RSS Feed

RSS Feed by Calculated Risk on 1/30/2006 07:27:00 PM

Monday, January 30, 2006

Fed Funds Rate: 4.5% almost guaranteed

Dr. Altig provides the Fed Funds probabilities for the next 3 meetings:

Jan 31st:So even with the dissapointing GDP data, it appears the market expects at least two more rate hikes. Dr. Duy channels the Fed with his always insightful Fed Watch: Now It Gets Interesting...

4.5%, 97%

March 28th:

4.75%, 73%

4.5%, 20%

May 10th:

4.75%, 53%

5%, 28%

4.5% 15%

For the Fed watcher, the 4Q05 GDP report is a real brainteaser. The central focus of the many, many blogs covering Friday’s news was the disappointing growth numbers (see William Polley’s and James Hamilton’s views, the latter including a long list of similar concerns). To be sure, the weak headline number deserved attention. But I was surprised by the relatively little attention placed on the inflation reading. I doubt the Fed is going to let that number slip by so lightly. Weak growth and higher inflation? Now that’s interesting.And on the topic of inflation, Fed Economist Mike Bryan writes: Holding on to the Edge of Comfort

Today’s PCE inflation report for December seems to have gotten a ho-hum response in financial markets. As it should. The data were tame and not widely off expectations.Not everyone agrees with Dr. Bryan's take on inflation (see Barry Ritholtz' Myths of the Greenspan Era). As a caveat, Dr. Bryan is writing for himself and not the Fed. Still its interesting to read his views.

30 year Pleasure Boat Loans

by Calculated Risk on 1/30/2006 02:04:00 PM

The LA Times reports: Sales of Pleasure Boats Buoyed by Soaring Home Values

California's hot real estate market has helped power a rise in boat sales by allowing people to borrow against the soaring value of their homes to buy boats and other big-ticket items.A couple of comments: I guess a 30 year loan on a pleasure boat is better financial planning than a 30 year loan for a hamburger!

In California, retail sales of recreational boats — from runabouts to $4-million luxury yachts — rose about 8% last year to a record $540 million, continuing a growth trend over the last five years, according to the Southern California Marine Assn. A similar increase is expected in 2006.

Though some economists worry that too many people are overextending themselves, the boating industry considers itself lucky that business is humming despite high gasoline prices.

"A lot of people are taking money out of their homes and buying different things, and one of them — fortunately — is boats," said Dave Geoffroy, executive director of the marine association, the organizer of the L.A. Boat Show.

But what happens when mortgage equity withdrawal slows?

... some dealers worry that boat sales could fall if real estate values drop, which happened in the early 1990s.I wonder if the slowdown in Q4 (1.1% annualized growth in GDP) was related to a slowdown in equity extraction? The Federal Reserve's Flow of Funds report (due March 9th) will help answer that question.

"I'm moderately concerned," said Michael Basso Jr., general manager of Sun Country Marine, which sells family boats and has locations in Castaic, Dana Point and Ontario.

He noted that half his buyers last year paid in cash, often from money they pulled out of their homes.

Friday, January 27, 2006

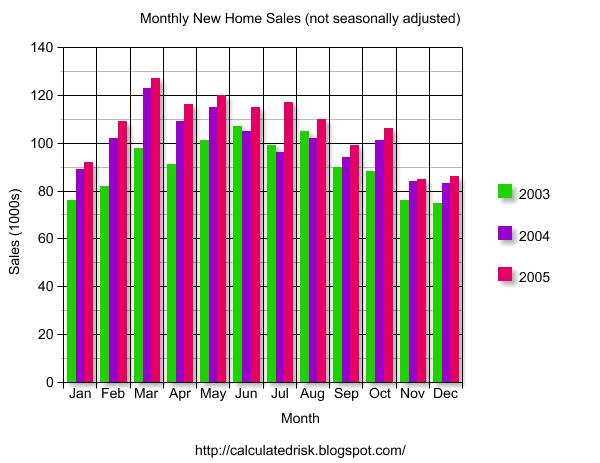

December New Home Sales: 1.269 Million Annual Rate

by Calculated Risk on 1/27/2006 12:16:00 AM

According to the Census Bureau report, New Home Sales in December were at a seasonally adjusted annual rate of 1.269 million vs. market expectations of 1.225 million. November's sales were revised down slightly to 1.233 million from 1.245 million.

Click on Graph for larger image.

NOTE: The graph starts at 700 thousand units per month to better show monthly variation.

The Not Seasonally Adjusted monthly rate was 86,000 New Homes sold, essentially the same as the 85,000 in November.

On a year over year basis, December 2005 sales were 3.6% higher than December 2004.

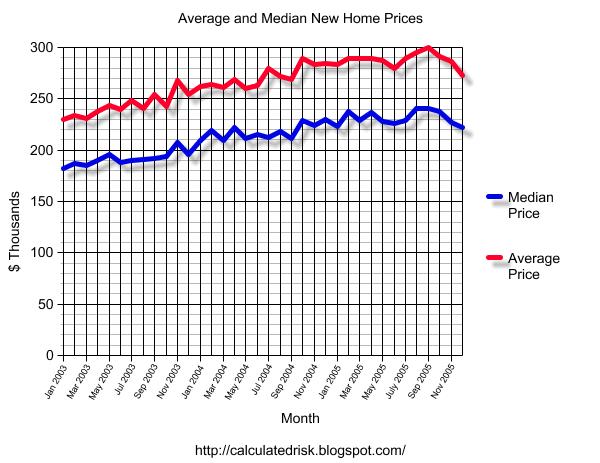

The median and average sales prices are trending down.

The median sales price of new houses sold in November 2005 was $225,200; the average sales price was $283,300.

The seasonally adjusted estimate of new houses for sale at the end of December was 516,000. This represents a supply of 4.9 months at the current sales rate.

The 516,000 units of inventory is the all time record for new houses for sale. On a months of supply basis, inventory is above the level of recent years.

This report is still reasonably strong.

Thursday, January 26, 2006

Lenders ask for Extension on New Mortgage Guidance

by Calculated Risk on 1/26/2006 01:14:00 AM

In December the FDIC, Office of the Comptroller, the Federal Reserve and other agencies issued a new proposed guidance on nontraditional mortgage products.

Now Reuters reports: US banks seek more mortgage proposal comment time

Lenders this week asked U.S. regulators to extend a comment period on a proposal that urged tighter underwriting on new mortgage products that may pose greater risks for banks and borrowers as interest rates rise.

Comments were due Feb. 27, but lenders have asked the Federal Reserve and other regulators for 30 more days.

"The proposal is extremely complex and has far-reaching consequences for our members, as well as for the nation's mortgage markets," wrote Janet Frank, director of mortgage finance in America's Community Bankers' government relations office.

"We believe that it will take an additional 30 days to complete the necessary evaluation and collect comments and data from our membership," Frank told regulators in a letter.

The Consumer Mortgage Coalition and HSBC North America Holdings Inc. also requested an additional 30 days.

Spokesmen for the Fed and Office of the Comptroller of the Currency were not immediately available to comment.

Wednesday, January 25, 2006

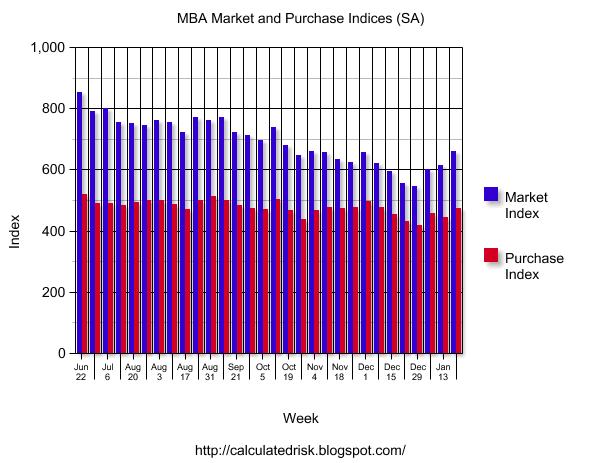

Mortgage Application Volume Up

by Calculated Risk on 1/25/2006 10:46:00 AM

The Mortgage Bankers Association (MBA) reports: Mortgage Application Volume Up In Latest Survey

Click on graph for larger image.

The Market Composite Index — a measure of mortgage loan application volume was 660.5 -- an increase of 7.7 percent on a seasonally adjusted basis from 613.3 one week earlier. On an unadjusted basis, the Index decreased 0.2 percent compared with the previous week and was down 0.4 percent compared with the same week one year earlier.Rates on fixed mortgages decreased slightly again, but ARM rates increased:

The seasonally-adjusted Purchase Index increased by 6.7 percent to 473.7 from 443.9 the previous week whereas the Refinance Index increased by 7.8 percent to 1773.9 from 1645.2 one week earlier.

The average contract interest rate for 30-year fixed-rate mortgages decreased to 6.04 percent from 6.07 percent on week earlier ...The MBA survey indicates RE activity is still at a fairly high level and rebounding in January.

The average contract interest rate for one-year ARMs increased to 5.44 percent from 5.39 percent one week earlier ...