RSS Feed

RSS Feed by Calculated Risk on 9/28/2010 12:26:00 PM

Tuesday, September 28, 2010

Misc: Case-Shiller, Manufacturing Surveys, QE2 and Europe

The headlines on Case-Shiller seemed contradictory this morning. Here are a few examples:

From the Financial Times: US home prices slip in July

From the WSJ: Home Prices Rose in July

From CNBC: US Home Prices Slipped In July And May Stabilize Near Lows

From MarketWatch: Home price growth slows in July

From HousingWire: S&P/Case-Shiller 20-city composite index rose 0.6% for July

The reason for the confusion is S&P Case-Shiller reports both seasonally adjusted (SA), and not seasonally adjusted (NSA) data. Because of concerns about the impact of foreclosures and government programs on prices, S&P switched to reporting NSA numbers in their press release, but many analysts are still using the SA numbers (I reported the SA numbers - see this post for the SA graphs from earlier this morning).

The important points are:

1) this is a three month average of May, June, and July. Seasonally this is the strongest time of the year for house prices.

2) sales collapsed in July, so the next report (for June, July and August) will probably show falling prices.

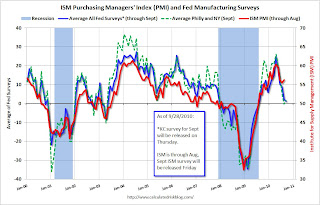

Here is an update to the graph comparing the regional Fed surveys with the ISM manufacturing survey, including the Richmond survey released this morning (Kansas City will be released Thursday):

Click on graph for larger image in new window.

Click on graph for larger image in new window.For this graph I averaged the New York and Philly Fed surveys (dashed green, through September), and averaged five surveys including New York, Philly, Richmond, Dallas and Kansas City (blue, through September - KC through August).

The Institute for Supply Management (ISM) PMI (red) is through August (right axis).

Last month, when the ISM survey came in slightly better than expected, I wrote: "Based on this graph, I'd expect either the Fed surveys to bounce back in September - or the ISM to decline." So far there has been little "bounce back" in the Fed surveys - so I expect a decline in the ISM survey.

The consensus is for a decline in ISM Manufacturing Index to 54.5 in September from 56.3 in August.

There was a very important article from Jon Hilsenrath at the WSJ yesterday: Fed Weighs New Tactics to Bolster Recovery (note: many people think that Hilsenrath has taken over Greg Ip's role (now at the Economist) and leaks to Hilsenrath might be part of the Fed's communication strategy).

I reviewed the article here, but the key points are the Fed is debating between announcing "massive bond purchases with a finite end" and a "smaller-scale program that they could adjust" over time. Based on the article, it appears the Fed is leaning towards the latter (small-scale program).

Although QE2 isn't a done deal, the odds are very high that the next round will be announced on November 3rd at 2:15 PM ET.

The crisis is not over in Europe.

From Reuters: Ireland Faces Threat of New Downgrades

Two more credit rating agencies warned Ireland on Tuesday that its debt was at risk of being downgraded further, setting off another leap in borrowing costs and heaping pressure on the government to accelerate the planned late-October release of a budget preview.The Ireland and Portugal to Germany bond spreads have hit new highs again today.