RSS Feed

RSS Feed by Calculated Risk on 2/12/2013 03:40:00 PM

Tuesday, February 12, 2013

Lawler: Table of Short Sales and Foreclosures for Selected Cities in January

Economist Tom Lawler sent me the table below of short sales and foreclosures for several selected cities in January.

Look at the right two columns in the table below (Total "Distressed" Share for Jan 2013 compared to Jan 2012). In every area that reports distressed sales, the share of distressed sales is down year-over-year - and down significantly in most areas.

Also there has been a decline in foreclosure sales just about everywhere. Look at the middle two columns comparing foreclosure sales for Jan 2013 to Jan 2012. Foreclosure sales have declined in all these areas, and some of the declines have been stunning (the Nevada sales were impacted by a new foreclosure law).

Also there has been a shift from foreclosures to short sales. In most areas, short sales now out number foreclosures (Minneapolis is an exception).

I think this is important: Imagine that the number of total existing home sales doesn't change over the next year - some people would argue that is "bad" news and the housing market isn't recovering. But also imagine that the share of distressed sales declines 20%, and conventional sales increase to make up the difference. That would be a positive sign - and that is what appears to be happening.

An example would be Sacramento (I posted data on Sacramento yesterday). In Sacramento, total sales were down 9% in Jan 2013 compared to Jan 2012, but conventional sales were up 51%! I'd say that market is still unhealthy, but recovering.

| Short Sales Share | Foreclosure Sales Share | Total "Distressed" Share | ||||

|---|---|---|---|---|---|---|

| 13-Jan | 12-Jan | 13-Jan | 12-Jan | 13-Jan | 12-Jan | |

| Las Vegas | 36.2% | 28.1% | 12.5% | 45.5% | 48.7% | 73.6% |

| Reno | 41.0% | 37.0% | 10.0% | 40.0% | 51.0% | 77.0% |

| Phoenix | 17.6% | 29.8% | 16.2% | 27.9% | 33.8% | 57.7% |

| Sacramento | 30.3% | 32.1% | 14.2% | 34.5% | 44.5% | 66.6% |

| Minneapolis | 10.6% | 16.2% | 32.3% | 39.0% | 42.9% | 55.2% |

| Mid-Atlantic (MRIS) | 13.1% | 16.4% | 12.7% | 16.9% | 25.8% | 33.3% |

| Hampton Roads | 34.9% | 37.2% | ||||

| Charlotte | 18.1% | 21.0% | ||||

| Metro Detroit | 36.3% | 54.5% | ||||

| Memphis* | 25.9% | 36.6% | ||||

| *share of existing home sales, based on property records | ||||||

More Research on Construction Employment

by Calculated Risk on 2/12/2013 12:24:00 PM

A key economic question this year is how many construction jobs will be added. Here are a few excerpts from analysis Kris Dawsey and Hui Shan at Goldman Sachs: Housing Sector Jobs Poised for a Comeback

Although many indicators of housing activity improved during 2012, employment in the sector remains close to post-bubble lows. Looking only at residential construction jobs, employment declined by 1.5 million (-42%) from its peak in 2006 to its recent trough in early 2011 and edged up only a modest 100 thousand since then. However, direct residential construction employment is only a part of all residential investment-related employment. Adding in housing-related employment in manufacturing, wholesale trade, retailing, and finance & real estate, employment dropped by 2.8 million (-31%) from its peak, and gained a bit less than 300 thousand from its trough to the present ...So their analysis suggests construction companies have been increasing hours worked for current employees, but now they need to hire more workers.

[R]eal residential investment declined somewhat more sharply than housing-related employment in the downturn, resulting in a decline in real value added per residential investment-related worker, according to our proxy measure, from more than $80,000 in 2006 to a bit less than $60,000 in Q4:2012, in chained 2005 dollars. This pattern of declining productivity during a downturn is called "labor hoarding" by economists (although labor hoarding is probably not what most people think of during a period of sharp job cuts) and reflects businesses' reluctance to fire workers at a rate commensurate with the decline in their sales.

The flip side of this phenomenon is more sluggish employment growth than would otherwise be the case once business activity turns around. On top of the only modest turnaround in activity, this secondary effect also argues for only a modest rebound in residential investment-related employment early on in the recovery. However, this effect may shortly be coming to an end. Hours per worker in the construction industry now exceed pre-crisis highs, suggesting that room to increase output on the "intensive margin" (i.e. more hours per worker) is diminishing, and that pushing on the "extensive margin" (hiring more workers) will likely account for a larger share of future increases in residential investment output.

...

Given that we expect real residential investment to continue growing at a roughly stable 10%-15% rate in 2013 and 2014, and that the effects of labor hoarding should be dissipating, what is our forecast for residential investment-related employment growth over the coming several years? In order to answer this question, we estimated two different econometric models: (1) an error correction model of national-level real residential investment and residential investment-related employment, and (2) a state-level panel analysis of the relationship between construction activity and employment. Both models suggest an increase in the rate of housing-related employment growth in 2013 and 2014 relative to 2012, probably to a rate around 25 to 30k per month.

emphasis added

Earlier articles on construction employment:

• From Michelle Meyer at Merrill Lynch: Construction Coming Back

• From Jed Kolko at Trulia: Here are the “Missing” Construction Jobs

• From Professor Tim Duy at EconomistsView: Employment Report Nothing If Not Consistent

BLS: Job Openings "little changed" in December

by Calculated Risk on 2/12/2013 10:05:00 AM

From the BLS: Job Openings and Labor Turnover Summary

There were 3.6 million job openings on the last business day of December, little changed from November ...The following graph shows job openings (yellow line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

The level of total nonfarm job openings was 2.4 million at the end of the recession in June 2009.

...

The number of quits was 2.2 million in December compared to 1.8 million at the end of the recession in June 2009.

This series started in December 2000.

Note: The difference between JOLTS hires and separations is similar to the CES (payroll survey) net jobs headline numbers. This report is for December, the most recent employment report was for January.

Click on graph for larger image.

Click on graph for larger image.Notice that hires (dark blue) and total separations (red and light blue columns stacked) are pretty close each month. This is a measure of turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

Jobs openings decreased in December to 3.617 million, down from 3.790 million in November. The number of job openings (yellow) has generally been trending up, but openings are only up 2% year-over-year compared to December 2011.

Quits decreased slightly in December, and quits are up 7% year-over-year. These are voluntary separations. (see light blue columns at bottom of graph for trend for "quits").

Not much changes month-to-month in this report, but the trend suggests a gradually improving labor market.

NFIB: Small Business Optimism Index increases slightly in January, Still very low

by Calculated Risk on 2/12/2013 08:50:00 AM

From the National Federation of Independent Business (NFIB): Small-Business Owner Confidence Barely Budges

Small-business owner confidence continues to drag, according to the National Federation of Independent Business (NFIB) Small Business Optimism Index. The Index gained 0.9 points, rising to 88.9, failing to regain the losses caused by last month’s “fiscal cliff” scare. Expectations for improved business conditions increased by five points, but remain overwhelmingly low—negative 30 percent—the fourth lowest reading in survey history. Actual job creation and job creation plans improved nominally, but still not enough to keep up with population growth.

Click on graph for larger image.

Click on graph for larger image.This graph shows the small business optimism index since 1986. The index increased to >88.9 in January from 88.0 in December.

Note: Small businesses have a larger percentage of real estate and retail related companies than the overall economy. This index remains low.

Monday, February 11, 2013

Nikkei Opens Up Sharply following Finance Ministers Price Target

by Calculated Risk on 2/11/2013 07:31:00 PM

Imagine Jack Lew (Treasury Secretary nominee) or Fed Chairman Ben Bernanke announcing a price target for the DOW or S&P500 ... that seems extremely unlikley. But in Japan ...

From MarketWatch: Japan stocks rally on yen in post-holiday return

Japan stocks surged in early Tuesday trade, as investors returned from a three-day weekend to find the yen at yet another fresh multiyear low, with the Nikkei Stock Average jumping 2.5% to 11,432.29, and the Topix up 2%.And from the Japan Times: Japan’s economic minister wants Nikkei to surge 17% to 13,000 by March

Economic and fiscal policy minister Akira Amari said Saturday the government will step up economic recovery efforts so that the benchmark Nikkei index jumps an additional 17 percent to 13,000 points by the end of March.Felix Salmon likes the idea: When the finance minister targets stock prices

“It will be important to show our mettle and see the Nikkei reach the 13,000 mark by the end of the fiscal year (March 31),” Amari said in a speech.

The Nikkei 225 stock average, which last week climbed to its highest level since September 2008, finished at 11,153.16 on Friday.

“We want to continue taking (new) steps to help stock prices rise” further, Amari stressed ...

I like this move: it shows imagination, and the upside is much bigger than the downside. The worst that can happen is that it doesn’t work, and the stock market ends up doing what the stock market would have done anyway; the best that can happen is that it helps accelerate the broad recovery that everybody in Japan is hoping for this year.CR Note: I don't think this is a good policy idea ...

What’s more, Amari is not the first policymaker to talk about targeting asset prices. Minneapolis Fed president Narayana Kocherlakota, for instance, said quite clearly in 2011 that stock prices “are really going to be a central ingredient in the recovery process”, adding:

In this kind of post financial crisis, post net worth driven recession, it makes sense to be thinking about asset value as a way to try to generate more stimulus than you do in a typical recession.In other words, don’t look to government spending for stimulus: Japan, of course, has learned that lesson the hard way. Instead, simply goose the stock market instead.

There are risks to this approach: if it works too well, you create a bubble — and when a bubble bursts, that can hurt confidence much more than a rising stock market helped it. But for the time being, the Japanese stock market still looks cheap, both on an absolute basis and in terms of its p/e ratio. Now’s no time to worry about overheating. Instead, Japan’s fiscal and monetary policymakers are working together to try to make the country as bullish and successful as possible. I’d do the same thing, if I were them.

Las Vegas Real Estate: Sales and Inventory decreased year-over-year in January

by Calculated Risk on 2/11/2013 04:13:00 PM

This is a key distressed market to follow since Las Vegas has seen the largest price decline of any of the Case-Shiller composite 20 cities.

The Greater Las Vegas Association of Realtors (GLVAR) reported (Most data via Tom Lawler):

• Residential home sales by realtors in the Las Vegas metro area totaled 2,821 in January, down 21.4% from last January’s pace

• Bank-owned properties were 12.5% of last month’s sales, down from 45.5% last January, while last month’s short-sales share were 36.2%, up from 28.1% a year ago.

• All-cash transactions were 56.2% of last month’s sales, up from 52.5% last January.

• Total listings in January totaled 17,910, down 0.9% from December and down 23.1% from a year ago. However single family home listings without offers were down over 58% from a year ago. A large number of the homes listed for sales are "short sale pending".

• Short sales are about three times foreclosures now. We've seen a shift from foreclosures to short sales in most areas (not just in areas with new foreclosure laws). Note: Some of the surge in short sales last month might have been due to sellers pushing to beat the expiration of the Mortgage Debt Relief Act of 2007, and there was a decline in January. The Act was extended as part of the fiscal deal, so the number of short sales should remain high in 2013.

• The decline in overall sales is because of fewer foreclosure sales. As the market slowly recovers, the number of distressed sales should fall and the number of conventional sales should rise.

Overall this is a slowly improving distressed market. Note: The median price was up 27.1% from a year ago, but I suggest using the repeat sales indexes because the median is impacted by the mix.

Fed's Yellen: "A Painfully Slow Recovery for America's Workers"

by Calculated Risk on 2/11/2013 01:21:00 PM

From Fed Vice Chair Janet Yellen: A Painfully Slow Recovery for America's Workers: Causes, Implications, and the Federal Reserve's Response. Some excerpts on the slow recovery:

In trying to account for why this recovery has been so weak, it is helpful to first consider several important factors that have in the past supported most economic recoveries. By this I don't mean everything that contributes to economic growth, but rather those things that typically play a key role when the U.S. economy is recovering from recession. Think of these as the tailwinds that usually promote a recovery.CR Note: The first missing tailwind is fiscal policy. Even as the Federal government provided some stimulus, state and local governments cut back significant for four consecutive years. And for the last couple of years, we've also seen austerity at the Federal level - and that will probably continue. The good news is the cutbacks at the state and local level are probably mostly over.

The first tailwind I'll mention is fiscal policy. History shows that fiscal policy often helps to support an economic recovery. Some of this fiscal stimulus is automatic, and intended to be. The income loss that individuals and businesses suffer in a recession is partly offset when their tax bills fall as well. Government spending on unemployment benefits and other safety-net programs rises in recessions, helping individuals hurt by the downturn and also supporting consumer spending and the broader economy by replacing lost income. These automatic declines in tax collections and increases in government spending are often supplemented with discretionary fiscal action--tax rate cuts, spending on infrastructure and other goods and services, and extended unemployment benefits. These discretionary fiscal policy actions are typically a plus for growth in the years just after a recession. For example, following the severe 1981-82 recession, discretionary fiscal policy contributed an average of about 1 percentage point per year to real GDP growth over the subsequent three years.

However, discretionary fiscal policy hasn't been much of a tailwind during this recovery. In the year following the end of the recession, discretionary fiscal policy at the federal, state, and local levels boosted growth at roughly the same pace as in past recoveries, as exhibit 3 indicates. But instead of contributing to growth thereafter, discretionary fiscal policy this time has actually acted to restrain the recovery. State and local governments were cutting spending and, in some cases, raising taxes for much of this period to deal with revenue shortfalls. At the federal level, policymakers have reduced purchases of goods and services, allowed stimulus-related spending to decline, and have put in place further policy actions to reduce deficits. ...

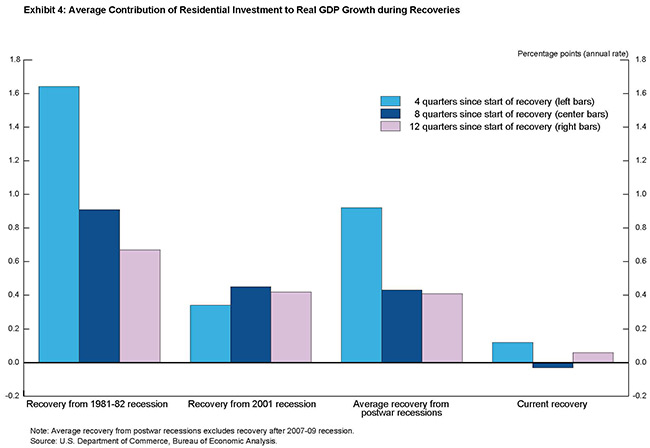

A second tailwind in most recoveries is housing. Residential investment creates jobs in construction and related industries. Before the Great Recession, housing investment added an average of 1/2 percentage point to real GDP growth in the two years after each of the previous four recessions, considerably more than its contribution to growth at other times.

During this recovery, in contrast, residential investment, on net, has contributed very little to growth since the recession ended. The reasons are easy to understand, given the central role that housing played in the Great Recession. Following an extended boom in construction driven in large part by overly loose mortgage lending standards and unrealistic expectations for future home price increases, the housing market collapsed--sales and prices plunged and mortgage credit was sharply curtailed. Tight mortgage credit conditions are continuing to make it difficult for many families to buy homes, despite record-low mortgage interest rates that have helped make housing very affordable. I'm encouraged by recent improvement in the residential sector, but the contribution of housing investment to overall economic activity remains considerably below the average seen in past recoveries, as exhibit 4 shows.

Beyond the direct effects on residential investment, the extraordinary collapse in house prices resulted in a huge loss of household wealth--at last count, net home equity is still down 40 percent, or about $5 trillion, from 2005. ...

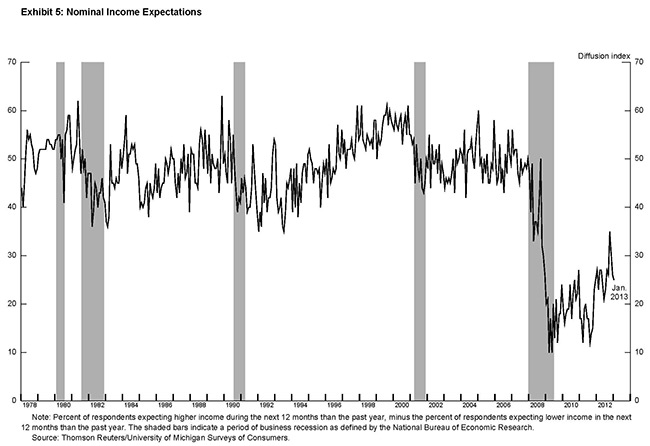

Another important tailwind in most economic recoveries is one that tends to be taken for granted--the faith most of us have, based on history and personal experience, that recessions are temporary and that the economy will soon get back to normal. Even during recessions, households' expectations for income growth tend to be reasonably stable, which provides support for overall spending. In the most recent recession, however, surveys suggest that consumers sharply revised down their prospects for future income growth and have only partially adjusted up their expectations since then (exhibit 5).

The recovery has also encountered some unusual headwinds. The fiscal and financial crisis in Europe has resulted in a euro-area recession and contributed to slower global growth. Europe's difficulties have blunted what had been strong growth in U.S. exports earlier in the recovery by sapping demand worldwide.

The next missing tailwind has been a focus of this blog: Residential investment (RI). RI has finally turned the corner and has started to contribute to the economy. Looking forward, I expect growth to improve over the next few years, although growth will be slowed by the fiscal agreement and other Federal austerity in 2013.

Sacramento January House Sales: Conventional Sales up 51% year-over-year

by Calculated Risk on 2/11/2013 09:27:00 AM

Note: I've been following the Sacramento market to look for changes in the mix of house sales in a distressed area over time (conventional, REOs, and short sales). The Sacramento Association of REALTORS® started breaking out REOs in May 2008, and short sales in June 2009.

Over the last two years there was a dramatic shift from REO to short sales, and the percentage of distressed sales declined.

Note: The percent of short sales declined in January because some sellers pushed to close in 2012 before the "Mortgage Debt Relief Act of 2007" expired. The Act was extended for one year as part of the fiscal agreement. (Usually cancelled debt is considered income, but some mortgage debt was exlcuded as part of the Act).

This data suggests continued improvement in the Sacramento market.

In January 2013, 44.5% of all resales (single family homes and condos) were distressed sales. This was down from 51.5% last month, and down from 66.6% in January 2012. This is the lowest percentage of distressed sales - and therefore the highest percentage of conventional sales - since the association started tracking the data.

The percentage of REOs stayed increased to 14.2%, and the percentage of short sales decreased to 30.3%.

Here are the statistics.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the percent of REO sales, short sales and conventional sales.

There has been an increase in conventional sales recently, and there were twice as many short sales as REO sales in January.

Total sales were down from January 2012, but conventional sales were up 51% compared to the same month last year. This is exactly what we expect to see in an improving distressed market - flat or even declining overall sales as distressed sales decline, and conventional sales increase.

Active Listing Inventory for single family homes declined 61.1% from last January.

Cash buyers accounted for 37.4% of all sales (frequently investors), and median prices were up sharply year-over-year (the mix has changed).

This continues to move in the right direction, although the market is still in distress. A "normal" market would be mostly blue on the graph, and this market is a long way from "normal". We are seeing a similar pattern in other distressed areas, with a move to more conventional sales, and a shift from REO to short sales. This is a sign of a recovering market.

A Compendium of Tanta's Posts

by Calculated Risk on 2/11/2013 09:02:00 AM

Reader Mike kindly sent me all of the links to Tanta's posts in 2007 and 2008, and I'd like to share the updated list.

Note: Tanta was very knowledgeable about the mortgage industry - and many other topics - and she was my blogging partner in 2007 and 2008.

Here is the updated list: Compendium of Tanta's Posts

And other reading:

The Compleat UberNerd

CR writes: Sad News: Tanta Passes Away

NY Times: Doris Dungey, Prescient Finance Blogger, Dies at 47

WaPo: Doris J. Dungey; Blogger Chronicled Mortgage Crisis

Tanta: In Memoriam

Sunday, February 10, 2013

Sunday Night Futures

by Calculated Risk on 2/10/2013 09:39:00 PM

On oil prices from Jim Hamilton: Dude, where's my cheap gas?

Those who have been told that oil production is booming may be wondering why the prices of oil and gasoline are climbing again.Monday:

...[Several graphs]

It's obvious from the above price charts that it makes no economic sense to add gallons of ethane or propane to gallons of crude oil to try to summarize global oil supply. But growth of natural gas liquids has been a key factor in the reported increases in "world oil supply" over the last few years and is also a key component of recent optimistic assessments of future oil production by Leonardo Maugeri and the IEA.

There is no question that the boom in production of natural gas liquids is providing a great benefit to industrial users of ethylene. But if you're waiting for it to lower the price you pay for gasoline at the pump, you may have to wait a while longer.

• At 1:00 PM ET: Speech by Fed Vice Chair Janet Yellen, "A Painfully Slow Recovery for America's Workers: Causes, Implications, and the Federal Reserve's Response"

Weekend:

• Summary for Week Ending Feb 8th

• Schedule for Week of Feb 10th

The Nikkei is closed for National Foundation Day, and the Hang Seng and Shanghai are closed for New Year.

From CNBC: Pre-Market Data and Bloomberg futures: the S&P futures and DOW futures are up slightly.

Oil prices have been mixed recently with WTI futures down to $95.76 per barrel and Brent up to $118.88 per barrel. Gasoline prices are up almost 30 cents over the last few weeks.

{kind=link}

{kind=link}