RSS Feed

RSS Feed by Calculated Risk on 4/05/2021 08:28:00 AM

Monday, April 05, 2021

Seven High Frequency Indicators for the Economy

These indicators are mostly for travel and entertainment. It will interesting to watch these sectors recover as the vaccine is distributed.

IMPORTANT: Be safe now - if all goes well, we could all be vaccinated by the end of Q2 2021.

----- Airlines: Transportation Security Administration -----

The TSA is providing daily travel numbers.

Click on graph for larger image.

Click on graph for larger image.

This data shows the seven day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Blue) and 2021 (Red).

The dashed line is the percent of 2019 for the seven day average.

This data is as of April 4th.

The seven day average is down 37.7% from the same week in 2019 (62.3% of last year). (Dashed line)

There was a slow increase from the bottom, with ups and downs due to the holidays - and TSA data has picked up in 2021.

----- Restaurants: OpenTable -----

The second graph shows the 7 day average of the year-over-year change in diners as tabulated by OpenTable for the US and several selected cities.

----- Hotel Occupancy: STR -----

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

The red line is for 2021, black is 2020, blue is the median, and dashed light blue is for 2009 (the worst year since the Great Depression for hotels - before 2020).

Even when occupancy increases to 2009 levels, hotels will still be hurting.

This data is through March 27th. Hotel occupancy is currently down 16.7% compared to same week in 2019). Note: Occupancy was up year-over-year, since occupancy declined sharply at the onset of the pandemic. However, occupancy is still down significantly from normal levels.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

----- Gasoline Supplied: Energy Information Administration -----

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

Blue is for 2020. Red is for 2021.

As of March 26th, gasoline supplied was off about 2.6% (about 974.4% of the same week in 2019).

Gasoline supplied was up year-over-year, since at one point, gasoline supplied was off almost 50% YoY in 2020.

----- Transit: Apple Mobility -----

This graph is from Apple mobility. From Apple: "This data is generated by counting the number of requests made to Apple Maps for directions in select countries/regions, sub-regions, and cities." This is just a general guide - people that regularly commute probably don't ask for directions.

There is also some great data on mobility from the Dallas Fed Mobility and Engagement Index. However the index is set "relative to its weekday-specific average over January–February", and is not seasonally adjusted, so we can't tell if an increase in mobility is due to recovery or just the normal increase in the Spring and Summer.

This data is through April 3rd for the United States and several selected cities.

This data is through April 3rd for the United States and several selected cities.

The graph is the running 7 day average to remove the impact of weekends.

IMPORTANT: All data is relative to January 13, 2020. This data is NOT Seasonally Adjusted. People walk and drive more when the weather is nice, so I'm just using the transit data.

According to the Apple data directions requests, public transit in the 7 day average for the US is at 63% of the January 2020 level. It is at 59% in Chicago, and 58% in Houston (the Houston dip was a weather related decline) - and moving up recently.

----- New York City Subway Usage -----

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider. This is weekly data since 2015.

This graph is from Todd W Schneider. This is weekly data since 2015.

The TSA is providing daily travel numbers.

Click on graph for larger image.

Click on graph for larger image.This data shows the seven day average of daily total traveler throughput from the TSA for 2019 (Light Blue), 2020 (Blue) and 2021 (Red).

The dashed line is the percent of 2019 for the seven day average.

This data is as of April 4th.

The seven day average is down 37.7% from the same week in 2019 (62.3% of last year). (Dashed line)

There was a slow increase from the bottom, with ups and downs due to the holidays - and TSA data has picked up in 2021.

The second graph shows the 7 day average of the year-over-year change in diners as tabulated by OpenTable for the US and several selected cities.

IMPORTANT: OpenTable notes: "we’ve updated the data including downloadable dataset from January 1, 2021 onward to compare seated diners from 2021 to 2019, as opposed to year over year." Thanks!

Thanks to OpenTable for providing this restaurant data:

Thanks to OpenTable for providing this restaurant data:

This data is updated through April 3, 2021.

This data is "a sample of restaurants on the OpenTable network across all channels: online reservations, phone reservations, and walk-ins. For year-over-year comparisons by day, we compare to the same day of the week from the same week in the previous year."

Note that this data is for "only the restaurants that have chosen to reopen in a given market". Since some restaurants have not reopened, the actual year-over-year decline is worse than shown.

Dining picked up during the holidays, then slumped with the huge winter surge in cases. Dining is picking up again - and is above 2019 in Texas and Florida.

----- Movie Tickets: Box Office Mojo -----

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

Thanks to OpenTable for providing this restaurant data:

Thanks to OpenTable for providing this restaurant data:This data is updated through April 3, 2021.

This data is "a sample of restaurants on the OpenTable network across all channels: online reservations, phone reservations, and walk-ins. For year-over-year comparisons by day, we compare to the same day of the week from the same week in the previous year."

Note that this data is for "only the restaurants that have chosen to reopen in a given market". Since some restaurants have not reopened, the actual year-over-year decline is worse than shown.

Dining picked up during the holidays, then slumped with the huge winter surge in cases. Dining is picking up again - and is above 2019 in Texas and Florida.

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue).

This data shows domestic box office for each week and the median for the years 2016 through 2019 (dashed light blue). Blue is 2020 and Red is 2021.

The data is from BoxOfficeMojo through Apr 2nd.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $40 million last week, down about 78% from the median for the week.

Note that the data is usually noisy week-to-week and depends on when blockbusters are released.

Movie ticket sales were at $40 million last week, down about 78% from the median for the week.

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

This graph shows the seasonal pattern for the hotel occupancy rate using the four week average. The red line is for 2021, black is 2020, blue is the median, and dashed light blue is for 2009 (the worst year since the Great Depression for hotels - before 2020).

Even when occupancy increases to 2009 levels, hotels will still be hurting.

This data is through March 27th. Hotel occupancy is currently down 16.7% compared to same week in 2019). Note: Occupancy was up year-over-year, since occupancy declined sharply at the onset of the pandemic. However, occupancy is still down significantly from normal levels.

Notes: Y-axis doesn't start at zero to better show the seasonal change.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.

This graph, based on weekly data from the U.S. Energy Information Administration (EIA), shows gasoline supplied compared to the same week of 2019.Blue is for 2020. Red is for 2021.

As of March 26th, gasoline supplied was off about 2.6% (about 974.4% of the same week in 2019).

Gasoline supplied was up year-over-year, since at one point, gasoline supplied was off almost 50% YoY in 2020.

This graph is from Apple mobility. From Apple: "This data is generated by counting the number of requests made to Apple Maps for directions in select countries/regions, sub-regions, and cities." This is just a general guide - people that regularly commute probably don't ask for directions.

There is also some great data on mobility from the Dallas Fed Mobility and Engagement Index. However the index is set "relative to its weekday-specific average over January–February", and is not seasonally adjusted, so we can't tell if an increase in mobility is due to recovery or just the normal increase in the Spring and Summer.

This data is through April 3rd for the United States and several selected cities.

This data is through April 3rd for the United States and several selected cities.The graph is the running 7 day average to remove the impact of weekends.

IMPORTANT: All data is relative to January 13, 2020. This data is NOT Seasonally Adjusted. People walk and drive more when the weather is nice, so I'm just using the transit data.

According to the Apple data directions requests, public transit in the 7 day average for the US is at 63% of the January 2020 level. It is at 59% in Chicago, and 58% in Houston (the Houston dip was a weather related decline) - and moving up recently.

Here is some interesting data on New York subway usage (HT BR).

This graph is from Todd W Schneider. This is weekly data since 2015.

This graph is from Todd W Schneider. This is weekly data since 2015. Most weeks are between 30 and 35 million entries, and currently there close to 10 million subway turnstile entries per week.

This data is through Friday, April 2nd.

Schneider has graphs for each borough, and links to all the data sources.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

This data is through Friday, April 2nd.

Schneider has graphs for each borough, and links to all the data sources.

He notes: "Data updates weekly from the MTA’s public turnstile data, usually on Saturday mornings".

Sunday, April 04, 2021

Sunday Night Futures

by Calculated Risk on 4/04/2021 06:17:00 PM

Weekend:

• Schedule for Week of April 4, 2021

Monday:

• At 10:00 AM ET, the ISM Services Index for March.

• During the Day, NY Fed, SCE Housing Survey: Data update

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 futures are up 15 and DOW futures are up 150 (fair value).

Oil prices were up over the last week with WTI futures at $61.45 per barrel and Brent at $64.86 per barrel. A year ago, WTI was at $28, and Brent was at $24 - so WTI oil prices are UP sharply year-over-year (oil prices collapsed at the beginning of the pandemic).

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.86 per gallon. A year ago prices were at $1.87 per gallon, so gasoline prices are up $0.99 per gallon year-over-year.

April 4th COVID-19 Vaccinations, New Cases, Hospitalizations

by Calculated Risk on 4/04/2021 04:11:00 PM

Note: I've been posting this data daily for over a year. I'll stop once all three of these criteria are met:

1) 70% of the population over 18 has had at least one dose of vaccine,

2) new cases are under 5,000 per day, and

3) hospitalizations are below 3,000.

According to the CDC, 165.1 million doses have been administered. 23.2% of the population over 18 is fully vaccinated, and 40.2% of the population over 18 has had at least one dose (103.7 million people have had at least one dose).

And check out COVID Act Now to see how each state is doing.

Almost 2,500 US deaths were reported so far in April due to COVID.

Click on graph for larger image.

Click on graph for larger image.

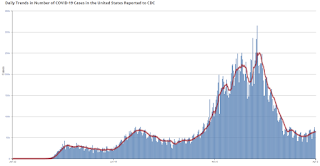

This graph shows the daily (columns) 7 day average (line) of positive tests reported.

Note: The ups and downs during the Winter surge were related to reporting delays due to the Thanksgiving and Christmas holidays.

This data is from the CDC.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) 7 day average (line) of positive tests reported.

Note: The ups and downs during the Winter surge were related to reporting delays due to the Thanksgiving and Christmas holidays.

This data is from the CDC.

The 7-day average is 64,001, up from 63,283 yesterday, and close to the summer surge peak of 67,337 on July 23, 2020.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.

The CDC cautions that due to reporting delays, the area in grey will probably increase.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 33,726, down slightly from 33,895 yesterday, but well above the post-summer surge low of 23,000.

Brief Discussion: The Impact of Rising Mortgage Rates on Home Sales and House Prices

by Calculated Risk on 4/04/2021 09:36:00 AM

CR Note: There is quite a bit of information (and charts) in this article by Matthew Graham at MortgageNewsDaily: Who's Lying About The Housing Market?. Here are a few excerpts on the impact of mortgage rates on home sales and house prices.

CR Note: There is much more in the article. As Graham notes, inventory is the key,Click on graph for larger image.

The inventory situation may mean that prices remain more resilient in the current housing cycle despite the recent surge in interest rates. Even then, past examples of rate spikes have only had moderate impacts on housing.

Using the same home sales data from above, let's highlight previous rate spikes so we can see the impact...

There was a big rate spike at the end of 2016 that had no discernible effect on prices. This is notable because that rate spike was fueled by economic optimism as opposed to 2013's rate spike which happened after the Fed said they would begin decreasing their rate-friendly bond buying program. 2018 was somewhat similar as the Fed was continuing to tighten monetary policy and raise short term interest rates.

A case could be made that the current rate spike shares some similarities with 2016. The path of 10yr Treasury yields (a benchmark for longer term rates like mortgages) has largely traced pandemic progress and economic recovery hopes. Yields (aka rates) began rising late last summer as vaccine trials showed promising results and economic data began to improve.

Bottom line, it is a rising rate environment until further notice. If we don't see a negative turn of events for the economy, rates will eventually run out of steam for other reasons. But that could take time, and the overall rate spike could rival the worst past examples by the time it fully runs its course.

Saturday, April 03, 2021

April 3rd COVID-19 Vaccinations, New Cases, Hospitalizations

by Calculated Risk on 4/03/2021 03:39:00 PM

Note: I've been posting this data daily for over a year. I'll stop once all three of these criteria are met:

1) 70% of the population over 18 has had at least one dose of vaccine,

2) new cases are under 5,000 per day, and

3) hospitalizations are below 3,000.

According to the CDC, 161.7 million doses have been administered. 23.1% of the population over 18 is fully vaccinated, and 40.1% of the population over 18 has had at least one dose (103.5 million people have had at least one dose).

And check out COVID Act Now to see how each state is doing.

Almost 2,000 US deaths were reported so far in April due to COVID.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

The 7-day average is 63,283, down slightly from 63.727 yesterday, and close to the summer surge peak of 67,337 on July 23, 2020.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.

The CDC cautions that due to reporting delays, the area in grey will probably increase.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 33,895, up from 33,698 yesterday, and well above the post-summer surge low of 23,000.

Schedule for Week of April 4, 2021

by Calculated Risk on 4/03/2021 08:11:00 AM

This will be a light week for economic data.

The key report this week is the Trade Deficit on Wednesday.

10:00 AM: the ISM Services Index for March.

During the Day: NY Fed, SCE Housing Survey: Data update

8:00 AM: Corelogic House Price index for February.

10:00 AM ET: Job Openings and Labor Turnover Survey for February from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for February from the BLS. This graph shows job openings (yellow line), hires (purple), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings increased in January to 6.917 million from 6.752 million in December.

The number of job openings (yellow) were down 3.3% year-over-year, and Quits were down 7.2% year-over-year.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Trade Balance report for February from the Census Bureau.

8:30 AM: Trade Balance report for February from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $70.3 billion. The U.S. trade deficit was at $68.2 billion in January.

2:00 PM: FOMC Minutes, Minutes Meeting of March 16-17, 2021

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for a decrease to 700 thousand from 719 thousand last week.

12:00 PM: Discussion, Fed Chair Jerome Powell, The Global Economy, At the International Monetary Fund Debate on the Global Economy

8:30 AM: The Producer Price Index for March from the BLS. The consensus is for a 0.5% increase in PPI, and a 0.2% increase in core PPI.

Friday, April 02, 2021

April 2nd COVID-19 Vaccinations, New Cases, Hospitalizations

by Calculated Risk on 4/02/2021 03:44:00 PM

Note: I've been posting this data daily for over a year. I'll stop once all three of these criteria are met:

1) 70% of the population over 18 has had at least one dose of vaccine,

2) new cases are under 5,000 per day, and

3) hospitalizations are below 3,000.

According to the CDC, 157.6 million doses have been administered. 22.4% of the population over 18 is fully vaccinated, and 39.2% of the population over 18 has had at least one dose (101.8 million people have had at least one dose).

And check out COVID Act Now to see how each state is doing.

Almost 1,000 US deaths were reported so far in April due to COVID.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

The 7-day average is 63,727, up from 62,828 yesterday, and close to the summer surge peak of 67,337 on July 23rd.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.

The CDC cautions that due to reporting delays, the area in grey will probably increase.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 33,698, up from 33,470 yesterday, and well above the post-summer surge low of 23,000.

March Vehicles Sales increased to 17.75 Million SAAR

by Calculated Risk on 4/02/2021 01:19:00 PM

Wards released their estimate of light vehicle sales for March yesterday. Wards estimates sales of 17.75 million SAAR in March 2021 (Seasonally Adjusted Annual Rate), up 13.3% from the February sales rate, and up 56% from March 2020 (sales collapsed in March 2020).

This was well above the consensus estimate of 16.5 million SAAR.

Click on graph for larger image.

Click on graph for larger image.

This graph shows light vehicle sales since 2006 from the BEA (blue) and the Wards' estimate for March (red).

The impact of COVID-19 was significant, and April was the worst month.

Since April, sales have increased.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

Note: dashed line is current estimated sales rate of 17.75 million SAAR.

Note: dashed line is current estimated sales rate of 17.75 million SAAR.

Click on graph for larger image.

Click on graph for larger image.This graph shows light vehicle sales since 2006 from the BEA (blue) and the Wards' estimate for March (red).

The impact of COVID-19 was significant, and April was the worst month.

Since April, sales have increased.

The second graph shows light vehicle sales since the BEA started keeping data in 1967.

Note: dashed line is current estimated sales rate of 17.75 million SAAR.

Note: dashed line is current estimated sales rate of 17.75 million SAAR.There was some bounce back from the weather related weakness in February, and apparently there was a surge in buying towards the end of March (probably related to the stimulus checks).

Black Knight: Number of Homeowners in COVID-19-Related Forbearance Plans Decreased

by Calculated Risk on 4/02/2021 12:09:00 PM

Note: Both Black Knight and the MBA (Mortgage Bankers Association) are putting out weekly estimates of mortgages in forbearance.

This data is as of March 30th.

From Black Knight: Servicers Continue to Work Through Forbearance Plans as U.S. Enters Fifth Consecutive Week of Improvement

The country saw yet another week of forbearance improvement this week, with active plans falling by 33,000 (-1.3%). This marks the fifth consecutive week of improvement and the longest such stretch since September 2020.The number of loans in forbearance has slowly declined over the last few months.

Weekly declines were seen across investor classes, with GSE plans down 15,000, FHA/VA plans down 12,000, and plan volumes among portfolio/PLS mortgages falling by 6,000 for the week.

This week’s improvement has pushed the number of active plans down by 172,000 (-6.3%) from last month, the largest such M/M improvement since November 2020. As of March 30, there are now 2.54 million active forbearance plans, representing 4.8% of all active mortgages.

Click on graph for larger image.

As anticipated, these improvements were driven by the large volume of forbearance plan reviews taking place in recent weeks. Entering March, 1.2 million plans were scheduled for review for removal/extension during the month; as of March 30, some 300,000 such scheduled expirations remain, with another 655,000 on tap for April. These numbers suggest we could see continued improvement in coming weeks as servicers continue to review plans with scheduled expirations for removal or extension.

We’ll have another forbearance update published here on this blog next Friday, April 9.

emphasis added

Comments on March Employment Report

by Calculated Risk on 4/02/2021 09:46:00 AM

The headline jobs number in the March employment report was well above expectations, and employment for the previous two months was revised up.

Leisure and hospitality gained 280 thousand. In March and April of 2020, leisure and hospitality lost 8.2 million jobs, and then gained about 60% of those jobs back. However, leisure and hospitality lost jobs in December and January due to the winter surge in COVID cases - before gaining jobs in February and March - and are now down 3.1 million jobs since February 2020.

Construction added 110 thousand jobs in March, and State and Local education added 126 thousand jobs. Manufacturing added 53 thousand jobs.

Earlier: March Employment Report: 916 Thousand Jobs, 6.0% Unemployment Rate

In March, the year-over-year employment change was minus 6.720 million jobs. This will turn positive in April due to the sharp jobs losses in April 2020.

Permanent Job Losers

Click on graph for larger image.

Click on graph for larger image.

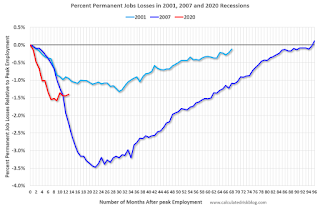

This graph shows permanent job losers as a percent of the pre-recession peak in employment through the March report. (ht Joe Weisenthal at Bloomberg).

Earlier: March Employment Report: 916 Thousand Jobs, 6.0% Unemployment Rate

In March, the year-over-year employment change was minus 6.720 million jobs. This will turn positive in April due to the sharp jobs losses in April 2020.

Permanent Job Losers

Click on graph for larger image.

Click on graph for larger image.This graph shows permanent job losers as a percent of the pre-recession peak in employment through the March report. (ht Joe Weisenthal at Bloomberg).

These jobs will likely be the hardest to recover.

This data is only available back to 1994, so there is only data for three recessions.

In March, the number of permanent job losers decreased slightly to 3.432 million from 3.497 million in February.

Prime (25 to 54 Years Old) Participation

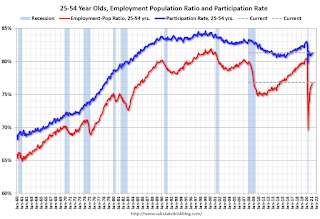

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

The prime working age will be key in the eventual recovery.

The 25 to 54 participation rate increased in March to 81.3% from 81.1% in February, and the 25 to 54 employment population ratio increased to 76.8% from 76.5% in February.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:

These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 10.7% from 11.1% in February. This is down from the record high in April 22.9% for this measure since 1994.

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more.

According to the BLS, there are 4.218 million workers who have been unemployed for more than 26 weeks and still want a job.

This does not include all the people that left the labor force. This will be a key measure to follow during the recovery.

Summary:

The headline monthly jobs number was well above expectations, and the previous two months were revised up 156,000 combined. The headline unemployment rate declined to 6.0%.

This data is only available back to 1994, so there is only data for three recessions.

In March, the number of permanent job losers decreased slightly to 3.432 million from 3.497 million in February.

Prime (25 to 54 Years Old) Participation

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the overall participation rate has declined due to cyclical (recession) and demographic (aging population, younger people staying in school) reasons, here is the employment-population ratio for the key working age group: 25 to 54 years old.The prime working age will be key in the eventual recovery.

The 25 to 54 participation rate increased in March to 81.3% from 81.1% in February, and the 25 to 54 employment population ratio increased to 76.8% from 76.5% in February.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:"The number of persons employed part time for economic reasons, at 5.8 million, changed little in March but is 1.4 million higher than in February 2020. These individuals, who would have preferred full-time employment, were working part time because their hours had been reduced or they were unable to find full-time jobs."The number of persons working part time for economic reasons decreased in March to 5.826 million from 6.088 million in February.

These workers are included in the alternate measure of labor underutilization (U-6) that decreased to 10.7% from 11.1% in February. This is down from the record high in April 22.9% for this measure since 1994.

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 4.218 million workers who have been unemployed for more than 26 weeks and still want a job.

This does not include all the people that left the labor force. This will be a key measure to follow during the recovery.

Summary:

The headline monthly jobs number was well above expectations, and the previous two months were revised up 156,000 combined. The headline unemployment rate declined to 6.0%.

This was a strong report, but there are still 8.4 million fewer jobs than in February 2020, and 3.4 million people have lost jobs permanently.