RSS Feed

RSS Feed by Calculated Risk on 6/30/2005 11:37:00 PM

Thursday, June 30, 2005

CNN Newsnight: Aaron Brown Discusses the Housing Bubble

On Tuesday night, CNN's Newsnight with Aaron Brown had a segment on the housing bubble. Here are excerpts from the transcript:

BROWN: Back in the mid '90s, when we were all thinking of early retirement after our Internet stocks tacked on another 10 or 15 points, there were naysayers who said it wouldn't last, who said rationality always returns eventually, who said it was a bubble and a dangerous one at that. Oh, those naysayers.There is more, but that was the most in-depth part of the discussion. Dean Baker didn't get much face time!

By the way, are you counting on home equity to fund your retirement? Like the fact that your home doubled in the last decade or so? Feeling rich again? So is this deja vu with a mortgage? Here's CNN's Andy Serwer.

(BEGIN VIDEOTAPE)

ANDY SERWER, CNN CORRESPONDENT (voice-over): Is there a housing bubble? It depends who you ask and where you ask.

DEAN BAKER, CTR FOR ECONOMIC POLICY RESEARCH: Well, there's absolutely a housing bubble. In the last seven or eight years, we've seen an unprecedented run-up in home prices nationwide.

SERWER: No question, certain markets are red hot. Since 2000, the price of a single family home has jumped 77 percent in New York City, 92 percent in Miami, and 105 percent in San Diego. And there are other signs besides just home prices, 86 books on real estate investing were published last year, nearly three times as many as 1998.

Speculators have added fuel to overheated markets. In Los Angeles, for example, the number of homes sold that have been owned for less than six months jumped 47 percent in a year.

Prices are so high in some areas that renting a home has become dirt cheap by comparison. In San Francisco, for example, rent on a median price house runs $1,532 a month. Owning the same house with a typical mortgage would cost $3,424 a month.

But not every market is on fire. Some experts say that bubbles are mostly in cities on the east and west coasts. If those bubbles were to burst, it would shock the entire economy. But some say prices won't collapse, they'll just ease up.

FRANK NOTHAFT, CHIEF ECONOMIST, FREDDIE MAC: As long as the local economy remains strong and there is good job creation, then we're not going to see a drop in home values.

SERWER: In cities such as Dallas or Salt Lake or Pittsburgh, prices haven't risen nearly so much. Radical differences in prices can make moving from a hot zone like LA to a colder one like Syracuse either a windfall or a slap in the face, depending on which way you're going.

So what does all this mean for the prospective buyer?

FRANK NOTHAFT: It's a very personal decision whether or not they should sell now and choose to rent. If you're happy with your home and you enjoy the home that you're in and the neighborhood you're in, there's no point to sell it right now and switch to renting.

SERWER: In other words, don't just buy a home because you think you'll make a ton of money on it in two years. And don't sell your home just because it's appreciated wildly either. Because in real estate, as in everything else in life, you can't count on getting a better deal down the road.

Andy Serwer, CNN, New York.

(END VIDEOTAPE)

BROWN: Taking the global view for a moment, globalization being the rage these days, in 2004, housing prices in Spain and France went up even faster than they did here in the United States, 15 percent up for the year. Compared to 9 percent nationwide in the U.S.

But before you bet the farm, or the house, consider this. In Japan, house prices have dropped for the last 14 years. And they are now down 40 percent from their peak back in 1991. Here at home again, the median price of a house is $207,000. That means half the houses cost more, half the houses cost less.

Any economic topic is difficult for TV News. No pictures. I can imagine the viewers reaching for the remote ... hmmm, any shark attacks today?

Real Estate "Summit" Comments

by Calculated Risk on 6/30/2005 09:21:00 PM

Following are some comments and stories from the Reuters Real Estate Summit in New York.

Property guru says U.S. market nearing peak Peter Korpacz, the head of real estate business advisory services for PriceWaterhouseCoopers told reporters:

"The thing the industry is focusing on now is jobs growth. For the most part its running at about 175,000 a month. It's a healthy economy, but it's not robust. During this point in the last recovery (in the early 1990s) jobs were growing at about 217,000 a month."Toll Bros sees possible correction in hot markets

Korpacz said real estate lenders and developers are far more disciplined now than in the past and so there was little threat to the market from speculative development, although the red-hot residential sector was giving rise to concerns among investors.

He added that if there is a major drop in prices for condos or single-family housing, it could hurt "real estate as a whole and just wash (away) the whole industry."

"In the hot markets, I wouldn't be surprised to see a 20 percent decline," [Robert Toll Brothers Inc.'s chief executive] said at the Reuters Real Estate Summit in New York. "You've got a price going from $1 million to $800,000, I don't have a problem with that.For more stories see the Reuters Summit site.

"I don't think you're going to have a pop, which means I don't think you've got a bubble," added the head of the luxury home builder at the summit held at Reuters U.S. headquarters in New York. "But I do think you're going to have a correction as the markets unnaturally overheat because of speculation."

Environmental Economics

by Calculated Risk on 6/30/2005 01:31:00 PM

An an undergrad, I was incredibly fortunate to take Chemistry from Drs.Sherwood Rowland and Mario Molina. At that time, the future Nobel Laureates (1995 Nobel Prize in Chemistry) Rowland and Molina were working on their ground breaking discoveries into how chlorofluorocarbons (CFCs) were impacting the ozone.

But Rowland and Molina's work was just the start. To correct the CFC caused ozone depletion problem it took a combination of great science, an open discussion of the environmental impact of various policy options, government action and international cooperation. Not only was the chemistry fascinating, but that was my introduction into market failures and externalities. When I spoke with Dr. Rowland a few months ago, he modestly told me the science might have been the easy part!

With that prelude, here is a new Environmental Economics blog with 17 contributing economists addressing many of the economic and political issues that are required to transform good science into good policy. Enjoy!

Britain: Headed for a Hard Landing?

by Calculated Risk on 6/30/2005 11:16:00 AM

According to MSNBC:

The Bank of England's attempt to bring Britain's highflying economy in for a soft landing is starting to reach the nail-biting stage.Of course less consumer spending is also related to the deflating housing bubble:

Fears are growing, even within the BOE, that consumer spending is faltering in response to past hikes in interest rates and soaring energy bills.

At the center of the drama is Britain's housing bubble, which began to lose air in the second half of last year. Although the growth rate of house prices has slowed sharply, a generally healthy economy has helped to allay worries over a collapse. Now the economic outlook is dimming.Housing slows, consumers retrench, and then the job market starts to soften:

In particular, consumers are pulling back more than anticipated.

The newest concern is the labor markets. In May the number of workers claiming jobless benefits rose for the fourth month in a row. That hasn't happened since 1993, and it could be a harbinger of softer job markets. Wage growth, excluding bonuses, is already slowing.And the next step in the downward vicious cycle? Falling housing prices, followed by even less consumer spending and more job losses and then a further reduction in house prices ...

Bloomberg columnist Matthew Lynn offers a similar view: U.K. Consumers Risk Recession With New Restraint.

The U.K. consumer shows every sign of having run out of steam and the economy is teetering as a result.The US has also had a "huge increase in household debt". Perhaps Britain's problems offer a glimpse of the future for the US housing market and economy.

British shoppers have become hypersensitive since the Bank of England increased interest rates five times from November 2003 through August 2004, and since their household debt skyrocketed to more than 1 trillion pounds ($1.82 trillion).

There may well be a lesson in that for policy makers in many other countries. Consumers who have piled up debt are far more responsive to rate changes than previously.

What used to be just a nudge on the interest-rate rudder is now sending the economy downhill. The U.K.'s growth rate has fallen in each of the past four quarters.

``The main factor has been the huge increase in household debt,'' said Stuart Thomson, a fixed-income strategist at Charles Stanley Sutherlands in Edinburgh, in a telephone interview. ``It is the highest in the developed world. So people are really getting squeezed as rates rise.''

UPDATE: Another take on UK: Economic growth weakest in 2 years

And the GDP data suggest an even greater link between the housing market and consumer spending than the BoE at first assumed, suggesting worse could be yet to come.

The saving ratio in 2004 fell to its lowest since 1963 as household spending was credited with making an even greater contribution to the economy over the last few years, before slowing in line with the housing market.

The Nationwide building society said house prices fell 0.2 percent in June, bringing the annual rate of increase to a nine-year low of 4.1 percent, compared with nearly 20 percent a year earlier.

"This obviously increases the danger that the saving ratio will rise over the coming quarters as the housing market weakens, slowing the growth of household spending even further," said Jonathan Loynes, chief economist at Capital Economics.

Tuesday, June 28, 2005

Housing: FDIC and California

by Calculated Risk on 6/28/2005 07:57:00 PM

According to the article in the previous post:

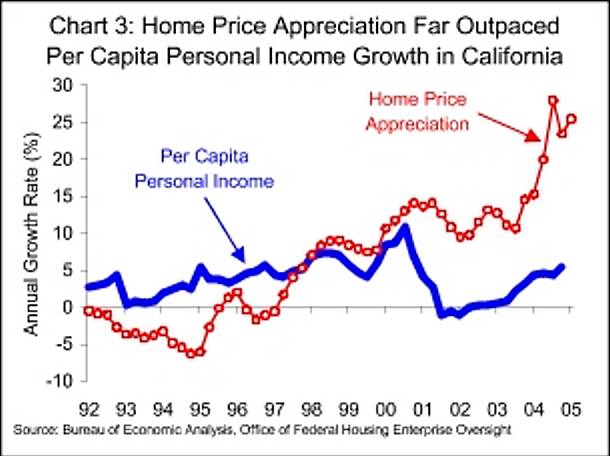

Today, the agency will release new state-by-state economic profiles. Taken together, the profiles conclude that most booming U.S. housing markets are sustained by strong growth in new jobs.Here is the California profile and two graphs.

"In general, that is where home prices are rising most rapidly," said Barbara Ryan, associate director of the FDIC's research division.

Click on graph for larger image.

Job growth in the bay area and southern California trailed the rest of the Nation.

Price appreciation outpaced income growth.

The data for California does not seem to support the FDIC's conclusion.

Sec. Snow and FDIC: No Housing Bubble

by Calculated Risk on 6/28/2005 07:04:00 PM

Treasury Secretary Snow appeared on CNBC today. According to FOX:

"I think in some markets housing prices have risen out of alignment with underlying earnings," Snow said. But also answering the question whether there was a housing bubble in the United States his answer was a flat-out "no."And officials at the FDIC apparently believe that housing prices are the result of strong job growth. From this article:

Top officials at the Federal Deposit Insurance Corp. (FDIC), which regulates national banks, yesterday dismissed fears that rising home prices nationwide reflect a speculative bubble ready to burst.Here are the FDIC State Profiles.

...

Today, the agency will release new state-by-state economic profiles. Taken together, the profiles conclude that most booming U.S. housing markets are sustained by strong growth in new jobs.

"In general, that is where home prices are rising most rapidly," said Barbara Ryan, associate director of the FDIC's research division.

Snow also commented on Oil prices:

"Energy prices are way too high," Snow said on CNBC television. "Clearly, it's hurting."Don't worry, be happy!

"Clearly, energy prices serve as a tax, they reduce the disposable income available to do other things and they take some oxygen out of the economy," Snow said. "Energy is my concern. I think energy is the biggest concern," he added.

But Snow said the U.S. economy is currently managing to withstand the "headwinds" of oil at $60 a barrel. When asked if these energy prices portend a recession, Snow said: "No. I don't see it derailing the strong recovery we're in ... but it does take a few tenths of a (percentage) point off GDP growth, that's for sure."

Monday, June 27, 2005

BIS: US Urged to Act First on Global Imbalances

by Calculated Risk on 6/27/2005 10:44:00 PM

From the Financial Times, the Bank for International Settlements (BIS) warned Monday that "growing domestic and international debt has created the conditions for global economic and financial crises".

UPDATE: Macroblog links to the BIS report with key excerpts.

The Basel-based organisation's annual report said no one could predict if and when such international economic imbalances would unravel but "time might well be running out".The BIS urged the US to act first:

"Given the size of the [US] government deficit, the obvious first step would be to cut expenditures and raise taxes"...The report then turned pessimistic.

Without a smaller budget deficit, lower private sector consumption and higher savings, there was little likelihood of stabilising the ballooning US current account deficit. The ever widening deficit “could eventually lead to a disorderly decline of the dollar, associated turmoil in other financial markets, and even recession."

...the BIS report questioned the Bush administration's willingness to impose the required policies to back up its deficit reduction ambition ..."Time is running out" and no action will be taken "in the near term". How sad.

"If what needs to be done to resolve external imbalances is reasonably clear, it also seems clear that much of it is simply not going to happen in the near term."

Housing Misinformation

by Calculated Risk on 6/27/2005 02:57:00 PM

The LA Times publishes a small community newspaper for my neighborhood called the Daily Pilot. The business section of today's Pilot featured an article on housing. What caught my eye were some quotes from local real estate professionals.

"Much of the appreciation we're seeing is permanent."John Burns, president of Irvine-based John Burns Real Estate Consulting June, 2005

Compare to:

"Stock prices have reached what looks like a permanently high plateau. I do not feel there will be soon if ever a 50 or 60 point break from present levels, such as (bears) have predicted. I expect to see the stock market a good deal higher within a few months."Irving Fisher, Ph.D. Economics, Oct. 17, 1929

But far more discouraging are the comments attributed to Bill Cote of the Cote Realty Group. He doesn't believe there is a bubble, but he also apparently wants to withhold information from the home buying public:

[Cote]...is bothered by the potential of academics forecasting real estate deflation to discourage the public. He said it's tough for general audiences to discern between the various forecasts that are out there."People start talking ..." We wouldn't want that to happen.

"It affects the confidence of the market -- people start talking," Cote said. "People can't tell unless they're sophisticated in economics."

Houses and Interest Rates

by Calculated Risk on 6/27/2005 12:22:00 AM

My latest post is up on Angry Bear: The Impact of Interest Rates on House Prices. Several people are arguing that housing prices are appropriate based on current interest rates. I argue that this is incorrect.

And from the NY Times: How Home Prices Can Be Hot but Inflation Cool. This article discusses a potential problem with the CPI calculation. When houses prices fall that might increase the reported CPI:

... when housing prices fall, a trend that most people would deem anti-inflationary, and renting becomes more attractive than owning, the index might process the information as evidence that inflation is on the rise. "We got a great deal of criticism that we were overstating inflation in the early 1990's, because housing prices were declining and rents were going up steadily," Mr. Jackman said.And my friend Mike Shedlock is hearing "Warning bells from homebuilder suppliers".

Best to all.

Friday, June 24, 2005

Buffett Examines living in Squanderville

by Calculated Risk on 6/24/2005 09:17:00 PM

Kash covered the political reaction to the announcement that China National Offshore Oil Corporation, or CNOOC, is bidding for Unocal. MaxSpeak and Dr. Setser work the numbers.

This event reminds me of the following cautionary tale from Warren Buffett (Oct, 2003).

[T]ake a wildly fanciful trip with me to two isolated, side-by-side islands of equal size, Squanderville and Thriftville. Land is the only capital asset on these islands, and their communities are primitive, needing only food and producing only food. Working eight hours a day, in fact, each inhabitant can produce enough food to sustain himself or herself. And for a long time that's how things go along. On each island everybody works the prescribed eight hours a day, which means that each society is self-sufficient.UPDATE: Buffett was on CNBC Thursday June 23rd. Here are his comments on China:

Eventually, though, the industrious citizens of Thriftville decide to do some serious saving and investing, and they start to work 16 hours a day. In this mode they continue to live off the food they produce in eight hours of work but begin exporting an equal amount to their one and only trading outlet, Squanderville.

The citizens of Squanderville are ecstatic about this turn of events, since they can now live their lives free from toil but eat as well as ever. Oh, yes, there's a quid pro quo-but to the Squanders, it seems harmless: All that the Thrifts want in exchange for their food is Squanderbonds (which are denominated, naturally, in Squanderbucks). Over time Thriftville accumulates an enormous amount of these bonds, which at their core represent claim checks on the future output of Squanderville. A few pundits in Squanderville smell trouble coming. They foresee that for the Squanders both to eat and to pay off-or simply service - the debt they're piling up will eventually require them to work more than eight hours a day. But the residents of squanderville are in no mood to listen to such doom saying.

Meanwhile, the citizens of Thriftville begin to get nervous. Just how good, they ask, are the IOUs of a shiftless island? So the Thrifts change strategy: Though they continue to hold some bonds, they sell most of them to Squanderville residents for Squanderbucks and use the proceeds to buy Squanderville land. And eventually the Thrifts own all of Squanderville. At that point, the Squanders are forced to deal with an ugly equation: They must now not only return to working eight hours a day in order to eat - they have nothing left to trade - but must also work additional hours to service their debt and pay Thriftville rent on the land so imprudently sold. In effect, Squanderville has been colonized by purchase rather than conquest. It can be argued, of course, that the present value of the future production that Squanderville must forever ship to Thriftville only equates to the production Thriftville initially gave up and that therefore both have received a fair deal. But since one generation of Squanders gets the free ride and future generations pay in perpetuity for it, there are - in economist talk - some pretty dramatic "intergenerational inequities."

Buffett said he doesn't subscribe to the view that China is engaging in a trade war with the U.S. He said Chinese corporate takeovers, such as CNOOC Ltd's (CEO) recent bid for Unocal Corp. (UCL) were an "inevitable" consequence of the U.S. trade deficit. He noted that the U.S. imported far more goods from China than it sold to the nation.

"If we're going to consume more than we produce, we have to expect to give away a little bit of the country," said the "Oracle of Omaha."

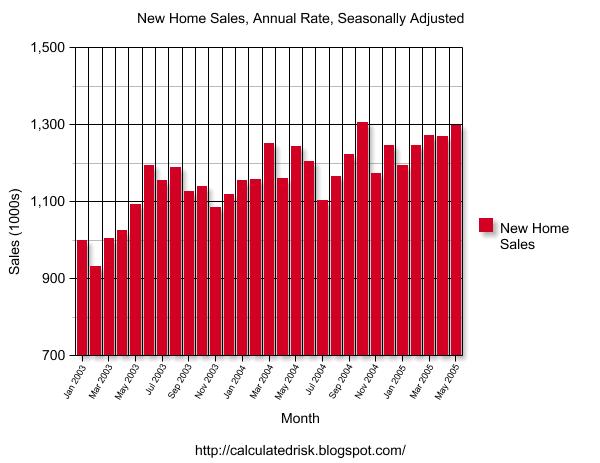

May New Home Sales: 1.298 Million

by Calculated Risk on 6/24/2005 10:19:00 AM

According to a Census Bureau report, New Home Sales in May were at a seasonally adjusted annual rate of 1.298 million vs. market expectations of 1.32 million. April sales were revised down significantly to 1.271 Million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

Sales of new one-family houses in May 2005 were at a seasonally adjusted annual rate of 1,298,000, according to estimates released jointly today by the U.S. Census Bureau and the Department of Housing and Urban Development. This is 2.1 percent above the revised April rate of 1,271,000 and is 4.4 percent above the May 2004 estimate of 1,243,000.

The Not Seasonally Adjusted monthly rate was 120,000 New Homes sold, up from a revised 117,000 in April.

The median sales price of new houses sold in May 2005 was $217,000; the average sales price was $281,400.

UPDATE: Add graph of median and average prices.

The average sales price is down slightly and the median price is the lowest since September of 2004.

The seasonally adjusted estimate of new houses for sale at the end of May was 442,000. This represents a supply of 4.2 months at the current sales rate.

The seasonally adjusted supply of New Homes was 4.2 months, about normal for the last few years. The supply for April was also 4.2 months, revised from 4.1 months.

New Home Sales were below Wall Street forecasts. The story is the downward revisions for March and April. Both months were originally reported as record sales, but they have been revised to be below the record of last October.

Thursday, June 23, 2005

Buffett on Housing: Some people may regret recent purchases

by Calculated Risk on 6/23/2005 10:24:00 PM

Warren Buffet was interviewed on CNBC today. Here are a few of his comments as reported by Dow Jones:

On The Real-Estate Bubble:

Lending practices, low interest rates, and "the psychology that ensues when an asset class moves year after year and people feel 'why didn't I get into it before?'" is creating a precarious situation in some of the real estate markets, Buffett said.On the Dollar and the Trade Deficit:

At the high end of the market, Buffett said people may regret recent purchases.

Buffett said the trade deficit was "a deeply embedded structural problem."On China:

The investor cited Federal Reserve Chairman Alan Greenspan in 2002, saying that countries who experience similar trade-deficit trends in the past, "invariably have run into problems."

"Eventually the current-account deficit will have to be restrained," Buffett said.

"We've gone from being a country that owned more of the rest of the world than they owned of us to a country probably $3 trillion in the hole right now in terms of our net worth position," Buffett said. "So it will have had a effect, it may be a month from now, it may be five years from now."

As a consequence of such imbalances, Buffett warned that the dollar will continue its downdraft "at some point," and indicated that he expects the dollar to be weaker five years from now.

Buffett said he doesn't subscribe to the view that China is engaging in a trade war with the U.S. He said Chinese corporate takeovers, such as CNOOC Ltd's (CEO) recent bid for Unocal Corp. (UCL) were an "inevitable" consequence of the U.S. trade deficit. He noted that the U.S. imported far more goods from China than it sold to the nation.

"If we're going to consume more than we produce, we have to expect to give away a little bit of the country," said the "Oracle of Omaha."

Fed Gov Olson: Housing Concerns

by Calculated Risk on 6/23/2005 11:16:00 AM

Federal Reserve Governor Mark Olson expressed concern today about "homebuying decisions premised on unrealistic rates of home appreciation":

Over the past several years, there has been an explosion of new and novel mortgage products, including mortgages that allow homeowners to skip mortgage payments (which results in increasing the size of their mortgage balance) and mortgages that allow homeowners to pay only the interest on a loan, and not the principal, for a preset period at the beginning of the life of their mortgage loan. Many of these products can be useful financial tools for homebuyers and, indeed, may have helped make homeownership more accessible for some households. But to the extent that these new mortgage products promote homebuying decisions that are premised on unrealistic rates of home appreciation, they raise concerns. Some borrowers may not be able to sustain such a loan over a long time horizon if the pace of home price growth moderates. In particular, when the payments on these novel mortgages adjust upward, the homebuyer may not be able to refinance such mortgages unless the home has increased in value.At the same conference, according to an MSNBC article, Cleveland Fed President Sandra Pianalto cited a study:

... that found 25 percent of Americans claim to have no spare cash after covering regular expenses, warned that tapping wealth stored in the family home carries risks.In a related commentary Double bubble trouble Danielle DiMartino points out that:

“Increasingly, home owners are using home equity as a source of ready cash ... this doesn’t bode well for the ownership society that we’re trying to build,”

Delinquency and foreclosure rates have been falling

The reason, said MBA chief economist Doug Duncan, is strong job creation.

Housing is a chief driver of job creation.

Housing is being driven by "creative loans". (see Olson's comments above)

And she concludes:

The debate reminds us that falling prices not only will coincide with higher foreclosures, they also will be accompanied by millions of pink slips.

Wednesday, June 22, 2005

Option ARMs

by Calculated Risk on 6/22/2005 05:54:00 PM

In the comments to an earlier post, malabar asked if "something like the PIK (payment in kind) bonds used during the 80s LBO days" were being used in the housing market. I suggested that Option ARMs might be similar in that one of the options is a minimum monthly payment that allows for negative amortization.

And reading our minds, The Housing Bubble featured a post today on option ARMs:

S&P Warns On Option ARMs

The alarms about option ARM loans couldn't be any louder. "Recently, option ARMs have become increasingly prevalent in the market. After extensive research, Standard & Poor's has determined that additional credit enhancement is required to account for the increased risk of default resulting from the payment shock inherent in these loans."

"The ratings company said the tightening applies to loans that are bundled into mortgage-backed securities for sale to investors as well as option adjustable-rate mortgage loans, or option ARMs, The Wall Street Journal said."

"Some economists fear that option ARMs and other loans that reduce initial payments are fueling house-price inflation by enabling people to bid more for homes than they could if they were taking out conventional loans, said the Journal."

"Option ARMs and similar loans are among 'the only things left that are keeping home prices rising,' Stuart Feldstein, of (a) financial-services market-research firm."

This link reveals the problem may be bigger than previously reported. "According to UBS AG, option ARMs now account for 40 percent of prime-rated mortgages packaged into securities, compared to just 1 percent in 2003."

The widespread use of Option ARMs is clear evidence of excessive leverage in the housing market.

Thanks to malabar. Hat tip to Ben Jones.

The Refinery Myth

by Calculated Risk on 6/22/2005 03:15:00 PM

Bloomberg reports that Chevron is expanding their Pascagoula, Miss. refinery to boost gasoline output:

The expansion will raise daily gasoline output by 11,900 barrels, or 500,000 gallons, to about 131,000 barrels, [Steve Renfroe, Chevron Spokesperson] said. The $150 million project is expected to begin in July and be finished in late 2006.I don't doubt that additional refining capacity will be needed. But the following sentence in the article perpetuates the myth that the lack of refining capacity is contributing to the high price of oil:

The shortage of refining capacity worldwide has contributed to the 57 percent rise in oil prices in the past year.This is similar to a recent comment by Saudi oil minister Ali al-Naimi:

"There is no shortage of oil. It's there. What is driving the price is the inability to make the oil into products."The BBC article continues:

Some analysts say there are insufficient oil refineries, both in the US, where no new refineries have been built since 1976, and worldwide.Here is a simple diagram of a bottleneck:

This shortage could help keep oil prices high.

Raw Material --->> bottleneck --->> Finished Good

What happens with a bottleneck? If the process is running at full capacity, there is a fixed supply of finished goods, so the price of the Finished Good will rise rapidly with any increase in demand.

But what happens to the price of the raw material? Since the process is running at full capacity (a bottleneck), the demand is fixed, and any additional supply of raw material will cause the price of the raw material to drop!

For the Oil industry: Crude oil is the raw material, the potential bottleneck is the refining process and the finished good is gasoline (also other products, but I'll use gasoline in this example). If refining is at or near full capacity, any additional demand for gasoline would increase the price of the finished good (gasoline) but would not change the demand for crude oil (demand is fixed by the refining bottleneck).

Since demand for crude would be fixed with a bottleneck, any additional supply of crude would depress the price of the raw material (crude oil). Therefore the lack of refining capacity could only depress the price of crude and would not contribute to the rise in the price of crude - the opposite of what is being reported. Adding more refining capacity would increase the demand for crude oil and could lead to higher crude oil prices, unless additional supply of crude is brought online.

Perhaps the Saudi oil minister has ulterior motives for blaming refining for the high price of crude oil, but that doesn't mean the financial press should perpetuate the myth.

UPDATE: In the comments, darffot suggests that he interprets al-Naimi's comments as: The lack of refining capacity for sour crude is pushing up the price of sweet crude. Here is darffot's comment:

i would like to offer an alternative interpretation, which is the way i have always taken al-Naimi's comments on this issue: the incremental production adds coming out of SA and elsewhere is primarily high-sulfur "sour" oil. this is oil which most refineries cannot process, especially thanks to recent enactment of emissions legislation in various parts of the world. just as American electricity producers created a glut of NG-based power plants in keeping with the clean air theme, refinery capacity additions have been skewed toward light sweet oil, which is easier to process with lower pollutants. and, just like the NG-turbine additions, these geniuses did not stop to think beforehand whether the supply would be there when the capacity came on.

the result today is that there is high competition for light sweet crude (the widely followed WTI) while the excess sour production goes begging for buyers. this can be clearly seen in the historically large spreads between sweet and sour crude products, and is also very apparent in the chart of Valero (VLO), the US based refiner most heavily focused on sour crude. just listen to a VLO conference call and you will learn how they are printing money thanks to the record spreads between sweet and sour. this, i believe, is what al-Naimi is alluding to when he says there is not enough refining capacity--there's not enough sour refining capacity to keep in alignment with the composition of crude coming online at the margin. meanwhile, there is high competition for the sweet crude.

UPDATE 2: According to a recent Forbes article, the spread between light and sour has increased from $2.50/ bbl to almost $9/bbl over the last 2 years. This is darffot's point and he is clearly correct about more demand for light sweet crude.

However, this still means there has been a substantial price increase for sour crude (from around $27 to almost $50 today spot prices). Perhaps a few dollars of the WTI prices are related to refinery mix (but that isn't what the financial press claimed), but blaming the doubling of oil prices on lack of sour crude refining capacity is also incorrect.

Tuesday, June 21, 2005

UCLA Anderson Preview: Bubble Burst could lead to Recession

by Calculated Risk on 6/21/2005 02:41:00 AM

The UCLA Anderson Forecast will be released today. According to a preview in the LA Times:

... the UCLA forecasters once again predict that a housing slowdown could push California into recession, while causing a noticeable slowing in U.S. economic growth.

UPDATE: Another preview article: Home bubble could weaken

the residential real estate market could soften in the latter half of this year, slowing the state and national economies.ORIGINAL POST:

Still, Edward Leamer, an author of the quarterly outlook from the university's Anderson School of Business, stopped well short of forecasting a recession this year. "The probability remains essentially zero ... before April 2006."

Leamer said the first indication of a turn for the economy will be fewer home sales with properties sitting longer on the market. Then builders will retreat and pull fewer permits, and jobs that depend on home sales will be lost. While a price softening and not a collapse is expected, this series of events will trickle down through the overall economy.

He noted a drop in spending on homes played a major role in nine of the past 10 economic downturns since World War II.

While the outlook for the economy over the next 12 months is positive, predicting after that gets dicey, but real estate will play a large role in what happens.

"The bad news is that we have real problems in the housing sector that will cause the economy a good deal of stress soon enough," Leamer said in his report, referring to home prices that have reached unsustainable levels in some markets.

Others are expressing similar concerns:

On Monday, Merrill Lynch added to the bubble concerns, releasing a report that said U.S. economic growth could slow by a full percentage point next year if home prices were to stagnate in the biggest cities.And on California:

Merrill Lynch senior economists found that six California markets — San Diego, Inland Empire, Los Angeles, San Francisco, San Jose and Sacramento — were "well in bubble territory" with above-normal ratios of home prices to household incomes.

Federal Deposit Insurance Corp. data, provided to The Times on Monday, further underscored such concerns that declines in the nation's biggest housing markets could throttle the entire U.S. economy.

... to the UCLA economists, the sizzling housing market has masked a number of weaknesses in California's economy, including job growth that is not as good as it looks. Employment and personal incomes in California have gained only modestly in the last year, UCLA's Thornberg said. Yet, many Californians "feel" wealthier because they perceive their homes to be worth a lot more.They could say the same thing about much of the US: the housing boom has masked otherwise weak job growth. Look for more comments later today.

Monday, June 20, 2005

Port of Los Angeles: Less traffic in May

by Calculated Risk on 6/20/2005 02:49:00 PM

The Port of Los Angeles released their May statistics today. Inbound (loaded containers) was 313 thousand compared to 329 thousand in April - a decline of 5%.

Outbound volume was 105 thousand loaded containers vs. 107 thousand for April. This is similar to the 1% decline for the Port of Long Beach.

Port of Long Beach statistics correlate better with imports from China, but I can't overlook the weak imports for the Port of LA.

Housing: Psychology Change?

by Calculated Risk on 6/20/2005 12:05:00 AM

My most recent post is up on Angry Bear - Housing: Bubble Talk.

UPDATE: I added this to my AB post: The WSJ (Greg Ip) has a front page article this morning: Booming Local Housing Markets Weigh Heavily on Overall Sector (pay): A few quotes:

New federal housing data show that the nation's most overheated local housing markets now make up such a large share of the total U.S. market that a sharp fall in their values could stall or slow national economic growth.

...

"It's a widespread boom and has macro implications," says Richard Brown, chief economist of the FDIC. "A slowdown would not only hurt these markets, but the U.S. as a whole."

...

Unlike stocks, the housing market "would be more likely flat with 10% to 20% declines in some regions, or down slightly nationally with some regions looking ugly," says Ethan Harris, chief U.S. economist at Lehman Brothers. Even local housing crashes take years to unfold, he says.

Also see WSJ: Fannie Sees Higher Odds of Regional Busts

ORIGINAL POST:

A couple of interesting facts about the San Diego market: First, here is an interactive graph showing the number of condos in the downtown San Diego market by week. There has been a surge in listings downtown.

And the last few paragraphs in this article indicate the job market is slowing down for housing related jobs in San Diego.

Phil Blair, a co-owner of the San Diego offices of Manpower, said construction firms are gearing up for continued growth. In a survey asking local companies about their hiring activity over the next three months, construction firms were the most optimistic that they would be adding new staff.Construction firms are hiring, but real estate and financing firms are cutting back. Is the bubble ending?

Blair said that financial and real estate firms were among the least optimistic, with some firms planning to lay off employees.

"Usually construction and real estate go together, but not this time around," he said. "I don't know if that means that there's some sort of a lag between one industry and the other or if the real estate people are beginning to worry that a bubble has burst."

He added that with real estate purchasing and mortgage applications slowing, there is less demand for work in those industries.

Sunday, June 19, 2005

Times: Is the global housing bubble set to burst?

by Calculated Risk on 6/19/2005 03:37:00 AM

The London Sunday Times asks: Is the global housing bubble set to burst?

As glittering spires continue to rise around the world and buyers still dream of escape to idylls in the sun, the questions grow more pressing. What has driven the boom? Has globalisation changed the law of gravity? Can the vertiginous ascent continue? Or is the biggest pop ever heard about to deflate the global property bubble and take the world economy down with it?The Times does not completely answer the question. They do argue that stagnation is more likely than a crash. But price stagnation might lead to recession, and a recession might cause lower house prices leading to a deeper recession - a vicious cycle.

Perhaps their real opinion can be gleaned from their choice of companion pieces: Booms Past.

TULIP MANIA 1634For a great summary of previous bubbles, I recommend "Extraordinary Popular Delusions And The Madness Of Crowds", By Charles MacKay, 1841.

In Holland the craze for collecting tulips peaked in 1636 when investors paid more than 5,000 florins — about £25,000 at today’s prices — for a single bulb. But when buyers dried up, prices plummeted.

SOUTH SEA BUBBLE 1711

The vogue for public companies in the early 1800s produced the South Sea Company, which was granted a monopoly over trade to North America. But the bubble burst in September 1720 when banks could not collect loans on inflated stock.

1929

In the 1920s technological change saw the Dow Jones rise sevenfold, prompting investors to stake their life savings on the stock market. Interest rates rose, Wall Street panicked and by November 1929 two-thirds the Dow’s value had gone.

LAWSON BOOM

House prices in Britain soared in the late 1980s, buoyed by low interest rates and tax cuts. When interest rates doubled in 18 months house prices crashed, dropping by 30%-40% in some areas.

DOTCOM BUBBLE

In the 1990s internet stocks boomed. But after peaking in spring 2000 they lost two-thirds of their value in three years. Many firms vanished.

Friday, June 17, 2005

EU Crisis as Budget Deal Collapses

by Calculated Risk on 6/17/2005 09:04:00 PM

Financial Times: EU crisis as Britain rejects deal on budget

Excerpt:

The European Union was plunged into political crisis on Friday night after Britain led the way in blocking a proposed deal on the new seven-year budget.This is another serious setback for the EU and is not good for America. A European Union in disarray and possibly entering recession will likely exacerbate the global imbalances and probably lead to larger US trade and current account deficits.

Tony Blair, the UK prime minister, was one of a minority of leaders who refused to accept a compromise package, as the Brussels summit collapsed in acrimony shortly before midnight. The failure of the talks means the transfer of billions of euros of aid to former communist countries in eastern Europe, due to start on January 1 2007, may be delayed.

The political ramifications of the breakdown, coming after French and Dutch voters rejected the EU constitution, could be severe.

See Dr. Serser's 6.4% of GDP current account deficit in q1

General Glut's 6.4% AND GROWING

See Dr. Altig's The EU Divide and more.

Thursday, June 16, 2005

May Trade Deficit Forecast: Part I

by Calculated Risk on 6/16/2005 06:04:00 PM

Last month I started building a simple model to help forecast the monthly trade deficit. A review of the partial forecast showed some promise.

So here we go for May starting with oil. Using the same model (described here) the ERPP trade numbers for May are forecast to be:

IMPORTS: Energy Related Petroleum Products.

Barrels Crude: 337.9 million barrels.

Barrels Other ERPP: 85.0 million barrels.

DOE Price per barrel (Crude): $43.90

DOE Price per barrel (Other): $50.48

Preliminary - Total NSA ERRP Imports: $19.1 Billion

NOTE: The BLS reports petroleum import prices fell 6.5% in May from April. The above model used DOE prices. After reviewing the prior prices and comparing the DOE and BLS approaches, the DOE has been slightly more accurate. However, I think it might be even better to try to split the difference. The BLS approach would predict P(crude) = $41.85. DOE P(crude) = $43.90. So the modified forecast for Imports NSA is:

BLS/DOE Price per barrel (Crude): $42.88

BLS/DOE Price per barrel (Other): $49.31

Forecast: Total NSA ERRP Imports: $18.7 Billion

Total ERPP FORECAST:

Imports SA: $17.4 Billion (seasonal factor estimated at 0.93 for May)

Exports SA: $1.9 Billion

Balance ERPP: $15.5 Billion

Housing: News Stories Links

by Calculated Risk on 6/16/2005 02:57:00 AM

UPDATE: I've been notified that "Housing Links" will not be continued. He recommends these two sites:

Patrick's Housing Links

RGEMonitor Housing Market Bubble?

I've been directed to a new housing resource: Housing Links. This site is a running compendium of stories, commentary and analysis on all aspects of the housing market. Here are some recent examples:

UPDATE2: In the comments, Stephane Grenier directs us to his interesting article "Is There Really a Real Estate Bubble?". He references me!

UPDATE: Two new stories in The Economist about the perils of the housing boom / pending bust: In come the waves (Great Graphs) and After the fall.

The Trillion-Dollar Bet - The NY Times looks at the widespread use of Adjustable Rate Mortgages:

This year, only about $80 billion, or 1 percent, of mortgage debt will switch to an adjustable rate based largely on prevailing interest rates, according to an analysis by Deutsche Bank in New York. Next year, some $300 billion of mortgage debt will be similarly adjusted.The Mortgage Trap - BusinessWeek "Lenders are cranking out an ever-growing array of financing schemes and lowering standards to keep the housing boom going":

But in 2007, the portion will soar, with $1 trillion of the nation's mortgage debt - or about 12 percent of it - switching to adjustable payments, according to the analysis.

All those innovative mortgage products are a sure sign that lenders are doing everything they can to keep the housing boom going and to capitalize on yet another round of falling interest rates that no one expected. There are plenty of other signs of frenzy as well. Home appraisers complain that mortgage originators are demanding the optimistic appraisals needed to close on loans. "They started warning me to 'be a team player' and to 'hit the number' they needed to seal the deal," says Robert Burnitt, an appraiser in Midlothian, Tex.And some positive stories:

Purchase Activity at Record High; Refinance Volume Jumps In Latest Application Survey - The Mortgage Bankers Association reports their "seasonally-adjusted Purchase Index increased by 10.4 percent to 529.3, a record high":

"This week there was a combination of record-setting purchase activity as well as a substantial pickup in refinance applications, with the refinance index at its highest level since April 2004," said Michael Fratantoni, senior director of single-family research and economics.Builder Confidence Hits New High For 2005 - According to a survey by the National Association of Home Builders and Wells Fargo, "single-family home builders are more confident this June than they’ve been all year".

The most optimistic builders are in the West, where an HMI reading of 88 far outpaces that of builders in all other regions. Moreover, the 88 reading reflected a solid four-point gain from last month. Southern builders were also a bit more confident this time around, posting a one-point gain in their regional confidence gauge to 76 in June. Builders in the Northeast maintained a healthy, 70-point reading on the confidence scale, while builders in the Midwest registered a two-point confidence boost, to 52.

Check it out. Enjoy!

Wednesday, June 15, 2005

Housing: The Empire Strikes Back

by Calculated Risk on 6/15/2005 06:35:00 PM

In a well coordinated attack, the Empire today unleashed a barrage of statistics and comments from in-house economists to poke holes in the silly notion of a "housing bubble". First up was Carl Steidtmann, chief economist of Deloitte Research:

"There has been much discussion recently about a housing bubble, but the truth is that home price appreciation has slowed considerably in the past three months. The time to talk about a bubble was last December," says Carl Steidtmann, chief economist of Deloitte Research and author of the monthly index.By this logic you should have worried about the Nasdaq bubble in the late '90s, but in March of 2000 everything was fine. Not the best investment strategy. And "job growth continues to accelerate"? The 3 month moving average of payroll growth (Seasonally adjusted from the BLS) shows job growth is at best flat after peaking in the Spring of 2004.

"Consumer spending growth in the summer months will be largely dependent on the direction of home prices and job growth," continued Steidtmann. "As job growth continues to accelerate, we should see a corresponding pickup in real wage growth."

But that was just the beginning. The ubiquitous David Lereah responded to Fed Chairman Greenspan's recent remarks:

"Yes, there is froth in the markets, but froth can be healthy," said David Lereah, chief economist for the National Association of Realtors. "It's not a bad word."Froth for a foamy latte or cappuccino might be good; froth in the housing market, especially when you are a new home buyer, is decidedly not good.

Economists representing members of the Washington, D.C.-based Homeownership Alliance, which includes a coalition of about 15 housing-related organizations, fired another salvo: See Housing boom won't let up.

Frank E. Nothaft, chief economist for mortgage industry giant Freddie Mac said "there are signs of 'suds' around the country" (good in your beer) but he is not worried:

"I think we'll see some gradual moderation in house-price valuation over the next couple of years," with about a one-in-three chance of a region in the country seeing stagnant or declining home values over the next couple of years, linked to regional economic weakness.Paul Merski, chief economist for the Independent Community Bankers of America added:

"Bankers are being very diligent now about their lending practices," and the FDIC is "closely monitoring bankers' lending practices right now due to the long run in the housing boom."Since bankers are being very "diligent", I wonder why the Office of the Comptroller of the Currency, the FED, the FDIC and other agencies took the highly unusual step of issuing new credit risk management guidance for home equity lending in May.

"(The notion) of exotic products out there that are extremely dangerous is well overblown."

Merski also addressed the issue of home-price "froth." He said, "Economists have a saying that unsustainable trends will not be sustained," and that may hold true for some markets that have rapid, double-digit price appreciation. He forecast a "reasonable cooling off in certain markets in the prices but certainly no crashes in these markets because of the strong demand." Even so, the overall housing market should be strong for the rest of the year and going into 2006, he added.No crashes. What a relief!

And finally, David W. Berson, chief economist for Fannie Mae added:

"There are no signs of any slowing in the housing market at all. You need a pretty good decline for the second half of the year not to set a record this year."Those final comments are true; the housing market is still HOT.

For some reason I'm having the same reaction to all of these industry economists' comments as I do when the oil industry scientists assure me that global warming is not a problem. Maybe I need some suds!

Housing: Record Purchase Activity and More

by Calculated Risk on 6/15/2005 03:22:00 PM

The Mortgage Bankers Association (MBA) released their weekly report today showing record purchase activity.

The seasonally-adjusted Purchase Index increased by 10.4 percent to 529.3, a record high, from 479.3 the previous week whereas the seasonally-adjusted Refinance Index increased by 25.6 percent to 2967.4 from 2362.1 one week earlier.The use of ARMs decreased:

"This week there was a combination of record-setting purchase activity as well as a substantial pickup in refinance applications, with the refinance index at its highest level since April 2004," said Michael Fratantoni, senior director of single-family research and economics.

The adjustable-rate mortgage (ARM) share of activity decreased to 30.9 percent of total applications from 31.7 percent the previous week.Also, the National Association of Home Builders and Wells Fargo reported that home builders were optimistic:

"single-family home builders are more confident this June than they’ve been all year".Meanwhile, DataQuick reported:

The most optimistic builders are in the West, where an HMI reading of 88 far outpaces that of builders in all other regions. Moreover, the 88 reading reflected a solid four-point gain from last month. Southern builders were also a bit more confident this time around, posting a one-point gain in their regional confidence gauge to 76 in June. Builders in the Northeast maintained a healthy, 70-point reading on the confidence scale, while builders in the Midwest registered a two-point confidence boost, to 52.

The sales pace of homes in Southern California eased back a notch in May as prices continued to climb to record levels, the result of steady demand and affordable mortgage financing, a real estate information service reported.Although appreciation has slowed in some of the hot markets like San Diego, overall the housing market is still HOT!

Port of Long Beach: May Import Traffic Strong

by Calculated Risk on 6/15/2005 02:02:00 AM

Import traffic at the Port of Long Beach rose 6% over April, almost to the highs of last fall's heavy shipping season. The Port of Los Angeles will report in the next couple of days.

For Long Beach, the number of loaded inbound containers for MAY April was 288 thousand, up 6% from April and up 19% from May 2004. Outbound traffic was off 1% at 106 thousand containers, just below April's record.

And in a related story, the Port of Long Beach hosted the "Peak Season Forecast Conference" on Tuesday.

At the Pulse of the Ports conference, the experts forecast 2005 cargo gains of 10 to 15 percent. In preparation for this year's increase, they said they have added workers and equipment, and cargo has been moving smoothly.This shipping data probably indicates near record imports from China. My very preliminary guess is that US imports from China will be over $19 Billion NSA for May compared to $18.12B for April 2005.

"We may see two-to-three-day delays," during the peak season, said Frank Baragona of CMA CGM.

"We had one-week delays last year and that's not going to happen this year," said Doug Tilden of Marine Terminals.

Tuesday, June 14, 2005

Thoma and Ritholtz: Where Will Rates Go From Here?

by Calculated Risk on 6/14/2005 06:40:00 PM

Dr. Thoma (Economist's View) and Barry Ritholtz (The Big Picture) discuss the Fed's path in the WSJ free feature "Where Will Rates Go From Here?"

Check it out!

Fed Gov Bies: Current Regulatory Issues

by Calculated Risk on 6/14/2005 11:51:00 AM

Federal Reserve Governor Susan Schmidt Bies spoke on "Current Regulatory Issues" today in South Carolina. She touched on the housing market and credit risk issues in her speech to the North Carolina Bankers Association.

In particular, in the commercial and residential real estate sectors, we worry that borrowers could become increasingly speculative, buying beyond their means and hoping for asset price appreciation--whether they are buying for their own use or strictly for the sake of investment. We worry that competitive pressures could drive banks to lower their underwriting standards, implicitly encouraging such speculation. And we worry that, in the inevitable downturn, credit quality could deteriorate to the extent that some banks could experience significant losses.

The residential real estate sector has been experiencing a remarkable bull market, with home prices rising 11.2 percent last year--the fastest rate in more than a quarter-century. Along with the high home prices, we see indications that underwriting standards are beginning to weaken. For example, "affordability products"--such as interest-only loans, negative amortizations, and second mortgages with high loan-to-value ratios--are becoming more popular; subprime lending is growing faster than prime lending; adjustable-rate mortgages, or ARMs, have grown substantially and now account for more than a third of all mortgage originations, the highest level since 1994. Industry experts are increasingly concerned about the quality of collateral valuations relied upon in home equity lending and residential refinancing activities. More homes are being purchased not as primary dwellings, but as vacation homes or pure investments, in which case anticipated price appreciation may be a large factor influencing purchase decisions. According to the National Association of Realtors, purchases of second homes and purchases of residential real estate for investment purposes together accounted for almost 40 percent of all home purchases last year.

Given the vast growth in residential housing markets and the apparent slippage in underwriting standards in certain sectors, it is entirely appropriate for banking supervisors to seek to ensure that banks are employing proper risk-management practices. Last month, the federal banking agencies released guidance on credit-risk management for financial institutions' home equity lines of credit (HELOCs). The recent growth in HELOCs has been remarkable; at the end of 2004, outstanding drawn HELOCs at all insured commercial banks totaled $398 billion, a 40 percent increase over 2003. Meanwhile, the agencies have observed some easing of underwriting standards, with lenders competing to attract home equity lending business. Lenders are sometimes offering interest-only loans and are sometimes requiring very small down payments and limited documentation of a borrower's assets and income. They are also relying more on automated-valuation models and entering into more transactions with loan brokers and other third parties. Given this easing of standards, there is concern that portions of banks' home equity loan portfolios may be vulnerable to a rise in interest rates and a decline in home values. In other words, there is concern that not all banks fully recognize the embedded risks in some of their portfolios.

Also, Gavin sent me this commentary from Australia: Beware the bang if the property bubble bursts. It is possible that both the UK and Australia are leading indicators for the US housing market.

UK "fear of housing crash"

by Calculated Risk on 6/14/2005 01:08:00 AM

From the Telegraph: A Royal Institute of Chartered Surveyors report on Tuesday sparks fears of a housing crash.

Almost half the country's chartered surveyors reported that house prices were falling in May, the highest total since the recession of 1992.The UK bears watching as a possible early indicator for the US market. The UK started raising rates about 8 months before the US: See my Angry Bear post.

The Royal Institute of Chartered Surveyors will say today that the number of its members reporting price falls has grown sharply - from 37pc in March to 40pc in April to 49pc last month.

The news will spark fears of a house price crash. In the early 1990s, RICS was the first housing market surveyor to predict the market's collapse.

In the latest report, the institute says new buyer inquiries had slipped and the number of completed sales had fallen by 29pc since last May.

Monday, June 13, 2005

Harvard on Housing: "Desperation" Buying

by Calculated Risk on 6/13/2005 07:17:00 PM

Harvard's Joint Center for Housing Studies released a new report: "State of the Nation's Housing 2005". From a story in the Union Tribune:

"Desperation is driving people," said Nicolas Retsinas, director of Harvard's Joint Center for Housing Studies. "They think, 'If I don't get it now, I will never get it.' People are not looking at what they are going to have to pay over the long term. They are asking what is the lowest possible payment I have to make over the next 12 months so I can get in."

In high-cost markets such as San Diego County, most purchases are made with adjustable-interest-rate loans, he noted. The greater buying power such "creative" loans offer is offset by the increased risk of default.

In the priciest metropolitan real estate markets, assuming greater risk is becoming the norm, Retsinas said.

"Although interest-only and adjustable loans can initially save a typical home buyer hundreds of dollars in monthly payments, these loans also leave borrowers vulnerable to sharply higher payments when interest rates adjust or principal payments start to become due."

Click on chart for larger image.

One of the startling statistics is that homebuyers' costs have soared in recent years, despite the record low interest rates and use of Interest Only ARMs.

From a SmartMoney.com review: Get Ready for a Housing Slowdown:

"We want to be sure people are aware that, notwithstanding these past few years, buying a house is not a risk-less investment...this is clearly near the apex of the cycle," says Nicolas Retsinas, director of Harvard's Joint Center for Housing Studies.And a less optimistic view:

To be clear, Retsinas isn't predicting a nationwide housing crisis. Indeed, 77 of the 110 largest metro areas show no affordability troubles and would likely be untouched if the housing bubble popped in the hottest markets, says Retsinas.

Mark Weisbrot, co-director of the Center for Economic and Policy Research, a Washington, D.C.-based think tank, says there's clearly a bubble in the housing market, and that when it bursts it will likely cause a national recession worse than the one following the stock market bubble. In 2001, the strong housing market tempered the downturn. This time, he says, it's difficult to imagine anything that could ease the pain.

Even those markets that didn't experience the huge run-up could be affected. Weisbrot says home prices in those areas won't fall drastically, but the local economies will suffer, as was the case when the stock market popped. And this will eventually dampen demand for housing.

As for first-time home buyers, Weisbrot sees no reason why they should jump in now — particularly with rentals so affordable by comparison. The risks, he says, are so high that he can't understand why anyone would take the gamble.

"Buying a home now in any of the bubble areas is very much like what it was like buying into the Nasdaq," he says. "You could get lucky and it could keep growing [for a little longer], but you are also taking a big risk."

Trade Deficit, Housing and more

by Calculated Risk on 6/13/2005 12:04:00 AM

In today's post on Angry Bear, I looked at the impact of the strong Euro on the US trade deficit with the European Union: "The Euro and the Trade Deficit".

Also, Greg Ip has an excellent article on housing in the WSJ today: "What Happens If Real Estate Goes Bust". A couple of excerpts:

If housing prices do fall, what would it mean for the economy? "A housing bust would be worse [than the stock bust]," says Kenneth Rogoff, an economics professor at Harvard University and former chief economist at the International Monetary Fund.And these interesting statistics:

Homes are collateral for about $7.7 trillion in mortgage and home-equity debt, whereas total margin debt in investors' stock brokerage accounts is only $194 billion. For the same reason, a decline in housing prices would put more bank loans at risk; mortgages make up 40% of the assets of U.S. commercial banks, mortgage-backed securities another 16% and stocks less than 1%.UPDATE: Oops, I forgot the "more" in the title. That can wait for another post!

Best to all!

Sunday, June 12, 2005

UCLA Anderson Forecast: June 21, 2005

by Calculated Risk on 6/12/2005 01:20:00 AM

Just a headsup. Dr. Leamer will present his quarterly forecast on June 21st. It sounds like the housing bubble will be the main topic. The UCLA Anderson forecast is typically one of the most accurate.

I'm confident there will be substantial news coverage.

JUNE 2005 ECONOMIC OUTLOOK

What Goes Up Might Come Down

How Long Can This Hot Housing Market Last?

UCLA - Ackerman Grand Ballroom

Tuesday, June 21, 2005

7:00am - 11:30am

Overview

The current level of hype about real estate bears a worrisome resemblance to the dot.com bubble of the late nineties. Financial companies tout no-money-down interest-only loans as a way of extending speculators' purchasing power, and developers pitch new developments to buyers the way Wall Street analysts used to pitch new IPOs. According to the National Association of Realtors, over a third of total sales in 2004 were to families buying a second home--most for 'investment' purposes.

While housing activity levels are still high from a historical perspective, there are signs that the market is starting to slow. Appreciation rates and sales rates have peaked, and some markets have seen a rapid increase in inventory levels. The recent Fed warning regarding inflation has sent mortgage rates up.

How long can this market last? Are we in for a soft landing or a crash? Who is likely to be left holding the bag when the smoke clears? These are the questions --among many others--about the California and National housing markets that we will attempt to answer at the Conference.

Saturday, June 11, 2005

Housing: Starting to "Chill"?

by Calculated Risk on 6/11/2005 12:06:00 PM

From the Sacramento Bee: "More houses 'for sale' a sign of market chill?" A few excerpts:

The number of capital region homes on the market has risen to its highest level since November 2001, suggesting the market might be seeing the first signs of cooling.So inventories are climbing.

"Inventory is up because of the psychological effect of the media reporting on the 'bubble,' " said Jeff Culbertson, who heads Coldwell Banker's capital region operations, of the barrage of news on a possible price bubble in housing. "Some of those people (investors) bought those properties two years ago and have seen a 50 percent increase in value. A lot of them are saying, 'I rode this up, and maybe I'll relocate my equity someplace else now.' "And from Analyst Pat Veling, president of Real Data Strategies Inc. on inventories:

"I'm surprised it's happening in the (prime) home buying and selling season, but we need to cool the market's jets a bit because it's going far too far, and far too fast, and we don't want the market to collapse under its own weight like it did in the early 1990s."But this could just be a one month anomaly.

Last fall the number of homes for sale in some Southern California markets shot up as sales dropped, causing some to conclude a downturn had begun. Since then, sales have picked up and inventory remains relatively low amid rising prices.So it is too early to tell. But this quote is funny:

"It's too early to panic, for sure," said housing analyst Greg Paquin, president of the Folsom-based Gregory Group.I hope Mr. Paquin lets us know when it is time to "panic"!

Trade Deficit Projection: A Review

by Calculated Risk on 6/11/2005 01:11:00 AM

This month I started to build a simple model to project the trade deficit. I didn't make as much progress as I had hoped, but the first two components (oil imports and China) were somewhat close.

First, I projected oil imports. And then I projected the trade deficit with China.

My model projected $19.3 B Not Seasonally Adjusted (NSA) in energy related petroleum product imports. The actual number was $18.94 B (see Exhibit 17). This is an error of just under 2%.

For the trade balance with China, my model projected a deficit of $15.1B. The actual number (see Exhibit 14) was $14.7B or an error of 2.7%.

Here are each of the components and how the model performed:

| ITEM | Projection | Actual | Error |

| US Exports to China | $3.4B | $3.4B | 0 |

| US Imports from China | $18.5B | $18.12B | 2.1% |

| US Trade Deficit: China | $15.1B | $14.7B | 2.7% |

| Oil: Contract Price BBL | $45.70 | $44.76 | 2.1% |

| Oil: BBLs Crude | 328.6M | 313.8M | 4.7% |

| Oil: Price Other BBL | $52.56 | $50.77 | 3.5% |

| Oil: BBLs Other | 82M | 96.5M | 15% |

| ERPP Total NSA | $19.3B | $18.94B | 1.9% |

UPDATE: I found an error in the oil model. I used 31 days for April to estimate the quantity of Crude. The actual Q(crude) should have been 318 million BBL, or an error of 1.3% (instead of 4.7%). The overall oil imports projection should have been $18.83B vs. actual of $18.94B. That is a dumb error!

I didn't have a good method for estimating "Other" energy related petroleum products. As I wrote: "The good news is that the larger percentage errors for "Other" are not very important for the overall ERPP."

There is much more to do!

Friday, June 10, 2005

Interest Only Loans across the US

by Calculated Risk on 6/10/2005 02:09:00 PM

MSNBC provides a table from LoanPerformance of interest only mortgages as a share of total mortgages for the 50 largest metro areas in 2004. Apparently many of these loans are both Interest Only (IO) and Adjustable Rate Mortgages (ARMs). As MSNBC cautioned:

"... borrowers may be able to buy a more expensive house than they might otherwise afford.MSNBC also quoted some recent data from BusinessWeek:

Trouble is, when borrowers do have to start making principal payments -- after anywhere from 2 years to 10 years -- the monthly payment could jump by up to 50%, or even more if the index for the adjustable rate rises as well."

BusinessWeek Online has also obtained new data from Fannie Mae and Freddie Mac that lend credence to the LoanPerformance numbers. They show that, in April, going by dollar volume, interest-only loans accounted for 35% of the adjustable-rate mortgages in securities sold by Fannie Mae and 39% of the adjustable-rate loans in securities sold by Freddie Mac. That represents a sharp increase for both giants, which buy mortgages from lenders and then repackage them as securities for sale to investors.Yesterday Kash looked at the percentage of ARMs and suggested that it appears

As recently as January, 2004, only 10% of adjustable-rate mortgages in securities sold by Fannie classified as interest-only.

"... people have decided to pay more for their house than they can afford with a fixed-rate mortgage."And he concluded that

"we shouldn't find it surprising if millions of recent home buyers soon find themselves unable to afford to live in their own houses."It is no surprise that a bubble state metro area like San Diego is at the top of the list. But, as a recent story noted, Georgia leads the nation in IOs. That seems unusual.

Interest-Only Loans Across the U.S. Metro Area Interest-Only Mortgages As Share of Total, 2004

San Diego 47.6%

Atlanta 45.5%

San Francisco 45.3%

Denver 43.4%

Oakland 43.1%

See table for next 45 metro areas: MSNBC article.

US Trade Deficit: $57 Billion for April

by Calculated Risk on 6/10/2005 02:23:00 AM

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis released the monthly trade balance report today for April:

"... total April exports of $106.4 billion and imports of $163.4 billion resulted in a goods and services deficit of $57.0 billion, $3.4 billion more than the $53.6 billion in March, revised.Note: all numbers are seasonally adjusted.

April exports were $3.1 billion more than March exports of $103.4 billion.

April imports were $6.5 billion more than March imports of $156.9 billion."

Click on graph for larger image.

This graph shows the monthly trade balances for 2003, 2004 and 2005 and depicts the worsening year over year trade imbalance. The April trade deficit worsened as exports increased $3.1 Billion and imports increased $6.5 Billion.

The recent increase in oil prices had an impact on the April trade deficit. The average contract price for oil jumped from $41.14 in March to $44.76 in April. This is a new record for the import contract price, exceeding the old record of $41.79 set in October.

This graph shows total petroleum imports (NSA) per month for 2003, 2004 and the first four months of 2005. Petroleum imports were about 30% of the trade deficit or about 1.5% of GDP. Even without petroleum imports, the trade deficit would be close to 4% of GDP - a serious problem.

April is the 4th largest trade deficit ever. The trade deficit has been over $50 billion 11 times - the last 11 months in a row.

Thursday, June 09, 2005

America's Debt Binge

by Calculated Risk on 6/09/2005 08:22:00 PM

The Federal Reserve released their quarterly Flow of Funds report today for Q1 2005. The summary: America's debt binge continued.

Borrowing in the first quarter was at an all time high of $2.4 Trillion (annualized) for all sectors. That is double the quarterly borrowing of just 3 years ago.

The leading offenders by percentage debt growth (annualized): State and Local Governments at 16.2%, the Federal Government at 13.8% (2nd worst quarter in almost 20 years), and household home mortgages at 10.6% (down from 2004 levels).

The surprise is the surge in State and Local borrowing. The $271 Billion annualized rate of borrowing is almost double any quarter in the last few years.

With approximately $600 Billion in new debt in Q1 (reported as $2.4 Trillion annualized) and GDP growth of approximately $50B for Q1 (current dollars - see table 3) is the United States just buying growth with debt?

Wednesday, June 08, 2005

Housing Indicators

by Calculated Risk on 6/08/2005 09:12:00 PM

Here are a couple of sites I'm following to check the pulse of the housing market (still tachycardia!):

The Mortgage Banker's Association issues the results of a weekly survey on mortgage applications. The MBAA's seasonally adjusted Purchase Index (PI) is a guide to ongoing purchase loan applications.

Click on graph for larger image.

This is a graph of the PI for the first week of each month since January 2004. Clearly purchase activity has been very stable. The most recent release shows the PI at 479.3, a slight increase from the previous week.

The MBAA also provides a Composite Index (jumps around based on percentage of ReFis), a Refinancing Index and more. They also provide percentages on refinancing and adjusted rate mortgages. Interesting stuff.

The National Association of Home Builders (and Wells Fargo) provide a monthly House Market Index. This is new (UPDATE: tea points out this is not new, here is the historical data) and is based on surveys of home builders. The index currently shows steady interest in new homes.

Tuesday, June 07, 2005

Income Inequality vs. Growth

by Calculated Risk on 6/07/2005 08:55:00 PM

Dr. DeLong directs us to a letter from Greg Mankiw (former chairman of President Bush's Council of Economic Advisers) to the New York Times. In the letter, Mankiw concluded:

Here's the lesson: If policy makers' primary goal is to reduce income inequality, they should put the economy through the wringer. But if they want economic prosperity for all, they should avoid focusing on the politics of envy.Dr. DeLong provides two graphs showing that Dr. Mankiw is wrong. There is extensive research on this subject to support Dr. DeLong's position that the relationship between growth and income inequality is inconclusive. At the extreme, there is no question that income and wealth inequality lead to slower growth (I'll let the reader think about this). But the US is far from that extreme.

So this is primarily a normative question: What kind of society do we want? Do we want a more egalitarian society where two people of equal talent, drive and risk tolerance can achieve similar economic success? Or do we want a more hereditary society? That is the primary question.

Another question is the appropriate public policy with regards to income inequality. At the least we should do nothing. In fact, shouldn't all Americans agree with this statement (from Tax Law Professor Geier)?

"...the government should not be intervening through the tax system to make the gap between the very rich and everyone else actually greater than it otherwise is (in the absence of tax)."But, according to Professor Geier that is exactly what the current tax law does:

"The distribution of the tax burden worsens inequality because there is less income inequality before annual tax bills are paid than after they are paid."To be charitable to Mankiw: Maybe we now know why Mankiw was a champion of Bush's tax policy - he erroneously thought income inequality leads to faster growth.

UPDATE: Via Dr. DeLong: WSJ.com - As Rich-Poor Gap Widens in the U.S., Class Mobility Stalls EXCERPTS:

The promise that a child born in poverty isn't trapped there remains a staple of America's self-portrait....

Although Americans still think of their land as a place of exceptional opportunity... the evidence suggests otherwise....

'The U.S. and Britain appear to stand out as the least mobile societies among the rich countries studied,'

When the Bubble will Burst

by Calculated Risk on 6/07/2005 03:30:00 PM

In March 2003, physicists Didier Sornette (UCLA) and Wei-Xing Zhou (East China University of Science & Technology) correctly predicted that the UK housing bubble would "burst" in mid-2004. At that time they argued the US housing market was not yet a bubble.

This week the physicists released a new paper "Is There a Real-Estate Bubble in the US?". They now conclude that there is a bubble in the US, it is widespread, but that the turning point is still a year away:

"We conclude that the turning point of the bubble will probably occur around mid-2006."Their analysis looks for "positive feedbacks" that result in faster-than-exponential growth in prices. They divide states into three groups: 22 (including DC) existing bubble states (red), 8 new bubble states (purple) and 21 non-bubble states (green). The following map shows these states:

Click on map for larger image.

The paper includes several interesting graphs of price trajectories for bubble and non-bubble states. Maybe Dr. Polley is right about Peoria!

Monday, June 06, 2005

My New Reading List

by Calculated Risk on 6/06/2005 03:37:00 PM

From the Westchester County Business Journal: Real estate book for 'dummies' exceeds expectations

UPDATE: Added to photo, thanks to benwood!

Click on covers for larger image.