a new contrary indicator (like the old magazine cover indicator).

Update on Oil Prices

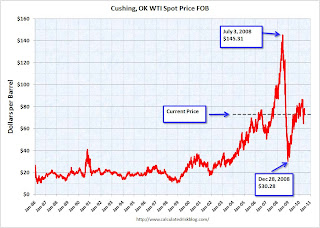

by Calculated Risk on 7/05/2010 01:21:00 PM

With the weakness in the US and European economies, and an apparent slowdown in China, it might be time to look at oil prices ... Click on graph for larger image in new window.

Click on graph for larger image in new window.

These are spot prices for Cushing WTI from the EIA (source).

Back in the Spring of 2008, we started seeing many signs of potential demand destruction - including fewer U.S miles driven, Asian countries reducing gasoline subsidies, and China stock piling oil for the Olympics. That was a pretty clear sign that oil prices would fall after China stopped stock piling oil.

So far miles driven have been increasing slowly (although the most recent data is for April, and there may be more weakness in June). And once again the Shanghai stock market is suggesting a slowdown in China. Not a clear sign like in 2008, but something to watch.

Europe: Austerity or "rigorous fiscal policies"?

by Calculated Risk on 7/05/2010 08:57:00 AM

A couple of quotes from the WSJ: Lagarde: Banks Will Pass Stress Tests

"There is no choice between austerity and stimulus," [Finance Minister Christine Lagarde] said at an economic conference in Aix-en-Provence. "Our policy is a subtle mix between growth-friendly spending cuts and letting play out the remainder of our stimulus package," she said.Paul Krugman disagrees: Plan XVII For Europe

...

"We are in a period when we have to manage budgets very cautiously. ... You may call that austerity if you want, I call this rigorous fiscal policies," [European Central Bank President Jean-Claude Trichet] told reporters on the sidelines of an economic conference in southern France.

"If you want sustainable growth, then you have to restore confidence and to do that you need to have balanced and sustainable fiscal policies in place," he added

Sunday, July 04, 2010

Happy July 4th

by Calculated Risk on 7/04/2010 11:02:00 PM

Two earlier posts:

The National Mall in D.C. July 4th, 2010. Best to all!

Investors buying foreclosures in Phoenix

by Calculated Risk on 7/04/2010 05:22:00 PM

Here is an article from the AP about investors buying foreclosures in the Phoenix area: Finding gold in them thar foreclosures (ht Ian).

I can add a little to this story: I know of an individual investor (through a close friend) in the Phoenix area who has bought almost 100 homes over the last 18 months. The investor has shared with me his portfolio. He has only bought single family homes, no condos. His average purchase price was under $35,000 and most of the homes are 3 br / 2 ba.

He is renting the homes, many by the room. Yeah, they sound like flophouses! The investor is starting to have a vacancy problem that he attributes to the new Arizona immigration law that takes effect on July 29th.

I reviewed the public records of some of the homes this investor bought - as an example he bought a 3 br / 2 ba 1,200 sq ft home for about $35,000 a couple of months ago - and that is about the average for the homes he has been buying. Very basic, dirt yards ... not the best area.

He paid in the low $20,000s for a home he bought last summer that sold for over $180,000 in 2006! That is almost 90% off the peak price (the house sold for $62,000 in 2004, so I'm guessing fraud in 2006 - and maybe in 2004 too).

Note: all numbers changed a little - the investor wants to remain anonymous.

Weekly Summary and a Look Ahead

by Calculated Risk on 7/04/2010 11:45:00 AM

This will be a light week for US economic data. The US stock markets will be closed on Monday to observe Independence Day.

Sometime this week, Reis will release the Q2 mall, office and apartment vacancy rates. In Q1, Reis reported the strip mall vacancy rate hit 10.8% (highest since 1991), the apartment vacancy rate was at a record 8% (large cities only), and the office vacancy rate rose to rose to 17.2% (highest since the early '90s).

On Tuesday, the June ISM non-manufacturing report will be released. Consensus is for a decrease to 55.0 from 55.4 in the service sector.

On Wednesday, the MBA will release the mortgage purchase applications index. This has been falling sharply after the expiration of the home buyer tax credit. Also on Wednesday, Minneapolis Fed President Narayan Kocherlakota will speak at the Université de Montréal at 3:30 PM ET (Society for Economic Dynamics).

On Thursday, the initial weekly unemployment claims will be released. Consensus is for a decline to 465K from 472K last week. Also on Thursday, the Fed will release Consumer Credit for May at 3 PM ET. Consumer credit has declined sharply since mid-2008, especially revolving debt (credit cards).

Also on Thursday, at 6 PM ET, Professor Robert Hall, the current Chairman of NBER, will speak at the Society for Economic Dynamics: “Reconsidering the Basic Tenets of Macroeconomics in the Light of the Past Two Years”. He might be asked about the possibility of a “double dip” recession.

On Friday the Census Bureau will release Wholesale Inventories for May, and the FDIC will probably get back to work ...

A couple of posts on the 2nd half:

And a summary of last week:

1) Total nonfarm payroll employment declined by 125,000 in June

2) Census 2010 hiring decreased 225,000 in June.

3) So non-farm payroll employment increased 100,000 in June ex-Census. Private-sector payroll employment increased by 83,000.

4) The unemployment rate declined down to 9.5 percent as the participation rate fell (workers leaving the workforce pushed down the unemployment rate).

5) Average hourly wages and average hours worked decreased.

Overall this was a weak report. Here are a few graphs ...

Percent Job Losses During Recessions, aligned at Bottom

Click on graph for larger image.

Click on graph for larger image.This graph shows the job losses from the start of the employment recession, in percentage terms - aligned at the bottom of the recession.

The dotted line shows the impact of Census hiring. In June, there were 339,000 temporary 2010 Census workers on the payroll. The number of Census workers will continue to decline - and the gap between the solid and dashed red lines will be mostly closed in three or four months.

Employment-Population Ratio

The Employment-Population ratio decreased to 58.5% in June from 58.7% in May. This had been increasing after plunging since the start of the recession, and the recovery in the Employment-Population ratio was considered a good sign - but the ratio has now decreased for two consecutive months.

This graph shows the employment-population ratio; this is the ratio of employed Americans to the adult population.

This graph shows the employment-population ratio; this is the ratio of employed Americans to the adult population.Note: the graph doesn't start at zero to better show the change.

Also the Labor Force Participation Rate decreased to 64.7% in June from 65.0% in May. This is the percentage of the working age population in the labor force. This decline is very disappointing, and the rate is well below the 66% to 67% rate that was normal over the last 20 years.

The reason the unemployment rate declined was because people left the workforce - and that is not good news. As the employment picture improves, people will return to the labor force, and that will put upward pressure on the unemployment rate.

Part Time for Economic Reasons

The number of workers only able to find part time jobs (or have had their hours cut for economic reasons) was at 8.63 million in June. This was a slight decline from May - and was a little bit of good news.

The number of workers only able to find part time jobs (or have had their hours cut for economic reasons) was at 8.63 million in June. This was a slight decline from May - and was a little bit of good news.The all time record of 9.24 million was set in October.

These workers are included in the alternate measure of labor underutilization (U-6) that was at 16.5% in June.

Unemployed over 26 Weeks

The blue line is the number of workers unemployed for 27 weeks or more. The red line is the same data as a percent of the civilian workforce.

The blue line is the number of workers unemployed for 27 weeks or more. The red line is the same data as a percent of the civilian workforce.According to the BLS, there are 6.751 million workers who have been unemployed for more than 26 weeks and still want a job. This is a record 4.39% of the civilian workforce. (note: records started in 1948). It does appear the increases are slowing ...

Based on an estimate from Autodata Corp, light vehicle sales were at a 11.08 million SAAR in June. That is up 14% from June 2009 (when sales were very low), and down 4.6% from the May sales rate.

Based on an estimate from Autodata Corp, light vehicle sales were at a 11.08 million SAAR in June. That is up 14% from June 2009 (when sales were very low), and down 4.6% from the May sales rate.This graph shows the historical light vehicle sales (seasonally adjusted annual rate) from the BEA (blue) and an estimate for June (red, light vehicle sales of 11.08 million SAAR from Autodata Corp).

This was below most forecasts of around 11.4 million SAAR.

S&P/Case-Shiller released the monthly Home Price Indices for April (actually a 3 month average).

This graph shows the nominal not seasonally adjusted Composite 10 and Composite 20 indices (the Composite 20 was started in January 2000).

This graph shows the nominal not seasonally adjusted Composite 10 and Composite 20 indices (the Composite 20 was started in January 2000).The Composite 10 index is off 29.7% from the peak, and up 0.3% in April (SA).

The Composite 20 index is off 29.0% from the peak, and up 0.4% in April (SA).

The next graph shows the price declines from the peak for each city included in S&P/Case-Shiller indices.

Prices increased (SA) in 17 of the 20 Case-Shiller cities in April (SA).

Prices increased (SA) in 17 of the 20 Case-Shiller cities in April (SA). Prices in Las Vegas are off 55.9% from the peak, and prices in Dallas only off 5.2% from the peak.

Case Shiller is reporting on the NSA data (18 cities up), and I'm using the SA data. As S&P noted, there probably was a small boost to prices from tax credit related buying, but prices will probably fall later this year.

From the BEA: Personal Income and Outlays, April 2010

The following graph shows real Personal Consumption Expenditures (PCE) through May (2005 dollars). Note that the y-axis doesn't start at zero to better show the change.

The quarterly change in PCE is based on the change from the average in one quarter, compared to the average of the preceding quarter.

The quarterly change in PCE is based on the change from the average in one quarter, compared to the average of the preceding quarter.Even with no growth in June, PCE growth in Q2 would be 2.5%. Even with the weak June data, it looks like my earlier estimate of 3% PCE growth in Q2 will be about right (maybe a little high).

Best wishes to all.

Cancellations along the Gulf: Real Estate Closings and Fireworks Displays

by Calculated Risk on 7/04/2010 08:55:00 AM

From Tom Bayles at the HeraldTribune: Home closings mired in crude. (ht Wayne in Elizabeth City) This is mostly anecdotes about canceled closings:

Coldwell Banker Residential Real Estate says that six of its 22 sales that failed to close in late May and early June were on waterfront homes and the direct result of buyer qualms about the spill.And from Bob Drogin at the LA Times: Oil spill takes boom out of holiday weekend

...

BP has received about 1,350 claims from Realtors and others who profit from the sale of real estate. Of the 583 claims from Florida, only two had been paid as of Tuesday ...

Alyssa M. Nohren, a real estate attorney with Sarasota's Icard Merrill firm, had a sale fall through this month on a home listed for about $350,000 on Sarasota Bay.

"It was an out-of-state buyer who just freaked out about the oil and was convinced the oil is coming this way and will further reduce property values," Noreen said. "I was devastated as a real estate lawyer because we were finally getting back on our feet, but what could I say? It is not going to come here? I can't say that."

Gulf beaches are bare and businesses are empty on what is usually one of the busiest weekends of the year. Alabama's Dauphin Island and Bayou La Batre have canceled fireworks displays.A tough holiday weekend.

Saturday, July 03, 2010

Condos: Post Tax Credit Price Cuts

by Calculated Risk on 7/03/2010 10:48:00 PM

From the Chicago Tribune: Price cuts mount as condos linger

A trio of condo developments — one small, one medium and one large — announced price cuts recently as the market readjusts in a post-tax credit market ...The $100,000 price decrease at Wabansia Row was from $800,000 to $700,000 (12.5%). And the other 40 unsold condos at "The Columbian"? Those prices will be reassessed next year.

Among the developments with recent price cuts is Parkside of Old Town, where prices were cut by up to 30 percent on 75 condos and up to 40 percent on 27 town homes ...

In Bucktown, Wabansia Row has dropped the price by up to $100,000 on 11 new town homes. At The Columbian, a 46-story condo tower that overlooks Grant Park and was taken over earlier this year by Fidelity Investments, prices on 20 of the remaining 60 unsold condos have been cut by an average of 25 percent.

"Price reduced" is a common sign where I live ...

Recession Dating and a "Double Dip"

by Calculated Risk on 7/03/2010 06:18:00 PM

My forecast is for U.S. economic growth to slow in the 2nd half (a sluggish and choppy recovery), but not slide into recession. However a recession is a possibility, and the following describes how NBER differentiates between a "double dip" and a new recession.

The National Bureau of Economic Research (NBER) Business Cycle Dating Committee is the recognized group for dating recessions in the U.S. It is always difficult to tell when a recession has ended, especially with a sluggish recovery. If the economy slides back into recession - a possibility right now - the NBER has to decide if it is a continuation of the previous recession, or if the new period of economic decline is a new separate recession.

This is just a technical question: for those impacted by the recession it makes no difference if it is called a "double dip" or a new recession.

Yesterday an AP story quoted Robert Hall, the current Chairman of NBER on a "double dip": So what exactly is a 'double-dip' recession?

"The idea -- hypothetical because it has yet to happen -- is that activity might rise for a period, but not far enough to complete a cycle, then fall again, and finally rise above its original level, only then completing the cycle."The closest we've seen to a "double dip" was in the early 1980s - and the NBER dated those as two separate recessions. We can use the NBER memos from that period to look for clues. From July 8, 1981 announcing the end of the 1980 recession: Business Cycle Trough Last July

The period following July 1980 will appear in the NBER chronology as an expansion. An important factor influencing that decision is that most major indicators, including real GNP, are already close to or above their previous highs.And from the January 1982 announcing the beginning of the 1981-1982 recession: Current Recession Began in July

The committee also reviewed its earlier decision that a peak of economic activity occurred in January 1980 and a trough in July 1980 and reaffirmed that decision. Although not all economic indicators had regained their 1979-80 peaks by the summer of 1981, the committee agreed that the resurgence of economic activity in the previous year clearly constituted a business cycle recovery.And from The NBER's Recession Dating Procedure

In choosing the dates of business-cycle turning points, the committee follows standard procedures to assure continuity in the chronology. Because a recession influences the economy broadly and is not confined to one sector, the committee emphasizes economy-wide measures of economic activity. The committee views real GDP as the single best measure of aggregate economic activity. ...GDP is the key measure, and the NBER actually uses two measures of GDP: 1) real GDP, and 2) real Gross Domestic Income (GDI). For a discussion on GDI, see from Fed economist Jeremy Nalewaik, “Income and Product Side Estimates of US Output Growth,” Brookings Papers on Economic Activity.

The committee places particular emphasis on two monthly measures of activity across the entire economy: (1) personal income less transfer payments, in real terms and (2) employment. In addition, the committee refers to two indicators with coverage primarily of manufacturing and goods: (3) industrial production and (4) the volume of sales of the manufacturing and wholesale-retail sectors adjusted for price changes.

Below is a look at four of the measures mentioned: real GDP (and real GDI), industrial production, employment and real personal income excluding transfer payments.

Note: The following graphs are all constructed as a percent of the peak in each indicator. This shows when the indicator has bottomed - and when the indicator has returned to the level of the previous peak. If the indicator is at a new peak, the value is 100%. On all graphs the recent recession is marked as ending in July 2009 or Q3 2009 - this is preliminary and NOT an NBER determination. GDP is quarterly, the other data is monthly.

Click on graph for larger image in new window.

Click on graph for larger image in new window.The first graph is for GDP through Q1 2010.

This is the key measure and real GDP is only 1.3% below the pre-recession peak - and real GDI 2.0% below the previous peak. GDP probably increased in Q2 too (probably at close to a 3% annualized rate), and at the end of Q2 both of these measures will be even closer to the previous peak, but not there yet.

If you look at the period between the two early '80s recessions, both real GDP and real GDI returned to pre-recession levels before declining again.

The second graph is for monthly industrial production based on data from the Federal Reserve through May.

The second graph is for monthly industrial production based on data from the Federal Reserve through May.Industrial production is still 8.1% below the pre-recession peak -and now it appears that growth is slowing in the manufacturing sector (although still expanding). Even if growth continues, it will take some time before industrial production is back to pre-recession levels.

Between the early '80s recessions, industrial production didn't quite return to pre-recession levels - but it was only about 0.5% below the previous peak.

The third graph is for employment through June.

The third graph is for employment through June.Between the two recession in the early '80s, employment returned to the pre-recession peak.

This time employment is barely off the bottom.

And the last graph is for real personal income excluding transfer payments through May. This bottomed in Sept 2009, but has only increased slightly since then and is still 6% below the pre-recession peak.

And the last graph is for real personal income excluding transfer payments through May. This bottomed in Sept 2009, but has only increased slightly since then and is still 6% below the pre-recession peak. Once again - looking back - this measure returned to the pre-recession peak between the 1980 and 1981/1982 recessions.

Based on these graphs and the NBER memos, it would seem pretty easy to date two recessions in the early '80s. However, if another recession starts this year, it will almost certainly be dated as a continuation of the "great recession" that started in 2007. If so, I'll need more blue ink to shade all my graphs ...