RSS Feed

RSS Feed by Calculated Risk on 2/16/2005 01:35:00 AM

Wednesday, February 16, 2005

The Impact of a RE Slowdown on Employment

Earlier I posted a bullish analysis on housing from the NAR and a cautionary report from the FDIC that expressed concerns about credit quality and excessive leverage for many homebuyers.

NAR President Al Mansell claims that "the population is growing faster than the supply of homes". However this is somewhat contradicted (in the short term) by the Housing Vacancies and Homeownership data from the Census Bureau. This data shows that an extra 800K rental units are available nationwide (above the normal percentage for the last 20 years). This increase has happened during the last 3 years. For other reasons, another 700K housing units are sitting vacant above the normal percentages. These are included in "bought but not occupied yet" and "other vacant" categories. Could this be speculation? Regardless of the reason, this suggests overcapacity in the housing market in the short term.

What about jobs?

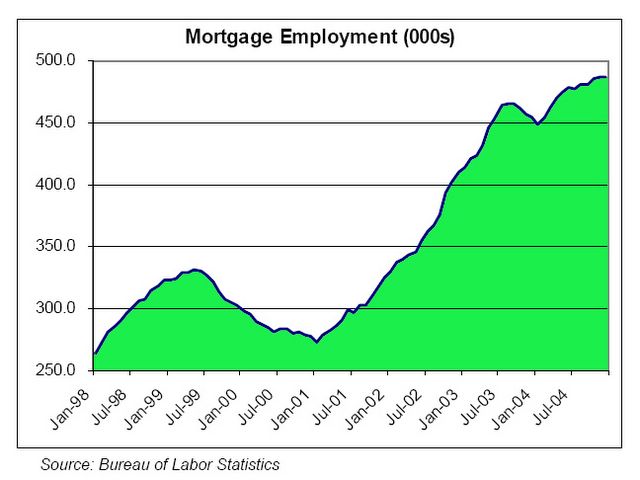

If we have a RE slowdown, it will probably have a significant impact on employment and aggregate income. From the following chart, we see that we have added 200K jobs in the mortgage industry alone in under 4 years. The mean salary (according to the BLS in 2001) was $45,380 for the mortgage industry. If we lost those jobs (returning to pre-2001 employment levels), we would lose $8 to $9 billion in aggregate annual income ... just from layoffs in the mortgage industry.

Thanks to ild and Elroy for the chart.

For RE agents, California alone has added 99,281 licensed RE agents since July 2000. Many of these agents only work part-time, but that is still a substantial loss of income if RE volumes drop 30 to 40% - like a typical RE slowdown.

And then there is the residential construction industry. Many of these jobs are reasonably high paying - and we have added over 300k construction jobs since 2000. And that figure doesn't include the impact of illegal immigrants working in the construction trade. When these immigrants lose their jobs, their lost income will also ripple through the economy.

We could add other potential lost jobs to this list: like service jobs in escrow, title, home inspection, and many other jobs on the periphery of RE. These are just the jobs directly impacted by a slowdown.

There are also the secondary effects (the vendors for the above businesses) and the tertiary impacts (restaurants, retailers, etc.) that suffer as aggregate income falls.

The bottomline: a significant RE slowdown would have a serious impact on employment and the economy.

Tuesday, February 15, 2005

Housing: Don't Worry, Be Happy

by Calculated Risk on 2/15/2005 05:53:00 PM

Yesterday I posted a cautionary report from the FDIC. Today, we have the National Association of Realtors with a bullish report on housing. The NAR reports that Record No. of Metros Show Double-Digit Home-Price Gains.

David Lereah, NAR's chief economist, says it's a simple matter of supply and demand. "We ended 2004 with a record low supply of homes on the market," he says. "With more buyers than sellers nationally, what we're seeing is a natural pressure on home prices as buyers compete to bid on available properties. Fortunately, the historically low cost of debt service on a home purchase means that we have a comfortable buffer in most of the country because the typical family can afford to buy a home well above the median price."

And Lereah went on to say that analysts looking for bad news will be disappointed.

"In the handful of areas with price declines, none had previously experienced rapid price growth," he says. "In fact, they were all lower-cost areas experiencing one or both of the conditions necessary for temporary price softness—local economic weakness, mainly in jobs, or a large supply of homes available in the local market."

And more bullish comments from NAR President Al Mansell:

"Although temporary price declines are always possible under the right conditions, people who were scared off by faulty predictions have missed out on the strongest housing market in U.S. history," he says. "Considering rents on comparable properties generally are higher than mortgage payments, and housing returns generally are multiples of a downpayment, a little perspective may help. The population is growing faster than the supply of homes, the cost of construction rarely declines and the long-term prospects are positive—one of the largest generations in U.S. history, who believe housing is a good investment, is just entering the years in which people typically buy their first home."

Don't Worry, Be Happy.

Monday, February 14, 2005

U.S. Home Prices: Does Bust Always Follow Boom?

by Calculated Risk on 2/14/2005 11:26:00 PM

The FDIC has released a new report titled "U.S. Home Prices: Does Bust Always Follow Boom?" Their analysis is based on the OFHEO House Price Index database.

Their conclusions:

1) Most booms did NOT lead to a bust.

2) Most booms ended with "stagnation in home prices".

"In these cases, nominal home prices rose by an average of 2 percent per year during the five years after the boom ended. The equivalent figure for real home prices was a modest 2 percent per year decline."

3) Busts followed booms when a local severe economic shock occurred.

"... severe economic shocks—often including a net outflow of population—appear to be a key factor in pushing nominal home prices sharply lower. Home price declines do not occur simply because home prices have boomed, and they do not occur independently of local economic conditions."

4) However, there are additional reasons for concern with the current situation:

a) Boom is almost Nationwide:

"Our count of 33 boom markets in 2003 is the highest witnessed at one time during the past 25 years—1988 ranks second, with 24 booms. Moreover, the 2003 boom markets account for roughly 40 percent of the nation's population base, contributing to the impression that this is a nationwide phenomenon."

b) Financing is in uncharted territory:

"A major financial development in the 1990s was the emergence and rapid growth of subprime mortgage lending. Subprime mortgage loan originations surged by a whopping 25 percent per year between 1994 and 2003, resulting in a nearly ten-fold increase in the volume of these loans in just nine years.12 Subprime mortgages currently account for just over 10 percent of all mortgage debt outstanding."

c) And more and more buyers are taking on high debt to equity ratio:

"Home buyers are also increasingly availing themselves of higher-leverage mortgage products. In 2003, loans exceeding 80 percent of the home purchase price accounted for 30 percent of all purchase mortgages underwritten. In a few cities, this share exceeded 50 percent.14 In addition, more borrowers are taking on second mortgages at closing. One method of doing so involves "piggyback" loans, which combine a first mortgage, usually for 80 percent of the value of the home, with a "piggyback" second mortgage amounting to 10 to 15 percent or more of the value of the home. The effect of this structure is to raise the total loan amount to a level very near the value of the home, which may make borrowers more likely to default in the event of a housing market downturn. An increased incidence of default and foreclosure could, in turn, contribute to downward pressure on home prices as distressed properties are liquidated by lenders."

I am not optimistic that we can avoid a bust ...

Do Foreign CBs distort the Treasury Yield?

by Calculated Risk on 2/14/2005 11:49:00 AM

Several economists have recently suggested that Foreign Central Bank purchases of treasuries have distorted bond yields by anywhere from 40 to 200 bps. As an example, from the Feb 3rd The Economist:

"By some estimates, Asian purchases of American bonds have reduced yields by between half and one percentage-point."

And from the Federal Reserve's Bernanke and Reinhart writing with Macroeconomic Advisers' Brian Sack "Monetary policy alternatives at the zero bound: an empirical assessment":

"The results ... indicate that both five-year and ten-year Treasury yields remained below the model’s predictions by an average of 50 to 100 basis points over this period. This suggests that some force not captured in the model was exerting downward pressure on yields over this period. But while the evidence is suggestive of effe[c]ts from MOF purchases, it is not conclusive."

And Roubini and Setser in "Will the Bretton Woods 2 Regime Unravel Soon? The Risk of Hard Landing in 2005-2006" reviewed recent estimates of the impact of Foreign CB purchases:

"Goldman Sachs (2004) has presented an analysis suggesting that central banks intervention is narrowing Treasury yields by only 40bps; Sack (2004) provides a similar estimate. Truman (2005) notes that sustained intervention from central banks is similar to a sustained reduction in the fiscal deficit: his ballpark estimate suggests a $300 billion in central bank intervention might have a 75 bp impact. Research from Federal Reserve suggests a 50 to 100 bps impact (see Bernanke, Reinhart and Sack (2004)); PIMCO’s Bill Gross puts it at closer to 100 bps, and Morgan Stanley’s Stephen Roach puts it at between 100 and 150 bps."

Roubini and Setser concluded that these estimates are too low:

"While estimating the effect of central banks intervention on US long rates is difficult, there is good reason to suspect that the impact of central bank purchases much larger than the 40bps static effect estimated in some studies. ... Consequently, the 40bp Goldman estimate seriously understates the effects of the Asian intervention on the market. Considering the size of recent central bank purchases, the indirect impact of central bank intervention on private demand for Treasuries, the interaction between central bank reserve accumulation and Treasury debt management policy and the effects of Asian reserve accumulation on inflation and growth (general equilibrium effects), we would bet the overall impact would be closer to 200bps." emphasis Added

Over the weekend, the IHT had an article (by Daniel Altman) titled: "U.S. debt: Watch out for the domino effect". Although the article didn't mention lowering of American bond yields by foreign CBs, it touched on the impacts of Foreign CBs diversifying away from dollar denominated assets.

With regards to foreign CBs distorting the treasury yield, I remain skeptical but intrigued. If Foreign CBs are depressing American bond yields, this has already boosted any RE bubble by lowering borrowing costs for homebuyers. Any unwinding of these positions could potentially lead to a slowdown in the US economy with rising interest rates. That would not be a good combination.

Friday, February 11, 2005

Consumer Confidence Plummets in February

by Calculated Risk on 2/11/2005 08:34:00 PM

The AP-Ipsos consumer confidence index sank to 79.1 in February, down sharply from 92.5 in January. February's showing was the worst since October 2003.

Consumer Confidence

"The AP-Ipsos confidence index is benchmarked to a 100 reading on January 2002, when Ipsos started the gauge.

A measure of consumers' attitudes about economic expectations over the next six months, including conditions in areas where people live or work and their own financial positions, showed a steep decline.

That "expectations" gauge fell to 58.6 in February, compared with 79.6 in January and 89.2 a year ago."

Rasmussen conducts a daily poll of consumer confidence. The Rasmussen Consumer Index dropped two points on Friday to 115.5. Surprisingly, thirty-five percent (35%) of Americans say the U. S. is still in a recession.

Thursday, February 10, 2005

Housing: Quotes of the Day

by Calculated Risk on 2/10/2005 04:51:00 PM

Here are a couple of quotes from this article:

"There is going to be a problem in the housing market, and there is going to be a recession."

James Davis, the chairman of the Bank of Alameda.

"If you are in a region where job growth is not a problem, then you really don't have anything to worry about as far as the price of your house going down," That seems unlikely in his area, he added, because "people who live in Marin are not the type of people who get laid off first."

Rob Bensch, a house and apartment investor from Novato.

Housing Update

by Calculated Risk on 2/10/2005 01:07:00 PM

Two recent updates in California show the housing market may be starting to slow. I believe housing (especially New Home Sales) will be the leading indicator of a global economic slowdown.

Morgan Stanley's Stephen Roach has been using the phrase "asset economy" to describe the current situation. If housing slows down, this could take out the main pillar of the asset economy.

Home prices dipped in the OC (Orange County, CA) last month:

"Market-watcher DataQuick said Thursday that the median sales price for all residences in January was $534,000. That's off December's record high of $551,000 but still up 18.7 percent from January 2004.

Total sales last month were 2,903, down 4.9 percent from a year ago. Especially hard-hit were builders, who sold just 197 newly constructed homes -- a 24 percent drop from a year ago. It was the slowest January for builders since 1993."

And in Northern California:

"... real estate market has lost much of its steam in terms of volume. Decreasing volume is 'normal' behavior for the Santa Clara County real estate market for the end of the year. It is the degree of the decrease that remains a concern. Volume went from 154% of the 10-year average to 132% in June. Then went from 132% to 114% from mid-November to mid-December; and finally from 114% to 98% starting January 12, 2005. SCC only experienced 44% of the offers seen during the peak summer. This is a lower percentage than any of the 10-years that we have data for."

Wednesday, February 09, 2005

What Does Price Indexing mean for Social Security Benefits?

by Calculated Risk on 2/09/2005 02:32:00 PM

A report from The Center for Retirement Research at Boston College analyzes the impact of the Bush Administration's proposed Price Indexing on Social Security. Their conclusion:

"The conclusion that emerges from this review of price indexing is that it creates a potentially unstable system. Price indexing does more than simply cut benefits below the amounts scheduled under current law, it cuts them more each year. Eventually benefits will become trivial relative to workers’ earnings. If the goal is to restore balance to the Social Security program by cutting benefits, an across-the-board cut of 20 percent for those under age 55 or an increase in the normal retirement age to 70 would achieve the same result over the next 75 years without putting the system on a downward trajectory."

Tuesday, February 08, 2005

The Economist on the Budget: Holding the line?

by Calculated Risk on 2/08/2005 04:15:00 PM

Add the Economist's take: Holding the line? to Macroblog's summary of budget commentary.

Excerpts:

"George Bush has submitted a budget that is tough on discretionary spending for this coming year. But Iraq and Afghanistan, as well as proposed changes to Social Security and the tax code, still leave black clouds on the fiscal horizon"

And more:

"But Mr Bush’s new-found fiscal conservatism is patchy. His current deficits are primarily the result of a collapse in tax revenues, down from 20.8% of GDP in 2000 to 16.8% this year, yet he intends to make his tax cuts permanent. Security spending is also largely exempt from his tight-fistedness. Next year, defence spending will grow by 4.8% in nominal terms, to $419 billion; homeland-security outlays will go up by 1.2%, to $29 billion. And the budget does not include likely “supplementals” for ongoing military operations in Iraq and Afghanistan. Congress has already approved one such supplemental, of $25 billion for fiscal 2005, and is preparing to consider another $80-billion request from Mr Bush.

Indeed, none of these numbers is safe from Congress. Budget hawks fear so-called “Washington Monument proposals”: proposals to cut or close emotive programmes or landmarks, which the public (and their legislators) will never allow."

And on the AMT:

"Other fiscal pain has also been put off, but cannot be avoided forever. One headache is the Alternative Minimum Tax (AMT)."

The major media is looking deeper than the Bush Administration inspired headlines of “Deep Spending Cuts” and “Sweeping Budget Cuts”. That is a start.

Saturday, February 05, 2005

A Worrisome Juxtaposition?

by Calculated Risk on 2/05/2005 07:16:00 PM

WaPo 2/5/2005: As SE Asian Farms Boom, Stage Set for a Pandemic

NYTimes 2/5/2005: Bush Budget Calls for Cuts in Health Services

"... Mr. Bush would cut spending for several programs that deal with epidemics, chronic diseases and obesity. His plan would also cut the budget of the Centers for Disease Control and Prevention by 9 percent ..."

Seems like bad timing to me.