RSS Feed

RSS Feed by Calculated Risk on 7/01/2010 09:56:00 PM

Thursday, July 01, 2010

Employment Report: Which payroll number to use?

Reading some of the employment preview articles tonight, I can see there will be some confusion just like last month. In May there were three payroll numbers commonly reported:

This created some confusion because I reported the underlying trend as +20,000 ex-Census, and many other reports used the private sector hiring of +41,000.

All three numbers have meaning, but the number consistent with previous reports (after removing temporary Census workers) was +20,000.

Tomorrow some sites will report private sector payroll jobs only - and that is not the correct method to remove the temporary Census workers and is inconsistent with previous reports (unless they were reporting private sector jobs only). Government hiring counts, especially since state and local governments might be cutting back later this year.

I will use the headline number and adjust by the number of temporary Census hires (the number will be reported here).

Housing: Timing for reported increase in Months-of-Supply and Decrease in House Prices

by Calculated Risk on 7/01/2010 07:10:00 PM

Some housing statistics are released with a long lag. Here is an overview ...

Earlier today, the NAR reported that the NAR's Pending Home Sales Index (PHSI) declined to a record low 77.6 in May. Although there is some variability, the PHSI usually leads existing home sales by about 45 to 60 days, so this suggests existing home sales will decline sharply in July. Of course we already knew this since tax credit buyers had to close by June 30th before the closing extension.

Note: The closing date for the tax credit was extended until Sept 30th, but that will only boost sales in July a little. (See from Reuters: US Congress Backs Home Tax Credit Extension)

In January 2009, the Pending Home Sales Index fell to a then record low 80.4. Two months later, existing home sales in March 2009 were at a 4.61 million rate. We can use that to estimate sales and months of supply in July.

If we assume sales fall a little little lower level in July 2010 than in March 2009 (because of the new record low PHSI), to say a 4.5 million sales rate, and that inventory stays about the same as in May 2010, say 3.9 million units for sale, the months-of-supply in July will be:

3.9 million units of inventory divided by 4.5 million existing sales (SAAR) times 12 months = 10.4 months of supply.

Maybe sales will be a little higher, or inventory a little lower, but the months-of-supply should be close to double digits in July.

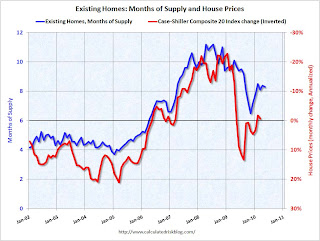

Earlier I posted this graph showing the relationship between months-of-supply and the change in house prices (change in house prices plotted inverted to show the relationship): Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows months of supply from NAR, and the annualized change in the Case-Shiller Composite 20 house price index (inverted).

Below 6 months of supply (blue line) house prices are typically rising (red line, inverted).

Above 6 months of supply house prices are usually falling (although there were many programs to support house prices over the last year).

Since the months-of-supply will probably be close to 10 months this summer, house prices will probably be falling again. I don't expect dramatic price declines later this year because prices are much closer to normal now, based on price-to-rent and price-to-income measures, than in 2007 and 2008. But I do expect falling house prices.

However it will take some time for this to show up in the house price indexes. The Case-Shiller index is a three month average and is released with a two month lag (the release this week was for a three month average ending in April).

The first Case-Shiller release with July prices will be released at the end of September - and that will include the months of May, June and July! And prices will be up in May and June.

The Corelogic data for July will also be released in September. There are other repeat sales measures (like from Radar Logic and Clear Capital), but in general it will be a long wait before reported house prices are falling.

U.S. Light Vehicle Sales 11.1 Million SAAR in June

by Calculated Risk on 7/01/2010 03:43:00 PM

Based on an estimate from Autodata Corp, light vehicle sales were at a 11.08 million SAAR in June. That is up 14% from June 2009 (when sales were very low), and down 4.6% from the May sales rate. Click on graph for larger image in new window.

Click on graph for larger image in new window.

This graph shows the historical light vehicle sales (seasonally adjusted annual rate) from the BEA (blue) and an estimate for June (red, light vehicle sales of 11.08 million SAAR from Autodata Corp).

The second graph shows light vehicle sales since the BEA started keeping data in 1967. Note: dashed line is current month sales rate.

Note: dashed line is current month sales rate.

Auto sales have recovered from the low levels of early 2009, but are below the lowest point of the '90/'91 recession (even with a larger number of registered drivers).

This was below most forecasts of around 11.4 million SAAR.

Hotel Occupancy Rate increases compared to same week in 2009

by Calculated Risk on 7/01/2010 02:40:00 PM

From HotelNewsNow.com: STR reports US results for week ending 26 June 2010

In year-over-year measurements, the industry's occupancy last week increased 6.8 percent to 69.7 percent. Average daily rate rose 1.1 percent to US$98.79. Revenue per available room rose 7.9 percent to US$68.88.The following graph shows the four week moving average for the occupancy rate by week for 2008, 2009 and 2010 (and a median for 2000 through 2007).

Click on graph for larger image in new window.

Click on graph for larger image in new window.Notes: the scale doesn't start at zero to better show the change.

On a 4-week basis, occupancy is up 5.4% compared to last year (the worst year since the Great Depression) and still 7.7% below normal. About half way back ...

Last year leisure travel held up better than business travel and leisure travel (summer) is the key for the next couple of months.

Data Source: Smith Travel Research, Courtesy of HotelNewsNow.com

Construction Spending declined in May

by Calculated Risk on 7/01/2010 12:25:00 PM

Overall construction spending declined in May, and private construction spending, both residential and non-residential, also decreased. From the Census Bureau: May 2010 Construction at $841.9 Billion Annual Rate

The U.S. Census Bureau of the Department of Commerce announced today that construction spending during May 2010 was estimated at a seasonally adjusted annual rate of $841.9 billion, 0.2 percent below the revised April estimate of $843.3 billion.

...

Spending on private construction was at a seasonally adjusted annual rate of $536.3 billion, 0.5 percent below the revised April estimate of $538.9 billion. Residential construction was at a seasonally adjusted annual rate of $260.8 billion in May, 0.4 percent below the revised April estimate of $261.7 billion. Nonresidential construction was at a seasonally adjusted annual rate of $275.6 billion in May, 0.6 percent below the revised April estimate of $277.2 billion.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows private residential and nonresidential construction spending since 1993. Note: nominal dollars, not inflation adjusted.

Private residential construction spending appears to have bottomed in early 2009, but has only increased gradually since then. Residential spending is now 61% below the peak of early 2006.

Private non-residential construction spending is now 33% below the peak of late 2008.

Residential spending will probably exceed non-residential later this year (or early 2011), but that will be mostly because of weakness in non-residential construction, as opposed to any significant increase in residential spending.