RSS Feed

RSS Feed by Calculated Risk on 5/05/2017 08:43:00 AM

Friday, May 05, 2017

April Employment Report: 211,000 Jobs, 4.4% Unemployment Rate

From the BLS:

Total nonfarm payroll employment increased by 211,000 in April, and the unemployment rate was little changed at 4.4 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in leisure and hospitality, health care and social assistance, financial activities, and mining.

...

The change in total nonfarm payroll employment for February was revised up from +219,000 to +232,000, and the change for March was revised down from +98,000 to +79,000. With these revisions, employment gains in February and March combined were 6,000 lower than previously reported.

...

In April, average hourly earnings for all employees on private nonfarm payrolls rose by 7 cents to $26.19. Over the year, average hourly earnings have risen by 65 cents, or 2.5 percent.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the monthly change in payroll jobs, ex-Census (meaning the impact of the decennial Census temporary hires and layoffs is removed - mostly in 2010 - to show the underlying payroll changes).

Total payrolls increased by 211 thousand in April (private payrolls increased 194 thousand).

Payrolls for February and March were revised down by a combined 6 thousand.

This graph shows the year-over-year change in total non-farm employment since 1968.

This graph shows the year-over-year change in total non-farm employment since 1968.In April, the year-over-year change was 2.24 million jobs. This is a decent year-over-year gain.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate was decreased in April to 62.9%. This is the percentage of the working age population in the labor force. A large portion of the recent decline in the participation rate is due to demographics.

The Labor Force Participation Rate was decreased in April to 62.9%. This is the percentage of the working age population in the labor force. A large portion of the recent decline in the participation rate is due to demographics. The Employment-Population ratio increased to 60.2% (black line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate decreased in April to 4.4%.

This was above expectations of 185,000 jobs, however the previous two months were revised down slightly.

I'll have much more later ...

Thursday, May 04, 2017

Friday: Jobs and Wages

by Calculated Risk on 5/04/2017 06:31:00 PM

Earlier:

My April Employment Preview: Mixed Signals

and Goldman: April Employment Preview

Friday:

• At 8:30 AM ET, Employment Report for April. The consensus is for an increase of 185,000 non-farm payroll jobs added in April, up from the 98,000 non-farm payroll jobs added in March. The consensus is for the unemployment rate to increase to 4.6%.

• At 3:00 PM, Consumer credit from the Federal Reserve. The consensus is for a $15.6 billion increase in credit.

Goldman: April Payrolls Preview

by Calculated Risk on 5/04/2017 03:15:00 PM

A few excerpts from a note by Goldman Sachs economist Spencer Hill:

We estimate nonfarm payrolls increased by 200k in April, somewhat above consensus of +190k. Our forecast reflects encouraging labor market fundamentals and a favorable swing in the weather, partially offset by slowing job growth in the retail sector.CR Note: My employment preview is here.

We estimate the unemployment rate remained stable at 4.5%, based on our expectation that household employment will hold on to its sharp year-to-date gains. Finally, we expect average hourly earnings to increase 0.3% month over month and 2.7% year over year, reflecting the interaction of firming wage growth with positive calendar effects.

April Employment Preview

by Calculated Risk on 5/04/2017 11:59:00 AM

On Friday at 8:30 AM ET, the BLS will release the employment report for April. The consensus, according to Bloomberg, is for an increase of 185,000 non-farm payroll jobs in April (with a range of estimates between 150,000 to 225,000), and for the unemployment rate to increase to 4.6%.

The BLS reported 98,000 jobs added in March.

Here is a summary of recent data:

• The ADP employment report showed an increase of 177,000 private sector payroll jobs in April. This was slightly above expectations of 170,000 private sector payroll jobs added. The ADP report hasn't been very useful in predicting the BLS report for any one month, but in general, this suggests employment growth close to expectations.

• The ISM manufacturing employment index decreased in April to 52.0%. A historical correlation between the ISM manufacturing employment index and the BLS employment report for manufacturing, suggests that private sector BLS manufacturing payroll decreased by about 10,000 in April. The ADP report indicated 11,000 manufacturing jobs added in April.

The ISM non-manufacturing employment index decreased in April to 51.4%. A historical correlation between the ISM non-manufacturing employment index and the BLS employment report for non-manufacturing, suggests that private sector BLS non-manufacturing payroll jobs increased about 110,000 in April.

Combined, the ISM indexes suggests employment gains of about 100,000. This suggests employment growth BELOW expectations.

• Initial weekly unemployment claims averaged 243,000 in April, down from 250,000 in March. For the BLS reference week (includes the 12th of the month), initial claims were at 243,000, down from 261,000 during the reference week in March.

The decrease during the reference week suggests fewer layoffs during the reference week in April than in March. This suggests a somewhat stronger employment report in April than in March.

• The final April University of Michigan consumer sentiment index increased slightly to 97.0 from the March reading of 96.9. Sentiment is frequently coincident with changes in the labor market, but there are other factors too like gasoline prices and politics.

• Conclusion: None of the indicators alone is very good at predicting the initial BLS employment report. The ADP report suggests a decent report, however the ISM surveys suggest weaker job growth. Weekly unemployment claims suggest slightly stronger job growth. I'll take the under for April.

Trade Deficit declines slightly to $43.7 Billion in March

by Calculated Risk on 5/04/2017 08:51:00 AM

From the Department of Commerce reported:

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis, through the Department of Commerce, announced today that the goods and services deficit was $43.7 billion in March, down $0.1 billion from $43.8 billion in February, revised. March exports were $191.0 billion, $1.7 billion less than February exports. March imports were $234.7 billion, $1.7 billion less than February imports.The first graph shows the monthly U.S. exports and imports in dollars through March 2017.

Click on graph for larger image.

Click on graph for larger image.Imports and exports decreased in March.

Exports are 15% above the pre-recession peak and up 9% compared to March 2016; imports are 1% above the pre-recession peak, and up 7% compared to March 2016.

In general, trade has been picking up, but has declined slightly the last two months.

The second graph shows the U.S. trade deficit, with and without petroleum.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.Oil imports averaged $46.26 in March, up from $45.25 in February, and up from $27.68 in March 2016. The petroleum deficit had been declining for years - and is the major reason the overall deficit has mostly moved sideways since early 2012. However, recently, the petroleum deficit has been increasing.

The trade deficit with China increased to $24.6 billion in March, from $20.9 billion in March 2016. Some of the increase this year was probably due to the timing of the Chinese New Year. In general the deficit with China has been declining.

Weekly Initial Unemployment Claims decrease to 238,000

by Calculated Risk on 5/04/2017 08:34:00 AM

The DOL reported:

In the week ending April 29, the advance figure for seasonally adjusted initial claims was 238,000, a decrease of 19,000 from the previous week's unrevised level of 257,000. The 4-week moving average was 243,000, an increase of 750 from the previous week's unrevised average of 242,250.The previous week was unrevised.

emphasis added

The following graph shows the 4-week moving average of weekly claims since 1971.

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 243,000.

This was lower than the consensus forecast.

The low level of claims suggests relatively few layoffs.

Wednesday, May 03, 2017

Thursday: Unemployment Claims, Trade Deficit

by Calculated Risk on 5/03/2017 06:40:00 PM

From Merrill Lynch on FOMC announcement:

The FOMC communicated today a lack of concern about the recent slowdown in economic data, describing it as "transitory" while "the fundamentals underpinning the continued growth of consumption remained solid". Not surprisingly then the statement was interpreted as hawkish relative to market expectations, as the Treasury curve bear flattened (10-year Treasury yield was 4bps higher while 30-year was flat) and the dollar appreciated.Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for 246 thousand initial claims, down from 257 thousand the previous week.

• Also at 8:30 AM, Trade Balance report for March from the Census Bureau. The consensus is for the U.S. trade deficit to be at $44.5 billion in March from $43.6 billion in February.

• At 10:00 AM, Manufacturers' Shipments, Inventories and Orders (Factory Orders) for March. The consensus is a 0.4% increase in orders.

FOMC Statement: No Change to Policy, Q1 Weakness "likely to be transitory"

by Calculated Risk on 5/03/2017 02:03:00 PM

As expected ...

FOMC Statement:

Information received since the Federal Open Market Committee met in March indicates that the labor market has continued to strengthen even as growth in economic activity slowed. Job gains were solid, on average, in recent months, and the unemployment rate declined. Household spending rose only modestly, but the fundamentals underpinning the continued growth of consumption remained solid. Business fixed investment firmed. Inflation measured on a 12-month basis recently has been running close to the Committee's 2 percent longer-run objective. Excluding energy and food, consumer prices declined in March and inflation continued to run somewhat below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee views the slowing in growth during the first quarter as likely to be transitory and continues to expect that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace, labor market conditions will strengthen somewhat further, and inflation will stabilize around 2 percent over the medium term. Near-term risks to the economic outlook appear roughly balanced. The Committee continues to closely monitor inflation indicators and global economic and financial developments.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 3/4 to 1 percent. The stance of monetary policy remains accommodative, thereby supporting some further strengthening in labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

The Committee is maintaining its existing policy of reinvesting principal payments from its holdings of agency debt and agency mortgage-backed securities in agency mortgage-backed securities and of rolling over maturing Treasury securities at auction, and it anticipates doing so until normalization of the level of the federal funds rate is well under way. This policy, by keeping the Committee's holdings of longer-term securities at sizable levels, should help maintain accommodative financial conditions. Voting for the FOMC monetary policy action were: Janet L. Yellen, Chair; William C. Dudley, Vice Chairman; Lael Brainard; Charles L. Evans; Stanley Fischer; Patrick Harker; Robert S. Kaplan; Neel Kashkari; and Jerome H. Powell.

emphasis added

ISM Non-Manufacturing Index increased to 57.5% in April

by Calculated Risk on 5/03/2017 10:04:00 AM

The April ISM Non-manufacturing index was at 57.5%, up from 55.2% in March. The employment index decreased in April to 51.4%, from 51.6%. Note: Above 50 indicates expansion, below 50 contraction.

From the Institute for Supply Management:April 2017 Non-Manufacturing ISM Report On Business®

Economic activity in the non-manufacturing sector grew in April for the 88th consecutive month, say the nation's purchasing and supply executives in the latest Non-Manufacturing ISM® Report On Business®.

The report was issued today by Anthony Nieves, CPSM, C.P.M., A.P.P., CFPM, Chair of the Institute for Supply Management® (ISM®) Non-Manufacturing Business Survey Committee: "The NMI® registered 57.5 percent, which is 2.3 percentage points higher than the March reading of 55.2 percent. This represents continued growth in the non-manufacturing sector at a faster rate. The Non-Manufacturing Business Activity Index increased to 62.4 percent, 3.5 percentage points higher than the March reading of 58.9 percent, reflecting growth for the 93rd consecutive month, at a faster rate in April. The New Orders Index registered 63.2 percent, 4.3 percentage points higher than the reading of 58.9 percent in March. The Employment Index decreased 0.2 percentage point in April to 51.4 percent from the March reading of 51.6 percent. The Prices Index increased 4.1 percentage points from the March reading of 53.5 percent to 57.6 percent, indicating prices increased for the 13th consecutive month, at a faster rate in April. According to the NMI®, 16 non-manufacturing industries reported growth. In April the non-manufacturing sector reflected strong growth after a slowing in the rate from the previous month. Respondents’ comments are mostly positive about business conditions and the overall economy."

emphasis added

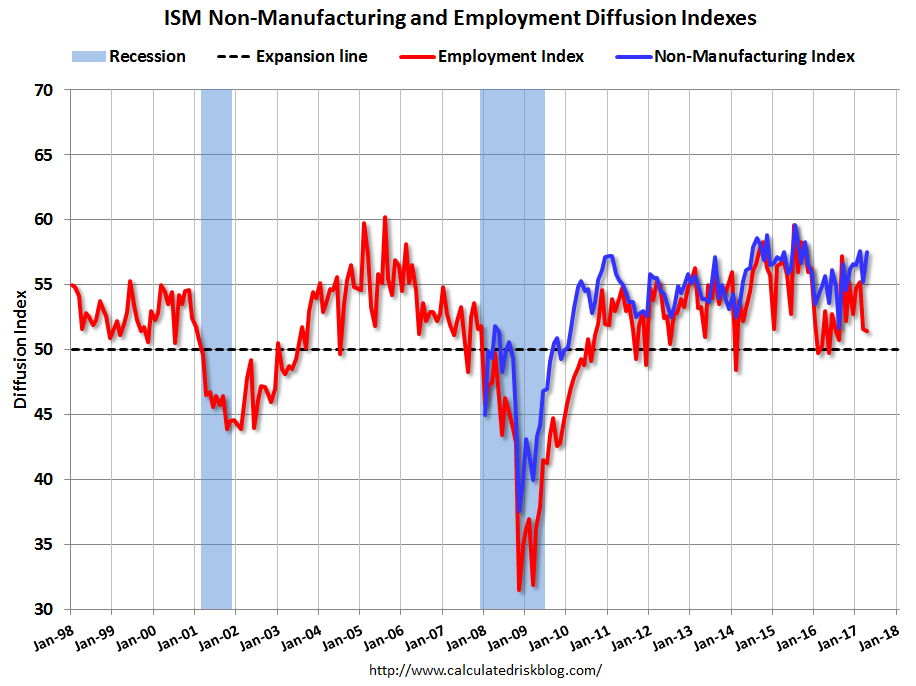

Click on graph for larger image.

Click on graph for larger image.This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

This suggests faster expansion in April than in March.

ADP: Private Employment increased 177,000 in April

by Calculated Risk on 5/03/2017 08:21:00 AM

Private sector employment increased by 177,000 jobs from March to April according to the April ADP National Employment Report®. ... The report, which is derived from ADP’s actual payroll data, measures the change in total nonfarm private employment each month on a seasonally-adjusted basis.This was above the consensus forecast for 170,000 private sector jobs added in the ADP report.

...

“In April we saw a moderate slowdown from the strong pace of hiring in the first quarter,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute. “Despite a dip in job creation, the growth is more than strong enough to accommodate the growing population as the labor market nears full employment. Looking across company sizes, midsized businesses showed persistent growth for the past six months.”

Mark Zandi, chief economist of Moody’s Analytics said, “Job growth slowed in April due to a pullback in construction and retail jobs. The softness in construction is continued payback from outsized growth during the mild winter. Brick-and-mortar retailers cut jobs in response to withering competition from online merchants.”

The BLS report for April will be released Friday, and the consensus is for 185,000 non-farm payroll jobs added in April.