RSS Feed

RSS Feed by Calculated Risk on 3/31/2005 11:07:00 PM

Thursday, March 31, 2005

Mortgage Rates Continue Climb

According to the FreddieMac weekly survey, 30 year fixed rate mortgages averaged 6.04% last week with 0.7 points. Also:

"Five-Year Treasury-indexed hybrid adjustable-rate mortgages (ARMs) averaged 5.43 percent this week, with an average 0.7 points, up from 5.35 last week. There is no annual historical information for last year since Freddie Mac only began tracking this mortgage rate at the start of this year.I would like to point out some quotes from this article "Higher rates dampen home ownership dreams in Bay Area" (hat tip to Ben at thehousingbubble for pointing this out):

One-year Treasury-indexed adjustable-rate mortgages (ARMs) averaged 4.33 percent this week, with an average 0.8 point, up from last week when it averaged 4.24 percent. At this time last year, the one-year ARM averaged 3.46 percent."

In the first two months of 2005, 82 percent of people who bought homes in the nine Bay Area counties and Santa Cruz County got adjustable-rate mortgages, according to DataQuick Information Systems. But buyers who chose a one-year adjustable last year could be facing payment shocks when their loans adjust for the first time this year, [Greg McBride, a senior financial analyst at Bankrate.com] said.First, it is important to note that 82% of buyers in the Bay Area used ARMs! So this is a relevant calculation.

Last spring, a buyer with a $450,000 loan at 3.47 percent had a monthly payment of $2,013.17. This year, with the increase capped at a typical two percentage points, the rate would be 5.47 percent, and the monthly payment would be $2,531.76.

"And you're not done," McBride said, "because this time next year it's likely to adjust again."

Next, we could do a similar calculation with the current rate. An ARM based on the one year treasury is 4.33% (the one year last week was yielding 3.4%). If someone took out a $450,000 loan this week, their monthly payment would be: $2234.86. If the loan increased the maximum, their payments next year would be $2794.18. Ouch!

But there is another interesting calculation. I've seen several analysts arguing that home prices are fundamentally correct assuming buyers only consider their monthly payment when purchasing a house (as opposed to other fundamentals, like replacement cost or buy vs. rent). If we assume $50K down and a $450K loan, a house that was worth $500K last year should only be worth $455K this year - a 9% price decline.

Of course prices of homes in the Bay Area have increased 12% (according to OFHEO) in the San Francisco, San Mateo, and Redwood area last year. Based on this "payment" approach to value, if homes were fairly valued last year, they are now overvalued by about 20%.

Buying GDP Growth with Debt

by Calculated Risk on 3/31/2005 12:43:00 AM

The final fourth quarter GDP numbers were released by the Commerce Department. The headline number was 3.8% annualized GDP growth in the 4th quarter of 2004. That is solid growth and about average for the last 10 years.

However, the growth in the National Debt and household mortgage debt in the 4th quarter, as a percentage of GDP, is the untold story. Here are the numbers for the 4th quarter, 2004:

GDP: $2.999 Trillion ($11.994 Trillion annual rate)

Increase in National Debt: $217 Billion (US Treasury)

Increase in Mortgage Debt: $205 Billion (Federal Reserve: Flow of Funds)

The increase in National and household mortgage debt as % of GDP: 14.1%

This continues a trend over the last four years as depicted in this chart. It appears that we are buying GDP growth with debt. If I was analyzing a company's balance sheet, and I saw this trend, I would be very concerned.

And the 4th quarter was even worse. The increase in debt was 14.1% of GDP.

With all that additional debt, maybe we should be asking why GDP growth was so low!

Wednesday, March 30, 2005

The Thirty Year Hamburger

by Calculated Risk on 3/30/2005 04:29:00 PM

Mortgage defaults are on the rise in Denver. This story says that "soaring foreclosure filings in Arapahoe County for the first three months of this year helped drive metro Denver's foreclosure rate 34 percent higher than the same period of last year and 30 percent higher than the fourth quarter of 2004."

Some interesting quotes:

"Lenders started giving money to people, and it's gotten out of hand," said Jeannie Reeser, public trustee of Adams County. "I am talking to people who have jobs, but their income doesn't come anywhere close to matching their financing."But this post is about hamburgers. And not just any hamburgers; 30 year hamburgers! At the end of the Post article was this comment:

"I am not in a position to say it's faulty lending, but we have too many foreclosures that are on brand-new loans not to conclude that something is wrong," [ said Arapahoe County Public Trustee Mary Wenke].

"Credit is so loose today that I can buy the groceries I need on a credit card, eat the food tonight, discard the food by tomorrow at noon and finance my debt on a 30-year, amortized loan. How stupid is that? But people do it all the time - and then they wonder why they're in foreclosure."The recipe for a 30 year hamburger:

1) Go to your fast food restaurant.

2) Buy a hamburger on your credit card.

3) Refinance your house and payoff your credit debt with a 30-year loan.

I hope it was a great hamburger!

Monday, March 28, 2005

AEI: Greenspan's Second Bubble

by Calculated Risk on 3/28/2005 11:10:00 PM

Even the conservative think tank, American Enterprise Institute, is opining about the housing bubble. AEI Economist John Makin both excuses and blames Greenspan for the bubble.

"Like so many difficult issues, the housing bubble has emerged from an unusual combination of events. The Fed’s response to each is defensible. However, taken collectively, those responses have encouraged what is arguably a worldwide housing bubble."Very interesting.

Recession Predictions: A Mug's Game?

by Calculated Risk on 3/28/2005 11:59:00 AM

"It's hard to make predictions - especially about the future."

Allan Lamport, former Toronto Mayor.

UPDATE: Two people have commented that the above quote was from Yogi Berra. It definitely sounds like Berra, and it is usually attributed to Berra, but I'm pretty sure it is from Mayor Lamport.

I’m going to take a look at the last consumer recession (July 1990 to March 1991) for clues about what to look for in the current situation. I believe the next recession will be consumer driven, led by a slow down in real estate, perhaps triggered by high energy prices and rising interest rates.

First, I would like to point out that forecasters have a terrible record at predicting downturns. Victor Zarnowitz wrote that major "...failures of forecasting are related to the incidence of slowdowns and contractions in general economic activity. Forecasts...go seriously wrong when such setbacks occur." The reason for this predictive failure is primarily due to the forecasters' incentives. Zarnowitz wrote: "predicting a general downturn is always unpopular and predicting it prematurely—ahead of others—may prove quite costly to the forecaster and his customers".

Incentives motivate economic forecasters to always be optimistic about the future (just like stock analysts). Luckily I have no customers (my thoughts are free and worth every penny), no financial incentives and no reputation! That said, I’m not predicting a recession (yet), only suggesting tools that might help identify the next recession.

The 1990/1991 Recession

As we look back at the ’90 recession, here are a few quotes from Fed Chairman Alan Greenspan (bear in mind that the recession started in July, 1990):

“In the very near term there’s little evidence that I can see to suggest the economy is tilting over [into recession].” Greenspan, July 1990

“...those who argue that we are already in a recession I think are reasonably certain to be wrong.” Greenspan, August 1990

“... the economy has not yet slipped into recession.” Greenspan, October 1990Source (pdf): "Booms, Busts, and the Role of the Federal Reserve" by David Altig (See macroblog)

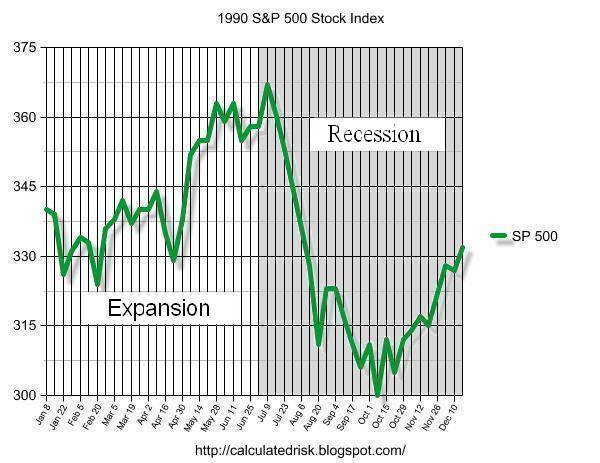

A common belief is that the stock market predicts economic activity. Looking back at 1990, here is a graph of the S&P 500. The graph shows that the market rallied right into the recession and only started selling off after the recession started.

Click on graph for larger image.

Another coincident indicator in 1990 was employment.

This graph shows monthly job creation in 1990. Although job creation was spotty for a couple of months before the recession, it didn’t turn negative until after the recession started.

A potentially predictive tool, often cited by investors, is an inverted yield curve. An inverted yield curve exists when the rates on shorter duration instruments are higher than rates on longer duration instruments. Here are the yields for the 13 week treasury note, and 5 year and 10 year treasury bills.

The curve inverted in mid-1989, a full year before the recession started. A popular joke on Wall Street at the time was that the yield curve has predicted eleven of the last 7 recessions! The yield between the 5 year and 10 year did stay narrow right up to the recession. I'm not sure why the bond market would have more information than the stock market, but this indicator is frequently cited.

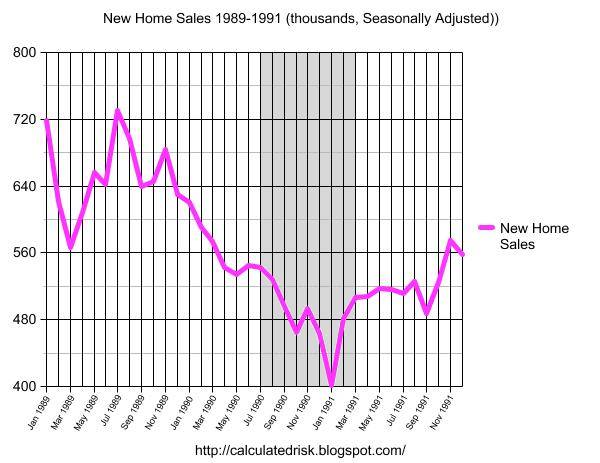

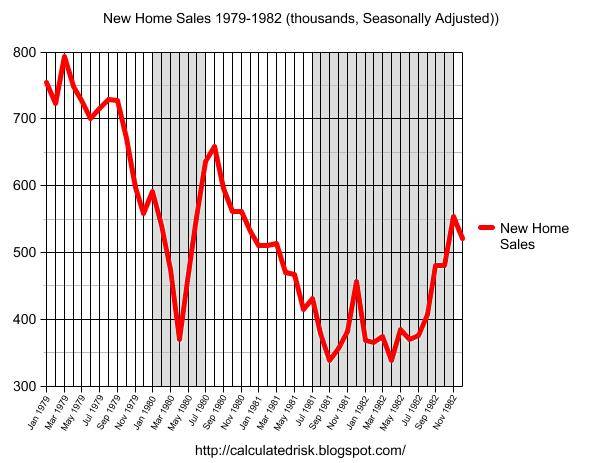

The last chart is my favorite leading indicator: New Home Sales. As the chart indicates, New Home Sales were declining for 12 months prior to the start of the recession. This has been observed (usually 8 to 12 months) for other consumer recessions (see New Home Sales as Leading Indicator and Update).

It makes sense that consumers, sensing economic weakness, would pull back on large purchases first (like homes). Then, since the Real Estate market is a large percentage of the U.S. economy, a slow down in Real Estate acts as a drag on the general economy - perhaps a self-fulfilling prophecy.

The Current Situation

So what does this mean for today?

First, here is the current chart for the 13 week treasury note, and 5 year and 10 year treasury bills. Clearly interest rates are rising, but the chart also shows that the yield curve is narrowing. The spread between the five and down year bills is close to 30 bps.

And finally, here is the current chart for New Home Sales. It is possible that New Home Sales peaked last October, however February's data was still very strong.

So, for now, I do not believe a recession is imminent. I'm just starting to watch for the early signs. Predicting recessions may be a mug's game, but I'm probably going to play.

Price-Rent Ratio: USA and San Diego

by Calculated Risk on 3/28/2005 03:19:00 AM

I posted a Price-Rent ratio for the US on Angry Bear:"Housing: Speculation and the Price-Rent Ratio". The following is the same calculation for San Diego (one of the hottest RE markets).

Click on graph for larger image.

The price component is from the OFHEO home price index for San Diego-Carlsbad-San Marcos and the rent series is from the BLS San Diego owner’s equivalent rent index.

Obviously San Diego has seen more recent appreciation. San Diego also experiences more volatility, but that is expected since the US is an average of many areas.

More on Housing Speculation

by Calculated Risk on 3/28/2005 01:13:00 AM

My most recent post is up on Angry Bear: Housing: Speculation and the Price-Rent Ratio

For a running list of News links on housing, see Patrick's Housing Crash site.

For an interesting graph and some great quotes, see Mish's "It's a Totally New Paradigm".

UPDATE: Another interesting article quoting Merrill Lynch chief economist David Rosenberg and Dean Baker, co-director of the Center for Economic & Policy Research: Bubble in housing will burst

Best to all.

Friday, March 25, 2005

Free Money!

by Calculated Risk on 3/25/2005 03:45:00 PM

Come and get it. Price doesn't matter. Interest rates don't matter. They're giving away free money, right here in Orange County, California. Just buy a home, wait a year, and put the cash in your pocket!

At least that was my reaction to this story in the OC Register: "Loan rates on the rise". The story quotes Gary Watts, a Mission Viejo "real-estate broker and economist" as expressing

... his enthusiasm this way: The recent $100 increase in monthly payments - or $1,200 a year - is nothing compared to what he predicts is Orange County home-price appreciation potential: as much as $70,000 a year.A simple calculation: The median home price in OC is $555,000. With 10% down, a buyer's monthly payment for P&I would be $2997.97 (plus property taxes of about $500 /month). This is based on a 30 year fixed rate loan at 6.01% (see FreddieMac)

"There's too much emphasis on interest rates in the marketplace," Watts said. "Who wouldn't trade $1,200 for $70,000?"

By my calculation, a speculator's first year risk is: $41.5K + their $55.5K down payment = $97K (minus the utility of the property), not $1200. Of course, with a 1 Year ARM (currently 4.24%) a speculator is only risking $35K + $55.5K = $90.5K (minus utility). And if the speculator can obtain a no money down loan, they are only risking the monthly payments minus the net rental income (or other utility if they occupy the house).

And what is the likelihood that houses in OC will appreciate $70K over the next year? Is there always a greater fool?

Thursday, March 24, 2005

New Home Sales Rebound in February

by Calculated Risk on 3/24/2005 10:38:00 AM

According to a Census Bureau report, New Home Sales rebounded in February to a seasonally adjust annual rate of 1.126 million.

Sales of new one-family houses in February 2005 were at a seasonally adjusted annual rate of 1,226,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 9.4 percent (±14.7%)* above the revised January rate of 1,121,000 and is 5.2 percent (±13.3%)* above the February 2004 estimate of 1,165,000.

The median sales price of new houses sold in February 2005 was $230,700; the average sales price was $288,400. The seasonally adjusted estimate of new houses for sale at the end of February was 444,000. This represents a supply of 4.4 months at the current sales rate.

Click on Graph for larger image.

The New Home Sales report shows no sign of a slowdown.

Wednesday, March 23, 2005

Refinance Applications Down 60% from Last Year

by Calculated Risk on 3/23/2005 07:06:00 PM

Mortgage applications were down 9.5% last week according to the Mortgage Bankers Association (MBA). According to their press release:

The Market Composite Index - a measure of mortgage loan application volume - was 658.8, an decrease of 9.5 percent on a seasonally adjusted basis from 727.6 one week earlier. On an unadjusted basis, the Index decreased 9.2 percent compared with last week but was down 39.3 percent compared with the same week one year earlier.My emphasis added. Is this the beginning of the end of mortgage equity extraction?

"The increase in mortgage rates has reduced application activity across the board, particularly for refinances. Refinance applications are down more than 60 percent relative to this time last year," said Michael Fratantoni, MBA's senior director of single family research and economics.

Tuesday, March 22, 2005

Forbes: Homeowners in Hock

by Calculated Risk on 3/22/2005 09:24:00 PM

This month's Forbes has an article about homeowners extracting equity from thier homes to "finance consumer expenditures". The article discusses several issues: the low savings rate, noting that "the personal savings rate has fallen from 6% of GDP 12 years ago to a mere 1% now", mortgage equity extraction (with a nice chart), and they hint at the link between equity extraction and the trade deficit.

If Forbes had taken the next step, they would have compared equity extraction to GDP growth (see: "Mortgage Debt and the Trade Deficit") and they would have asked what is the impact on trade and GDP if housing slows (see my musings "Housing and Trade: Virtuous Cycle about to Become Vicious?")

If housing slows that will end the equity extraction game. With rising interest rates and higher energy costs, a housing slow down is probably imminent and inevitable. Trying to determine the impact of an impending housing slow down on the general economy is the next puzzle.

Monday, March 21, 2005

Guest Bloggin' on Angry Bear

by Calculated Risk on 3/21/2005 01:24:00 AM

I've been invited to be a guest blogger on the Angry Bear. I will be posting on Mondays.

Here is my first (and hopefully not last) post: "Another Budget, Another Disaster".

A little introspection: What am I trying to accomplish with blogging? Initially I just wanted to understand what blogging was all about. Then I wanted to improve my writing skills (still working on that) and my understanding of economics (a hobby and a passion for me).

But most of all, I'm hopeful that the Internet and blogging will bring the America I love and believe in, back to the fore. Blogging is the 21st century pamphleteering and sometimes (offered in all humbleness) I sense the ghost of Thomas Paine.

Best Regards to all!

Saturday, March 19, 2005

Housing and Trade: Virtuous Cycle about to Become Vicious?

by Calculated Risk on 3/19/2005 09:33:00 PM

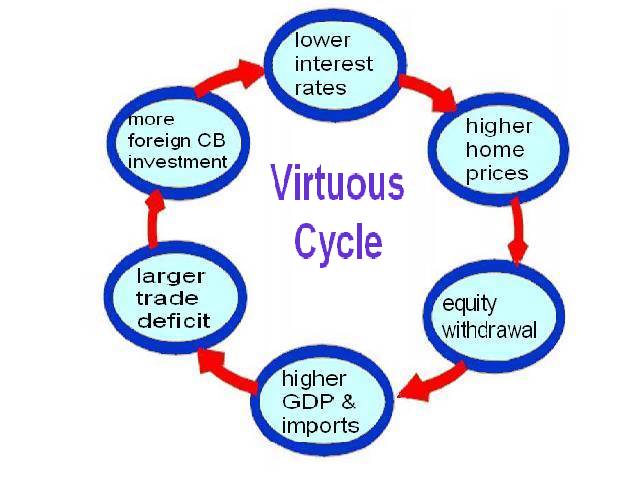

There appears to be a relationship between housing and the trade deficit as suggested by the 2nd graph in this earlier post. Perhaps we have seen a Virtuous Cycle as depicted in the following diagram: Click on diagram for larger image.

Click on diagram for larger image.

Starting from the top: There is no question that lower interest rates have led to an increase in housing prices. And those higher housing prices have led to an ever increasing equity withdrawal by homeowners.

A few numbers: Total mortgage debt increased $900 Billion in 2004 and $733 Billion in 2003; a significant increase from the $200 Billion in '97. In another measure called MEW "Mortgage Equity Withdrawal" (that is used in the UK), Goldman Sachs senior economist Jan Hatzius has calculated (reg. required) that homeowners have pulled $640 Billion from their homes in 2004, as compared to just $74 Billion ten years ago.

Since the savings rate has declined, it is reasonable to assume that a large percentage of this equity withdrawal has flowed to consumption, increasing both GDP and imports over the last few years. Since the annual increase in mortgage debt has exceeded GDP growth for four consecutive years (see graph 1), a large portion of this equity withdrawal has flowed to consumption of imports. Therefore it appears mortgage equity withdrawal has been a meaningful contributor to the ever widening trade and current account deficits.

To finance the current account deficit, foreign Central Banks (CBs) have been investing heavily in dollar denominated securities. Some analysts have suggested that these investments have lowered interest rates by between 40 bps and 200 bps (Roubini and Setser: "Will the Bretton Woods 2 Regime Unravel Soon? The Risk of a Hard Landing in 2005-2006")

If these analysts are correct, and foreign CB intervention is lowering treasury yields, then this has also lowerered mortgage interest rates ... and the cycle repeats. The result: a Virtuous Cycle with higher housing prices, more consumption and lower interest rates.

As a result of the rapidly increasing housing prices, we are now seeing significant speculation, excessive leverage and poor credit quality of new homebuyers; all the signs of an overheated market. As an example, in this article "Miami's Changing Skyline: Boom Or Bust?", a Raymond James and Associates representative is quoted as saying: "as much as 85 percent of all condominium sales in the downtown Miami market are accounted for by investors and speculators." What happens if the housing market cools down?

The Vicious Cycle

The following diagram depicts the possible unwinding of the current cycle.

If housing cools down (prices do not need to collapse), this will lead to lower equity withdrawal. In turn this will lead to a slow down in GDP growth and lower imports.

Lower imports might lead to a lower trade deficit, depending on the strength of exports. This could lead to less foreign CB investment in dollar denominated assets. And this could lead to higher interest rates followed by lower housing prices and the cycle repeats.

The result: a Vicious Cycle with lower housing prices, less consumption and higher interest rates.

Thursday, March 17, 2005

Senator Reid: An Online Interview

by Calculated Risk on 3/17/2005 10:29:00 PM

Democratic Senator and Minority Leader Harry Reid (D-Nev) gave an interview to a blogger this week. The interview is worth reading and I would like to highlight a couple of points:

Sen. Reid on the budget:

... –this budget–everything is being put to the back burner except these tax cuts being made permanent. This document should be filed under fiction in the Library of Congress because they don’t include the costs of the ongoing war in Iraq, they don’t list there the tax cuts, what that cost is going to be over the years; it doesn’t take into consideration so many different things, Social Security costs, and for the first time in the history of the country, they’re doing a budget on a five year budget rather than a ten year because if you look past five years its even more bleak than the first five years.And on the media and the Internet:

Raw Story: I think it’s significant that you’re giving an interview to us as an online site. I’m curious as to what your opinions are on the role of blogs and where you see them in the political ecosystem.

Sen. Reid:

I personally believe that much of what goes on in America today is governed by wealth and power. That if you look at what’s happened with the newspapers over the years, during the days of the founding fathers, they used to post newspapers in public squares and people who couldn’t read had the papers read to them. The Federalist Papers were a way of communicating; people read and learned. Well, when the radio came along, it changed it a little bit, but you still had the Fairness Doctrine so you didn’t have to worry. Really, the beginning came in the early 1950s; I think it was ‘52 or ‘53 when the networks decided to go to half-hour news programs. Then people stopped reading the newspapers even more. But on television you had the Fairness Doctrine.My emphasis added.

What has happened in recent years, the Fairness Doctrine has been taken away, that is, equal time for pros and cons on an issue. And they also allowed the concentration of media power, so one station, one owner can own 1,200 radio stations. What this means is that wealth and power control most everything in this country. But one thing they do not control–wealth and power does not control the Internet. Through the Internet, regular ordinary people have a voice. That’s why I go out of my way to communicate any way that I can on the Internet and I think the blogs are a tremendously important way for the American public to find out what’s really going on.

I agree with Sen. Reid's comments on the budget and the media. Read the entire interview here.

Tuesday, March 15, 2005

California Real Estate Prices: Boom and Bust

by Calculated Risk on 3/15/2005 11:39:00 PM

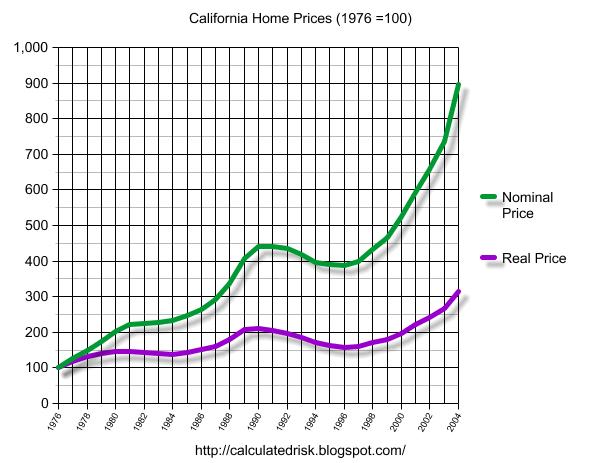

Today I heard someone comment that California Real Estate never goes down. In fact, California RE has declined in the past in both real and nominal terms.

Click on graph for larger image.

This graph shows the price of California RE based on the OFHEO California housing index. For the real price, the nominal price is adjusted by CPI, less Shelter, from the BLS.(1976 = 100)

The graph shows that in real terms we have seen two declines since 1980. The first decline, in the early '80s, lasted 3 years. The second decline, in the early to mid '90s, lasted 6 years.

The second graph shows the same information by annual rate of return, both real and nominal.

The decline in the '90s lasted 24 quarters from peak to trough. It took 9 years for prices to recover in nominal terms to their early '91 peak. Overall prices declined 12% in nominal terms and 26% in real terms.

Even more important for the economy are the coincident declines in sales volume. Real Estate prices are “sticky downward” since sellers are slow to adjust their prices down, and buyers are reluctant to buy a declining price asset. In this regards, real estate is an imperfect market in that prices adjust slowly to changes in supply and demand (unlike commodities like corn or wheat). Although prices do decline, it’s the decline in volume that leads to declining employment in real estate related occupations like construction, RE sales, mortgages, and more, and impacts the general economy.

UCLA Anderson Forecast: False Sense of Wealth

by Calculated Risk on 3/15/2005 09:46:00 AM

2nd UPDATE: Another good article with more quotes and facts from the Anderson Forecast:

From 2001 to 2004, the value of California's 7 million homes has increased by about $175,000 per home, resulting in a total rise of more than $1.2 trillion according to UCLA Anderson Forecast. Appreciation of apartments has added an additional $440 billion.And on the Central Valley:

"To put this in context, the personal income for the state was $4.7 trillion over the same period of time," the forecast states. "Hence, Californians have been essentially given a 30 percent-plus boost to their annual incomes due to the housing bubble we are currently experiencing."

The forecast is especially ominous for the central San Joaquin Valley, where the building boom has fueled some of the strongest job growth in the state. Of the 3,900 net new nonfarm jobs created in Fresno County last year, for instance, 2,100 were created in construction, an amount 3 1/2 times greater than that added in manufacturing, according to state jobs data.

UPDATE: A couple more quotes:

“This year we are expecting trouble with housing in the second half that will make GDP growth a little weaker than normal, but it (is) unlikely that a recession could get started that quickly without more telltale signs today,” [UCLA Anderson Forecast Director Edward] Leamer’s report said.ORIGINAL POST:

“The key here is that at best the state economy can be expected to maintain slow growth over the next few years as the weak housing sector saps off strength created in other parts of the state’s recovering external economy,” the report stated. “On the other hand, a sudden rise in interest rates or some other spark that could cause the housing sector bubble to implode at a faster rate could instead cause another recession, both in California and the U.S.”

This morning, at a UCLA conference, forecasters will caution on the impact of a Real Estate slowdown on California and the Nation. From an LA Times article:

Half of the private-sector jobs created in California in the last two years are connected in some way to real estate. Meanwhile, property values in the last four years have swelled $1.7 trillion, the equivalent of about 35% of the total personal income in the state since 2001.

This sharp increase in home equity has spurred consumer spending that, in turn, has fueled more economic growth.

"We have an economy that's rolling along on the basis of a false sense of wealth," said Christopher Thornberg, a senior economist with the Anderson Forecast team.

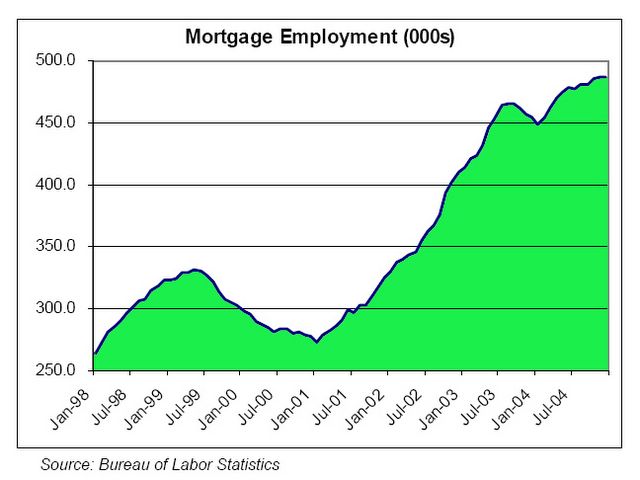

In a previous post, I discussed the impact of a housing slowdown on employment. The following graph shows the growth in employment in just one housing related area: mortgage employment.

We see that we have added 200K jobs in the mortgage industry alone in under 4 years. The mean salary (according to the BLS in 2001) was $45,380 for the mortgage industry.

Click on graph for larger image.

Graph thanks to ild and Elroy.

Another example: Just 2 years ago, there were 338,579 licensed RE Agents (brokers and salespeople) in California. Now, according to the Department of Real Estate, there are 423,315 licensees.

More from the article:

Thornberg said that in California, where home prices have increased faster than in the rest of the nation, the situation is precarious. Even a simple slowdown in the accumulation of equity in the state, he said, could harshly depress spending habits, job creation and economic expansion.

Real estate has become central to California's economy. Real estate-related jobs account for about 10% of private sector jobs in the state, according to the Anderson Forecast, and are growing rapidly.

Of the 243,000 private payroll jobs added in California since 2003, 122,000 are linked to the industry — jobs with construction companies, mortgage processing centers and the like.

And Thornberg's final comment: "The best-case scenario is mediocre."

Monday, March 14, 2005

Mortgage Debt and the Trade Deficit

by Calculated Risk on 3/14/2005 09:02:00 PM

Money flowing into the housing market works its way back into the economy by increasing consumption or savings (and investment). In recent years, aggregate savings have declined, therefore it appears money has flowed to consumption, both domestic (measured by the increase in GDP) and imports (measured by the increase in the trade deficit).

This is very simplistic but provides a general description of what I believe is happening. I will use the annual increase in mortgage debt as a measure of the money flowing into the economy from housing activities.

Previously I posted a graph of the annual Increase in Mortgage Debt vs. the Increase in GDP. The graph illustrated that during each of the preceding four years, U.S. households had assumed more mortgage debt than the increase in nominal GDP. I was asked if there were any other periods of similar increases in mortgage debt. The answer is NO, at least not in the last 40 years, as shown by the following graph:

The last four years have been atypical. There has been a surge in mortgage borrowing that far exceeded nominal GDP growth. It is unclear how much of GDP growth was driven by the increase in mortgage debt. However, since I believe most of the mortgage debt has flowed to consumption (not savings or investment); the portion that didn’t contribute to GDP growth must have flowed to imports.

Click on graph for larger image.

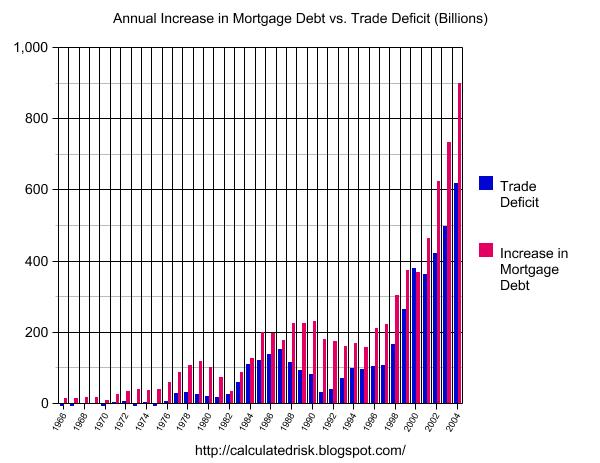

From the following chart it appears that the increase in mortgage debt is a factor in the increased trade deficit. The chart shows the annual trade deficit compared to the annual increase in mortgage debt. Data sources: trade deficit, GDP, New Home Sales, Mortgage Debt. There is a strong correlation between increases in mortgage debt and increases in the trade deficit. Although the correlation is high, it is very possible that there is no direct linkage, instead the same economic causes that led to higher trade deficits also led to more household borrowing. However, in recent years, with the dramatic increases in mortgage borrowing (far exceeding the increases in GDP) it is reasonable to expect that some of that money is flowing to imports.

There is a strong correlation between increases in mortgage debt and increases in the trade deficit. Although the correlation is high, it is very possible that there is no direct linkage, instead the same economic causes that led to higher trade deficits also led to more household borrowing. However, in recent years, with the dramatic increases in mortgage borrowing (far exceeding the increases in GDP) it is reasonable to expect that some of that money is flowing to imports.

The implications are important: if the housing market slows down, it will negatively impact both the domestic economy and the economies of our export driven trading partners: China, Japan, S. Korea and others.

The concern is obvious: If we slide into a global recession, we have limited tools available to stimulate the economy. Interest rates are already very low (although the Fed has recently put some arrows back into the quiver), and we are already running general fund budget deficits of close to 6% of GDP. And the concerns are not just economic. Historically, poor economic conditions are the precursors to civil unrest and wars.

One thing is certain, mortgages and housing play a much larger role in today's economy than in the past. In another recent post, I had suggested that the volume of New Home Sales seemed like a reasonable leading indicator of the consumer economy. The following graph shows New Home Sales since 1963.

The gray lines are approximate U.S. economic recessions as determined by NBER. With the exceptions of the 2001 (non-consumer recession) and '69-'70 recessions, New Home Sales were falling for 8 to 12 months prior to the onset of the recession. Since housing is a significantly larger portion of the economy today, a slowdown in housing would have a corresponding larger impact on the overall economy.

That is why I’m so focused on the housing market. I would like to see an orderly rebalancing of the World's economy, but I am not sanguine.

Friday, March 11, 2005

China Reduces Dollars in Its Reserves, Lehman Says

by Calculated Risk on 3/11/2005 01:39:00 AM

According to a Bloomberg article based on a Lehman report, China has "cut the share of its currency reserves held in dollars and raised its holdings of euros".

Lehman also predicts China will allow the yuan to fluctuate by the end of June.

First, in late February, Korea was rumored to be diversifying "the currencies in which it invests".

Then, two days ago, Japanese Prime Minister Junichiro Koizumi said his country ``in general'' needs to consider diversifying its foreign currency reserves.

Now China.

Thursday, March 10, 2005

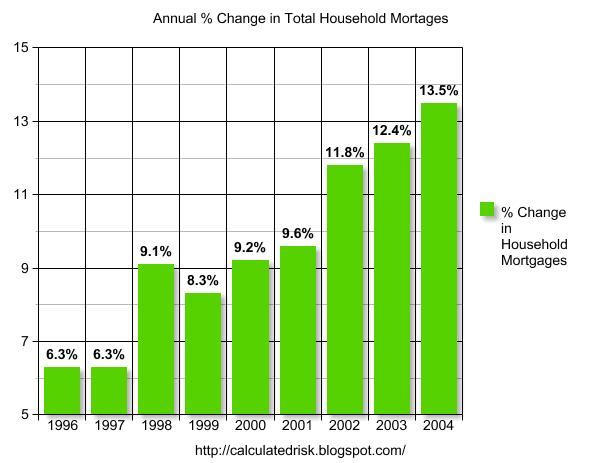

Mortgage Debt Increases 13% in 2004

by Calculated Risk on 3/10/2005 11:47:00 PM

Today the Federal Reserve released the "Flow of Funds Accounts" for 2004. The report shows that total household mortgage debt increased 13.5% in 2004. The following chart shows the annual rate of mortgage debt increase:

Click on graphs for larger image.

The rate of increase of mortgage debt has increased every year since 1999.

Household mortgage debt increased from $6.64 Trillion in 2003 to $7.54 Trillion in 2004.

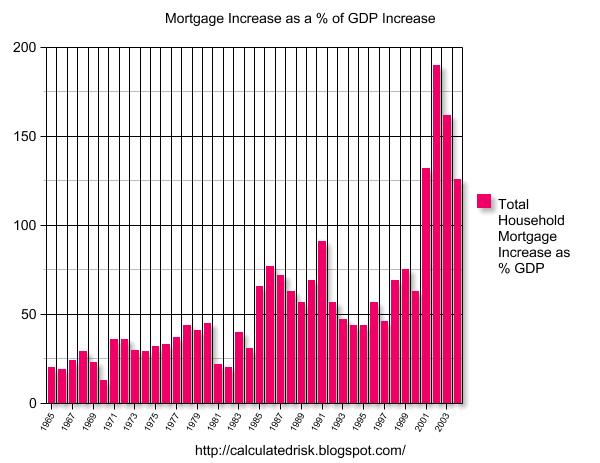

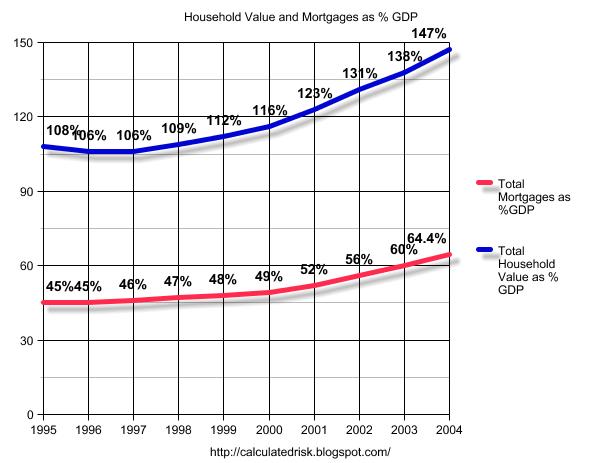

The next graph shows the Fed's estimate of the market value of all household real estate and household mortgage debt as a % of GDP.

Although mortgage debt has shown a substantial increase as a % of GDP (almost 20% over the last decade), the estimated value of household Real Estate has also increased substantially.

The appreciating value of household RE has kept the debt to value ratio under 50% based on the Fed's estimates.

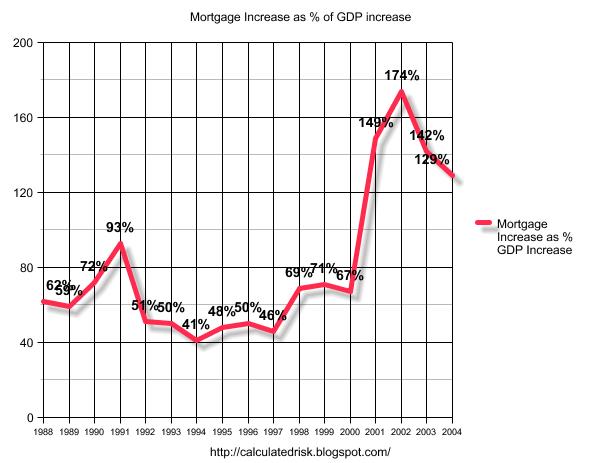

The final graph compares the annual increase in mortgage debt to the annual increase in GDP. This shows the impact of mortgage debt on GDP.

The economy was in recession for part of 2001, so it is not surprising that mortgage debt exceeded GDP growth for that year.

However, it is surprising that mortgage debt has substantially exceeded GDP growth for four consecutive years.

This lends credence to the idea that the American consumers are maintaining their lifestyles using their homes as ATMs. Please see these previous posts that expound on this supposition:

Mortgage Debt and the "Recovery"

A Recovery Built on a Marshland of Debt?

Volcker: Circumstances "dangerous and intractable"

The Other Trust Funds

by Calculated Risk on 3/10/2005 03:02:00 PM

With all of the attention on Social Security (OASI), perhaps we should also look at some of the other trust funds. As an example, the CSRS (Civil Service Retirement System) is similar to OASI program. CSRS is a defined benefit plan that uses contributions from today's employees to pay today's retirees. And like OASI, CSRS is running annual surpluses; $28 Billion in fiscal 2003. SOURCE: Monthly Treasury Statement.

But unlike OASI, CSRS is on-budget and is included in the President's budget report. In fact, with the exception of OASI and the Postal Service, all of the other trust funds (150+ in all) are included on-budget. This means that the surpluses from these programs are used to directly offset any deficit spending by the Federal Government. Of course, even Fed Chairman Greenspan talks about the "unified" budget that includes the OASI surplus as part of the budget - so the distinction between on-budget and off-budget is being lost.

This graph shows the growth of both OASI and the other trust funds. SOURCE: Treasury Dept.

Trust Fund reserves in Billions.

Click on Graph for larger image.

Many of these programs will suffer similar demographic issues as OASI. So when someone like victor at the Dead Parrot questions the existence of the OASI Trust Fund, he is also speaking to our military, Federal employees, Civil Service workers and many others who are paying into similar retirement insurance plans. Thanks to pgl at Angry Bear and William Polley for reminding me of this issue.

Tuesday, March 08, 2005

Fed's Poole: Social Security Needs Small Changes

by Calculated Risk on 3/08/2005 03:31:00 PM

In a Q&A session after a speech today in West Palm Beach, Federal Reserve Bank of St. Louis President William Poole said, according to a Reuters article, that it would not take a large change in some combination of either tax increases, benefit cuts or an increase in the retirement age to put the Social Security retirement plan in "pretty good balance."

In the speech, "A Perspective on the Graying Population and Current Account Balances" Poole argued that demographic factors are being overlooked with regards to the Current Account Balance.

Housing: Excessive Leverage?

by Calculated Risk on 3/08/2005 01:46:00 AM

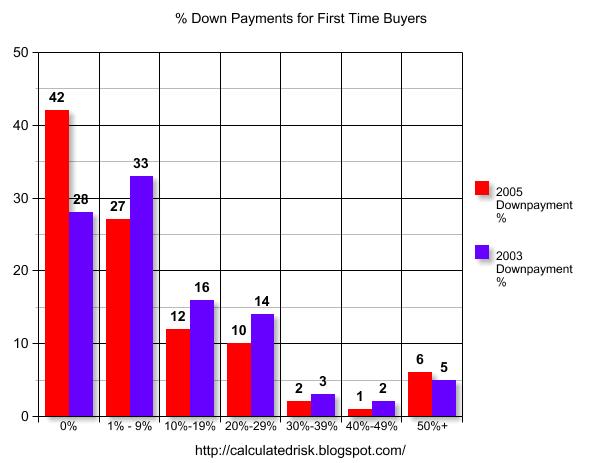

The article "Risky real estate moves" on CNN Money discusses the growing prevalence of no money down home purchases by first time buyers. The article presents a table showing the percentage down payment for first time homebuyers. The following table combines CNN's table (data from the National Association of Realtors in early 2005) with earlier data from NAR in early 2003.

Click on graph for larger image.

Source: NAR

Fully 42% of first time buyers put no money down and 69% put less than 10% down. Two years ago 28% put no money down and 61% put less than 10% down. Clearly first time buyers are opting for more leveraged transactions.

The CNN article also discusses three leveraged borrowing programs. The first, "piggyback" loans, allows the homebuyer to take out a line of credit to cover the down payment resulting in 100% financing.

The second, interest only loans, allows the buyer to purchase more home by limiting their payment to the interest due. And the third program has several payment options, including a "minimum payment" that allows the buyer to pay less than the interest owed, resulting in an increasing loan balance.

All of these programs are increasing in popularity and increasing the amount of leverage for the buyer. The third program, combined with no money down, creates significant systemic risk. Who bears the risk? Not the first time buyer. Since the loan is collateralized with the house, the buyer can just walk away and only suffer the minor indignity of a foreclosure on their credit record. The real risk is borne by the lender.

Monday, March 07, 2005

Housing: Two Worrisome Signs

by Calculated Risk on 3/07/2005 03:25:00 AM

Two articles on Real Estate caught my attention tonight ...

The first is a "How to Flip" article on ABC News! (thanks to Patrick)

Sensible Shopper: Real Estate 'Flipping'Oh my! Of course I've been telling people that it is rational to speculate in Real Estate as long as very little of their own money is at risk. I've even explained "moral hazard" to a few people.

What You Need to Know to Get in on the Trend in the Hot Real-Estate Market

The second is a monthly newsletter concerning Bay Area Real Estate (Northern California). Here is the executive summary:

"The SCC real estate market has lost much of its steam in terms of volume. Decreasing volume is 'normal' behavior for the Santa Clara County real estate market for the end of the year. It is the degree of the decrease that remains a concern. Volume went from 154% of the 10-year average to 132% in June. Then went from 132% to 114% from mid-November to mid-December; and finally from 114% to 98% starting January 12, 2005. SCC only experienced 44% of the offers seen during the peak summer. This is a lower percentage than any of the 10-years that we have data for."Blame it on the rain?

Sunday, March 06, 2005

China and the Price of Gas

by Calculated Risk on 3/06/2005 08:51:00 PM

Last Friday, the USA Today reported that "Gas prices might increase 24 cents". Then at the annual meeting of the National People's Congress, Chinese Foreign Minister Li Zhaoxing told reporters that China 'should not be held responsible for the world's rising oil prices'.

Is China responsible for the increase in oil prices, and consequently, gas prices?

Li was quoted as saying: "Although China's energy import has increased a little bit over the past two years, its import only accounts for approximately six per cent of the world's total traded oil."

From the article:

It's true that China's energy demand has increased to certain extent as the country's economy has been growing rapidly in recent years, but the demand is mainly to be met domestically, he said.

Besides, he said, there is a big potential of saving energy and improving the use of energy efficiency in China's domestic energy supply.

Therefore, the Western media criticism saying that China is a major impact on the world's oil price is "groundless", he said

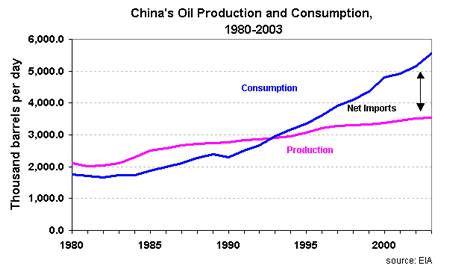

First, here is a chart of China's oil production and consumption since 1980 (Source: Dept of Energy)

Click on graph for larger image.

Source: Dept of Energy

Starting in 1994 China became a net importer of oil. The graph ends in 2003 with China importing 2.1 million barrels per day (bbl/d). In 2004 China's oil imports increased another 35% to approximately 3 million bbl/d. Still, as Minister Li pointed out, that is a small percentage of the World's traded oil. Also, the United States increased oil imports in 2004 by about 0.7 million bbl/d to 12.25 m bbl/d. Although China's oil imports are growing faster than the US, both in percentage and bbl/d terms, China's oil import quantities are still only about 25% of the United States.

So why has the price of oil increased so dramatically? Here is at least part of the reason: Both the supply and demand curves for oil are very steep. We all know this intuitively. If there is little unused capacity, it takes time for more oil production to become available since this involves huge capital intensive projects. And, in the short term, demand is fairly inelastic over a wide range of prices; for the most part people stay with their routines and keep their same vehicle. With two steep curves (supply and demand) we get the following:

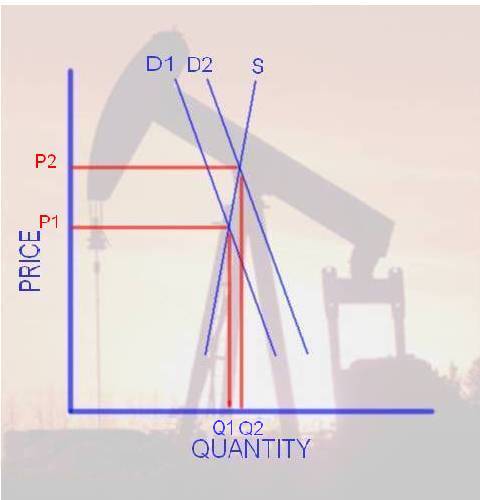

OIL Supply and Demand

UPDATE: fixed typo on drawing. With a small increase in Demand (from D1 to D2), we see a small increase in Quantity (Q1 to Q2), but a large change in Price (from P1 to P2). Also a large price increase would occur if we had a small decrease in supply such as disruption to production, transport or refining (like hurricane Ivan in the GOM last year).

Of course the opposite is also true. A relatively small decrease in demand (or increase in supply) would cause a significant drop in price. So China's relatively small increase in demand (and the US too!) could have caused a large increase in oil prices.

Is China to blame for higher gas prices? Of course not. They have the same right to oil as any other consumer. But the increased demand in the US and China has most likely caused (without blame) the increase in prices.

The above assumes perfectly competitive markets. And oil differs from most commodities: "it is an exhaustible resource, production is controlled by national governments, and for the major oil exporters oil is the overwhelmingly dominant source of national income." (See: Krugman "The Energy Crisis Revisited") However if the world's spare capacity is exhausted, then the simple approach is probably reasonable.

There could be other factors effecting the price of oil - a terrorism premium and hedge funds speculation are often mentioned as culprits - however, I think the simple explanation is probably the most accurate: fast growth in China coupled with strong growth in the U.S. has utilized most of the world's spare capacity. Since supply is almost inelastic (in the short term), price fluctuates significantly with small changes in demand.

But what happens in the intermediate term? In the longer term the situation becomes more complicated. Since oil is an exhaustible resource, we may be getting close to "peak production" - where the maximum annual oil production is reached and then we will start a long decline in production. There is no way of knowing how close the world is to peak production since many of the key reserves are held by national governments (like Saudi Arabia) and they are not forthcoming with hard data. This lack of transparency has caused concern and might be leading to some of the rumored hedge fund speculation. After oil production starts to decline, the world will need to find a substitute for the loss of oil supply. In that regards, I believe high prices will be the wellspring of innovation.

More certain is that if the prices hold, we will see both more production (assuming we are not at Peak Oil), substitution and a moderation in demand. The following chart shows US oil consumption for the last 50 years.

Source: Dept of Energy

The two oil shocks (1973 and 1979) were followed by periods of slackening demand. The industrial sector has never returned to the 1979 consumption levels (due to a combination of efficiencies and substitutes) and "other uses", like electricity generation using oil, has also declined significantly. This leaves motor fuel and "other transportation" as the growth sectors for oil consumption. For demand to decrease, people will probably have to park their Hummers and buy a Prius!

Final comments: There are other reasons than just price to decrease our dependence on oil.

First, burning oil products is a major contributor to global warming. This is a serious problem and, as Professor Tim Barnett of the Scripps Institution of Oceanography said in February: "The debate over whether there is a global warming signal is over now at least for rational people."

And the second is an ethical question: Since oil is an exhaustible resource, do we, the 21st Century cohorts, have a right to burn all of it? Or do we have a responsibility to future generations to use it more discerningly?

Saturday, March 05, 2005

Greenspan's March to Infamy

by Calculated Risk on 3/05/2005 02:22:00 AM

On two March 2nds, exactly four years apart, Fed Chairman Alan Greenspan testified before the House Committee on the Budget, not in his role as Chairman of the Federal Reserve, but speaking for "himself".

In his 2001 testimony, Mr Greenspan, with his usual caution and caveats, talked of surpluses for the foreseeable future. Greenspan was effusive (well, effusive for Greenspan) offering projections of "an on-budget surplus of almost $500 billion ... in fiscal year 2010". The National Debt would soon be retired and the Boomer's retirements secure. Greenspan offered a projection of "an implicit on-budget surplus under baseline assumptions well past 2030 despite the budgetary pressures from the aging of the baby-boom generation, especially on the major health programs."

Just four years later, again on March 2nd, Greenspan offered a starkly different view to the same committee. This year Greenspan talked of large "unified" deficits and commented that "our budget position is unlikely to improve substantially in the coming years unless major deficit-reducing actions are taken." He targeted Social Security and Medicare for cuts, saying "we may have already committed more physical resources to the baby-boom generation in its retirement years than our economy has the capacity to deliver."

I will leave the interpretation of Greenspan's motivations to others (like Paul Krugman's Op-Ed piece "Deficits and Deceit" in the NYTimes). But for this review, I would like to point out three significant misleading comments in Greenspan's speeches.

First, in both speeches Greenspan praised the fiscal discipline of Congress in the '90s and suggested that Congress' discipline, along with strong productivity gains, brought the deficits of the '80s under control. Greenspan is only half right. Look at this graph (with the 1990s enlarged) from this previous post.

NOTE: Click on graphs for larger image.

Source: U.S Treasury

Not only did Government Outlay as a % of GDP decline in the '90s, but Greenspan seems to have forgotten that Government Income increased as a % of GDP; the tax side of the equation! In fact there were 5 major General Fund tax increases between 1982 and 1993 that contributed to bringing the budget into balance. They were:

Tax Equity and Fiscal Responsibility Act of 1982 - ReaganFor an analysis of Major Tax Bills since 1940 see OTA Working Paper 81, U.S. Treasury Office of Tax Analysis by Jerry Tempalski.

Deficit Reduction Act of 1984 - Reagan

Omnibus Budget Reconciliation Act of 1987 - Reagan

Omnibus Budget Reconciliation Act of 1990 - G HW Bush

Omnibus Budget Reconciliation Act of 1993 - Clinton

Second, Mr. Greenspan erroneously suggests that only budget cuts, not tax increases, will bring the budget back into balance. He said "... tax increases ... arguably pose significant risks to economic growth and the revenue base." Further, Greenspan said "... if at all possible ... close the fiscal gap primarily, if not wholly, from the outlay side." That argument ignores the cause of the budget deficit that the following graph illustrates (same as above without '90s enlarged):

The annual deficit is the difference between the red and blue lines. Although spending increased after 2000, most of the deficit came from the substantial tax cuts of the last four years. These are historically low tax rates (as a % of GDP) and to suggest that raising the rates would jeopardize the recovery has no foundation in economic theory. It also contradicts recent history (that Mr. Greenspan seems to have forgotten).

Source: U.S. Treasury

And third, in his 2005 speech, Mr. Greenspan referred to the "unified budget" saying that "the unified budget is running deficits equal to about 3-1/2 percent of gross domestic product". In his 2001 speech, Mr. Greenspan more correctly spoke of on-budget and off-budget surpluses. Now that we are running large deficits, he only talks about the "unified budget". This is very misleading.

The problem with the "unified budget" is that it adds the Social Security surplus (and other off-budget surpluses) to the General Fund and masks the actually budget problem. One would think that the annual budget deficit would equal the annual increase in the National Debt. This is true if you use the General Fund deficit, but not the "unified deficit". The real fiscal issue is the General Fund deficit; the General Fund is running annual deficits of almost 6% of GDP!

Of course, if the Social Insurance payroll tax is just another General Fund tax then Mr. Greenspan is correct. But let me remind Mr. Greenspan (who chaired the 1983 Social Security "Greenspan Commission"):

1) IF the entire Social Insurance payroll tax is used for social insurance (retirement insurance, survivors insurance, health insurance) then the tax is NOT regressive.

2) IF the Social Insurance surplus is used as a General Fund tax (as using the "unified budget" suggests), then that portion of the payroll tax is highly regressive.

A regressive tax is redistributive of wealth from lower income workers to the wealthy. Not a desired consequence of tax policy.

These are three major misleading comments. Mr. Greenspan may have been speaking for himself, but his words carry the power and authority of the World's leading banker. I believe he should be more careful and far more accurate.

Wednesday, March 02, 2005

Will an Adjustment in the Current Account Deficit Lead to a Recession?

by Calculated Risk on 3/02/2005 07:05:00 PM

Here is a new paper that does an historical review of previous CAD adjustments , "Financial Market Developments and Economic Activity during Current Account Adjustments in Industrial Economies" by Croke, Kamin and Leduc.

The consequences of an adjustment in the current account deficit is being widely discussed. Some observers believe that an orderly adjustment is probable. Others, like Roubini and Setser, argue that a disorderly adjustment is very possible and "could result in a sharp economic slowdown in the US." This new paper looks at historical occurrences of Current Account Adjustments and Croke, Kamin and Leduc conclude:

"a significant subset of the adjustment episodes we studied were associated with substantial declines in GDP growth ... Thus, the fear that current account adjustment might be associated with recession is not entirely without basis."

BUT ...

"[O]ur second main finding is that the shortfall in growth experienced in the contraction episodes appears to reflect the playing out of standard cyclical developments rather than a response to current account adjustment."My interpretation of their conclusion is that a CAD adjustment doesn't necessarily cause a recession, but a recession cures a CAD problem. Is that good news or bad?

NOTE: DeLong reviews another recent paper "The U.S. Current Account and the Dollar" by Oliver Blanchard, Francesco Giavazzi, Filipa Sa". I also recommend Macroblog and New Economist.

UPDATE: Both Macroblog and New Economist have posts reviewing this new paper.

The Worsening General Fund Deficit

by Calculated Risk on 3/02/2005 03:06:00 PM

Here is the current Year over Year deficit number (March 1, 2004 to March 1, 2005). As of March 1, 2005 our National Debt is:

$7,701,629,503,518.55 (that is over $7.7 Trillion)

As of March 1, 2004, our National Debt was:

$7,065,724,603,168.71

So the General Fund has run a deficit of $635.9 Billion and change over the last 12 months. SOURCE: US Treasury

Source: U.S. Treasury

For comparison:

For Fiscal 2004 (End Sept 30, 2004): $596 Billion

For Jan 1, 2004 to Jan 1, 2005: $609.8 Billion

For Feb 1, 2004 to Feb 1, 2005: $618.6 Billion

It just keeps getting worse.

NOTE: I use the increase in National Debt as a substitute for the General Fund deficit. For technical reasons this is not exact, but it is close. Besides I think this is a solid measure of our indebtedness; it is how much we owe!

Update: New Home Sales as Leading Indicator

by Calculated Risk on 3/02/2005 02:53:00 AM

In my earlier post, I suggested that the volume of New Home Sales might be a leading indicator for a consumer led economic slowdown. One of the questions I was asked was how many times did housing decline and the economy not slide into recession (a false positive)? Another reasonable question would be how many recessions does the signal miss (a false negative)?

We only have 42 years of data from the Census Bureau that includes 6 recessions. This is a very small sample. A housing slowdown did not immediately precede either the 1969 or 2001 recessions (the 2001 recession was mostly business related). The following graph shows the annual volume of New Home Sales since 1963 (the earliest data from the Census Bureau).

NOTE: The annual data loses resolution and does not show all of the information contained in the previous post's graphs.

The shaded lines on the graph are approximate and represent U.S. economic recessions.

Click on the graph for a larger image.

Source: Census Bureau

Here is a graph from the earlier post showing housing and the early '80s recession. Compare that to the double dip recession in the previous graph. In this graph we can see the monthly detail and that the declining volume of New Home Sales were a reasonable leading indicator for both economic recessions.

Source: Census Bureau

K Harris pointed out some potential anomalies in the Census Bureau data. It is very possible that the January numbers were impacted by weather or other factors. I was NOT suggesting that the January drop in housing was indicative of a slowdown, only that if housing volumes continue to decrease that that might be a strong leading indicator. For this indicator to suggest an economic slowdown, the volume of New Home Sales would have to continue to decline over the next few months.

Predicting recessions is very difficult. The only reliable indicator is a flattening (or inverted) yield curve - and the running joke is that the yield curve has predicted 11 of the last 7 recessions! Also there is a strong incentive for most economists to always be bullish on the economy. Nobody will blame you if you miss a turning point, but to cry wolf is a disaster for your reputation. Here are a couple of examples from the Fed Chairman Alan Greenspan:

"It is very rare that you can be unqualifiedly bullish as you can be now."

Alan Greenspan, Jan 1973 (about 6 months before the economy went into recession).

"But such imbalances and dislocations as we see in the economy today probably do not suggest anything more than a temporary hesitation in the continuing expansion of the economy."

Alan Greenspan, Jan 1990 (about 6 months before the recession)

I'm not picking on Mr. Greenspan, just using him as an example. Here is another example: The WSJ conducted a survey of 40 economists in July 1990, and only one predicted a recession. The Journal went so far as to ridicule the one economist predicting a recession, suggesting that he "now has predicted four of the past zero recessions." With hindsight we now know that in July 1990 the economy was ALREADY in recession!

For an excellent analysis of recession prediction, I suggest the following paper by the IMF's Prakash Loungani "The Arcane Art of Predicting Recessions".

Tuesday, March 01, 2005

More Evidence of Housing Speculation

by Calculated Risk on 3/01/2005 01:26:00 PM

The National Association of Realtors released a new report today. Here are a few key findings:

"... 23 percent of all homes purchased in 2004 were for investment, while another 13 percent were vacation homes. In addition, there was a record of 2.82 million second home sales in 2004, up 16.3 percent from 2.42 million 2003. The investment-home component rose 14.4 percent to 1.80 million sales in 2004 from 1.57 million in 2003, while vacation-home sales rose 19.8 percent to 1.02 million in 2004 from 850,000 in 2003."

And in the NYTimes today, "Speculators Seeing Gold in a Boom in the Prices for Homes", the story starts with this anecdote:

'Within six months last year, Carlos and Betti Lidsky bought and sold two condominiums. Then they bought and sold two houses. They say they will clear a half-million dollars in profit, and none of the homes have even been built.

Now Mr. Lidsky, a lawyer, and his wife, a charity fund-raiser, have put down a deposit on a fifth property, a $1.3 million condo in a high-rise under construction, and are planning to sell before the deal closes, without even taking out a mortgage.

"It is much better than the stock market," Mr. Lidsky said. "This is an extraordinary, phenomenally good result." '

And this on speculation:

'According to LoanPerformance Inc., a San Francisco mortgage data firm, about 8.5 percent of mortgages nationwide in the first 11 months of last year were taken out by people who did not plan to live in the houses themselves, up from 5.8 percent in 2000. In some markets, that proportion is much higher: in Phoenix, more than 12 percent of mortgages were taken out by investors; in Miami, the figure is 11 percent.

The National Association of Realtors, a trade organization that represents real estate brokers, said in a study being released on Tuesday that the percentage of homes bought for investment might be as high as one-quarter of the 7.7 million sold last year.

"Americans are treating real estate as a viable alternative to stocks and bonds," said David Lereah, chief economist at the Realtors association. And some are buying at least two properties at a time.'

Excessive speculation, poor credit quality, excessive leverage, oversupply of housing units ... all indicators of a bubble.

"Homeownership has become a vehicle for borrowing and leveraging as much as a source of financial security."

Former Fed Chairman Paul Volcker, Feb 11, 2005 (See Volcker's speech)