RSS Feed

RSS Feed by Calculated Risk on 3/24/2010 10:00:00 AM

Wednesday, March 24, 2010

New Home Sales at Record Low in February

The Census Bureau reports New Home Sales in February were at a seasonally adjusted annual rate (SAAR) of 308 thousand. This is a new record low and a decrease from the revised rate of 315 thousand in January (revised from 309 thousand). Click on graph for larger image in new window.

Click on graph for larger image in new window.

The first graph shows monthly new home sales (NSA - Not Seasonally Adjusted).

Note the Red columns for 2010. In February 2010, 24 thousand new homes were sold (NSA).

This is below the previous record low of 29 thousand hit three times; in February 2009, 1982 and 1970. The second graph shows New Home Sales vs. recessions for the last 45 years. New Home sales fell off a cliff, but after increasing slightly, are now 6% below the previous record low in January 2009.

The second graph shows New Home Sales vs. recessions for the last 45 years. New Home sales fell off a cliff, but after increasing slightly, are now 6% below the previous record low in January 2009.

Sales of new single-family houses in February 2010 were at a seasonally adjusted annual rate of 308,000, according to estimates released jointly today ... This is 2.2 percent (±15.3%)* below the revised January rate of 315,000 and is 13.0 percent (±12.2%) below the February 2009 estimate of 354,000.And another long term graph - this one for New Home Months of Supply.

There were 9.2 months of supply in February. Rising, but still significantly below the all time record of 12.4 months of supply set in January 2009.

There were 9.2 months of supply in February. Rising, but still significantly below the all time record of 12.4 months of supply set in January 2009.The seasonally adjusted estimate of new houses for sale at the end of February was 236,000. This represents a supply of 9.2 months at the current sales rate.

The final graph shows new home inventory.

The final graph shows new home inventory. Note that new home inventory does not include many condos (especially high rise condos), and areas with significant condo construction will have much higher inventory levels.

New home sales are far more important for the economy than existing home sales, and new home sales will remain under pressure until the overhang of excess housing inventory declines much further. Obviously this is another extremely weak report.

MBA: Mortgage Applications Decrease, Rates Rise

by Calculated Risk on 3/24/2010 08:52:00 AM

The MBA reports: Mortgage Refinance Applications Decrease in Latest MBA Weekly Survey

The Market Composite Index, a measure of mortgage loan application volume, decreased 4.2 percent on a seasonally adjusted basis from one week earlier. ...

The Refinance Index decreased 7.1 percent from the previous week and the seasonally adjusted Purchase Index increased 2.7 percent from one week earlier. ...

The refinance share of mortgage activity decreased to 65.0 percent of total applications from 67.3 percent the previous week. This is the lowest refinance share observed in the survey since the week ending October 30, 2009. ...

The average contract interest rate for 30-year fixed-rate mortgages increased to 5.01 percent from 4.91 percent, with points decreasing to 0.76 from 1.30 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans.

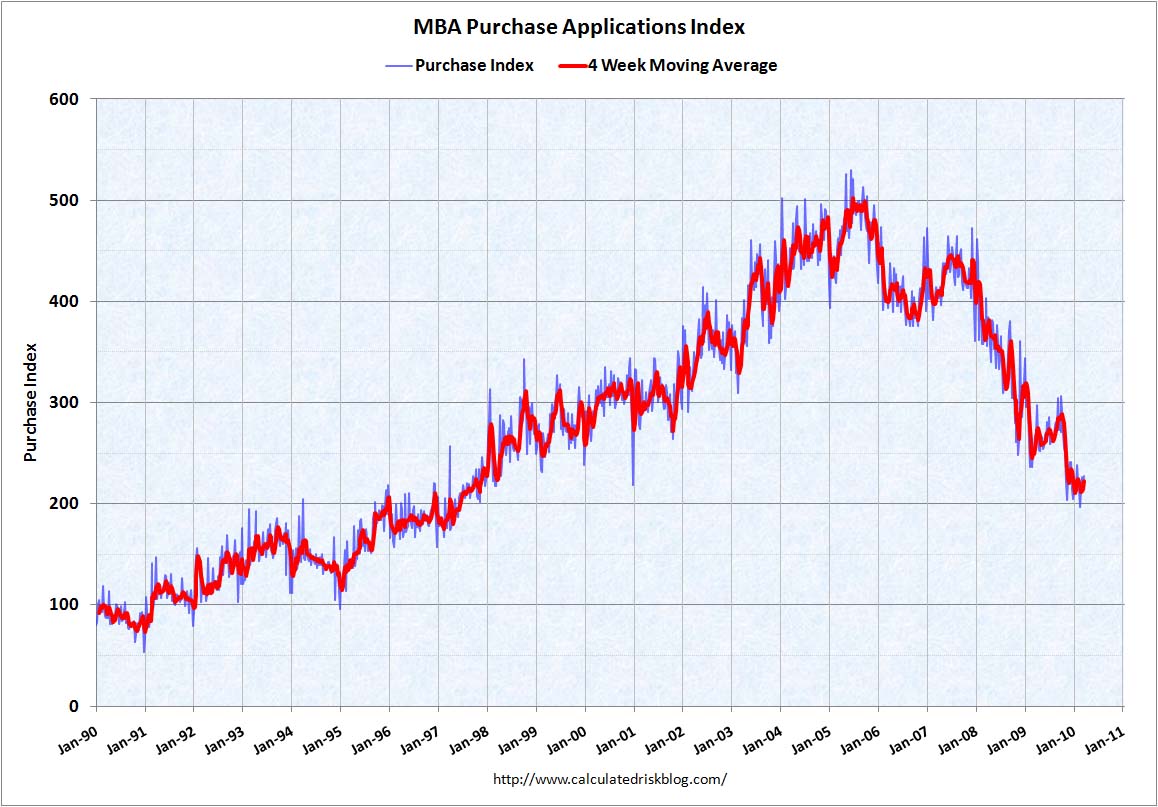

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the MBA Purchase Index and four week moving average since 1990.

There was a slight increase in purchase applications last week, but the 4-week average is still near the levels of 1997 - after falling sharply at the end of last year. This index shows no indication yet of the expected increase in home sales due to the expiration of the home buyer tax credit.

Report: BofA to Announce Mortgage Principal Reduction Plan

by Calculated Risk on 3/24/2010 05:35:00 AM

From Reuters: BofA to start reducing mortgage principal-sources

Bank of America will ... announce plans to start forgiving mortgage loan principal for troubled homeowners who owe more than 120 percent of their home's value or are battling ever-expanding "negative amortization" loans.Apparently under the plan, the mortgage debt will be reduced to 100% of the house's value over 5 years. The details should be released today by BofA.

According to a summary of the program obtained by Reuters, Bank of America pledged to offer an "earned principal forgiveness" of up to 30 percent in two stages. The lender will first offer an interest-free forbearance of principal that the homeowner can turn into forgiven principal annually over five years, provided they stay current on their payments.

Tuesday, March 23, 2010

AIA: Architecture Billings Index Shows Contraction in February

by Calculated Risk on 3/23/2010 11:59:00 PM

Note: This index is a leading indicator for Commercial Real Estate (CRE) investment. Any reading below 50 indicates contraction.

The WSJ reports that the American Institute of Architects’ Architecture Billings Index increased to 44.8 in February from 42.5 in January.

The ABI press release is not online yet. Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the Architecture Billings Index since 1996. The index has remained below 50, indicating falling demand, since January 2008.

The second graph compares the Architecture Billings Index with the year-over-year change in non-residential structure investment.  Historically, according to the AIA, there is an "approximate nine to twelve month lag time between architecture billings and construction spending" on non-residential construction. This suggests further significant declines in CRE investment through all of 2010, and probably longer.

Historically, according to the AIA, there is an "approximate nine to twelve month lag time between architecture billings and construction spending" on non-residential construction. This suggests further significant declines in CRE investment through all of 2010, and probably longer.

Note: Nonresidential construction includes commercial and industrial facilities like hotels and office buildings, as well as schools, hospitals and other institutions.

California Extends Homebuyer Tax Credit

by Calculated Risk on 3/23/2010 08:03:00 PM

From the Mercury News: Gas tax deal comes with goodies for California home buyers and green-tech manufacturers

The deal reached Monday provides $200 million in new tax credits for homebuyers, to be split evenly among those buying a home for the first time and anyone buying a newly constructed home. Anyone qualified who makes a purchase between this May and August 2011 will receive a credit for 5 percent of the home's purchase price, up to $10,000 over three years.Dumb. Not that there is budget problem in California ...

Fed's Yellen: Outlook for the Economy and Inflation

by Calculated Risk on 3/23/2010 03:43:00 PM

From San Francisco Fed President Janet Yellen: The Outlook for the Economy and Inflation, and the Case for Federal Reserve Independence

Some excerpts on housing (Note: Yellen is likely to be nominated as the next Fed Vice Chairman):

It was housing of course that led the economy down. The great bust wiped out some $7 trillion in home values. In the second half of 2009 though, housing showed signs of stabilizing and I became hopeful that the sector would provide a significant boost to the economy this year. Now the market seems to have stalled. Home prices have been more or less stable since the middle of last year, but new home sales have resumed a downward slide and are at very low levels. Existing home sales spiked towards the end of last year in response to the homebuyer tax credit and have receded markedly since then. The credit expires this spring, removing an important prop. With sales still weak, builders have little incentive to ramp up home construction.As Yellen notes, one of the defining characteristics of this housing bust is how few mortgage delinquencies are cured. Of course when a borrower has equity in their home, they can cure the delinquency by selling. And this time many borrowers have negative equity and can't sell.

The continued high pace of foreclosures also creates risks to the recovery of the housing sector. Mortgage delinquencies and foreclosures are still rising as a consequence of the plunge in house prices over the past few years combined with high levels of unemployment. Despite the return to growth of the broader economy, we’ve seen no let-up in the pace at which borrowers are falling behind in their loans. Further additions to the already swollen stockpile of vacant homes represent a threat to house prices and new home construction activity.

It’s not always easy to understand the dynamics of the housing sector. Last year, for example, the share of mortgages that was 30 to 89 days past due declined. On the face of it, that looked like a hopeful sign. Unfortunately, when my staff examined the numbers more closely, it turned out that the drop actually represented a worsening of mortgage market conditions. What you want to see is delinquent borrowers becoming current. Instead, what happened was that delinquent mortgages moved in the other direction to an even poorer performance status. Many wound up in foreclosure. All in all, I expect that the share of loans that are seriously delinquent will continue to move higher. I am also concerned that we had a temporary reprieve in new foreclosures as the federal government’s trial modification program got under way. But not all of these modifications will stick, which means that some borrowers in the program could find themselves facing foreclosure again.

At the end of this month, the Fed will complete a large-scale program of purchases of mortgage-backed securities issued by Fannie Mae and Freddie Mac. Lenders sell mortgages to these two agencies, which package them as securities sold to investors. Last year, the Fed began buying these securities as part of a series of extraordinary measures to promote recovery. At the time the program was announced, mortgage spreads over yields on Treasury securities of comparable maturity were very high, reflecting in part the disruptions that had occurred in financial markets. I believe that our program worked to narrow those spreads, bringing mortgage rates down and contributing to the stabilization of the housing market. Financial markets have improved considerably over the last year, and I am hopeful that mortgages will remain highly affordable even after our purchases cease. Any significant run-up in mortgage rates would create risks for a housing recovery.

I think Yellen is a little too optimistic on the overall economy - she is forecasting 3 1/2% GDP growth this year. And on unemployment:

I was heartened when the unemployment rate dropped in January to 9.7 percent from 10 percent the month before. I was further encouraged when the rate remained at 9.7 percent in February, suggesting it was not just a flash in the pan. In the months ahead, we could get a bump in employment from census hiring. But that, of course, would be temporary. Given my moderate growth forecast, I fear that unemployment will stay high for years. The rate should edge down from its current level to about 9 1/4 percent by the end of this year and still be about 8 percent by the end of 2011, a very disappointing prospect.I think that is a little optimistic too - although the next few months will see a slight decline because of Census hiring (but that will be unwound later in the year).

HAMP applicants tanned and juiced

by Calculated Risk on 3/23/2010 01:23:00 PM

CR Note: The following is from long time reader Shnaps. Shnaps has been working in the mortgage industry in various capacities "since people were extending the antennas on their mobile phones". Shnaps currently serves in a key role related to HAMP at one of the largest non-prime mortgage servicers in the Nation.

Shnaps writes:

One aspect of the Making Home Affordable loan modification program known as ‘HAMP’ is almost always taken for granted in its wide reporting – that the borrowers in fact need ‘help’. Moreover, it is generally taken for granted that those seeking modification under HAMP simply cannot afford their monthly mortgage payment. It is assumed that they have made great sacrifices, assumed they have already cut back drastically on discretionary expenses, assumed that they have already gone over their monthly budgets with a fine-toothed comb to eliminate all but the most necessary expenditures in an effort to keep their home. So prepare to be shocked – shocked! – as I share with you that I have seen first-hand that this assumption is oftentimes greatly, seriously flawed.

Let me begin with a word to the wise for HAMP applicants: unless you believe Snooki is now in charge of approving HAMP applications, it might be a good idea to cut back a bit on some of the creature comforts to which you have become accustomed at least a month before submitting your HAMP modification application.

Allow me to explain. The guidelines for servicers participating in HAMP stipulate that the borrower must submit a “hardship affidavit”. This, ostensibly, is to serve as their sworn testimony that they have been driven into default due to some particular hardship they encountered, and despite making every possible sacrifice, they can no longer “maintain payment on the mortgage and cover basic living expenses at the same time". (see HAMP Directive)

To demonstrate this, applicants are required to submit recent paystubs and bank statements. The statements are to help further corroborate the income they report (lest they forget to include all of their paystubs) and also to demonstrate that their monthly expenses are as described on their application. Which is to say that they have already ‘cut back to the bone’ and STILL are unable to make ends meet.

So how do these look in practice? The very first ‘HAMPlication’ that your correspondent pulled up recently showed a wanton disregard for minimizing spending. On the contrary, it looked like “cutting back” for this applicant does not involve such Draconian cuts as eliminating:

• visits to the tanning salon

• the nail spa

• some kind of gourmet produce market (have you seen the price of arugula?)

• various liquor stores

• A DirecTV bill that must involve some serious premium programming or pay-per-view events (or both?).

• And over $1,700 in retail purchases, including: Best Buy, Baby Gap, Brookstone, Old Navy, Bed, Bath & Beyond, Home Depot, Macy’s, Pac Sun, Urban Behavior, Sears, Staples, and Footlocker.

And that was just in one month! They were seeking to reduce a $1,880 mortgage payment that had just gotten to be a real cramp to their ability to keep a roof over their heads.

I’d like to say this is the exception, but it’s much closer to the norm. Many people who request HAMP modifications submit bank statements that demonstrate little if any “belt-tightening” going on.

Somehow, we now expect the same people who asked for ‘liar’s loans’ to be truthful on when it comes to ‘hardship affidavits’?

More on Existing Home Sales and Inventory

by Calculated Risk on 3/23/2010 11:22:00 AM

Earlier the NAR released the existing home sales data for February; here are a couple more graphs ...  Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows NSA monthly existing home sales for 2005 through 2010 (see Red columns for 2010).

Sales (NSA) in February 2010 were 7.9% higher than in February 2009, and 3.2% lower than in February 2008.

We will probably see an increase in sales in May and June because of the tax credit, however I expect to see existing home sales below last year later this year.

The second graph shows the Year-over-year change in reported existing home inventory. There was a rapid increase in inventory in the 2nd half of 2005 (that helped me call the peak of the bubble), and the YoY inventory has been decreasing for the last 19 months. However the YoY decline is getting smaller - even with a large reported inventory (and probably more shadow inventory). This is something to watch.

There was a rapid increase in inventory in the 2nd half of 2005 (that helped me call the peak of the bubble), and the YoY inventory has been decreasing for the last 19 months. However the YoY decline is getting smaller - even with a large reported inventory (and probably more shadow inventory). This is something to watch.

This slow decline in the inventory is especially concerning with 8.6 months of supply in February - well above normal.

Existing Home Sales Decline in February

by Calculated Risk on 3/23/2010 10:00:00 AM

The NAR reports: February Existing-Home Sales Ease with Mixed Conditions Around the Country

Existing-home, which are finalized transactions that include single-family, townhomes, condominiums and co-ops, slipped 0.6 percent nationally to a seasonally adjusted annual rate of 5.02 million units in February from 5.05 million in January, but are 7.0 percent higher than the 4.69 million-unit pace in February 2009.

...

Total housing inventory at the end of February rose 9.5 percent to 3.59 million existing homes available for sale, which represents an 8.6-month supply at the current sales pace, up from a 7.8-month supply in January. Raw unsold inventory is 5.5 percent below a year ago.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows existing home sales, on a Seasonally Adjusted Annual Rate (SAAR) basis since 1993.

Sales in February 2010 (5.02 million SAAR) were 0.6% lower than last month, and were 7.0% higher than February 2009 (4.69 million SAAR).

Sales surged last November when many first-time homebuyers rushed to beat the initial expiration of the tax credit. There will probably be another increase in May and June this year, although that will be probably be smaller than the November increase. Note: existing home sales are counted at closing, so even though contracts must be signed in April to qualify for the tax credit, buyers have until June 30th to close.

The second graph shows nationwide inventory for existing homes.

The second graph shows nationwide inventory for existing homes.According to the NAR, inventory increased to 3.59 million in February from 3.27 million in January. The all time record high was 4.57 million homes for sale in July 2008.

Inventory is not seasonally adjusted and there is a clear seasonal pattern - inventory should increase further in the spring.

The last graph shows the 'months of supply' metric.

The last graph shows the 'months of supply' metric.Months of supply increased to 8.6 months in February.

A normal market has under 6 months of supply, so this is high - and probably excludes some substantial shadow inventory.

I'll have more later ...

Geithner on Fannie and Freddie

by Calculated Risk on 3/23/2010 08:21:00 AM

From Bloomberg: Treasury’s Geithner Urges End to Fannie, Freddie ‘Ambiguity’

U.S. Treasury Secretary Timothy F. Geithner said the government should end the “ambiguity” over its involvement in mortgage finance companies Fannie Mae and Freddie Mac.Here is Geithner's testimony (ht TD) Some excerpts (note: Embargo was broken by the Financial Services Committee and several web sites):

“Private gains can no longer be supported by the umbrella of public protection, capital standards must be higher and excessive risk-taking must be appropriately restrained,” Geithner said in testimony prepared for the House Financial Services Committee that was obtained by Bloomberg News. The hearing is scheduled for today at 10 a.m. in Washington.

The Administration has defined a framework of objectives for reform of the mortgage finance system. A reformed housing finance system should deliver stability and efficiency to the housing market, while minimizing the risks and costs borne by the American taxpayer.NOTE: 10 AM ET embargo was broken by several web sites before this was posted.

Objectives of Reform

In considering reform, the Administration will be guided by the view that a stable and wellfunctioning housing finance market should achieve the following objectives:The housing finance system could be redesigned in a variety of ways to meet these objectives. However, the Administration believes that any system that achieves these goals should be characterized by:Widely available mortgage credit. Mortgage credit should be available and distributed on an efficient basis to a wide range of borrowers, including those with low and moderate incomes, to support the purchase of homes they can afford. This credit should be available even when markets may be under stress, at rates that are not excessively volatile. Housing affordability. A well-functioning housing market should provide affordable housing options, both ownership and rental, for low- and moderate-income households. The government has a role in promoting the development and occupancy of affordable single- and multi-family residences for these families. Consumer protection. Consumers should have access to mortgage products that are easily understood, such as the 30-year fixed rate mortgage and conventional variable rate mortgages with straightforward terms and pricing. Effective consumer financial protection should keep unfair, abusive or deceptive practices out of the marketplace and help to ensure that consumers have the information they need about the costs, terms, and conditions of their mortgages. Financial stability. The housing finance system should distribute the credit and interest rate risk that results from mortgage lending in an efficient and transparent manner that minimizes risk to the broader financial and economic system and does not generate excess volatility. The mortgage finance system should not contribute to systemic risk or overly increase interconnectedness from the failure of any one institution. Alignment of incentives. A well functioning mortgage finance system should align incentives for all actors – issuers, originators, brokers, ratings agencies and insurers – so that mortgages are originated and securitized with the goal of long-term viability rather than short term gains. Avoidance of privatized gains funded by public losses. If there is government support provided, such as a guarantee, it should earn an appropriate return for taxpayers and ensure that private sector gains and profits do not come at the expense of public losses. Moreover, if government support is provided, the role and risks assumed must be clear and transparent to all market participants and the American people. Strong regulation. A strong regulatory regime should (i) ensure capital adequacy throughout the mortgage finance chain, (ii) enforce strict underwriting standards and (iii) protect borrowers from unfair, abusive or deceptive practices. Regulators should have the ability and incentive to identify and proactively respond to problems that may develop in the mortgage finance system. Standardization. Standardization of mortgage products improves transparency and efficiency and should provide a sound basis in a reformed system for securitization that increases liquidity, helps to reduce rates for borrowers and promotes financial stability. The market should also have room for innovations to develop new products which can bring benefits for both lenders and borrowers. Support for affordable single- and multifamily-housing. Government support for multifamily housing is important and should continue in a future housing finance system to ensure that consumers have access to affordable rental options. The housing finance system must also support affordable and sustainable ownership options. Diversified investor base and sources of funding. Through securitization and other forms of intermediation, a well functioning mortgage finance system should be able to draw efficiently upon a wide variety of sources of capital and investment both to lower costs and to diversify risk. Accurate and transparent pricing. If government guarantees are provided, they should be priced appropriately to reflect risks across the instruments guaranteed. If there is crosssubsidization in the housing finance system, care must be exercised to insure that it is transparent and fully consistent with the appropriate pricing of the guarantee and at a minimal cost to the American taxpayer. Secondary market liquidity. Today, the US housing finance market is one of the most liquid markets in the world, and benefits from certain innovations like the “to be announced” (or TBA) market. This liquidity has provided a variety of benefits to both borrowers and lenders, including lower borrowing costs, the ability to “lock in” a mortgage rate prior to completing the purchase of a home, flexibility in refinancing, the ability to pre-pay a mortgage at the borrowers’ discretion and risk mitigation. This liquidity also further supports the goal of having well diversified sources of mortgage funding. Clear mandates. Institutions that have government support, charters or mandates should have clear goals and objectives. Affordable housing mandates and specific policy directives should be pursued directly and avoid commingling in general mandates, which are susceptible to distortion.