RSS Feed

RSS Feed by Calculated Risk on 3/20/2010 09:33:00 PM

Saturday, March 20, 2010

Federal Home Loan Bank sues Wall Street Banks for Billions

This was lawsuit was filed on March 15th. Here are some details from the bank and see Morgenson's story in the NY Times for more ...

From the Federal Home Loan Bank of San Francisco: Statement Regarding PLRMBS Litigation

Today the Federal Home Loan Bank of San Francisco (Bank) filed complaints in the Superior Court of California, County of San Francisco, against nine securities dealers in relation to certain of the Bank’s investments in private-label residential mortgage-backed securities (PLRMBS). The Bank is seeking to rescind its purchases of 134 securities in 113 securitization trusts, for which the Bank originally paid more than $19.1 billion. The Bank’s complaints allege that the dealers made untrue or misleading statements about the characteristics of the mortgage loans underlying the securities.From Grechen Morgenson at the NY Times: Pools That Need Some Sun

All of the PLRMBS in the Bank’s mortgage portfolio, including those identified in the complaints filed today, were rated AAA when purchased, based on the information provided by the securities dealers.

The suit, filed March 15 in state court in California, seeks the return of the $5.4 billion as well as broader financial damages.All the private mortgage insurers are working hard to rescind as many insurance policies as possible based on fraud and misrepresentation . As are Fannie and Freddie.

...

The defendants in the Federal Home Loan Bank case were among the biggest sellers of mortgage-backed securities back in the day; among those named are Deutsche Bank; Bear Stearns; Countrywide Securities, a division of Countrywide Financial; Credit Suisse Securities; and Merrill Lynch. The securities at the heart of the lawsuit were sold from mid-2004 into 2008 ...

In the complaint, the Federal Home Loan Bank recites a list of what it calls untrue or misleading statements .... The alleged inaccuracies involve disclosures of the mortgages’ loan-to-value ratios ... as well as the occupancy status of the properties securing the loans. ...

Finally, the complaint said, the sellers of the securities made inaccurate claims about how closely the loan originators adhered to their underwriting guidelines.

Fannie Mae and Freddie Mac may force lenders including Bank of America Corp., JPMorgan Chase & Co., Wells Fargo & Co. and Citigroup Inc. to buy back $21 billion of home loans this year as part of a crackdown on faulty mortgages.It makes sense that the Federal Home Loan Banks get more aggressive too.

Economic Outlook: Review of Possible Downside Risks to Forecast

by Calculated Risk on 3/20/2010 06:02:00 PM

Last week I reviewed some possible upside surprises for my economic outlook for sluggish and choppy growth in 2010. The most likely upside surprise appears to be coming from consumer spending and the lack of an increase in the saving rate. I still think the saving rate will continue to rise - although maybe not as fast as I originally expected.

Before I comment on downside risks, a quick comment on forecasts: I think a reasonably intelligent person can always make a compelling bearish argument for the economy, and yet most of the time the economy grows and employment increases. Just something I like to remember.

And although I enjoy being a contrarian at times (like calling the housing bubble and bust, or predicting in 2006 that a recession would start in 2007 - or calling the bottom for housing and autos early last year), I try to avoid the mistake of being a contrarian just to be contrary.

Right now my forecast is middle-of-the-road; no V-shaped recovery and no double-dip recession in 2010. Of the two, I think a double-dip is more likely, but I think we will avoid both. Of course the downside to sluggish growth is that unemployment will probably stay elevated for some time.

Don't get me wrong - I'd like to see 6% to 8% GDP growth and the unemployment rate dropping sharply (a "V-shaped recovery") but that seems very unlikely with the two usual engines of recovery, consumer spending and residential investment, both under pressure.

Downside Risks

There are a number of international risks that might impact the U.S. economy in 2010 such as a sovereign debt issues in Europe and elsewhere, and the escalating dispute with China over currency manipulation or a slowdown in the global economy. My guess is the impact on the U.S. this year will be minimal. And there are also long term issues - like the U.S. structural budget deficit and debt - but this will have little impact in the short term.

So I'll focus on domestic issues, and the number one risk remains housing:

The next wave of distressed sales is building based on analysis by both Barclays Capital and economist Tom Lawler. Although this wave will probably be somewhat smaller than in late 2008, it might be more sustained (it will just keep flooding the market with distressed homes).

After the expiration of the tax credit, demand will probably decline - and prices could start falling again in areas with significant distressed sale activity. Note: For the tax credit, buyers have to sign agreements by April 30th and close by June 30th. This wave of distressed sales will probably be concentrated in the bubble states, but will be more price diverse than the late 2008 foreclosure wave that was primarily in lower end areas.

If prices fall further than I expect that could have a serious impact on banks (more losses) and consumer confidence (less spending).

Note: Most of the forecasts for residential investment (RI) in 2010 were for moderate growth. My forecast was for RI to move sideways with perhaps sluggish growth. This is especially important for construction related industries and employment. Most of the forecasts have recently been revised down substantially, as an example from Reuters: Fannie Mae slashes mortgage investment forecast

Residential investment is likely to drop 17.2 percent in the first quarter and rebound for the rest of 2010, Fannie Mae economists, led by Doug Duncan, said in their outlook. Just a month ago, they expected the first quarter's residential investment would rise 2.8 percent.The other possible downside risks I mentioned last year were (these all still remain although are less likely):

For all of 2010, residential investment will grow 10 percent, slightly below the previous forecast, they said.

An index measuring small-business optimism fell 1.3 points to 88.0 in February, erasing January's gain, according to a monthly survey released Tuesday by the National Association of Independent businesses.To summarize: I think sluggish and choppy growth in 2010 is still likely, but the key downside risks are from falling home prices and less than expected residential investment.

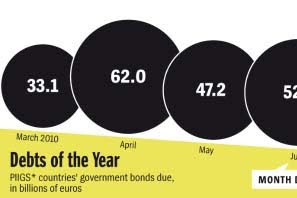

PIIGS Debt Coming Due

by Calculated Risk on 3/20/2010 01:09:00 PM

Click on graphic for Full Image at Der Spiegel

Click on graphic for Full Image at Der Spiegel

This graphic is from Anne Seith at Der Spiegel: Moment of Truth for Europe's Common Currency

Greece's financial difficulties have exposed numerous weaknesses which threaten Europe's common currency. Now, policy makers and economic experts are trying to find ways to stabilize the euro. SPIEGEL ONLINE takes a look at the proposals.Seith looks at several proposals from the formation a common EU economic government, to having better and automatic economic stablizers, to a Eurpoean Monetary Fund (EMF). None seem likely in the near term ...

"Worst of the IMF, without the benefits of a loan"

And from Le Monde (Google Translation): The cacophony lowers the euro

Greek Prime Minister George Papandreou has ... called for EU leaders to agree at the summit of Heads of State and Government on 25 and 26 March. Otherwise, it could well turn to the IMF. ... Mr. Papandreou stressed that with the austerity measures demanded by Brussels to Athens, his country had, in theory, "the worst of the IMF, but without the benefits of a loan".

...

Meanwhile, the IMF scenario seems to attract more and more within a Euro disoriented. After Germany, it is the Netherlands, Finland and Sweden are out of the woods Friday to support such intervention. Some are opposed, however, as the President of the European Central Bank (ECB), Jean-Claude Trichet.

Bank Failure Update

by Calculated Risk on 3/20/2010 09:38:00 AM

There have been 205 bank failures in this cycle (starting in 2007):

| FDIC Bank Failures by Year | 2007 | 3 |

|---|---|

| 2008 | 25 |

| 2009 | 140 |

| 2010 | 37 |

| Total | 205 |

Click on graph for larger image in new window.

Click on graph for larger image in new window.The first graph shows bank failures by week in 2008, 2009 and 2010.

The FDIC started fast in 2010, but slowed down when the snow storm hit D.C. - now it looks like the pace is picking back up again.

My (easy) prediction is the FDIC will close more banks in 2010 than in 2009 (more than 140), but fewer banks than in 1989 - peak of the S&L crisis (534 banks).

The second graph shows bank failures by year since the FDIC was started.

The second graph shows bank failures by year since the FDIC was started.The 140 bank failures last year was the highest total since 1992 (181 bank failures).

For those interested in bank failures by number of institutions and assets, the December Congressional Oversight Panel’s Troubled Asset Relief Program report through Nov 30th for 2009 (see page 45).

Friday, March 19, 2010

Unofficial Problem Bank List increases to 653

by Calculated Risk on 3/19/2010 10:51:00 PM

This is an unofficial list of Problem Banks compiled only from public sources. Changes and comments from surferdude808:

Publication of actions issued by the OCC and OTS contributed to an increase in the number of institutions and aggregate assets on the Unofficial Problem Bank List this week.The list is compiled from regulator press releases or from public news sources (see Enforcement Action Type link for source). The FDIC data is released monthly with a delay, and the Fed and OTC data is more timely. The OCC data is a little lagged. Credit: surferdude808.

This week the list includes 653 institutions with assets of $332.0 billion, up from 640 institutions with assets of $325.6 billion last week. The list increased despite the FDIC best efforts closing seven institutions of which five were on last week's list. The removals because of failure include Advanta Bank Corp. ($1.6 billion Ticker: ADVNQ), Appalachian Community Bank ($1.0 billion Ticker: APAB), First Lowndes Bank ($137 million), American National Bank ($70 million), and State Bank of Aurora ($28 million).

There were 18 institutions with assets of $9.3 billion added to the list this week. Additions include Los Alamos National Bank, Los Alamos, NM ($1.7 billion); NCB, FSB, Hillsboro, OH ($1.6 billon); Citizens First National Bank, Princeton, IL ($1.3 billion Ticker: PNBC); First Chicago Bank & Trust, Itasca, IL ($1.2 billion); and Norstates Bank, Waukegan, IL ($626 million Ticker: NSFC).

Other changes for institutions already on the list include Prompt Corrective Action Orders issued by the OTS against Savings Bank of Maine ($892 million); Inter Savings Bank, FSB ($701 million); and Woodlands Bank ($388 million).

See description below table for Class and Cert (and a link to FDIC ID system).

For a full screen version of the table click here.

The table is wide - use scroll bars to see all information!

NOTE: Columns are sortable - click on column header (Assets, State, Bank Name, Date, etc.)

Class: from FDIC

The FDIC assigns classification codes indicating an institution's charter type (commercial bank, savings bank, or savings association), its chartering agent (state or federal government), its Federal Reserve membership status (member or nonmember), and its primary federal regulator (state-chartered institutions are subject to both federal and state supervision). These codes are:Cert: This is the certificate number assigned by the FDIC used to identify institutions and for the issuance of insurance certificates. Click on the number and the Institution Directory (ID) system "will provide the last demographic and financial data filed by the selected institution".N National chartered commercial bank supervised by the Office of the Comptroller of the Currency SM State charter Fed member commercial bank supervised by the Federal Reserve NM State charter Fed nonmember commercial bank supervised by the FDIC SA State or federal charter savings association supervised by the Office of Thrift Supervision SB State charter savings bank supervised by the FDIC