RSS Feed

RSS Feed by Calculated Risk on 4/27/2010 12:34:00 AM

Tuesday, April 27, 2010

Shanghai Composite index down 2.1%

Since I haven't posted a graph of the Shanghai index in some time ...

From MarketWatch: Shanghai Composite index down 2.1% at midday break

Mainland Chinese shares extend losses in the Tuesday morning session, with sharp retreats in commodity producers further pressuring markets already weighed by fears of policy tightening, especially in the property sector.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the Shanghai SSE Composite Index and the S&P 500 (in blue).

The SSE Composite Index is at 2,906.35 mid-day.

Monday, April 26, 2010

Home Tax Credit a Costly Failure

by Calculated Risk on 4/26/2010 09:40:00 PM

From David Kocieniewski at the NY Times: Home Tax Credit Called Successful, but Costly

Though the Treasury Department and the real estate industry have termed the program a success, helping 1.8 million people buy homes, many tax policy experts say it has been singularly cost-ineffective: most of the $12.6 billion in credits through end of February was collected by people who would have bought homes anyway or who in some cases were not even eligible.There is no question this program was very costly. And why is the Treasury confusing activity with accomplishment? Sure sales briefly surged, but were new households formed? How many new jobs were created?

“We were happy in our apartment, but $8,000 was just too much to pass up,” said [Mr. James Green, a student at Purdue University], 29, who shopped furiously with his wife for two months before signing a contract in March to buy a three-bedroom ranch.This is very optimistic - the ratio was probably 5-to-1 for the initial credit and even higher for the extension. But this shows two failures of the tax credit: 1) the high cost, and 2) it was just moving people from apartments to homes and didn't reduce the excess housing inventory (yes, rentals count as housing inventory too).

“We bid on a couple places that didn’t work out,” he said, “but we always made sure we had a backup plan because we didn’t want to miss the deadline for the credit. And when we finally agreed to a contract, it was this huge relief.”

For every home buyer like the Greens, real estate agents say there are at least three others who collected the credit even though they would have bought without it. That means for each new buyer who was truly lured into the market by the credit, the federal government paid more than $30,000.

“The tax credit helped to stanch the price declines, which had substantial benefit for the entire economy,” said Mark Zandi at Moody’s Economy.com.And this has been the policy - support asset prices by limiting the supply (all the foreclosure delays), and pushing demand (low mortgage rates and the tax credit). This has helped the banks significantly, and Zandi argues this has boosted confidence. Maybe ... but I'm not convinced that supporting house prices above the market clearing level to help the banks and boost consumer confidence makes sense. I think targeting jobs - and therefore household formation - would have been a far more cost effective program.

Yield on Greek Two-Year Bonds jumps to 13.5%

by Calculated Risk on 4/26/2010 05:49:00 PM

From the Financial Times: Greek bond markets plunge again

The yield on two-year Greek government bonds ... jumped 3 percentage points ... to close at 13.522 per cent.This is now higher than Venezuela at 11%.

This is the highest yield on short-dated government debt in the world ...

excerpt with permission

The yields jumped for some of the other PIIGS too (Portugal, Ireland, Italy, Greece and Spain). For Portugal the two-year yield increased more than 3/4 of a point to 3.98%.

New Offering: Bullet Proof Mortgage Backed Securities

by Calculated Risk on 4/26/2010 01:45:00 PM

There was an article on Bloomberg last week about "the first new-mortgage securities without government-backed guarantees in more than two years": Redwood, Citigroup End Two-Year Mortgage-Bond Drought (ht Brian)

My reaction was that these will be all low LTV mortgages with stellar credit ratings. I guessed the mortgages were essentially "bullet proof" ... Sure enough, here is the SEC filing: Sequoia Mortgage Trust 2010-H1 (ht Ramsey Su)

The details of the mortgages and the borrowers start on page 16. This is for 255 mortgages with an aggregate principal balance of $238 million. The weighted FICO score is 768, and the average Loan-to-Value is 56%.

Most are just refis of existing mortgage on owner occupied properties. There are 52 purchase mortgage with an average of just over 30% down.

This deal will close this week. Ramsey is concerned the media will hype this transaction. He points out that the sponsors cherry picked the mortgages and he wrote "these are the crème de la crème of mortgages". In addition the sponsors are taking the first loss positions:

"The sponsor (or affiliates of the sponsor) will initially retain the following certificates: (i) all of the Non-Offered Certificates, representing 6.50% of the original principal balance of the securitization, and (ii) 5% of the original principal balance of Offered Certificates."There are plenty of details - heck, 22 of the borrowers make over $100,000 per month (yes, per month).

This is as close to bulletproof as it gets.

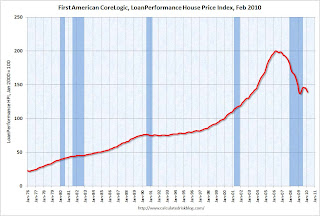

First American CoreLogic: House Prices Decline 2.0% in February

by Calculated Risk on 4/26/2010 10:48:00 AM

The Fed's favorite house price indicator from First American CoreLogic’s LoanPerformance ...

From LoanPerformance: Home Price Index Shows First Annual Increase in Over Three Years, But Shadow Inventory and End of Tax Credit Program May Result in Further Declines

National home prices, including distressed sales, increased by 0.3 percent in February 2010 compared to February 2009, according to First American CoreLogic and its LoanPerformance Home Price Index (HPI). This was an improvement over January’s year-over-year price decline of 0.5 percent. Excluding distressed sales, year-over-year prices increased in February by 0.6 percent; an improvement over the January non-distressed HPI which fell by 1.1 percent year-over-year.

On a month-over-month basis, the national average home price index fell by 2.0 percent in February 2010 compared to January 2010, which was steeper than the previous one-month decline of 1.6 percent from December to January. Prices are typically weak in the winter months, so seasonal effects may be driving this one-month change.

Click on graph for larger image in new window.

Click on graph for larger image in new window. This graph shows the national LoanPerformance data since 1976. January 2000 = 100.

The index is up 0.3% over the last year, and off 30.6% from the peak.

House prices are off 4.9% from the recent peak in August 2009 (although some of the decline is seasonal).

With all the distressed sales and government programs, it is hard to separate the seasonal factors from other distortions. However I expect that we will see lower prices on this index later this year - as does CoreLogic (from the press release):

After a modest increase this spring and summer, the national single-family combined index is projected to decline by 3.4 percent from February 2010 to February 2011 assuming the expiration of current Federal Housing Stimulus programs.