RSS Feed

RSS Feed by Calculated Risk on 11/10/2012 01:10:00 PM

Saturday, November 10, 2012

Schedule for Week of Nov 11th

Earlier:

• Summary for Week Ending Nov 9th

Several economic reports this week will be impacted by Hurricane Sandy including retail sales, weekly unemployment claims, and the regional NY and Philly Fed manufacturing surveys.

The key report for the week is retail sales for October. For manufacturing, the November NY Fed (Empire state) and Philly Fed surveys, and the October Industrial Production and Capacity Utilization report will all be released this week.

On prices, CPI for October will be released on Thursday.

Also Fed Chairman Ben Bernanke speaks Thursday on "Housing and Mortgage Markets".

4:00 AM ET: Eurozone Finance Ministers Meeting

8:30 AM: Producer Price Index for October. The consensus is for a 0.1% increase in producer prices (0.1% increase in core).

8:30 AM ET: Retail sales for October will be released. Note: Retail sales (especially auto sales) were impacted by Hurricane Sandy.

8:30 AM ET: Retail sales for October will be released. Note: Retail sales (especially auto sales) were impacted by Hurricane Sandy.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline). Retail sales are up 24.6% from the bottom, and now 9.0% above the pre-recession peak (not inflation adjusted)

The consensus is for retail sales to decrease 0.2% in October, and for retail sales ex-autos to increase 0.1%.

10:00 AM: Manufacturing and Trade: Inventories and Sales for September (Business inventories). The consensus is for 0.6% increase in inventories.

2:00 PM: FOMC Minutes for Meeting of October 23-24, 2012.

8:30 AM: Consumer Price Index for October. The consensus is for CPI to increase 0.1% in October and for core CPI to increase 0.1%.

8:30 AM: NY Fed Empire Manufacturing Survey for November. The consensus is for a reading of minus 9, down from minus 6.2 in October (below zero is contraction).

10:00 AM: Philly Fed Survey for November. The consensus is for a reading of minus 1.0, down from 5.7 last month (above zero indicates expansion).

1:20 PM: Speech, Fed Chairman Ben Bernanke, Housing and Mortgage Markets, At the HOPE Global Financial Dignity Summit, Atlanta, Georgia

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for October.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for October.This shows industrial production since 1967.

The consensus is for no change in Industrial Production in October, and for Capacity Utilization to decrease to 78.2%.

Summary for Week Ending Nov 9th

by Calculated Risk on 11/10/2012 08:05:00 AM

The big event this week was the presidential election. For economic data, this was a pretty light week.

The key report was the trade deficit that showed exports increased more than imports in September, and the trade deficit declined. Also Consumer sentiment has increased to pre-recession levels.

Other data was a little weak: The ISM service index declined in October, and job openings declined in September.

Next week will be busier.

Here is a summary of last week in graphs:

• Trade Deficit declined in September to $41.5 Billion

Click on graph for larger image.

Click on graph for larger image.

The first graph shows the monthly U.S. exports and imports in dollars through September 2012.

Both exports and imports increased in September. Exports are at a new high. The trade deficit was smaller than the consensus forecast of $45.4 billion.

Exports are 13% above the pre-recession peak and up 3.5% compared to September 2011; imports are 1% below the pre-recession peak, and up about 1.5% compared to September 2011.

The second graph shows the U.S. trade deficit, with and without petroleum, through September.

The second graph shows the U.S. trade deficit, with and without petroleum, through September.

The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

Oil averaged $98.88 in September, up from $94.36 per barrel in August. The trade deficit with China increased to $29.1 billion in September, up from $28.0 billion in September 2011. Most of the trade deficit is due to oil and China.

This suggests a small upward revision to Q3 GDP.

• ISM Non-Manufacturing Index decreases in October

The October ISM Non-manufacturing index was at 54.2%, down from 55.1% in September. The employment index increased in October to 54.9%, up from 51.1% in September. Note: Above 50 indicates expansion, below 50 contraction.

The October ISM Non-manufacturing index was at 54.2%, down from 55.1% in September. The employment index increased in October to 54.9%, up from 51.1% in September. Note: Above 50 indicates expansion, below 50 contraction.

This graph shows the ISM non-manufacturing index (started in January 2008) and the ISM non-manufacturing employment diffusion index.

This was below the consensus forecast of 54.9% and indicates slower expansion in October than in September. The internals were mixed with the employment index up, but new orders down.

• BLS: Job Openings "essentially unchanged" in September, Up year-over-year

This graph shows job openings (yellow line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

This graph shows job openings (yellow line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Notice that hires (dark blue) and total separations (red and light blue columns stacked) are pretty close each month. This is a measure of turnover. When the blue line is above the two stacked columns, the economy is adding net jobs - when it is below the columns, the economy is losing jobs.

Jobs openings decreased in September to 3.561 million, down slightly from 3.661 million in August. The number of job openings (yellow) has generally been trending up, and openings are only up about 2% year-over-year compared to September 2011.

Quits decreased in September, and quits are down slightly year-over-year. These are voluntary separations. (see light blue columns at bottom of graph for trend for "quits").

• Weekly Initial Unemployment Claims decline to 355,000

The DOL reported: "In the week ending November 3, the advance figure for seasonally adjusted initial claims was 355,000, a decrease of 8,000 from the previous week's unrevised figure of 363,000. The 4-week moving average was 370,500, an increase of 3,250 from the previous week's unrevised average of 367,250."

The DOL reported: "In the week ending November 3, the advance figure for seasonally adjusted initial claims was 355,000, a decrease of 8,000 from the previous week's unrevised figure of 363,000. The 4-week moving average was 370,500, an increase of 3,250 from the previous week's unrevised average of 367,250."The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 370,500. This is about 7,000 above the cycle low for the 4-week average of 363,000 in March.

Mostly moving sideways this year, but near the cycle bottom.

SPECIAL NOTE: Due to Hurricane Sandy, we will probably see an increase in initial unemployment claims over the next few weeks. The decline this week was probably because some people in a few states - like New York and New Jersey - were not able to file claims immediately.

• Fannie, Freddie, FHA REO inventory declined in Q3

This graph shows the REO inventory for Fannie, Freddie and the FHA (FHA for August). This was the seventh straight quarterly decline in the "F's" REO inventory, and total "F" REO was down 12% from a year ago.

This graph shows the REO inventory for Fannie, Freddie and the FHA (FHA for August). This was the seventh straight quarterly decline in the "F's" REO inventory, and total "F" REO was down 12% from a year ago. This is only a portion of the total REO. There is also REO for private-label MBS, FDIC-insured institutions, VA and more. REO has been declining for those categories too.

The second graph shows the same data with Private Label Securities added.

From Tom Lawler:

From Tom Lawler: Here is a chart showing some history of SF REO holdings of Fannie, Freddie, FHA, and private-label securities (from Barclays Capital). Note that FHA has not yet released its report to the FHA commissioner for September (everything there may be focused on the FY 2012 Actuarial Review due out next week, which could be a doozy!), and the number for the end of Q3/2012 (38,187) is actually the August inventory number.

More from CR: When the FDIC's Q3 quarterly banking profile is released in a couple of weeks, I'm sure Tom will add an estimate for REO at FDIC-insured institutions. This is not all REO: In addition to the FDIC-insured institution REO, this excludes non-FHA government REO (VA, USDA, etc.), credit unions, finance companies, non-FDIC-insured banks and thrifts, and a few other categories.

• Preliminary November Consumer Sentiment increases to 84.9

The preliminary Reuters / University of Michigan consumer sentiment index for November increased to 84.9 from the October reading of 82.6. This was the highest level since July 2007 - before the recession started.

The preliminary Reuters / University of Michigan consumer sentiment index for November increased to 84.9 from the October reading of 82.6. This was the highest level since July 2007 - before the recession started.This was above the consensus forecast of 83.1. Overall sentiment is still somewhat weak - probably due to a combination of the high unemployment rate and the sluggish economy - but consumer sentiment has been improving recently.

However - remember - that sharp decline in sentiment in August 2011 was due to the threat of default and the debt ceiling debate. Hopefully we will not see that again early next year before the fiscal slope is resolved.

Friday, November 09, 2012

Las Vegas Real Estate: Sales increase slightly in October

by Calculated Risk on 11/09/2012 06:02:00 PM

This is a key distressed market to follow since Las Vegas has seen the largest price decline of any of the Case-Shiller composite 20 cities.

From the GLVAR: GLVAR reports increasing local home sales, as prices begin to level off heading into winter

GLVAR said the total number of local homes, condominiums and townhomes sold in October was 3,651. That’s up from 3,298 in September, but down from 3,881 total sales in October 2011.A few key points:

...

The total number of homes listed for sale on GLVAR’s Multiple Listing Service bounced back in October, with a total of 16,778 single-family homes listed for sale at the end of the month. That’s up from 16,775 homes listed for sale at the end September, but down 21.9 percent from one year ago. ...

The number of available homes listed for sale without any sort of pending or contingent offer also increased from the previous month. By the end of October, GLVAR reported 4,079 single-family homes listed without any sort of offer. That’s up 3.4 percent from 3,943 such homes listed in September, but still down 60.6 percent from one year ago.

...

Meanwhile, 44.7 percent of all existing local homes sold during October were short sales. That’s down slightly from a record 44.8 percent in September, but still up dramatically from 25.4 percent one year ago. Continuing a trend of declining foreclosure sales in recent months, bank-owned homes accounted for 11.6 percent of all existing home sales in October, down from 13.6 percent in September.

...

"The biggest thing I noticed in this month’s report is that the inventory of homes available for sale went up. We sold fewer homes in October than we listed,” GLVAR President Kolleen Kelley explained. “As inventory goes up, you’re not going to see prices go up as much. It’s supply and demand.”

• Inventory increased slightly in September, and inventory is down 21.9% from October 2011. However, for single family homes without contingent offers, inventory is still down sharply from a year ago (down 60.6% year-over-year).

• Short sales are almost four times foreclosures now. The GLVAR reported 44.7% of sales were short sales, and only 11.6% foreclosures. We've seen a shift from foreclosures to short sales in most areas (not just in areas with new foreclosure laws).

• The percent distressed sales was extremely high at 56.3% in September (short sales and foreclosures), but down from 58.4% in September.

• There is a push to complete short sales, from the article:

Kelley said many homeowners have been rushing to short-sell their homes by the end of 2012, when the Mortgage Forgiveness Debt Relief Act is set to expire unless Congress acts to extend it. If Congress does not extend this law by Dec. 31, she said any amount of money a bank writes off in agreeing to sell a home as part of a short sale will become taxable when sellers file their income taxes.

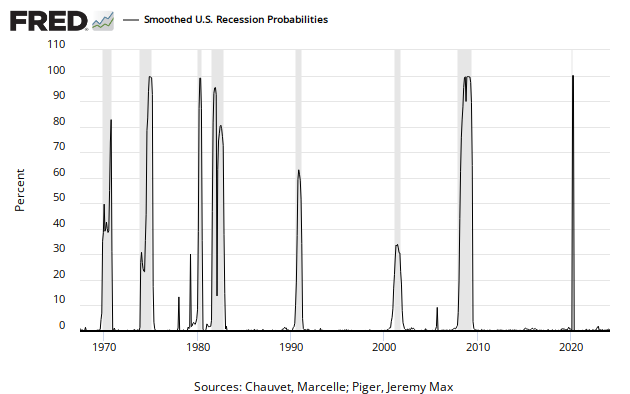

The Recession Probability Chart

by Calculated Risk on 11/09/2012 02:22:00 PM

One of the most frequent questions I receive via email is: "Is another recession starting?" There are quite a few people who have been calling a recession recently (ECRI has called several recessions since August 2011 or so). They still have time on their most recent calls, but their earlier calls were wrong.

Part of the problem in forecasting right now is the sluggish recovery has ups and downs, and each down looks like the start of a recession to some models. Another problem is that negative news sells ... and there is an entire industry that sells doom and gloom. And that industry has expanded significantly in recent years ...

There is a recession probability chart from the St Louis Fed making the rounds today. The chart shows that the odds of a recession have increased recently (ht Bruce).

Click on graph for larger image in new window.

Click on graph for larger image in new window.

Here is the chart from FRED at the St Louis Fed: "This recession probabilities series from University of Oregon economist Jeremy Piger is a monthly measure of the probability of recession in the United States obtained from a dynamic-factor Markov-switching model applied to 4 monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales."

However there are reasons this shouldn't be interpreted as indicating a new recession. Jeff Miller at a Dash of Insight does the heavy lifting: Debunking the 100% Recession Chart. Jeff actually read the underlying papers - and contacted the authors. Please read his post for more.

My view is the economy is not currently in a recession, and that economic growth will pickup in 2013, although there are downside risks from Europe and the potential for a policy mistake in the US (no agreement on the fiscal bluff). As I've noted before, I see two key reason for a pickup in the US: 1) I expect residential investment to increase next year (the key leading indicator for the economy), 2) I think the drag from state and local governments will subside.

Of course I could be wrong, but currently I'm not even on recession watch!

A few thoughts on Fiscal Agreement

by Calculated Risk on 11/09/2012 12:33:00 PM

A personal note: I'd like to thank Governor Romney for his personal sacrifice. I believe he is a decent man, and I think everyone should appreciate the sacrifice all candidates made in running for office (I'd never do it, even at the local level). I also think President Obama is a decent man, and I remain optimistic about the future.

From Reuters: Obama to Make Statement on Economy Friday

The president is likely to discuss looming tax increases and government spending cuts — the so-called fiscal cliff — that would go into effect early next year unless Congress acts to prevent them. He is due to make the statement from the East Room of the White House at 1:05 p.m.As I've noted before, there is no "cliff" and January 1st is not a drop dead date. Note: In the comments, Jackdawracy suggests "Fiscal Hillock" and energyecon suggests "fiscal bluff".

There are a few things that appear certain (but you never know with policy):

1) The top marginal tax rate will increase from 35% to 39.6%. The details still need to be worked out (at what income the highest bracket will start, and what happens with dividends and capital gains). The it is pretty clear the top tax rate will increase.

2) The payroll tax cut is probably going away. This was the 2% payroll tax reduction that workers received in 2010 and 2011. For a family with a $50,000 per year income, this is a tax increase of about $20 per week.

3) The Alternative Minimum Tax (AMT) relief will probably be extended (it is every year).

4) Given that the top marginal tax rate will increase - and that certain politicians can't vote for any bill with a tax increase - the agreement will probably be voted on in January after the Bush tax cuts expire.

I doubt we will see the current scheduled defense spending cuts (aka "sequestration"), but there will probably be some defense cuts.

Probably the most controversial issue, and least economically important (minimal drag on economy) is raising the top marginally tax rate. High income earners have a propensity to save, and raising their marginal rate a few percentage points will not have much impact on the economy - but it will significantly reduce the deficit.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the top marginal tax rate since 1920. There are many details missing (like the level of the top tax bracket). The current proposal is to raise the top tax bracket back to 39.6% from 35% - the same level as in the '90s.

Back in 1993, many analysts (like Larry Kudlow) argued raising the tax rate from 31% to 39.6% would take the economy into a deep recession or even depression. They were wrong. The other parts of the "fiscal cliff" are more important for the economy in the short run than the top tax rate.

One of the arguments against raising the top tax rate is that it will be a disincentive to start new companies. Wrong again. Note the top marginal tax rate in the 1970s - it was 70%. That was when Bill Gates started Microsoft, Steve Jobs started Apple and ... many others (Thomas Peterffy, who founded Interactive Brokers and ran many political ads recently started his company in 1977 with a 70% top tax rate). I've met with many entrepreneurs over the years, and none of them even mentioned the top personal tax rate - they were too focused on their company, products and market.

Hopefully this fiscal issue will be resolved without much disruption, and my guess is some sort of compromise will be reached early in 2013.

{kind=link}