RSS Feed

RSS Feed by Calculated Risk on 12/08/2006 11:55:00 AM

Friday, December 08, 2006

Mortgage Equity Withdrawal Declines in Q3

A few comments on Mortgage Equity Withdrawal (MEW):

1) The reason we are interested in MEW is that a portion of MEW is probably flowing to consumption and boosting GDP. As MEW declines, consumption growth will likely slow. Unfortunately MEW is difficult to calculate, and the percentage of MEW that flows to consumption is uncertain.

2) MEW is not an official statistic. Many people refer to the work of Greenspan and Kennedy: Estimates of Home Mortgage Originations, Repayments, and Debt On One-to-Four-Family Residences.

3) MEW could be calculated as the quarterly increase in mortgage debt minus the following: investment in new homes, investment in home improvements, commissions on homes sold, loan origination fees (including points), miscellaneous fees, capital gains (on homes) and other home sale related taxes. The result would be the total amount available for consumption. Some of this data is readily available, some is not.

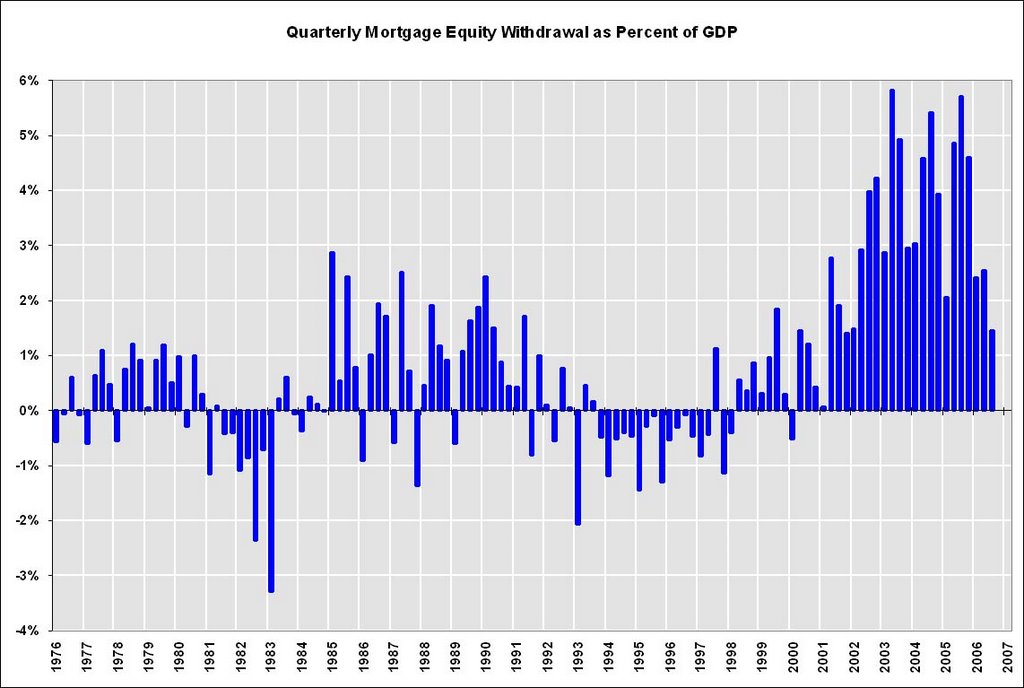

4) I've suggested a simple and quick method of calculating MEW. I use the quarterly increase in the mortgage debt, and subtract 70% of Residential Investment (from the BEA). This is just a rough estimate of MEW. Click on graph for larger image.

Click on graph for larger image.

Using the simple approach, this graph shows quarterly MEW (not SAAR) as a percent of GDP. This shows MEW has dropped to about 1.5% of GDP in Q3 2006, from close to 6% in Q3 2005.

Since MEW flows to consumption over the next few quarters, this might indicate a slowdown in consumer spending in the near future.