RSS Feed

RSS Feed by Calculated Risk on 12/12/2006 09:52:00 AM

Tuesday, December 12, 2006

Tanta on Fitch 2007 Global Structured Outlook

Tanta comments on the Fitch’s 2007 Global Structured Finance Outlook

On RMBS:

“More borrowers today than historically are sensitive to a slowdown in HPA due to the increased amount of leverage assumed to afford the higher house prices of recent years. For the entire non-agency sector [prime jumbo plus Alt-A plus subprime], combined LTVs have increased to 83% in 2006 to date from 73% in 2002. The increase in combined LTVs has been driven by a growing number of “combination” first and second liens (also known as “piggyback” second liens), which allow borrowers to purchase homes with little or no downpayment. Also, since 2002, debt-to-income ratios (“DTIs”) are up on average from 37% to 41%. The increase in DTIs is likely understated as the percentage of borrowers choosing “stated-income” documentation programmes has increased to 60% this year from 37% in 2002. Fitch has not seen any strong indications that the trend of increased leverage is abating and the trend will likely continue through 2007.” [emphasis added]Tanta: So we have guidance adoption pushing subprime borrowers into 40-year loans. Can anyone out there sketch a pricing model that would make a 40Y FRM affordable to your average overleveraged deeply indebted subprime borrower? Or, alternately, model loss severity expectations on a slowly amortizing 40Y ARM that is a substantial improvement over an IO? I thought not.

“Under these [Nontraditional Mortgage] guidelines, originators will have to qualify borrowers at a fully indexed, fully amortising rate. Since these guidelines are generally already practiced for prime and Alt-A IO products, the change will likely have the greatest impact on sub-prime IO loan originations and, to a lesser degree, Alt-A option ARM originations. Sub-prime IO borrowers have traditionally been qualified at the IO payment and some Alt-A originators [can anyone say WaMu?] have not used the fully indexed rate to qualify borrowers for option ARMs. Fitch expects the new guidelines to push more subprime borrowers into 40-year loans and to result in a decline in option ARM issuance in the Alt-A sector.”

Prime Jumbos:

“Credit characteristics of loans originated in 2006 have continued the trend in recent years of weakening risk attributes in the sector. Averages show a trend of increased risk every year since 2003 in almost every major category, with the exception of Fair Isaac Corp (“FICO”) score. The weighted average LTV ratio in 2006 (70.6%) is the highest since 2001. The 2006 DTI ratio (37%), non-owner occupied property (9%) and non-full documentation loans (55%) are all at the highest levels on record. Additionally, more prime borrowers are choosing mortgage products with interest-rate and payment shock risk. Hybrid ARM IO loans now make up the greatest share of new originations. . . . Although still early, there appears to be a marked distinction between fixed-rate and ARM loans when the performance of recent origination is compared with prior vintages at comparable points in their seasoning. Both 15- and 30-year fixed-rate loans originated in 2005 and 2006 are outperforming prior vintages to date when age-adjusted. Conversely, recently originated ARM loans are underperforming prior vintages. The 2006 vintage ARM performance has the highest age-adjusted delinquency of any vintage since 2001.”Alt-A:

“Credit attributes for Alt-A loans originated in 2006 continue to exhibit the trend towards increased borrower leverage in recent years. While the reported LTV ratios of loans securitised have remained relatively stable, the percentage of loans reporting a subordinate second lien has more than doubled since 2002. Additionally, the weighted average DTI ratio (37%) and the percentage of borrowers using non-full documentation (82%) are both at all-time highs. The high percentage of borrowers with non-full documentation was driven by the growing number of option ARM loans, almost 90% of which chose non-full documentation in 2006. Affordability products dominate the sector, with approximately 75% of the Alt-A loans originated in 2006 falling into that category. . . . The rise in recent vintage delinquency is dramatic relative to earlier vintage option ARM performance, but remains very low in absolute terms and well below the delinquency of other Alt-A products. However, the increase in delinquency does not fully reflect the deterioration in performance of that product. The dramatic increase in short-term rates between 2003 and 2006 has meant much higher interest rates for option ARM borrowers once the teaser period ended. Option ARM borrowers from the 2006 vintage are facing coupons above 7% by month six, several hundred basis points higher than option ARM borrowers from prior vintages at similar points in their seasoning. The result has been a significant increase in the number of borrowers choosing the minimum payment, which negatively amortises the loans. Over 90% of option ARM borrowers from the 2006 vintage are already negatively amortising. However, while the incidence of this is high, the amount of the negative amortisation is relatively small to date. Of those borrowers in this situation, the average rate of negative amortisation is between 1-2% a year. [emphasis added]

Tanta: 90% of Option ARMs originated in 2006 were low or no doc. The rate shock at reset is extreme. Plus 90% of them are negatively amortizing at something like 100% of nominal house price appreciation (at best). But they had a nice-looking FICO when they were originated!

Subprime:

"[T]he loans originated in 2006 have exhibited increased leverage from prior years. While the LTV ratios of the loans securitised has remained relatively stable in recent years, the number of borrowers with reported subordinate second liens has almost doubled since 2004. Additionally, the weighted-average DTI ratio (42%) and the percentage of borrowers choosing non-full documentation (44%) in 2006 are both at all-time highs. [emphasis added]Tanta: A “2/28 hybrid” means the rate is fixed for two years, and then adjusts each 6 months for the remaining 28 years based on the six-month LIBOR. The margin over index could be anything from 300 to 450 basis points. And we are seeing record delinquencies in the first two years, during the fixed period with a discounted start rate.

“The performance of loans originated in 2005 and 2006 generally reflects the increased leverage and delinquencies are up across all product types relative to the age-adjusted delinquency of the 2003 and 2004 vintages. However, the largest challenge of the 2005 and 2006 vintages still lies ahead when roughly three-quarters of those borrowers are required to make a higher monthly payment with the scheduled rate adjustment at month 24. The 2/28 hybrid ARMs originated in 2005 and 2006 have an initial rate below their fully indexed rate and are scheduled to face a rate increase . . . even if Libor remains flat.”

Monday, December 11, 2006

Brokers' Commissions

by Calculated Risk on 12/11/2006 07:16:00 PM

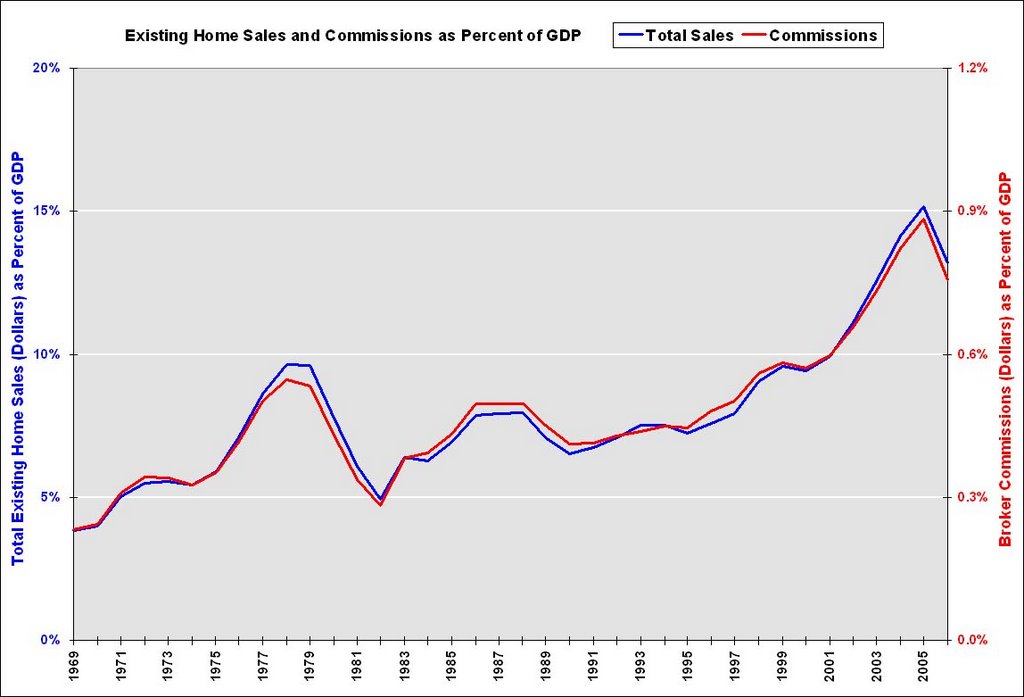

One of the incredible stories of the housing boom was the surge in brokers' commissions over the last 5 years. Brokers' commissions are included in residential investment, and are the third largest category behind new single family residential construction and home improvements. See BEA GDP underlying Table 5.4.5BU, line 43. Click on graph for larger image.

Click on graph for larger image.

This graph shows the dollar value of existing home sales as a percent of GDP, and the dollar value of commissions as a percent of GDP. Commissions have averaged approximately 6% of gross sales for years. (2006 estimated from first three quarters).

My initial reaction was that the surge in commissions, and the total value of existing home sales, was primarily related to the recent rapid increase in house prices.

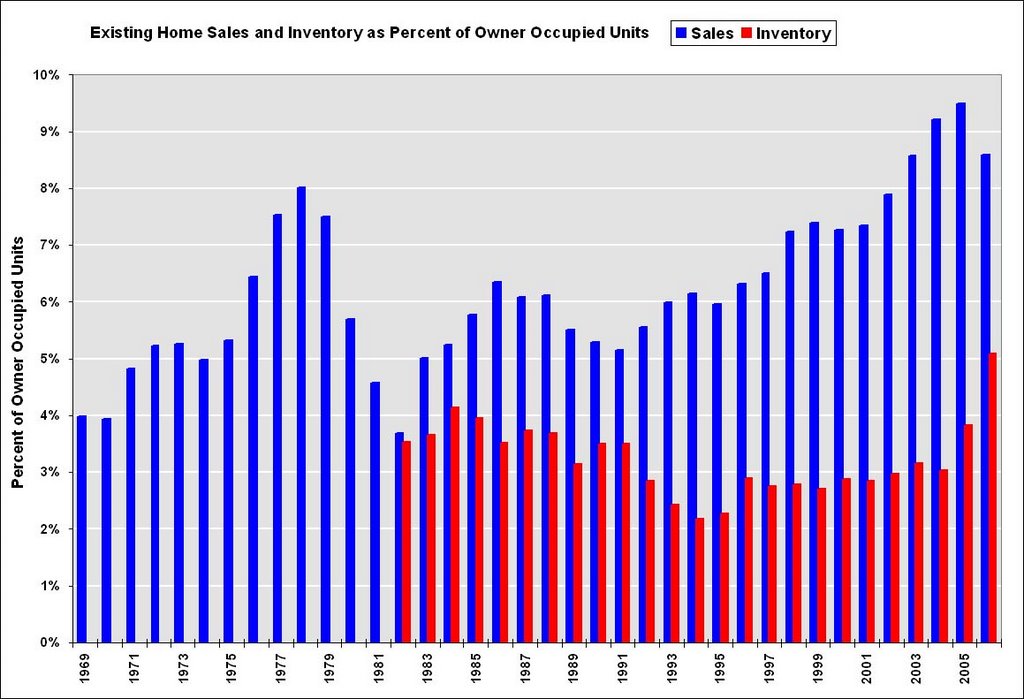

Actually the increase in house prices is the second most important factor with respect to the rapid increase in commissions (as percent of GDP). The most important factor was the increase in turnover of the existing stock. The second graph shows existing home sales and inventory normalized by the number of owner occupied units. This shows the extraordinary level of sales for the last few years, reaching 9.5% of owner occupied units in 2005. The median level is 6.0% for the last 35 years. Inventory is only available since 1982.

The second graph shows existing home sales and inventory normalized by the number of owner occupied units. This shows the extraordinary level of sales for the last few years, reaching 9.5% of owner occupied units in 2005. The median level is 6.0% for the last 35 years. Inventory is only available since 1982.

The primary factor in the rapid increase in commissions, as a percent of GDP, was the increased turnover of existing stock. If sales return to normal (6% of existing stock per year), commissions will drop dramatically from the levels of recent years.

When brokers talk about the housing market returning to "normal", I don't think they mean sales dropping to 6% of existing stock (or about 4.5 million units per year currently). From CNN: Realtors: Home sales may keep falling in 2007

Next year will likely bring a second annual decline in existing home sales, the National Association of Realtors predicted Monday.So NAR is forecasting another year with sales above 8% of existing stock; far above the median level of the last 35 years.

Sales of existing homes are expected to decline 8.6 percent to 6.47 million for 2006 and contract another 1 percent to 6.40 million units next year.

Still, the housing sector should see a rebound by the end of next year, said David Lereah, the association's chief economist.

Office of Thrift Supervision: The National Housing Forum

by Calculated Risk on 12/11/2006 06:35:00 PM

The Office of Thrift Supervision hosted a National Housing Forum today. An archived recording will be available soon.

The forum included four panels:

Panel 1: Outlook for the U.S. Housing Market and Potential Impact on Banks and Thrifts

Panel 2: Challenges & Emerging Risks in the Home Mortgage Business

Panel 3: Critical Consumer Protection Issues in Housing Finance Today

Panel 4: Mortgage Fraud

Here are some excerpts from an AP article: Mortgage delinquencies a rising threat

Mortgage delinquency and foreclosure rates are on the rise, and the impact could be greatest on low-income families that took out higher-interest loans for risky borrowers, some experts said Monday.

...

Some experts are concerned that the increase in mortgage foreclosure rates could affect the banking system's financial health.

There have started to be "early signs of credit distress" in financial institutions' holdings of so-called "subprime" mortgages, especially in California, Richard Brown, chief economist for the Federal Deposit Insurance Corp., said at the conference.

...

William Longbrake, a senior policy adviser to the Financial Services Roundtable, an industry group, said he is among a minority of experts "who believe the worst is still ahead in the housing market" for home prices to continue to fall.

"There is worse to come. ... The bottom is probably still many months ahead," Longbrake said. He noted that the rise in delinquencies and foreclosures in subprime mortgages particularly affects low-income families.

Mortgage defaults could snowball in the coming months, a situation that bears close watching, he said.

LA Times: A loan that'll get ugly fast

by Calculated Risk on 12/11/2006 10:55:00 AM

From David Streitfeld, Times Staff Writer: A loan that'll get ugly fast

EVERY day, Will Hertzberg owns a little less of his three-bedroom house in Corona.And here are his payment options:

Like hundreds of thousands of other homeowners around the state, Hertzberg has a mortgage that lets him choose how much he pays each month.

Like many of them, he always chooses to pay as little as possible.

For the moment, this allows the 56-year-old Hertzberg to continue living in his tract home despite being only marginally employed. But his debt is swelling, and his mortgage company controls his fate.

"I am rather screwed," he said.

One of his options is to pay $2,513 a month. That would cover the principal and interest as if it were a traditional 30-year loan.Hertzberg is not alone. The use of option ARMs have really taken off, especially in California:

A second possibility is to pay $2,279, which would cover only the interest.

But each month he always takes the cheapest option: paying $1,106 and promising to make up the shortfall later.

In 2003, only about 8 of every 1,000 people buying a home or refinancing a mortgage in California got a pay option loan ...But the impact is a still a "big unknown":

Last year, 1 in 5 loan applicants got one.

In the first eight months of 2006... Nearly 1 in 3 California loan applicants are now choosing them.

Just how many of these homeowners will end up in trouble is the big unknown for the housing market and the economy. Although many economists expect the loans to prompt a certain degree of turmoil, they don't think it would cause a recession.UPDATE: And from Reuters: U.S. home lenders brace for bad news, legislation

During the recent U.S. housing boom, mortgage lenders touted so-called exotic mortgages that allowed people to buy houses they could not otherwise afford. Now those lenders are bracing for the not-so-happy story of borrowers...

...

A mortgage survey due on Wednesday is expected to show that more and more Americans are in danger of losing their homes. The quarterly report from the Mortgage Bankers Association is also expected to show that the same mortgage products that helped send the housing market into the stratosphere are now weighing homeowners down.

In a hint at Wednesday's data, October saw more foreclosure actions than any other month this year ...

Saturday, December 09, 2006

Northern Trust Economic Outlook

by Calculated Risk on 12/09/2006 07:25:00 PM

Congratulations to Paul Kasriel, the recipient of the 2006 Lawrence R. Klein Award for Blue Chip Forecasting Accuracy:

"Kasriel [was] honored for having the most accurate economic forecast among the Blue Chip survey participants for the years 2002 through 2005."From the Northern Trust December Economic Outlook:

We continue to expect sub-2% annualized real GDP growth in the final quarter of this year and have revised down our first-quarter 2007 forecast to 1.8% from 2.0% -- not much more than a rounding error. In addition to the fifth consecutive quarterly decline in real residential investment expenditures, we expect a considerable deceleration in the growth of real business expenditures for capital equipment and software in the fourth quarter, based on the weak October shipments data for nondefense capital goods excluding aircraft. ...

Based on the excesses of the past real estate boom, the considerable supply overhang and the typical peak-to-trough behavior of residential investment expenditures, we continue to expect that the trough of the housing recession is not near at hand....

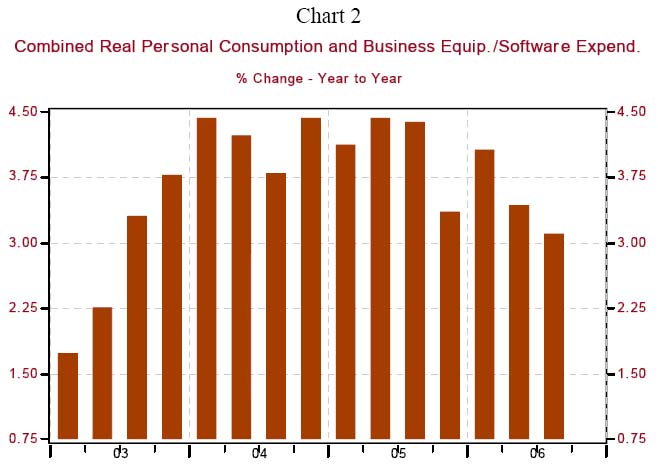

Click on graph for larger image.

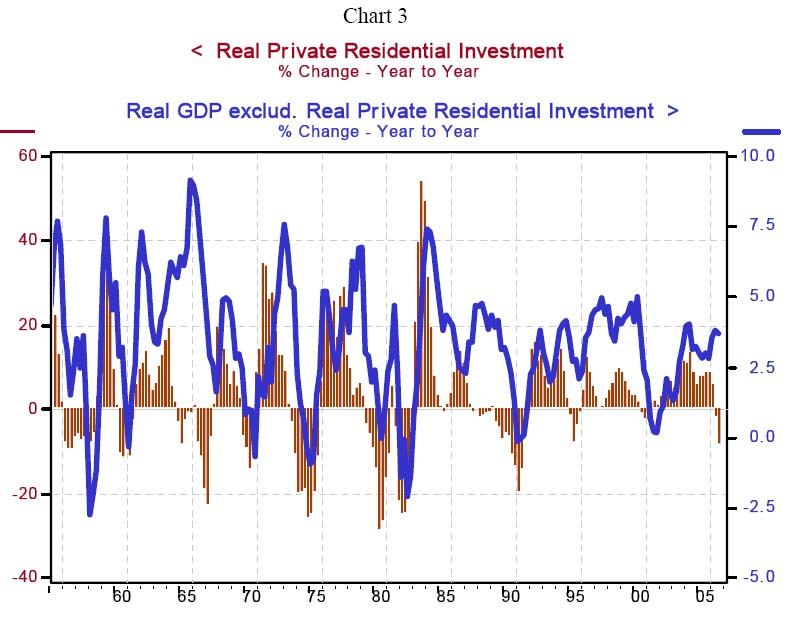

Click on graph for larger image.We continue to hear that the weakness in housing has not spread to other parts of the economy. To that we say “Not so” and “You ain’t seen nothin’ yet.” As Chart 2 shows, the year-over-year growth in combined real personal consumption and business equipment/software expenditures, at 3.1% in the third quarter, is the slowest since the second quarter 2003 and is down 130 basis points from its year-ago growth. That takes care of the “not so.”

With regard to the “you-ain’t-seen-nothin’-yet” argument, take a look at Chart 3. You don’t have to examine it closely to see that the year-over-year behavior of residential investment expenditures leads the behavior of the rest of the economy. If you did look closely, you would see that the lead time tends to be about two calendar quarters. This implies that even if the trough of the housing recession is at hand, the full ripple effects from the weak housing sector have yet to lap up on the shore of the rest of the economy. Moreover, if the housing-recession trough lies ahead, the wave action from this sector will continue through most of 2007.Currently Northern Trust is forecasting 1.6% real annualized GDP growth in Q4, and 1.8%, 2.0%, 2.4% and 3.0% for each successive quarter in 2007. This is a forecast for sluggish growth in 2007, without a recession, and is similar to the Anderson forecast.

Another reason we believe the recession in housing will have a lingering retarding effect on economic activity concerns its impact on the “home ATM”, i.e., mortgage equity withdrawal (MEW). With home prices either falling or advancing more slowly, depending on the price series used, it stands to reason that growth in homeowners’ equity would be slowing.... So, the home ATM is not refilling as rapidly as it has in recent years. The slower growth in home equity along with the higher level of mortgage and home equity loan interest rates is slowing MEW, an important source of funding for household spending in recent years.

Friday, December 08, 2006

Freddie Mac: Anatomy of a Housing Recovery

by Calculated Risk on 12/08/2006 03:20:00 PM

From Freddie Mac chief economist Frank Nothaft, et al: Anatomy of a Housing Recovery

"The housing market has been central to the economic outlook for the past several years. A buoyant residential sector provided critical support in the recovery from the 2001 recession. More recently, the housing slowdown since mid-2005 has been instrumental in helping realize the Fed's goal of moderating economic growth, in order to nip inflationary pressures in the bud. Over the next several quarters, housing will again be key to the outlook, as a prolonged downturn could threaten more severe consequences for the overall economy, while a housing recovery could engender a broader upturn. Given the importance of housing at the current juncture, two key questions arise: What will a housing recovery look like; and, When will it arrive?

Previous housing booms help provide a historical context. Residential investment as a share of GDP, a broad indicator of overall housing activity, rose to nearly 6 percent in both 1973 and 1978, compared to a long-run average of 4 ½ percent. The investment share subsequently slid to approximately 4 percent over the ensuing six to eight quarters, before stabilizing. After reaching a trough, real residential investment rose in the following four quarters. Price appreciation (as measured by the yearly change in repeat-sales indexes) tends to slow after a peak, but did not turn negative on a national basis after these booms. Rather, the boom periods are generally followed by extended sluggish price gains, though economically depressed local and regional markets may register outright declines."

Click on graph for larger image.

Click on graph for larger image.Residential investment (RI) has now fallen to 5.7% of GDP from the peak of 6.3% in the second half of 2005.

"During the recent boom, residential investment rose to a slightly higher share of GDP, reaching 6 ¼ percent in the second half of 2005. Investment has been declining rapidly since then, however, falling at an 18 percent annual rate (adjusted for inflation) in the third quarter, and is on track to a similar decline in the current period. This trend would reduce residential investment relative to GDP to 4 ½ percent in the second quarter of 2007, a change in line with declines in previous episodes, and over a similar six- to eight-quarter time frame."In the previous cycles mentioned, starting in 1973 and 1978, residential investment as a percent of GDP eventually declined to 3.7% and 3.2% respectively. To reduce residential investment relative to GDP to 4%, the current trend would have to continue through all of 2007. The Freddie Mac analysis excludes the early '90s bust: residential investment peaked at only 5.0% of GDP and declined over 13 quarters to 3.3% of GDP in early 1991.

I'm not sure why Nothaft is suggesting residential investment will only decline to the long-run average of 4 ½ percent. Also, for the previous residential investment downturns, the period from peak to trough were: early '70s - 8 quarters, late 70's, early '80s - 16 quarters, and late 80's, early '90s - 18 quarters. So the "six to eight quarters" timeframe seems optimistic.

"By contrast, forecasts of a more serious and prolonged housing slowdown fall well outside the range of post-war experience. For example, consider an annualized 18 percent decline in residential construction every quarter through end-2008. Under such a scenario, the drop in residential investment relative to GDP would be 50 percent greater than what occurred during the 1973-74 recession, reaching roughly 3 percent, a result worse than during even the most severe post-war recessions."The bottom of three previous troughs were: 3.7%, 3.3% and 3.2% relative to GDP. At the current rate of decline, the current downturn could last to about mid-2008 to reach about the same level. And the duration would only be about 11 quarters - shorter than two of the three previous downturns.

"... We expect housing markets to stabilize some time during the first half of 2007...."At each step of this analysis, Dr. Nothaft has shaded to the most positive view. The three previous cycles lasted from seven to eighteen quarters, and that became "six to eight quarters". The three previous bottoms were all in the mid 3% range (3.2% to 3.7%), yet Dr. Nothaft forecast the bottom of the current decline at the long-run average of 4 ½ percent. And, as Nothaft noted, a decline at the current pace to the long-run average would persist through mid-2007, but then Nothaft forecast the market to "stabilize some time during the first half of 2007".

If we are using a "historical context", why not forecast a more normal cycle downturn of 11 quarters and a bottom of 3.4%? Of course the bottom wouldn't occur until Q2 2008 at the current pace.

Mortgage Equity Withdrawal Declines in Q3

by Calculated Risk on 12/08/2006 11:55:00 AM

A few comments on Mortgage Equity Withdrawal (MEW):

1) The reason we are interested in MEW is that a portion of MEW is probably flowing to consumption and boosting GDP. As MEW declines, consumption growth will likely slow. Unfortunately MEW is difficult to calculate, and the percentage of MEW that flows to consumption is uncertain.

2) MEW is not an official statistic. Many people refer to the work of Greenspan and Kennedy: Estimates of Home Mortgage Originations, Repayments, and Debt On One-to-Four-Family Residences.

3) MEW could be calculated as the quarterly increase in mortgage debt minus the following: investment in new homes, investment in home improvements, commissions on homes sold, loan origination fees (including points), miscellaneous fees, capital gains (on homes) and other home sale related taxes. The result would be the total amount available for consumption. Some of this data is readily available, some is not.

4) I've suggested a simple and quick method of calculating MEW. I use the quarterly increase in the mortgage debt, and subtract 70% of Residential Investment (from the BEA). This is just a rough estimate of MEW. Click on graph for larger image.

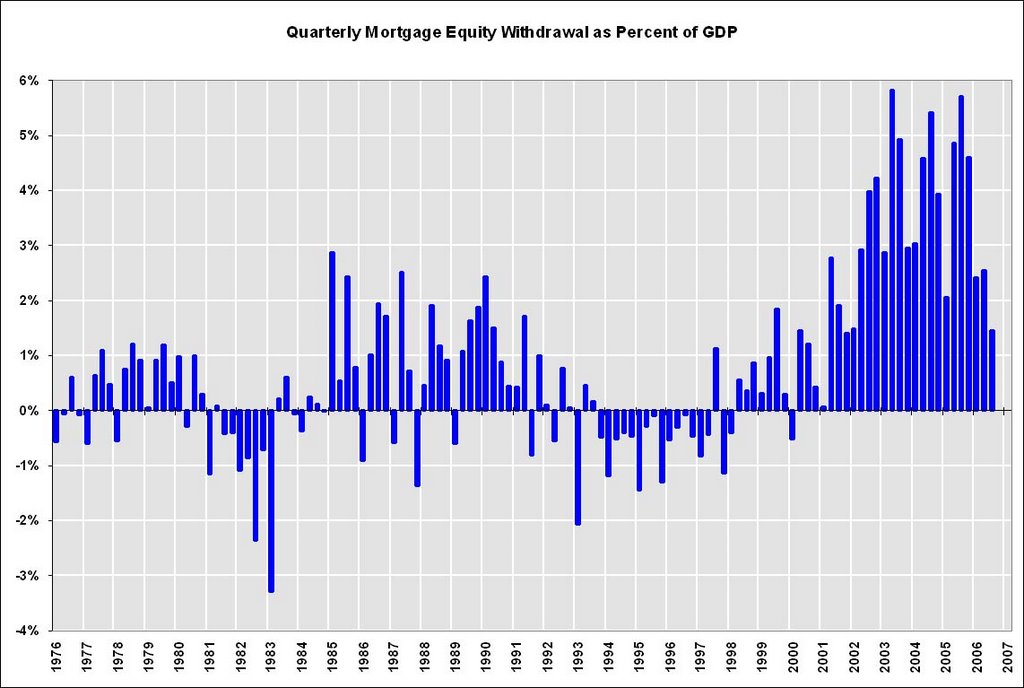

Click on graph for larger image.

Using the simple approach, this graph shows quarterly MEW (not SAAR) as a percent of GDP. This shows MEW has dropped to about 1.5% of GDP in Q3 2006, from close to 6% in Q3 2005.

Since MEW flows to consumption over the next few quarters, this might indicate a slowdown in consumer spending in the near future.

November Employment Report

by Calculated Risk on 12/08/2006 09:44:00 AM

The BLS reports: U.S. nonfarm payrolls rose by 132,000 in November, after a revised 79,000 gain in October. The unemployment rate rose to 4.5% in November, compared to 4.4% in October. Click on graph for larger image.

Click on graph for larger image.

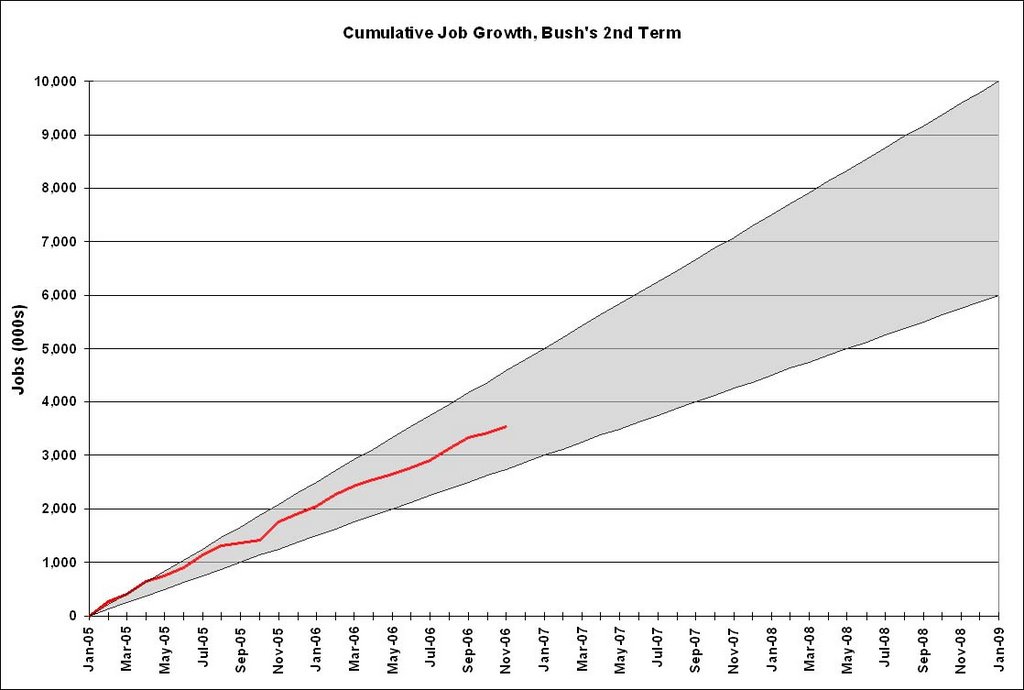

Here is the cumulative nonfarm job growth for Bush's 2nd term. The gray area represents the expected job growth (from 6 million to 10 million jobs over the four year term). Job growth is about in the middle of the expected range.

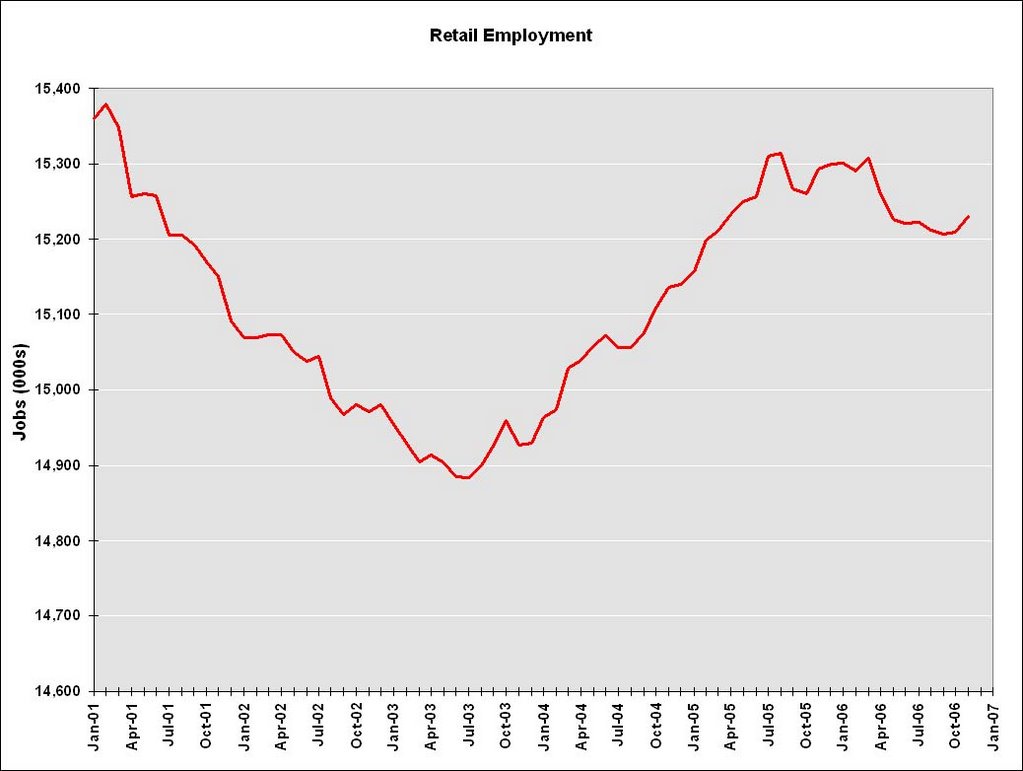

The following two graphs are the areas I've been watching closely: residential construction and retail employment.

Residential construction employment decreased by 15,500 jobs in November and is down 110 thousand, or about 3.3%, from the peak in February. This is the beginning of the loss of several hundred thousand residential construction jobs over the next year or so.

Note the scale doesn't start from zero: this is to better show the change in employment.

Retail employment increased 20,400 jobs in November. The YoY change in retail employment is now -0.4%.

The YoY decrease in retail employment is concerning: see Retail Employment

Overall this is a solid report, but there are weaknesses. It appears nonresidential construction might have peaked too:

Construction employment declined by 29,000 in November, following a loss of similar size in October. The November decline was spread across all component industries.And other weak areas:

Manufacturing employment continued to trend down (-15,000) in November. Motor vehicles and parts lost 7,000 jobs. Employment continued to fall in two construction-related industries: wood products (-6,000) and furniture and related products (-5,000).The expected job losses in residential construction employment has just started, but the spillover to retail isn't significant yet. I expect the rate of residential construction job losses to increase over the next few months.

Thursday, December 07, 2006

Credit Suisse on Homebuilders

by Calculated Risk on 12/07/2006 09:26:00 PM

In a research note titled: "Not So Fast", Credit Suisse' Zelman, et al, offered their top ten reason to downgrade the homebuilding sector.

Some of the reasons were technical or based on valuations, but mostly it was more supply and less demand.

I'm surprised at the percentage of respondents that are expecting to expand next year - I expect 2007 will be worse in every way for the homebuilders than 2006; fewer sales, fewer starts, less employment, lower prices, smaller margins, more homebuilders going under, etc..

Fed: Record Low Percentage Homeowner Equity

by Calculated Risk on 12/07/2006 01:43:00 PM

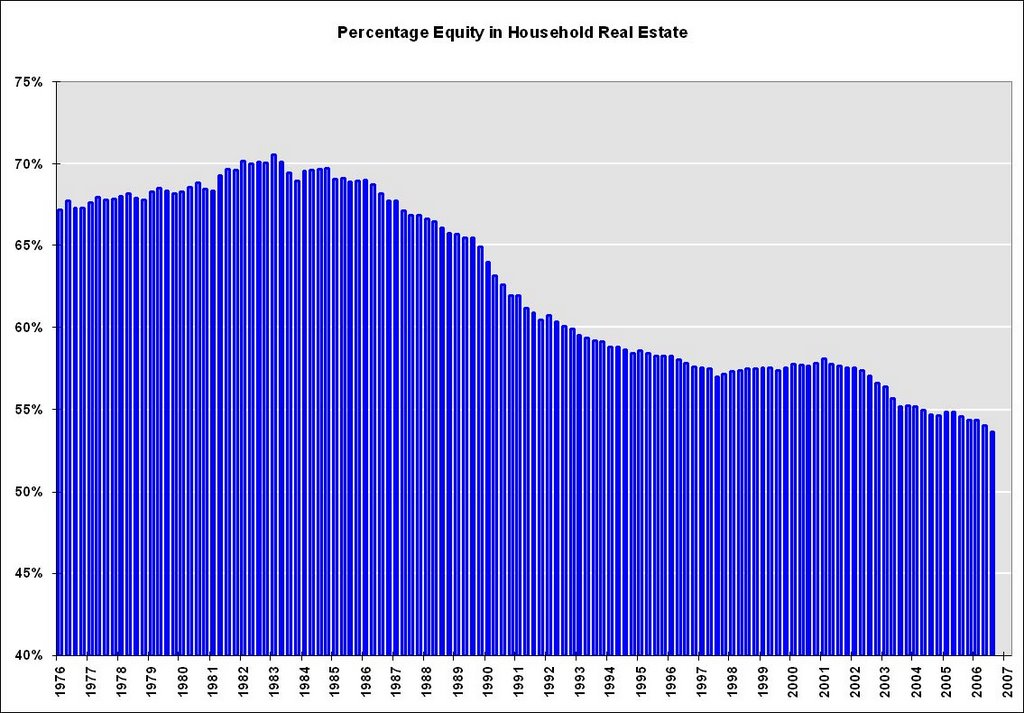

The Fed reported today that houseowner equity, as a percent of market value, fell to a record low 53.6%, compared to 54.0% in Q2, and 54.6% one year ago.

Homeowners borrowed almost the entire amount that their homes increased in value in Q3. Homeowner equity market value increased $194.5 Billion in Q3, to $20.48 trillion. Meanwhile homeowners mortgage debt increased $180 Billion. So homeowners borrowed 92% of the increase in market value.  Click on graph for larger image.

Click on graph for larger image.

Note: Graph doesn't start at zero to better show change in percent equity.

This may sound like a high percentage of equity, but according to Robert Broeksmit, Chairman of the Residential Board of Governors, Mortgage Bankers Association (from the Senate hearing on Wednesday):

"More than a third of homeowners, approximately 34 percent, own their homes free and clear."So many of the remaining homeowners have a very low percentage of equity. Note: Typically free and clear homes are older and have a lower market value than newer homes - so you can't just subtract 34% from 53.6% to find the percent equity of homeowners with mortgages. But this probably indicates that more and more homeowners have maxed out their "home ATM".

If house prices stabilize or fall over the next few years, the percentage equity will drop sharply (see 1990). This will make it more difficult for homeowners to extract equity from their homes.