RSS Feed

RSS Feed by Calculated Risk on 9/10/2005 12:25:00 PM

Saturday, September 10, 2005

Return from Paradise

After a week without news, hopefully I return with a clear head and a fresh look at the world. But first a few photos of Yellowstone ...

Click on photos for larger image.

The Yellowstone river winds its way through the Hayden valley in early September.

The wildlife viewing was excellent. Herds of bison were ubiquitous. We encountered several bull elk herding their harems through the forest. We saw wolves in the Lamar Valley, Pronghorn antelope, moose, coyote, trumpeter swan, mule deer and more. Did I mention the Bison were everywhere? Examining a large petrified Redwood tree stump on Specimen Ridge.

Examining a large petrified Redwood tree stump on Specimen Ridge.

This tree was buried some 50 million years ago by volcanic deposits and mudflows during a volcanic eruption. There are two smaller petrified Redwood trees just below the large Redwood (one in the bright sun, one in the shade). The view and the numerous specimens on the ridge (hence the name) made the steep climb worth the effort.

This Great Gray Owl greeted us on a short walk to the Natural Bridge (a small natural arch near Lake Yellowstone).

The park is incredible. The burn areas from the '88 fire are filling in with new growth and many of the young Lodgepole Pines, in the better growing areas, are 10 to 15 feet tall. I heartily recommend a September visit to Yellowstone.

Best to all and its great to be home!

Friday, September 02, 2005

Some Good News on Oil and Gas

by Calculated Risk on 9/02/2005 04:28:00 PM

NOTE: I will be out of town over the next week (leaving tonight). I hope everyone has a good week ... and my thoughts are with the victims of Hurricane Katrina.

The AP reports: Nations to Release 60M Barrels of Oil, Gas

Twenty-six countries in an international energy consortium will release more than 60 million barrels of crude oil and gasoline to relieve the energy crunch caused by Hurricane Katrina in the United States.This is a short term (30 day) fix since these countries are drawing down reserves to help the US. OCT Crude Oil was down to $67.57 per barrel and unleaded gasoline (OCT) down to $2.18 per gallon on the news.

...

[Energy Secretary Samuel Bodman] said he had received indications from other IEA members that a significant part of their portion would be refined products, mostly gasoline, which will be released onto global markets.

"We have made it known that we are facing shortfalls in available supplies of refined products in our country as a consequence of this storm," Bodman said, expressing confidence the gasoline will find its way to the United States where prices are expected to remain high.

Already there are 20 ships carrying gasoline from commercial foreign stocks to the United States, he said. The supplies from government stocks would be in addition.

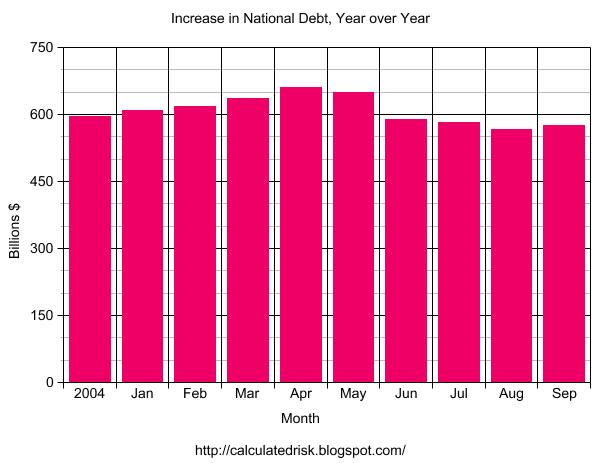

National Debt Increase: $575 Billion YoY

by Calculated Risk on 9/02/2005 03:06:00 PM

As of Sep 1, 2005 our National Debt is:

$7,929,658,283,890.28 (almost $8 Trillion)

As of Aug 1, 2004, our National Debt was:

$7,354,611,427,274.47

SOURCE: US Treasury.

Click on graph for larger image.

For comparison Year over Year Increase:

For Fiscal 2004 (End Sept 30, 2004): $596 Billion

For Jan 1, 2004 to Jan 1, 2005: $609.8 Billion

For Feb 1, 2004 to Feb 1, 2005: $618.6 Billion

For Mar 1, 2004 to Mar 1, 2005: $635.9 Billion

For Apr 1, 2004 to Apr 1, 2005: $660.9 Billion

For May 1, 2004 to May 1, 2005: $648.8 Billion

For Jun 1, 2004 to Jun 1, 2005: $588.0 Billion

For Jul 1, 2004 to Jul 1, 2005: $581.2 Billion

For Aug 1, 2004 to Aug 1, 2005: $566.2 Billion

For Sep 1, 2004 to Sep 1, 2005: $575.0 Billion

The debt situtation worsened slightly in August and fiscal 2005 has a chance to see the worst annual increase in National Debt ever. The current record annual increase in the National Debt is $596 Billion for fiscal '04.

So far, despite the much ballyhooed "budget improvement", the US keeps accumulating debt at about the same pace as last year.

August Jobs Report: 169 Thousand Added

by Calculated Risk on 9/02/2005 09:54:00 AM

From the AP:

In Friday's report, U.S. employers added 169,000 jobs in August, reflecting increased employment in industries, including construction, professional and business services, health care and education, and financial activities. But manufacturers shed jobs for the third straight month, reflecting the industry's sometimes bumpy road to recovery from the 2001 recession.Numbers are before the impact of Hurricane Katrina.

Also encouraging was that payroll gains were revised up for both June and July. Employers in July added 242,000 jobs, an improvement from the government's initial estimate of 207,000 net job gains. For June, 175,000 jobs were added, up from a previous estimate of a 166,000 jobs gain.

The payroll gain of 169,000 reported for August was less than the 190,000 new jobs some economists were forecasting before the release of the report. Economists were predicting the unemployment would hold steady at July's 5 percent rate.

Professional and business services added 29,000 jobs in August. Financial companies added 15,000. Education and health services expanded employment by 43,000. Leisure and hospitality added 34,000 jobs. Retailers added close to 12,000 during the month. Construction companies boosted payrolls by 25,000.

But factories cut another 14,000 jobs in August. Auto makers accounted for the biggest chunk of those job losses.

The labor market is the one part of the economy that has had difficulty getting back to full throttle after the 2001 recession.

Jobseekers still face challenges. The report showed that the average time that the 7.4 million unemployed spent searching for work in August was 18.9 weeks, up from 17.6 weeks in July.

Those who do have jobs are seeing wages rising. Average weekly earnings climbed to $544.59 in August, up from $543.92 in July. The figures aren't adjusted for inflation.

Bush's first term, with a net loss of 759K private sector jobs (a gain of 119K total jobs), has to be considered disappointing. For Bush's 2nd term, anything less than 6.8 Million net jobs will have to be considered poor. And anything above 10 million net jobs as excellent. Of course, in additional to the number of jobs, the quality of the jobs and real wage increases are also important measures.

For the quantity of jobs, the following graph provides a measurement tool for job growth during Bush's 2nd term.

Click on graph for larger image.

The blue line is for 10 million jobs created during Bush's 2nd term; the purple line for 6.8 million jobs. The insert shows net job creation for the first 7 months of the 2nd term - currently just below the blue line.

Thursday, September 01, 2005

DOE: Storm may shut refineries for months

by Calculated Risk on 9/01/2005 02:41:00 PM

From Reuters: Storm may shut refineries for months

The government warned on Thursday that some U.S. refineries shut by Hurricane Katrina may not resume processing oil for several months ...This is a temporary refined products supply shock. See Dr. Thoma's overview of AD vs. AS shocks.

...

"Some refineries likely (will be) able to restart their operations within the next 1 to 2 weeks, while others will likely be down for a more extended period, possibly several months," the Energy Information Administration said.

The Energy Department's analytical arm said nine major oil refineries in Louisiana and Mississippi remained shut from the hurricane. Those refineries account for about 11 percent of total U.S. refining capacity.

"Unlike 2004's Hurricane Ivan, which affected oil production facilities and had a lasting impact on crude oil production in the Gulf of Mexico, it appears that Hurricane Katrina may have a more lasting impact on refinery production and the distribution system," the EIA said in its most recent update on the effects of the hurricane on the energy sector.

Some key points: Oil is a global market. The loss of production in the GOM will be felt worldwide. Gasoline is much more of a domestic market (and regional), though some refined gasoline is imported - so there is a global aspect.

A Supply Shock will force the reduction in consumption of refined products through higher prices (Rationing hasn't been mentioned yet). It is possible that this reduction in demand will lead to lower crude oil prices even though gasoline and other refined products will remain elevated.

Just musing about possibilities ...