RSS Feed

RSS Feed by Calculated Risk on 12/05/2013 08:39:00 AM

Thursday, December 05, 2013

Weekly Initial Unemployment Claims decline to 298,000, Q3 GDP Revised up to 3.6%

The BEA reports:

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 3.6 percent in the third quarter of 2013 (that is, from the second quarter to the third quarter), according to the "second" estimate released by the Bureau of Economic Analysis. ... The GDP estimate released today is based on more complete source data than were available for the "advance" estimate issued last month. In the advance estimate, the increase in real GDP was 2.8 percentThe DOL reports:

The upward revision to the percent change in real GDP primarily reflected upward revisions to private inventory investment and to nonresidential fixed investment that were partly offset by an upward revision to imports and a downward revision to exports

In the week ending November 30, the advance figure for seasonally adjusted initial claims was 298,000, a decrease of 23,000 from the previous week's revised figure of 321,000. The 4-week moving average was 322,250, a decrease of 10,750 from the previous week's revised average of 333,000.The previous week was up from 316,000.

The following graph shows the 4-week moving average of weekly claims since January 2000.

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased to 322,250.

The level of weekly claims suggests an improving labor market.

Wednesday, December 04, 2013

Thursday: Unemployment Claims, Q3 GDP

by Calculated Risk on 12/04/2013 09:05:00 PM

On the MBA Purchase Index: This morning I mentioned a WSJ article Smaller Mortgage Lenders Lead Field. This suggests that the MBA Purchase Index might be understating purchase activity if smaller lenders (not in the survey) are gaining share. MBA's Mike Fratantoni told me today:

[I]n the last couple of years ... independent mortgage bankers have accounted for a fast growing share of the purchase market ... We have actively recruited independents and smaller banks to get better coverage of the purchase market. ... It is likely that many of the lenders not in the survey have a higher purchase share and lower refi share.It appears these small independent lenders are focusing on the purchase market (probably marketing through real estate agents - and selling the loans to Fannie and Freddie). A result of this change in market share is the Purchase Index is probably understating the increase in purchase activity.

Thursday:

• At 8:30 AM ET, the initial weekly unemployment claims report will be released. The consensus is for claims to increase to 322 thousand from 316 thousand last week.

• Also at 8:30 AM, the is the second estimate of Q3 GDP from the BEA. The consensus is that real GDP increased 3.1% annualized in Q3, revised up from the advance estimate of 2.8%.

• At 10:00 AM, the Manufacturers' Shipments, Inventories and Orders (Factory Orders) for October. The consensus is for a 1.2% decrease in October orders.

Trulia: Asking House Price increases Slow in Hot Markets

by Calculated Risk on 12/04/2013 06:04:00 PM

From Trulia this morning: Trulia Price Monitor: Hottest Housing Markets Cool, While Warm Markets Heat Up

In November, asking home prices rose 12.1 percent year-over-year (Y-o-Y), increasing in 98 of the 100 largest U.S. metro areas. Regaining a bit of steam since the slowdown began in July, asking prices rose 1.0 percent month-over-month (M-o-M) and 3.0 percent quarter-over-quarter (Q-o-Q). In fact, the quarterly increase is the fastest in five months, though still lower than in the spring.Note: These asking prices are SA (Seasonally Adjusted) - and adjusted for the mix of homes - and this suggests further house price increases over the next few months on a seasonally adjusted basis.

...

The slowing of asking home price gains is most apparent in the housing markets with the biggest price rebounds. The slowdown – measured as the difference in the Q-o-Q price changes between November and August – was more than two percentage points in Las Vegas, Oakland, Atlanta, Phoenix, Detroit, and Los Angeles.

The price slowdown happening nationally is really a sharp deceleration in price gains in the hottest markets. Among the 100 U.S. largest metros, the quarterly price increase in the 10 metros where prices rose more than 20 percent Y-o-Y fell from 6.1 percent in August to 3.7 percent in November. But in the 56 markets where prices rose by less than 10 percent Y-o-Y, price gains actually accelerated in the most recent quarter, rising 1.6 percent in November compared with 1.3 percent in August. Prices accelerated in Philadelphia, Pittsburgh, and Miami, for instance.

“The price slowdown – like everything about housing – is all local,” said Jed Kolko, Trulia’s Chief Economist. “Price gains are cooling in 2013’s hottest markets, like Las Vegas and Oakland, but heating up in markets that haven’t been in the limelight.” emphasis added

More from Kolko: Hottest Housing Markets Cool, But Warm Markets Heat Up

Fed's Beige Book: Economic activity increased "at a modest to moderate pace"

by Calculated Risk on 12/04/2013 02:00:00 PM

Fed's Beige Book "Prepared at the Federal Reserve Bank of Cleveland and based on information collected on or before November 22, 2013. This document summarizes comments received from business and other contacts outside the Federal Reserve and is not a commentary on the views of Federal Reserve officials."

Reports from the twelve Federal Reserve Districts indicated that the economy continued to expand at a modest to moderate pace from early October through mid-November. Activity in the New York, Cleveland, Richmond, Atlanta, St. Louis, Minneapolis, and Dallas Districts grew at a moderate pace, while Philadelphia, Chicago, Kansas City, and San Francisco cited modest growth. Boston reported that economic activity continued to expand.And on real estate:

Residential real estate activity improved in Boston, Philadelphia, Chicago, St. Louis, Minneapolis, and San Francisco, while remaining steady or softening in other Districts. Some slowing in single-family home sales was attributed to seasonal factors. Nonetheless, sales remain largely above year-ago levels. Increasing demand, low to declining levels of inventory, and slowly rising new-home construction were cited by almost all Districts as reasons for a continued rise in home prices, but at a slower pace than was observed earlier in 2013. Historically low inventories of unsold homes were reported in Philadelphia, Richmond, Chicago, Kansas City, and Dallas. Chicago noted that the inventory of homes for sale is at a record low. In the Philadelphia, Cleveland, Kansas City, and San Francisco Districts, builders continued to face a scarcity of high-skilled trade workers. Boston, New York, Philadelphia, Cleveland, Richmond, and Chicago indicated that multifamily construction continued to experience moderate to strong growth, with strength concentrated in the apartment segment. Vacancy rates declined across most Districts.Overall this was similar to the previous beige book with economic activity increasing at a "modest to moderate" pace.

Commercial real estate activity remained stable or improved slightly across many Districts. Philadelphia, Cleveland, Richmond, Chicago, St. Louis, and Minneapolis all saw gains in industrial construction, while Boston, Chicago, and St. Louis cited a rise in hotel construction. The technology sector drove demand for commercial real estate in the San Francisco District, and Cleveland saw gains in affordable housing and shale-gas-related activity. The outlook of market participants is for continued improvement in the Philadelphia, Atlanta, Kansas City, and Dallas Districts, while contacts were cautiously optimistic in Boston and Cleveland.

emphasis added

ISM Non-Manufacturing Index at 53.9 indicates slower expansion in November

by Calculated Risk on 12/04/2013 11:35:00 AM

Catching up ... the November ISM Non-manufacturing index was at 53.9%, down from 55.4% in October. The employment index decreased in October to 52.5%, down from 56.2% in October. Note: Above 50 indicates expansion, below 50 contraction.

From the Institute for Supply Management: November 2013 Non-Manufacturing ISM Report On Business®

Economic activity in the non-manufacturing sector grew in November for the 47th consecutive month, say the nation's purchasing and supply executives in the latest Non-Manufacturing ISM Report On Business®.

The report was issued today by Anthony Nieves, CPSM, C.P.M., CFPM, chair of the Institute for Supply Management™ Non-Manufacturing Business Survey Committee. "The NMI® registered 53.9 percent in November, 1.5 percentage points lower than October's reading of 55.4 percent. This indicates continued growth at a slower rate in the non-manufacturing sector. The Non-Manufacturing Business Activity Index decreased to 55.5 percent, which is 4.2 percentage points lower than the 59.7 percent reported in October, reflecting growth for the 52nd consecutive month, but at a slower rate. The New Orders Index decreased slightly by 0.4 percentage point to 56.4 percent, and the Employment Index decreased 3.7 percentage points to 52.5 percent, indicating growth in employment for the 16th consecutive month, but at a slower rate. The Prices Index decreased 3.9 percentage points to 52.2 percent, indicating prices increased at a slower rate in November when compared to October. According to the NMI®, 11 non-manufacturing industries reported growth in November. Respondents' comments for the most part indicate the non-manufacturing sector is maintaining a steady course of incremental growth and a positive outlook for the upcoming months."

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

This was below the consensus forecast of 55.5% and indicates slower expansion in November than in October.

New Home Sales increased to 444,000 Annual Rate in October

by Calculated Risk on 12/04/2013 10:00:00 AM

Note: The New Home sales reports for September and October were both released today (delayed due to government shutdown).

The Census Bureau reports New Home Sales in October were at a seasonally adjusted annual rate (SAAR) of 444 thousand, and sales in September were at a 354 thousand SAAR.

August sales were revised down from 421 thousand to 379 thousand, and July sales were revised down from 390 thousand to 373 thousand.

The first graph shows New Home Sales vs. recessions since 1963. The dashed line is the current sales rate.

"Sales of new single-family houses in October 2013 were at a seasonally adjusted annual rate of 444,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 25.4 percent above the revised September rate of 354,000 and is 21.6 percent above the October 2012 estimate of 365,000."

Click on graph for larger image in graph gallery.

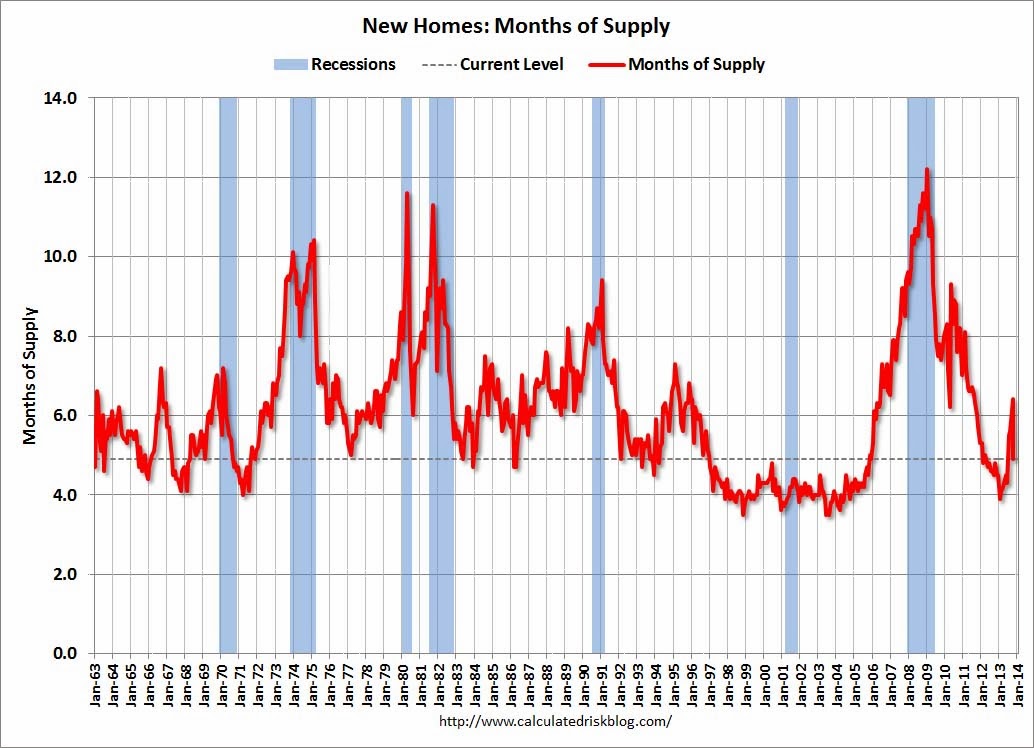

Click on graph for larger image in graph gallery.The second graph shows New Home Months of Supply.

The months of supply decreased in October to 4.9 months from 6.4 months in September.

The all time record was 12.1 months of supply in January 2009.

This is now in the normal range (less than 6 months supply is normal).

This is now in the normal range (less than 6 months supply is normal)."The seasonally adjusted estimate of new houses for sale at the end of October was 183,000. This represents a supply of 4.9 months at the current sales rate."On inventory, according to the Census Bureau:

"A house is considered for sale when a permit to build has been issued in permit-issuing places or work has begun on the footings or foundation in nonpermit areas and a sales contract has not been signed nor a deposit accepted."Starting in 1973 the Census Bureau broke this down into three categories: Not Started, Under Construction, and Completed.

This graph shows the three categories of inventory starting in 1973.

This graph shows the three categories of inventory starting in 1973.The inventory of completed homes for sale is near the record low. The combined total of completed and under construction is increasing, but still very low.

The last graph shows sales NSA (monthly sales, not seasonally adjusted annual rate).

In October 2013 (red column), 35 thousand new homes were sold (NSA). Last year 29 thousand homes were sold in October. The high for October was 105 thousand in 2005, and the low for October was 23 thousand in 2010.

This was above expectations of 425,000 sales in October, but there were significant downward revisions to prior months (as expected based on builder reports).

I'll have more later today - but no worries - the housing recovery will continue!

Trade Deficit decreased in October to $40.6 Billion

by Calculated Risk on 12/04/2013 08:30:00 AM

The Department of Commerce reported this morning:

[T]otal October exports of $192.7 billion and imports of $233.3 billion resulted in a goods and services deficit of $40.6 billion, down from $43.0 billion in September, revised. October exports were $3.4 billion more than September exports of $189.3 billion. October imports were $1.0 billion more than September imports of $232.3 billion.The trade deficit was close to the consensus forecast of $40.2 billion.

The first graph shows the monthly U.S. exports and imports in dollars through October 2013.

Click on graph for larger image.

Click on graph for larger image.Both imports and exports increased in October.

Exports are 16% above the pre-recession peak and up 5% compared to October 2012; imports are just above the pre-recession peak, and up about 4% compared to October 2012.

The second graph shows the U.S. trade deficit, with and without petroleum, through October.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.Oil averaged $99.96 in October, down from $102.00 in September, and up slightly from $99.76 in October 2012. Prices will probably decline further in November. The petroleum deficit has generally been declining and is the major reason the overall deficit has declined since early 2012.

The trade deficit with China decreased to $28.9 billion in October, down from $29.4 billion in October 2012. A majority of the trade deficit is related to China.

Overall it appears trade is picking up a little again.

ADP: Private Employment increased 215,000 in November

by Calculated Risk on 12/04/2013 08:19:00 AM

Private sector employment increased by 215,000 jobs from October to November, according to the November ADP National Employment Report®. ... The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.This was above the consensus forecast for 185,000 private sector jobs added in the ADP report.

...

Mark Zandi, chief economist of Moody’s Analytics, said, "The job market remained surprisingly resilient to the government shutdown and brinkmanship over the treasury debt limit. Employers across all industries and company sizes looked through the political battle in Washington. If anything, job growth appears to be picking up.”

Note: ADP hasn't been very useful in predicting the BLS report on a monthly basis. The BLS report for November will be released on Friday.

MBA: Mortgage Applications Decrease in Latest Survey

by Calculated Risk on 12/04/2013 07:03:00 AM

First, an interesting article from Shayndi Raice at the WSJ: Smaller Mortgage Lenders Lead Field

As of the third quarter, smaller mortgage players held a 60% market share of the U.S. origination market, up from 39% in 2009, according to industry publication Inside Mortgage Finance.This shift in market share has possible implications for the MBA purchase index. Back in 2007, the MBA index started to increase - and some observers like Alan Greenspan thought this meant the housing bust was over. I pointed out back then that the index was being distorted by a shift from smaller lenders to larger lenders (the smaller lenders were going out of business). The MBA index includes many lenders, but is skewed towards the larger lenders.

...

The midsize and smaller players have grown despite tightening their underwriting standards, much like larger banks have since the financial crisis. But the smaller banks' capital rules aren't as stringent as those that make mortgages a costly enterprise for the biggest firms.

Now the index is probably understating the activity in the market - because there is a market shift from large lenders to smaller lenders.

From the MBA: Mortgage Applications Fall During Holiday-Shortened Week

Mortgage applications decreased 12.8 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending November 29, 2013. This week’s results include an adjustment for the Thanksgiving holiday. ...

The Refinance Index decreased 18 percent from the previous week and is at its lowest level since the week ending September 6, 2013. The seasonally adjusted Purchase Index decreased 4 percent from one week earlier. ...

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) increased to 4.51 percent from 4.48 percent, with points increasing to 0.38 from 0.31 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the refinance index.

The refinance index is down sharply - and down 69% from the levels in early May.

The second graph shows the MBA mortgage purchase index.

The second graph shows the MBA mortgage purchase index. The 4-week average of the purchase index is now down about 8% from a year ago.

Tuesday, December 03, 2013

Wednesday: New Home Sales, Trade Deficit, ADP Employment, ISM Service, Beige Book and More

by Calculated Risk on 12/03/2013 07:50:00 PM

From Cardiff Garcia at FT Alphaville: ISM vs the hard data

Two recent notes emphasise that the impressive recent ISM manufacturing readings in the US are probably as much about expectations of future performance as about what has already happened.Another hint that economic growth will increase in 2014.

...

Tom Porcelli of RBC Capital Markets highlights the point that ISM is normally a leading indicator for the hard data:

ISM new orders has historically led the 3-month run rate of capex shipments by about one full quarter. Bottom line: the ISM data continue to flag an acceleration in capex growth near term.

Wednesday:

• At 7:00 AM ET, the Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:15 AM, the ADP Employment Report for November. This report is for private payrolls only (no government). The consensus is for 185,000 payroll jobs added in November, up from 130,000 in October.

• At 8:30 AM, the Trade Balance report for October from the Census Bureau. The consensus is for the U.S. trade deficit to decrease to $40.2 billion in October from $41.8 billion in September.

• At 10:00 AM, the New Home Sales for September and October from the Census Bureau. The consensus is for an increase in sales to 425 thousand Seasonally Adjusted Annual Rate (SAAR) in October from 421 thousand in August.

• Also at 10:00 AM, the ISM non-Manufacturing Index for November. The consensus is for a reading of 55.5, up from 55.4 in October. Note: Above 50 indicates expansion, below 50 contraction.

• Also at 10:00 AM, the Trulia Price Rent Monitors for November. This is the index from Trulia that uses asking house prices adjusted both for the mix of homes listed for sale and for seasonal factors.

• At 2:00 PM. the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.