RSS Feed

RSS Feed by Calculated Risk on 4/04/2014 01:29:00 PM

Friday, April 04, 2014

Construction and Government Payrolls

The following table shows the net payroll jobs added per year for construction and government jobs. Construction was the hardest hit sector during (and before) the recession, and construction employment is now up 532 thousand from the bottom.

Government employment is still falling (state and local employment has bottomed, but Federal employment is still declining). Combined there are about 2.3 million fewer construction and government jobs compared to before the recession started.

| Annual Change in Construction and Government Payroll jobs (000s) | ||

|---|---|---|

| Year | Construction Jobs | Government |

| 2002 | -85 | 233 |

| 2003 | 127 | -42 |

| 2004 | 290 | 147 |

| 2005 | 416 | 186 |

| 2006 | 152 | 209 |

| 2007 | -195 | 288 |

| 2008 | -789 | 180 |

| 2009 | -1047 | -74 |

| 2010 | -192 | -219 |

| 2011 | 144 | -317 |

| 2012 | 114 | -58 |

| 2013 | 156 | -34 |

| 20141 | 88 | -13 |

| 1through March 2014 | ||

This graph shows total construction employment as reported by the BLS (not just residential).

This graph shows total construction employment as reported by the BLS (not just residential).Since construction employment bottomed in January 2011, construction payrolls have increased by 532 thousand - but there are still 1.76 million fewer construction jobs now than at the peak in 2006.

Historically there is a lag between an increase in activity and more hiring - and it appears hiring should pickup in 2014.

Comments on Employment Report

by Calculated Risk on 4/04/2014 10:19:00 AM

First, a milestone: Private payroll employment increased 192 thousand in March and private employment is now 110 thousand above the previous peak (total employment is still 437 thousand below the peak in January 2008). Of course the labor force has continued to increase over the last 6+ years, and there are still millions of workers unemployed - so the economy still has a long way to go.

Important: Although this was a slow recovery compared to most previous recessions, this was actually a relatively fast recovery compared to recessions following a severe financial crisis. It is easy to complain about policy makers, but we have to recognize that some policies actually helped ease the pain for millions of workers. There is more work to do, but no sentient being would want to return to the policies of 2001 through 2006 that caused the crisis!

There will be another milestone this summer when total non-farm employment will be above the pre-recession high (the unprecedented large number of government layoffs have held back total employment).

Overall this was a decent employment report. Hopefully job growth will be averaging over 200,000 jobs per month soon. The economy added 533 thousand jobs in Q1 this year compared to 618 thousand in Q1 2013 - not far behind last year considering the severe winter this year. I still expect stronger employment growth in 2014 than in 2013 even with the relatively poor start to the year.

Earlier: March Employment Report: 192,000 Jobs, 6.7% Unemployment Rate

Employment-Population Ratio, 25 to 54 years old

Since the participation rate declined recently due to cyclical (recession) and demographic (aging population) reasons, an important graph is the employment-population ratio for the key working age group: 25 to 54 years old.

Since the participation rate declined recently due to cyclical (recession) and demographic (aging population) reasons, an important graph is the employment-population ratio for the key working age group: 25 to 54 years old.

In the earlier period the employment-population ratio for this group was trending up as women joined the labor force. The ratio has been mostly moving sideways since the early '90s, with ups and downs related to the business cycle.

The 25 to 54 participation rate was unchanged in March at 81.2%, and the 25 to 54 employment population ratio increased to 76.7%. As the recovery continues, I expect the participation rate for this group to increase.

Percent Job Losses During Recessions

This graph shows the job losses from the start of the employment recession, in percentage terms - this time aligned at maximum job losses. At the recent pace of improvement, it appears employment will be back to pre-recession levels mid-year (Of course this doesn't include population growth).

In the earlier post, the graph showed the job losses aligned at the start of the employment recession.

Part Time for Economic Reasons

From the BLS report:

From the BLS report:

The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) was little changed at 7.4 million in March. These individuals were working part time because their hours had been cut back or because they were unable to find full-time work.This suggests significantly slack in the labor market. These workers are included in the alternate measure of labor underutilization (U-6) that increased slightly to 12.7% in March from 12.6% in February.

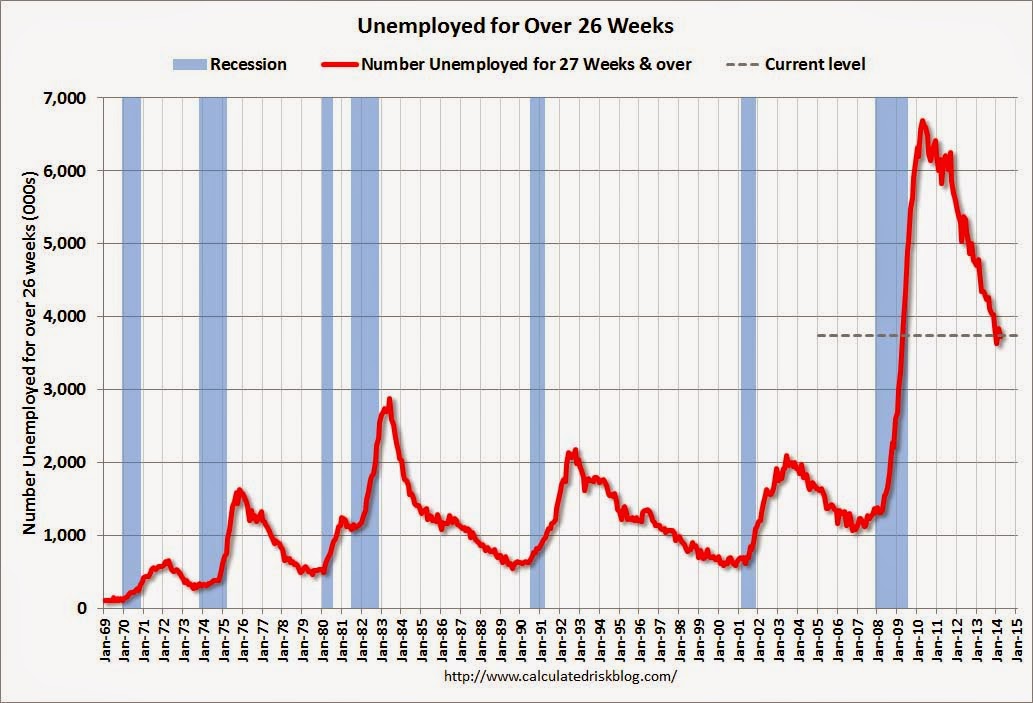

Unemployed over 26 Weeks

This graph shows the number of workers unemployed for 27 weeks or more.

This graph shows the number of workers unemployed for 27 weeks or more. According to the BLS, there are 3.739 million workers who have been unemployed for more than 26 weeks and still want a job. This was down from 3.849 in February. This is trending down, but is still very high.

Long term unemployment remains one of the key labor problems in the US.

State and Local Government

This graph shows total state and government payroll employment since January 2007. State and local governments lost jobs for four straight years. (Note: Scale doesn't start at zero to better show the change.)

This graph shows total state and government payroll employment since January 2007. State and local governments lost jobs for four straight years. (Note: Scale doesn't start at zero to better show the change.) In March 2014, state and local governments added 9,000 jobs.

It appears state and local employment employment has bottomed. Of course Federal government layoffs are ongoing.

All things considered, this was a solid report. Hopefully, now that the severe weather is behind us, the pace of employment growth will pick up.

March Employment Report: 192,000 Jobs, 6.7% Unemployment Rate

by Calculated Risk on 4/04/2014 08:30:00 AM

From the BLS:

Total nonfarm payroll employment rose by 192,000 in March, and the unemployment rate was unchanged at 6.7 percent, the U.S. Bureau of Labor Statistics reported today.

...

The change in total nonfarm payroll employment for January was revised from +129,000 to +144,000, and the change for February was revised from +175,000 to +197,000. With these revisions, employment gains in January and February were 37,000 higher than previously reported.

Click on graph for larger image.

Click on graph for larger image.The headline number was below expectations of 206,000 payroll jobs added.

The first graph shows the job losses from the start of the employment recession, in percentage terms, compared to previous post WWII recessions. The dotted line is ex-Census hiring.

This shows the depth of the recent employment recession - worse than any other post-war recession - and the relatively slow recovery due to the lingering effects of the housing bust and financial crisis.

Employment is 0.3% below the pre-recession peak (437 thousand fewer total jobs). Private employment is now above the pre-recession peak by 110 thousand and at a new all time high.

NOTE: The second graph is the change in payroll jobs ex-Census - meaning the impact of the decennial Census temporary hires and layoffs is removed to show the underlying payroll changes.

The third graph shows the employment population ratio and the participation rate.

The Labor Force Participation Rate was increased in March to 63.2%. This is the percentage of the working age population in the labor force.

The participation rate is well below the 66% to 67% rate that was normal over the last 20 years, although a significant portion of the recent decline is due to demographics.

The participation rate is well below the 66% to 67% rate that was normal over the last 20 years, although a significant portion of the recent decline is due to demographics.The Employment-Population ratio was increased in March at 58.9% (black line).

I'll post the 25 to 54 age group employment-population ratio graph later.

The fourth graph shows the unemployment rate.

The fourth graph shows the unemployment rate. The unemployment rate was unchanged in March at 6.7%.

This was a solid employment report, and including revisions, in line with expectations.

I'll have much more later ...

Thursday, April 03, 2014

Friday: Employment Report

by Calculated Risk on 4/03/2014 07:20:00 PM

From Goldman Sachs economist David Mericle:

"We forecast a 200,000 increase in nonfarm payrolls in March ... We expect that the unemployment rate declined to 6.6% ...Friday:

As growth accelerates later in 2014, we expect the trend rate of payrolls growth to rise to about 225,000 per month."

• At 8:30 AM ET the BLS will release the Employment Report for March. The consensus is for an increase of 206,000 non-farm payroll jobs in March, up from the 175,000 non-farm payroll jobs added in February.

The consensus is for the unemployment rate to decline to 6.6% in March.

This graph shows the percentage of payroll jobs lost during post WWII recessions through February.

This graph shows the percentage of payroll jobs lost during post WWII recessions through February.The economy has added 8.7 million private sector jobs since employment bottomed in February 2010 (8.0 million total jobs added including all the public sector layoffs).

There are still 129 thousand fewer private sector jobs now than when the recession started in 2007, and it is very likely that private employment now exceeds the pre-recession peak.

Employment Preview for March

by Calculated Risk on 4/03/2014 03:15:00 PM

Friday at 8:30 AM ET, the BLS will release the employment report for March. The consensus, according to Bloomberg, is for an increase of 206,000 non-farm payroll jobs in March (range of estimates between 175,000 and 275,000), and for the unemployment rate to decline to 6.6%.

Note: It is difficult to predict how much hiring will be a "bounce back" related to the severe weather in December, January and February. The economy only added an average of 129 thousand per month over the last three months, significantly below the trend of close to 200 thousand per month. We might see some upward revisions to prior months, and not all of the missing jobs will return in March, but there will probably be some hiring related to better weather.

Here is a summary of recent data:

• The ADP employment report showed an increase of 191,000 private sector payroll jobs in February. This was close to expectations of 190,000 private sector payroll jobs added. The ADP report hasn't been very useful in predicting the BLS report for any one month, but in general, this suggests employment growth close to expectations.

• The ISM manufacturing employment index declined in March to 51.1%. A historical correlation between the ISM manufacturing employment index and the BLS employment report for manufacturing, suggests that private sector BLS manufacturing payroll jobs decreased about 14,000 in March. The ADP report indicated a 5,000 increase for manufacturing jobs in March.

The ISM non-manufacturing employment index increased in March to 53.6% from 47.5% in February. A historical correlation between the ISM non-manufacturing index and the BLS employment report for non-manufacturing, suggests that private sector BLS reported payroll jobs for non-manufacturing increased 167,000 in March.

Taken together, these surveys suggest around 153,000 jobs added in March - below the consensus forecast.

• Initial weekly unemployment claims averaged close to 320,000 in March. This was down from an average of 338,000 in February. For the BLS reference week (includes the 12th of the month), initial claims were at 323,000; this was down from 330,000 during the reference week in February.

This suggests layoffs mostly in line with the consensus forecast.

• The final March Reuters / University of Michigan consumer sentiment index decreased to 80.0 from the February reading of 81.6. This is frequently coincident with changes in the labor market, but there are other factors too.

• The small business index from Intuit showed no change in small business employment in March.

• Conclusion: The ADP report was higher in March compared to the February report - and probably in line with most forecasts, the Intuit small business index showed no net hiring, and the ISM surveys suggest an increase but below the consensus. However there will probably be some bounce back from the below trend employment reports over the last three months (weather related).

There is always some randomness to the employment report - and the timing and survey methods are different than for some other reports - but my guess is the BLS report will be close to the consensus forecast of 206,000 nonfarm payrolls jobs added in March.