RSS Feed

RSS Feed by Calculated Risk on 7/05/2010 01:21:00 PM

Monday, July 05, 2010

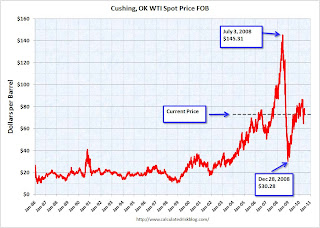

Update on Oil Prices

With the weakness in the US and European economies, and an apparent slowdown in China, it might be time to look at oil prices ... Click on graph for larger image in new window.

Click on graph for larger image in new window.

These are spot prices for Cushing WTI from the EIA (source).

Back in the Spring of 2008, we started seeing many signs of potential demand destruction - including fewer U.S miles driven, Asian countries reducing gasoline subsidies, and China stock piling oil for the Olympics. That was a pretty clear sign that oil prices would fall after China stopped stock piling oil.

So far miles driven have been increasing slowly (although the most recent data is for April, and there may be more weakness in June). And once again the Shanghai stock market is suggesting a slowdown in China. Not a clear sign like in 2008, but something to watch.

Europe: Austerity or "rigorous fiscal policies"?

by Calculated Risk on 7/05/2010 08:57:00 AM

A couple of quotes from the WSJ: Lagarde: Banks Will Pass Stress Tests

"There is no choice between austerity and stimulus," [Finance Minister Christine Lagarde] said at an economic conference in Aix-en-Provence. "Our policy is a subtle mix between growth-friendly spending cuts and letting play out the remainder of our stimulus package," she said.Paul Krugman disagrees: Plan XVII For Europe

...

"We are in a period when we have to manage budgets very cautiously. ... You may call that austerity if you want, I call this rigorous fiscal policies," [European Central Bank President Jean-Claude Trichet] told reporters on the sidelines of an economic conference in southern France.

"If you want sustainable growth, then you have to restore confidence and to do that you need to have balanced and sustainable fiscal policies in place," he added

Sunday, July 04, 2010

Happy July 4th

by Calculated Risk on 7/04/2010 11:02:00 PM

Two earlier posts:

The National Mall in D.C. July 4th, 2010. Best to all!

Investors buying foreclosures in Phoenix

by Calculated Risk on 7/04/2010 05:22:00 PM

Here is an article from the AP about investors buying foreclosures in the Phoenix area: Finding gold in them thar foreclosures (ht Ian).

I can add a little to this story: I know of an individual investor (through a close friend) in the Phoenix area who has bought almost 100 homes over the last 18 months. The investor has shared with me his portfolio. He has only bought single family homes, no condos. His average purchase price was under $35,000 and most of the homes are 3 br / 2 ba.

He is renting the homes, many by the room. Yeah, they sound like flophouses! The investor is starting to have a vacancy problem that he attributes to the new Arizona immigration law that takes effect on July 29th.

I reviewed the public records of some of the homes this investor bought - as an example he bought a 3 br / 2 ba 1,200 sq ft home for about $35,000 a couple of months ago - and that is about the average for the homes he has been buying. Very basic, dirt yards ... not the best area.

He paid in the low $20,000s for a home he bought last summer that sold for over $180,000 in 2006! That is almost 90% off the peak price (the house sold for $62,000 in 2004, so I'm guessing fraud in 2006 - and maybe in 2004 too).

Note: all numbers changed a little - the investor wants to remain anonymous.

Weekly Summary and a Look Ahead

by Calculated Risk on 7/04/2010 11:45:00 AM

This will be a light week for US economic data. The US stock markets will be closed on Monday to observe Independence Day.

Sometime this week, Reis will release the Q2 mall, office and apartment vacancy rates. In Q1, Reis reported the strip mall vacancy rate hit 10.8% (highest since 1991), the apartment vacancy rate was at a record 8% (large cities only), and the office vacancy rate rose to rose to 17.2% (highest since the early '90s).

On Tuesday, the June ISM non-manufacturing report will be released. Consensus is for a decrease to 55.0 from 55.4 in the service sector.

On Wednesday, the MBA will release the mortgage purchase applications index. This has been falling sharply after the expiration of the home buyer tax credit. Also on Wednesday, Minneapolis Fed President Narayan Kocherlakota will speak at the Université de Montréal at 3:30 PM ET (Society for Economic Dynamics).

On Thursday, the initial weekly unemployment claims will be released. Consensus is for a decline to 465K from 472K last week. Also on Thursday, the Fed will release Consumer Credit for May at 3 PM ET. Consumer credit has declined sharply since mid-2008, especially revolving debt (credit cards).

Also on Thursday, at 6 PM ET, Professor Robert Hall, the current Chairman of NBER, will speak at the Society for Economic Dynamics: “Reconsidering the Basic Tenets of Macroeconomics in the Light of the Past Two Years”. He might be asked about the possibility of a “double dip” recession.

On Friday the Census Bureau will release Wholesale Inventories for May, and the FDIC will probably get back to work ...

A couple of posts on the 2nd half:

And a summary of last week:

1) Total nonfarm payroll employment declined by 125,000 in June

2) Census 2010 hiring decreased 225,000 in June.

3) So non-farm payroll employment increased 100,000 in June ex-Census. Private-sector payroll employment increased by 83,000.

4) The unemployment rate declined down to 9.5 percent as the participation rate fell (workers leaving the workforce pushed down the unemployment rate).

5) Average hourly wages and average hours worked decreased.

Overall this was a weak report. Here are a few graphs ...

Percent Job Losses During Recessions, aligned at Bottom

Click on graph for larger image.

Click on graph for larger image.This graph shows the job losses from the start of the employment recession, in percentage terms - aligned at the bottom of the recession.

The dotted line shows the impact of Census hiring. In June, there were 339,000 temporary 2010 Census workers on the payroll. The number of Census workers will continue to decline - and the gap between the solid and dashed red lines will be mostly closed in three or four months.

Employment-Population Ratio

The Employment-Population ratio decreased to 58.5% in June from 58.7% in May. This had been increasing after plunging since the start of the recession, and the recovery in the Employment-Population ratio was considered a good sign - but the ratio has now decreased for two consecutive months.

This graph shows the employment-population ratio; this is the ratio of employed Americans to the adult population.

This graph shows the employment-population ratio; this is the ratio of employed Americans to the adult population.Note: the graph doesn't start at zero to better show the change.

Also the Labor Force Participation Rate decreased to 64.7% in June from 65.0% in May. This is the percentage of the working age population in the labor force. This decline is very disappointing, and the rate is well below the 66% to 67% rate that was normal over the last 20 years.

The reason the unemployment rate declined was because people left the workforce - and that is not good news. As the employment picture improves, people will return to the labor force, and that will put upward pressure on the unemployment rate.

Part Time for Economic Reasons

The number of workers only able to find part time jobs (or have had their hours cut for economic reasons) was at 8.63 million in June. This was a slight decline from May - and was a little bit of good news.

The number of workers only able to find part time jobs (or have had their hours cut for economic reasons) was at 8.63 million in June. This was a slight decline from May - and was a little bit of good news.The all time record of 9.24 million was set in October.

These workers are included in the alternate measure of labor underutilization (U-6) that was at 16.5% in June.

Unemployed over 26 Weeks

The blue line is the number of workers unemployed for 27 weeks or more. The red line is the same data as a percent of the civilian workforce.

The blue line is the number of workers unemployed for 27 weeks or more. The red line is the same data as a percent of the civilian workforce.According to the BLS, there are 6.751 million workers who have been unemployed for more than 26 weeks and still want a job. This is a record 4.39% of the civilian workforce. (note: records started in 1948). It does appear the increases are slowing ...

Based on an estimate from Autodata Corp, light vehicle sales were at a 11.08 million SAAR in June. That is up 14% from June 2009 (when sales were very low), and down 4.6% from the May sales rate.

Based on an estimate from Autodata Corp, light vehicle sales were at a 11.08 million SAAR in June. That is up 14% from June 2009 (when sales were very low), and down 4.6% from the May sales rate.This graph shows the historical light vehicle sales (seasonally adjusted annual rate) from the BEA (blue) and an estimate for June (red, light vehicle sales of 11.08 million SAAR from Autodata Corp).

This was below most forecasts of around 11.4 million SAAR.

S&P/Case-Shiller released the monthly Home Price Indices for April (actually a 3 month average).

This graph shows the nominal not seasonally adjusted Composite 10 and Composite 20 indices (the Composite 20 was started in January 2000).

This graph shows the nominal not seasonally adjusted Composite 10 and Composite 20 indices (the Composite 20 was started in January 2000).The Composite 10 index is off 29.7% from the peak, and up 0.3% in April (SA).

The Composite 20 index is off 29.0% from the peak, and up 0.4% in April (SA).

The next graph shows the price declines from the peak for each city included in S&P/Case-Shiller indices.

Prices increased (SA) in 17 of the 20 Case-Shiller cities in April (SA).

Prices increased (SA) in 17 of the 20 Case-Shiller cities in April (SA). Prices in Las Vegas are off 55.9% from the peak, and prices in Dallas only off 5.2% from the peak.

Case Shiller is reporting on the NSA data (18 cities up), and I'm using the SA data. As S&P noted, there probably was a small boost to prices from tax credit related buying, but prices will probably fall later this year.

From the BEA: Personal Income and Outlays, April 2010

The following graph shows real Personal Consumption Expenditures (PCE) through May (2005 dollars). Note that the y-axis doesn't start at zero to better show the change.

The quarterly change in PCE is based on the change from the average in one quarter, compared to the average of the preceding quarter.

The quarterly change in PCE is based on the change from the average in one quarter, compared to the average of the preceding quarter.Even with no growth in June, PCE growth in Q2 would be 2.5%. Even with the weak June data, it looks like my earlier estimate of 3% PCE growth in Q2 will be about right (maybe a little high).

Best wishes to all.