RSS Feed

RSS Feed by Calculated Risk on 1/23/2023 04:00:00 PM

Monday, January 23, 2023

MBA Survey: "Share of Mortgage Loans in Forbearance Remains Flat at 0.70% in December"

Note: This is as of December 31st.

From the MBA: Share of Mortgage Loans in Forbearance Remains Flat at 0.70% in December

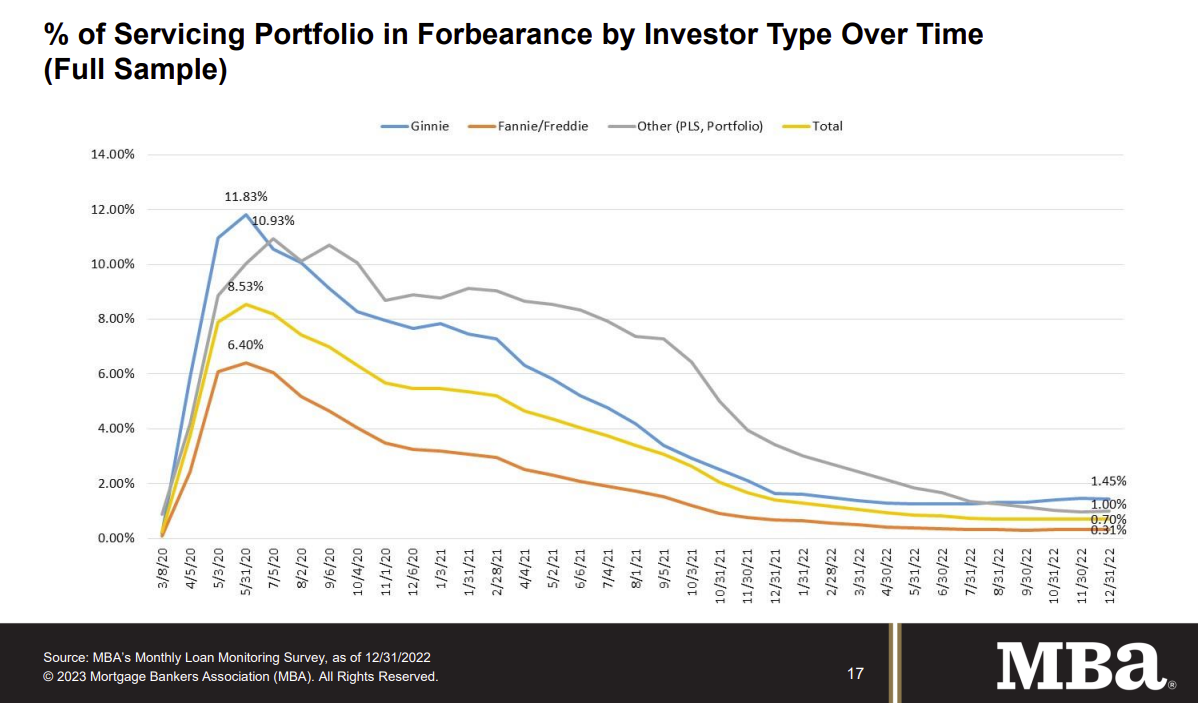

The Mortgage Bankers Association’s (MBA) monthly Loan Monitoring Survey revealed that the total number of loans now in forbearance remained flat relative to the prior month at 0.70% as of December 31, 2022. According to MBA’s estimate, 350,000 homeowners are in forbearance plans.

The share of Fannie Mae and Freddie Mac loans in forbearance decreased 1 basis point to 0.31%. Ginnie Mae loans in forbearance decreased 1 basis point to 1.45%, and the forbearance share for portfolio loans and private-label securities (PLS) increased 3 basis points to 1.00%.

“For three consecutive months, the forbearance rate has remained flat — an indicator that we may have reached a floor on further improvements,” said Marina Walsh, CMB, MBA’s Vice President of Industry Analysis. “New forbearance requests and re-entries continue to trickle in at about the same pace as forbearance exits. The overall performance of servicing portfolios was also flat compared to the previous month, but there was some deterioration in the performance of Ginnie Mae loans.”

Added Walsh, “Forbearance remains an option for struggling homeowners and its usage may continue, especially if unemployment increases as expected. MBA is forecasting for the unemployment rate to reach 5.2 percent in the second half of 2023, up from its current level of 3.5 percent.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the percent of portfolio in forbearance by investor type over time.

The share of forbearance plans had been decreasing, although the percent in forbearance was unchanged in November and December.

At the end of December, there were about 350,000 homeowners in forbearance plans.

LA Port Inbound Traffic Down 20% YoY in December

by Calculated Risk on 1/23/2023 01:18:00 PM

Notes: The expansion to the Panama Canal was completed in 2016 (As I noted several years ago), and some of the traffic that used the ports of Los Angeles and Long Beach is probably going through the canal. This might be impacting TEUs on the West Coast.

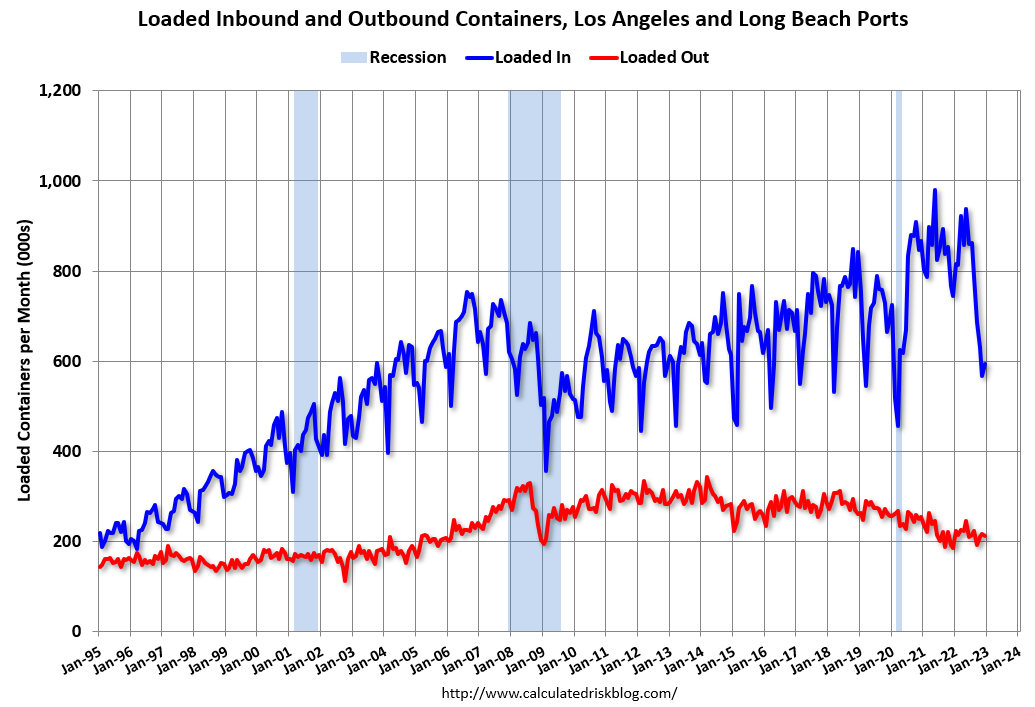

Container traffic gives us an idea about the volume of goods being exported and imported - and usually some hints about the trade report since LA area ports handle about 40% of the nation's container port traffic.

The following graphs are for inbound and outbound traffic at the ports of Los Angeles and Long Beach in TEUs (TEUs: 20-foot equivalent units or 20-foot-long cargo container).

To remove the strong seasonal component for inbound traffic, the first graph shows the rolling 12-month average.

Click on graph for larger image.

Click on graph for larger image.

On a rolling 12-month basis, inbound traffic decreased 1.6% in December compared to the rolling 12 months ending in November. Outbound traffic increased 1.1% compared to the rolling 12 months ending the previous month.

The 2nd graph is the monthly data (with a strong seasonal pattern for imports).

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.

Usually imports peak in the July to October period as retailers import goods for the Christmas holiday, and then decline sharply and bottom in February or March depending on the timing of the Chinese New Year.Imports were down 20% YoY in December, and exports were up 15% YoY.

It is possible that exports have bottomed after declining for several years (even prior to the pandemic).

1.51 million Total Housing Completions in 2022 including Manufactured Homes; Most Since 2007

by Calculated Risk on 1/23/2023 09:36:00 AM

Today, in the CalculatedRisk Real Estate Newsletter: 1.51 million Total Housing Completions in 2022 including Manufactured Homes; Most Since 2007

Excerpt:

Although total housing starts decreased 3.0% in 2022 compared to 2021, completions increased year-over-year. Construction delays impacted completions in 2022, and that left a record number of housing units under construction. However, there still were 1.507 million total completions and placements in 2021, the most since 2007.There is much more in the article. You can subscribe at https://calculatedrisk.substack.com/ Please subscribe!

Not counting Manufactured homes, there are 1.392 million completions in 2022, up from 1.341 million in 2021, and also the most since 2007.

This graph shows total housing completions and placements since 1968 through 2022. Note that the net addition to the housing stock is less because of demolitions and destruction of older housing units. The housing start report last week indicated 1,021.9 thousand single family completions in 2022, 10.0 thousand in 2-to-4 units, and 360.4 thousand in 5+ units.

Housing January 23rd Weekly Update: Inventory Decreased Slightly Week-over-week

by Calculated Risk on 1/23/2023 08:30:00 AM

Altos reports inventory was down 0.1% week-over-week. Usually inventory bottoms in February; in 2022, inventory bottomed in early March. It is possible that inventory is already near a bottom for the year!

Here are the same week inventory changes for the last five years:

2023: -0.6K

2022: -6.8K

2021: -8.2K

2020: +2.1K

2019: +10.3K

Click on graph for larger image.

Click on graph for larger image.This inventory graph is courtesy of Altos Research.

As of January 20th, inventory was at 472 thousand (7-day average), compared to 473 thousand the prior week.

The red line is for 2023. The black line is for 2019. Note that inventory is up from the previous two years (the record low was in 2022), but still well below normal levels.

Inventory was up 70.5% compared to the same week in 2022, and down 42.8% compared to the same week in 2019.

A key will be when inventory starts increasing in 2023 - so far inventory has essentially been flat for the first three weeks of 2023.

Mike Simonsen discusses this data regularly on Youtube.

Sunday, January 22, 2023

Sunday Night Futures

by Calculated Risk on 1/22/2023 06:43:00 PM

Weekend:

• Schedule for Week of January 22, 2023

Monday:

• No major economic releases are scheduled.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are down slightly (fair value).

Oil prices were up over the last week with WTI futures at $81.64 per barrel and Brent at $87.63 per barrel. A year ago, WTI was at $85, and Brent was at $90 - so WTI oil prices are DOWN 5% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.41 per gallon. A year ago, prices were at $3.30 per gallon, so gasoline prices are up $0.11 per gallon year-over-year.

The Normal Seasonal Pattern for Median House Prices

by Calculated Risk on 1/22/2023 09:24:00 AM

Earlier, in the CalculatedRisk Real Estate Newsletter on December existing home sales, NAR: Existing-Home Sales Decreased to 4.02 million SAAR in December, I mentioned that the median price was down more than normal seasonally.

Below is a table of the seasonal pattern over the last several years.

Seasonally prices typically peak in June (closed sales for contracts signed mostly in April and May).

And seasonally prices usually bottom the following January (contracts signed in November and December). I've included the decline from the peak for December for each year to compare to 2022.

| 2018 | 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|---|

| Peak Month | June | June | Oct | June | June |

| December | -7.0% | -3.8% | -0.7% | -2.2% | -11.3% |

| January | -8.9% | -6.7% | -1.2% | -3.4% | N/A |

In 2020, prices increased late into the year and only decline slightly seasonally (the start of the pandemic buying boom), and in 2021, median prices only declined about 3% from peak to bottom.

But the decline this year, 11.3% so far, is larger than in the pre-pandemic years. And we will probably see a further decline in January and maybe in February - putting median prices down year-over-year soon.

Saturday, January 21, 2023

Real Estate Newsletter Articles this Week: Median House Prices Down 11.3% from Peak in June 2022; Record Number of Housing Units Under Construction

by Calculated Risk on 1/21/2023 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

• NAR: Existing-Home Sales Decreased to 4.02 million SAAR in December Median Prices Down 11.3% from Peak in June 2022

• December Housing Starts: Record Number of Housing Units Under Construction

• 4th Look at Local Housing Markets in December California Home Sales down 44% YoY in December; Prices Down 2.8% YoY

• The Housing Bubble and Mortgage Debt as a Percent of GDP

• Homebuilder Price Cuts

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

You can subscribe at https://calculatedrisk.substack.com/

Most content is available for free (and no Ads), but please subscribe!

Schedule for Week of January 22, 2023

by Calculated Risk on 1/21/2023 08:11:00 AM

The key reports scheduled for this week are the advance estimate of Q4 GDP, December New Home sales and December Personal Income and Outlays.

For manufacturing, the Richmond and Kansas City Fed manufacturing surveys will be released.

No major economic releases are scheduled.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for January.

10:00 AM: State Employment and Unemployment (Monthly) for December 2022

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

During the day: The AIA's Architecture Billings Index for December (a leading indicator for commercial real estate).

8:30 AM: Gross Domestic Product, 4th quarter and Year 2022 (Advance estimate). The consensus is that real GDP increased 2.6% annualized in Q4.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 205 thousand initial claims, up from 190 thousand last week.

8:30 AM: Durable Goods Orders for December. The consensus is for a 2.6% increase in durable goods.

8:30 AM ET: Chicago Fed National Activity Index for December. This is a composite index of other data.

10:00 AM: New Home Sales for December from the Census Bureau.

10:00 AM: New Home Sales for December from the Census Bureau. This graph shows New Home Sales since 1963.

The dashed line is the sales rate for last month.

The consensus is for 614 thousand SAAR, down from 640 thousand in November.

11:00 AM: the Kansas City Fed manufacturing survey for January.

8:30 AM ET: Personal Income and Outlays for December. The consensus is for a 0.2% increase in personal income, and for a 0.1% decrease in personal spending. And for the Core PCE price index to increase 0.3%. PCE prices are expected to be up 5.0% YoY, and core PCE prices up 4.4% YoY.

10:00 AM: Pending Home Sales Index for December. The consensus is for a -1.0% decrease in the index.

10:00 AM: University of Michigan's Consumer sentiment index (Final for January). The consensus is for a reading of 64.6.

Friday, January 20, 2023

COVID Jan 20, 2023: Update on Cases, Hospitalizations and Deaths

by Calculated Risk on 1/20/2023 09:17:00 PM

On COVID (focus on hospitalizations and deaths). Data is now weekly.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| New Cases per Week2 | 332,212 | 436,776 | ≤35,0001 | |

| Hospitalized2 | 33,405 | 39,413 | ≤3,0001 | |

| Deaths per Week2 | 3,953 | 4,209 | ≤3501 | |

| 1my goals to stop weekly posts, 2Weekly for Cases, Currently Hospitalized, and Deaths 🚩 Increasing number weekly for Cases, Hospitalized, and Deaths ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported.

January was the worst month for the previous two years, and this has seen a much smaller increase in deaths.

Hotels: Occupancy Rate Down 5.5% Compared to Same Week in 2019

by Calculated Risk on 1/20/2023 04:16:00 PM

U.S. hotel performance rose from the previous week and showed mixed comparisons against 2019, according to STR‘s latest data through Jan. 14.The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

Jan. 8-14, 2023 (percentage change from comparable week in 2019*):

• Occupancy: 54.8% (-5.5%)

• Average daily rate (ADR): $144.81 (+15.7%)

• Revenue per available room (RevPAR): $79.38 (+9.3%)

*Due to the pandemic impact, STR is measuring recovery against comparable time periods from 2019. Year-over-year comparisons will once again become standard after the first quarter.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2023, black is 2020, blue is the median, and dashed light blue is for 2022. Dashed purple is 2019 (STR is comparing to a strong year for hotels).

The 4-week average of the occupancy rate is below the median rate for the previous 20 years (Blue), but this is the slow season - and some of the early year weakness might be related to the timing of the report.

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average of the occupancy rate will increase seasonally over the next few months.