RSS Feed

RSS Feed by Calculated Risk on 7/15/2005 07:19:00 PM

Friday, July 15, 2005

June Trade Deficit Forecast: OIL

The May numbers are barely dry, and here we go for June, starting with oil. Using the same model (described here) the ERPP (Energy Related Petroleum Products) trade numbers for June are forecast to be:

Forecast: Total NSA ERRP Imports: $19.6 Billion

Total SA ERPP FORECAST:

Imports SA: $19.4 Billion (seasonal factor estimated at 0.9925 for June)

Exports SA: $2.3 Billion

Balance ERPP: $17.1 Billion

DETAIL ALERT: The following are the internal numbers (mostly for my notes) that will cause your eyes to glaze over!

IMPORTS: Energy Related Petroleum Products.

Barrels Crude: 328.0 million barrels.

Barrels Other ERPP: 90.0 million barrels.

DOE Price per barrel (Crude): $45.11

DOE Price per barrel (Other): $51.88

Preliminary - Total NSA ERRP Imports: $19.5 Billion

NOTE: The BLS reports petroleum import prices rose 7.6% in June from May. The above model used DOE prices. After reviewing the prior prices and comparing the DOE and BLS approaches, the DOE has been slightly more accurate. Last month I split the difference between the estimates (the DOE was slightly closer).

This month I think the BLS numbers are too high (the real time data is revised significantly every month). The BLS approach would predict P(crude) = $46.35 compared to the DOE P(crude) = $45.11. I'm not going to split the difference, since I think the BLS is too high. Instead I will modify the DOE price forecast slightly upwards to reflect the BLS data as follows:

BLS/DOE Price per barrel (Crude): $45.40

BLS/DOE Price per barrel (Other): $52.21

Forecast: Total NSA ERRP Imports: $19.6 Billion

Total SA ERPP FORECAST:

Imports SA: $19.4 Billion (seasonal factor estimated at 0.9925 for June)

Exports SA: $2.3 Billion

Balance ERPP: $17.1 Billion

NOTE: This compares to the actual ERPP balance of -$15.8 Billion in May, so Oil is estimated to add $1.3 Billion to the deficit in June. Gen'l Glut has pointed out that the big jump in oil imports will come in July.

Bernanke, Job Growth and Home Prices

by Calculated Risk on 7/15/2005 05:20:00 PM

Earlier I quoted Ben Bernanke, the new chairman of the White House's Council of Economic Advisers suggesting that the boom in house prices was related to job growth:

"... states exhibiting higher rates of job growth also tend to have experienced greater appreciation in house prices."Now MSNBC's Martin Wolk provides data to show that Bernanke misspoke: Job growth fails to explain soaring home prices (Hat Tip to pgl at Angry Bear)

See the chart "Jobs & Home Prices". The conclusion ... Bernanke is wrong: "Job growth fails to explain soaring home prices".

Housing: New Loan Guidance Ignored

by Calculated Risk on 7/15/2005 11:19:00 AM

The NY Times is reporting: A Hands-Off Policy on Mortgage Loans

For two months now, federal banking regulators have signaled their discomfort about the explosive rise in risky mortgage loans.The regulators think Banks are not in danger because they have shifted the risk to investors and borrowers:

First they issued new "guidance" to banks about home-equity loans, warning against letting homeowners borrow too much against their houses. Then they expressed worry about the surge in no-money-down mortgages, interest-only loans and "liar's loans" that require no proof of a borrower's income.

The impact so far? Almost nil.

"It's as easy to get these loans now as it was two months ago," said Michael Menatian, president of Sanborn Mortgage, a mortgage broker in West Hartford, Conn. "If anything, people are offering them even more than before."

The reason is that federal banking regulators, from the Federal Reserve to the Office of the Comptroller of the Currency, have been reluctant to back up their words with specific actions. For even as they urge caution, officials here are loath to stand in the way of new methods of extending credit.

The main issue for regulators is whether banks and other lenders are properly managing their own risk, and the lenders are looking good.A couple of comforting thoughts:

They have hedged their risks by bundling mortgages into securities that are then sold to investors around the world. And if interest rates go higher, they have shifted much of the risk onto consumers because a growing share of home buyers have taken on adjustable-rate mortgages. At the same time, they have built sturdier financial institutions through mergers and the breakdown of barriers to interstate banking.

Bert Ely, an independent banking analyst who was among the first to recognize the crisis at savings and loan institutions in the 1980's, said the banks are far sounder today. "It's a night-and-day difference," Mr. Ely said. "No comparison."

But consumers - and perhaps the broader economy - are taking on more risk.

"There is a lot of pressure on banks to build market share, and consumers are looking for a quick response," said Barbara J. Grunkemeyer, deputy comptroller for credit risk at the Office of the Comptroller of the Currency. "With respect to these new mortgage products, they are new and have taken off rapidly. We are still in the process of understanding the risk-management systems that surround them."

"If you are the comptroller of the currency or the Federal Reserve, you're looking out for the system of the world," Mr. Frank added. "You're making macroeconomic policy. It's much more fun than looking out for consumers."

Thursday, July 14, 2005

Housing Humor

by Calculated Risk on 7/14/2005 08:50:00 PM

"The joke now in Lee County [Florida] is when the cops pull you over they ask for your real estate license because not everyone has a driver's license."From this otherwise serious article: Housing boom fraught with disasters waiting to happen.

And a Las Vegas story: Valley Home Buying Fallout.

Dyan Harmell, a Pulte home buyer, is drowning in a sea of debt. Her living room table is covered with bills and she's not quite sure how to pay them.Hat tip to Ben Jones for Vegas story. As the Vegas article says: "The real estate boom that sent Las Vegas home prices skyrocketing may be over, but the hangover is only getting worse."

"There are bills everywhere. House payments and debt," Harmell told FOX5. She's a long way from those heady days of Las Vegas' real estate boom, when she says Pulte's sales staff pushed and pushed her to buy.

"They call you and say 'you are so lucky .. this just came across.. it's going to be worth 100k before it closes,'"said Dyan Harmell. "We came with the hopes of buying two houses. We left the first day owning four. Within the next week, owning 6 -- all the way up to 19."

But Harmell's story is not unique. Walk around Pulte's Solera neighborhood and it's a ghost town. It seems as if "For Sale" signs are everywhere.

Signs that many people who thought they'd make a killing in Las Vegas' real estate market are now trying to unload homes at deep discounts.

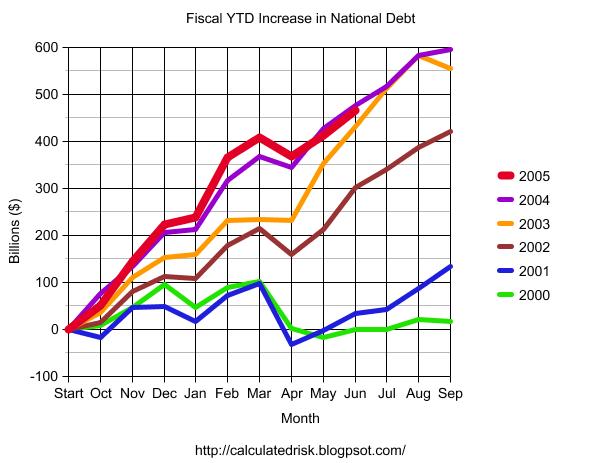

Deficit Improvement?

by Calculated Risk on 7/14/2005 04:37:00 PM

The following graph shows the fiscal year to date increase in the National Debt for each of the last six fiscal years. The "fiscal year" is the accounting period of the federal government. It begins on October 1st and ends on September 30th of the next calendar year. Each fiscal year is identified by the calendar year in which it ends - so fiscal year 2005 ends on September 30, 2005.

Click on graph for larger image.

The Year to Date increase in the National Debt is plotted for fiscal years 2000 through 2005. For 2005 (in RED) the data is plotted through June, 2005. The graph shows that contrary to the claims of the Bush Administration there has only been minor improvement in the overall deficit picture for 2005.

NOTE: There are many methods of looking at the annual budget deficit. The Bush Administration uses the "Enron Method" commonly called the "unified budget deficit". For a comparison of the unified budget deficit, the general fund deficit and the increase in the National Debt method see "Another Budget, Another Disaster".

Housing: The Bagholders

by Calculated Risk on 7/14/2005 11:47:00 AM

A couple weeks ago on Angry Bear, I quoted Econobrowser's Dr. Hamilton who asked: If there is a housing bubble,

"[W]hy are banks making loans to people who aren't going to be able to pay them back?"To try to answer Dr. Hamilton's question, I suggested we try to identify who would be left holding the bag and work backwards to motive.

Caroline Baum touches on the same topic in Enough About Loans. What About Lenders?

Forget the borrowers for a minute. Who's making these arguably risky loans? Why are lenders extending credit to seemingly bad credit risks?But this still doesn't identify the bagholders. Fannie Mae? Hedge Funds? Are investors underestimating the risk? Just more questions ...

One answer is that they aren't taking the risk. Rather, the risk is spread out, diluted. Lenders sell the loans, or the loans are securitized, in which case investors assume the risk.

As Federal Reserve Chairman Alan Greenspan reiterates, highly efficient capital markets in the U.S. diversify the risk, transferring it from those who don't want it to those who do.

Still, ``someone is taking on a lot of risk for someone to be able to take on less risk,'' [Michael Carliner, an economist at the National Association of Homebuilders in Washington] says.

Spreading the Risk

Then there's the question of whether risk is being priced correctly.

``There's been a dramatic explosion in lending to people with poorer credit-management history, and not a lot of history how certain loan products will perform,'' says Doug Duncan, chief economist at the Mortgage Bankers Association in Washington. ``We have no experience in 10-year interest-only mortgages.''

The risks apply to all parties in the transaction, Duncan says.

``For the borrower, did he understand how the loan would change?'' he says. For the servicer of the mortgage, ``did he understand how the loan would perform? Would it pre-pay faster, go delinquent? For the investor, did it achieve the yield expectations?''

OK, so the risk is spread out among various parties. Still, banks and thrifts do hold loans, especially ARMs, Duncan says. Won't they get stuck if the value of the house goes down, the borrower defaults and the lender can't recoup what was owed -- multiplied many times over?

Trade Deficit Projection: May Review

by Calculated Risk on 7/14/2005 01:24:00 AM

Two months ago I started to build a simple model to project the trade deficit. I didn't make as much progress as I had hoped, but the first two components (oil and China) have performed reasonably well for two months..

First, I projected the oil trade balance. And then I projected the trade deficit with China.

My model projected a deficit of $15.5 Billion Seasonally Adjusted in energy related petroleum product imports. The actual number was $15.8 Billion (see Exhibit 9). This is an error of just under 2%.

For the trade balance with China, my model projected a deficit of $15.5B NSA (SA is not available). The actual number (see Exhibit 14) was $15.7B or an error of 1.2%.

Here are each of the components and how the model performed:

| ITEM | Projection | Actual | Error |

| US Exports to China (NSA) | $3.4B | $3.3B | 3% |

| US Imports from China (NSA) | $18.9B | $19.05B | <1% |

| US Trade Deficit: China (NSA) | $15.5B | $15.75B | 1.6% |

| Oil: Imports SA | $17.4B | $18.1B | 3.9% |

| Oil: Exports SA | $1.9B | $2.3B | 17% |

| OIL Balance SA | $15.5B | $15.8B | 2% |

Some internal data:

| ITEM | Projection | Actual | Error |

| Oil: Contract Price BBL | $42.88 | $43.08 | <1% |

| Oil: BBLs Crude | 337.9M | 318.6M | 6% |

| Oil: Price Other BBL | $49.31 | $48.99 | <1% |

| Oil: BBLs Other | 85M | 99.7M | 15% |

| Oil: Oil Imports NSA | $18.7B | $18.6B | <1% |

It appears my SA factor for oil imports was somewhat off the mark. I'll have to take another look at that step. There is much more to do!

Wednesday, July 13, 2005

US Trade Deficit: $55.3 Billion for May

by Calculated Risk on 7/13/2005 08:33:00 AM

The U.S. Census Bureau and the U.S. Bureau of Economic Analysis released the monthly trade balance report today for May:

"... total May exports of $106.9 billion and imports of $162.2 billion resulted in a goods and services deficit of $55.3 billion, $1.6 billion less than the $56.9 billion in April, revised.Note: all numbers are seasonally adjusted.

May exports were $0.2 billion more than April exports of $106.7 billion.

May imports were $1.4 billion less than April imports of $163.6 billion."

Click on graph for larger image.

UPDATE: fixed a couple of errors.

May

The average contract price for oil dropped from a record $44.76 per barrel in April to $43.08 in May. The temporary drop in oil prices lowered the impact of oil on the trade deficit for May. However, the June trade deficit will be impacted by record high oil prices again.

I think the deficit will start to expand again starting in June.

Tuesday, July 12, 2005

May Trade Deficit Prediction

by Calculated Risk on 7/12/2005 06:39:00 PM

Once again, I've only modeled Oil and China, although I've added exports for Oil. Hopefully I will add more in the future. Here is a review of last month's predictions.

PROJECTIONS:

I: For petroleum, I project that NSA petroleum trade imports will be $18.7 Billion, down from $18.9 Billion in April. Including petroleum exports and adjusting for seasonal effects, the SA oil balance for May is projected at $15.5 Billion. This compares to $17.2 Billion for April.

II: For China, I project (see bottom) a NSA deficit of $15.5 Billion for May compared to $14.7 Billion in April. SA this is $16.1 Billion vs. $15.5 Billion for April.

III. OVERALL: I haven't developed a method for predicting the deficit for other countries, but based on Oil and China I think the deficit in May might improve slightly from April's deficit of $57 Billion. Oil will be about $1.7 Billion less in May (than April) and China approximately $0.6 Billion more.

My Guess (not enough work to call it a projection / estimate): $56.5 Billion Deficit.

NOTE: I expect June to be significantly worse than May.

CHINA: The following is the estimate for trade with China based on this methodology.

CHINA TRADE BALANCE: Table numbers in Billions $

NOT SEASONALLY ADJUSTED

| MONTH | NSA Balance | NSA Exports | NSA Imports |

| February | -$13.9 | $3.08 | $16.95 |

| March | -$12.9 | $3.3 | $16.21 |

| April | -$14.7 | $3.4 | $18.12 |

| May | -$15.5(est) | $3.4(est) | $18.9(est) |

SEASONALLY ADJUSTED (all estimates)

| MONTH | SA Balance | SA Exports | SA Imports |

| February | -$18.1 | $3.08 | $21.19 |

| March | -$15.1 | $3.3 | $18.42 |

| April | -$15.5 | $3.4 | $18.88 |

| May | -$16.1(est) | $3.4(est) | $19.5(est) |

Bernanke on Housing: Market Forces, not Speculation

by Calculated Risk on 7/12/2005 11:27:00 AM

Ben Bernanke gave his first speech this morning as the new chairman of the White House's Council of Economic Advisers. At the American Enterprise Institute, Bernanke commented on housing:

"While speculative behavior appears to be surfacing in some local markets, strong economic fundamentals are contributing importantly to the housing boom,"I disagree. Speculation, including excessive leverage, appears rampant in many markets.

Those fundamentals, Bernanke said, include low mortgage rates, rising employment and incomes, a growing population and a limited supply of homes or land in some areas.I disagree. Low mortgage rates are not a housing "fundamental", employment in California (one of the hottest real estate markets) is struggling, and population growth / limited supply of land was true 10 years ago too when housing was in a bust.

"For example, states exhibiting higher rates of job growth also tend to have experienced greater appreciation in house prices,"

"The administration will continue to monitor" developments in the housing market, Bernanke said. "However, our best defenses against potential problems in housing markets are vigilant lenders and banking regulators, together with perspective and good sense on the part of borrowers."And on the budget deficit:

"One consequence of the strong income growth we are enjoying is higher-than-expected levels of tax collections so far this year which, if maintained with spending controls, will reduce the government's budget deficit for this year well below its projected level,"This is laughable. There is a small improvement in the deficit this year, due to one time events, but next year will be worse.

As the Chairman of the CEA, it is understandable that Bernanke supports the Bush Administration's positions.