RSS Feed

RSS Feed by Calculated Risk on 5/12/2025 02:00:00 PM

Monday, May 12, 2025

Fed April SLOOS Survey: Banks reported Weaker Demand for Residential Real Estate

From the Federal Reserve: The April 2025 Senior Loan Officer Opinion Survey on Bank Lending Practices

The April 2025 Senior Loan Officer Opinion Survey on Bank Lending Practices (SLOOS) addressed changes in the standards and terms on, and demand for, bank loans to businesses and households over the past three months, which generally correspond to the first quarter of 2025.

Regarding loans to businesses over the first quarter, survey respondents reported, on balance, tighter lending standards and weaker demand for commercial and industrial (C&I) loans to firms of all sizes. Furthermore, banks reported tighter or basically unchanged lending standards, and weaker or basically unchanged demand for commercial real estate (CRE) loans.

Banks also responded to a set of special questions about changes in lending policies and demand for CRE loans over the past year. For all CRE loan categories, banks reported having tightened policies related to loan-to-value ratios and debt service coverage ratios. For some CRE loan categories, banks also tightened policies related to market areas served and the length of interest-only payment periods. For office loans, banks reported having tightened all queried policies on such loans over the past year.

For loans to households, banks reported basically unchanged lending standards and weaker demand for most categories of residential real estate (RRE) loans, on balance. Banks similarly reported basically unchanged lending standards but stronger demand for home equity lines of credit (HELOCs). In addition, banks reported having tightened standards for credit card loans, while standards remained basically unchanged for auto and other consumer loans. Meanwhile, demand reportedly weakened for credit card and other consumer loans and remained basically unchanged for auto loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph on Residential Real Estate demand is from the Senior Loan Officer Survey Charts.

This graph is for demand and shows that demand has been weak since late 2021.

The left graph is from 1990 to 2014. The right graph is from 2015 to Q1 2025.

2nd Look at Local Housing Markets in April

by Calculated Risk on 5/12/2025 10:31:00 AM

Today, in the Calculated Risk Real Estate Newsletter: 2nd Look at Local Housing Markets in April

A brief excerpt:

It appears sales will be down year-over-year for the 3rd consecutive month, and sales-to-date in 2025 are trailing sales in 2024 - and 2024 was the lowest sales year since 1995! And sales in April might have a 3 handle (be under 4 million).There is much more in the article.

...

Here is a look at months-of-supply using NSA sales. Since this is NSA data, it is likely months-of-supply will increase into the Summer.

Months in red are areas that are seeing 5 months of supply now and might see price pressures later this summer.

...

Many more local markets to come!

Housing May 12th Weekly Update: Inventory up 1.6% Week-over-week, Up 32.9% Year-over-year

by Calculated Risk on 5/12/2025 08:11:00 AM

Altos reports that active single-family inventory was up 1.6% week-over-week.

Inventory is now up 21.1% from the seasonal bottom in January and is increasing.

Usually, inventory is up about 11.5% from the seasonal low by this week in the year. So, 2025 is seeing a larger than normal pickup in inventory.

The first graph shows the seasonal pattern for active single-family inventory since 2015.

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025. The black line is for 2019.

Inventory was up 32.9% compared to the same week in 2024 (last week it was up 32.9%), and down 15.7% compared to the same week in 2019 (last week it was down 16.0%).

This is the highest level since prior to the pandemic.

It now appears inventory will be close to 2019 levels towards the end of 2025.

This second inventory graph is courtesy of Altos Research.

This second inventory graph is courtesy of Altos Research.

As of May 9th, inventory was at 756 thousand (7-day average), compared to 744 thousand the prior week.

Mike Simonsen discusses this data regularly on Youtube

Sunday, May 11, 2025

Sunday Night Futures

by Calculated Risk on 5/11/2025 06:21:00 PM

Weekend:

• Schedule for Week of May 11, 2025

Monday:

• At 2:00 PM ET, Senior Loan Officer Opinion Survey on Bank Lending Practices for April.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are up 73 and DOW futures are up 449 (fair value).

Oil prices were up over the last week with WTI futures at $61.39 per barrel and Brent at $64.21 per barrel. A year ago, WTI was at $80, and Brent was at $83 - so WTI oil prices are down about 23% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.08 per gallon. A year ago, prices were at $3.59 per gallon, so gasoline prices are down $0.51 year-over-year.

Trends in Educational Attainment in the U.S. Labor Force

by Calculated Risk on 5/11/2025 08:16:00 AM

The first graph shows the unemployment rate by four levels of education (all groups are 25 years and older) through April 2025. Note: This is an update to a post from several years ago.

Unfortunately, this data only goes back to 1992 and includes only three recessions (the stock / tech bust in 2001, and the housing bust/financial crisis, and the 2020 pandemic). Clearly education matters with regards to the unemployment rate, with the lowest rate for college graduates at 2.5% in April, and highest for those without a high school degree at 6.2% in April.

All four groups were generally trending down prior to the pandemic, and all are close to pre-pandemic levels now.

Click on graph for larger image.

Click on graph for larger image.

Note: This says nothing about the quality of jobs - as an example, a college graduate working at minimum wage would be considered "employed".

This brings up an interesting question: What is the composition of the labor force by educational attainment, and how has that been changing over time?

Here is some data on the U.S. labor force by educational attainment since 1992.

Currently, almost 67 million people (25 and over) in the U.S. labor force have a bachelor's degree or higher. This is almost 45% of the labor force, up from 26.2% in 1992.

Currently, almost 67 million people (25 and over) in the U.S. labor force have a bachelor's degree or higher. This is almost 45% of the labor force, up from 26.2% in 1992.

This is the only category trending up. "Some college", "high school" and "less than high school" have been trending down.

Based on recent trends, probably half the labor force will have at least a bachelor's degree sometime next decade (2030s).

Some thoughts: Since workers with bachelor's degrees typically have a lower unemployment rate, rising educational attainment is probably a factor in pushing down the overall unemployment rate over time.

Also, I'd guess more education would mean less labor turnover, and that education is a factor in lower weekly claims.

A more educated labor force is a positive for the future.

Saturday, May 10, 2025

Real Estate Newsletter Articles this Week: Current State of the Housing Market

by Calculated Risk on 5/10/2025 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Part 1: Current State of the Housing Market; Overview for mid-May 2025

• ICE Mortgage Monitor: Home Prices Continue to Cool

• 1st Look at Local Housing Markets in April

• Asking Rents Mostly Unchanged Year-over-year

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of May 11, 2025

by Calculated Risk on 5/10/2025 08:11:00 AM

The key reports this week are April CPI, Retail Sales and Housing Starts.

For manufacturing, April Industrial Production, and the May NY and Philly Fed manufacturing surveys will be released.

2:00 PM: Senior Loan Officer Opinion Survey on Bank Lending Practices for April.

6:00 AM ET: NFIB Small Business Optimism Index for April.

8:30 AM: The Consumer Price Index for April from the BLS. The consensus is for 0.3% increase in CPI (up 2.4% YoY), and a 0.3% increase in core CPI (up 2.8% YoY).

11:00 AM: NY Fed: Q1 Quarterly Report on Household Debt and Credit

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for initial claims of 230 thousand, up from 228 thousand last week.

8:30 AM ET: Retail sales for April are scheduled to be released. The consensus is for 0.1% increase in retail sales.

8:30 AM ET: Retail sales for April are scheduled to be released. The consensus is for 0.1% increase in retail sales.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

8:30 AM: The Producer Price Index for April from the BLS. The consensus is for a 0.3% increase in PPI, and a 0.3% increase in core PPI.

8:30 AM: The New York Fed Empire State manufacturing survey for May. The consensus is for a reading of -7.1, up from -8.1.

8:30 AM: the Philly Fed manufacturing survey for May. The consensus is for a reading of -8.5, up from -26.4.

8:40 AM: Speech, Fed Chair Jerome Powell, Framework Review, At the Thomas Laubach Research Conference, Washington, D.C.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for April.

9:15 AM: The Fed will release Industrial Production and Capacity Utilization for April.This graph shows industrial production since 1967.

The consensus is for a 0.1% increase in Industrial Production, and for Capacity Utilization to be unchanged at 77.8%.

10:00 AM: The May NAHB homebuilder survey. The consensus is for a reading of 40 up from 39 last month. Any number below 50 indicates that more builders view sales conditions as poor than good.

8:30 AM ET: Housing Starts for April.

8:30 AM ET: Housing Starts for April. This graph shows single and total housing starts since 2000.

The consensus is for 1.360 million SAAR, up from 1.324 million SAAR in March.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for May).

Friday, May 09, 2025

May 9th COVID Update: COVID Deaths Continue to Decline

by Calculated Risk on 5/09/2025 07:10:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

For deaths, I'm currently using 4 weeks ago for "now", since the most recent three weeks will be revised significantly.

Note: "Effective May 1, 2024, hospitals are no longer required to report COVID-19 hospital admissions, hospital capacity, or hospital occupancy data." So, I'm no longer tracking hospitalizations.

| COVID Metrics | ||||

|---|---|---|---|---|

| Now | Week Ago | Goal | ||

| Deaths per Week | 337✅ | 393 | ≤3501 | |

| 1my goals to stop weekly posts. 🚩 Increasing number weekly for Deaths. ✅ Goal met. | ||||

Click on graph for larger image.

Click on graph for larger image.This graph shows the weekly (columns) number of deaths reported since Jan 2023.

Although weekly deaths met the original goal to stop posting in June 2023 (low of 314 deaths), I've continued to post since deaths were above the goal again - and I'll continue to post until weekly deaths are once again below the goal for several weeks.

Weekly deaths are steadily decreasing following the winter pickup and are nearing the lows of last June.

This appears to be a leading indicator for COVID hospitalizations and deaths. This is moving towards the lows last May.

This appears to be a leading indicator for COVID hospitalizations and deaths. This is moving towards the lows last May.Nationally COVID in wastewater is "Low".

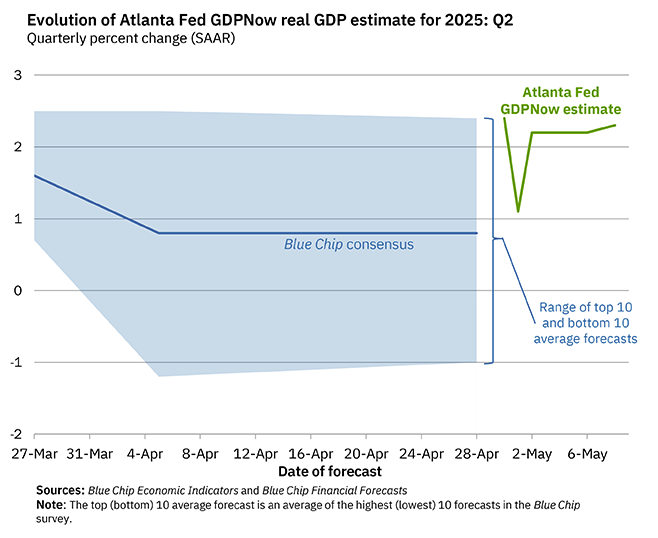

Q2 GDP Tracking: Around 2%

by Calculated Risk on 5/09/2025 02:27:00 PM

Plenty of data next week! Note that the Blue Chip consensus is wide - and currently around 1%.

From the Atlanta Fed:

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2025 is 2.3 percent on May 8, up from 2.2 percent on May 6. After this morning’s wholesale trade report from the US Census Bureau, the nowcast of the contribution of inventory investment to annualized second-quarter real GDP growth increased from -0.46 percentage points to -0.43 percentage points. [May 8th estimate]

Part 1: Current State of the Housing Market; Overview for mid-May 2025

by Calculated Risk on 5/09/2025 11:00:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Part 1: Current State of the Housing Market; Overview for mid-May 2025

A brief excerpt:

This 2-part overview for mid-May provides a snapshot of the current housing market.There is much more in the article.

Right now, the key story for existing homes is that inventory is increasing sharply, and sales are essentially flat compared to last year. That means prices will be under pressure (although there will not be a huge wave of distressed sales).

Yesterday, Realtor.com reported that there were “more than 1 million homes for sale last week, crossing this threshold for the first time since December 2019”.

...

Since inventory has increased sharply and sales are flat, a key for house prices is to watch months-of-supply. The following graph shows months-of-supply since 2017 using data from the NAR. Note that months-of-supply is higher than the previous 8 years!

Months-of-supply was at 4.0 months in March compared to 3.8 months in March 2019.

Inventory would probably have to increase to 5 1/2 to 6 months of supply to see national price declines.

AAR: Rail Carloads and Intermodal Up in April

by Calculated Risk on 5/09/2025 08:12:00 AM

From the Association of American Railroads (AAR) AAR Data Center. Graph and excerpts reprinted with permission.

Recent shifts in U.S. policies on trade and immigration have introduced volatility in financial markets and heightened uncertainty for firms. The ultimate outcomes and impacts of these policy changes remain unclear. Nevertheless, U.S. rail volumes have thus far remained stable, and many core economic indicators continue to signal underlying resilience. Railroads have long adapted to changing conditions, a legacy of resilience that continues today.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This table from the AAR shows the year-over-year change in carloads by category.

U.S. railroads originated 1.13 million total carloads in April 2025, up 6.2% (65,524 carloads) over April 2024. That’s the largest year-over-year percentage gain in 16 months and the third largest in nearly four years. Carloads averaged 225,569 per week in April—slightly below March, but otherwise the highest since October 2024, with gains in 13 of 20 categories tracked by AAR. Through the first four months of 2025, total carloads were up 1.8% (67,282 carloads) over the same period last year, with 11 of 20 carload categories seeing gains.

emphasis added

And on intermodal:

And on intermodal: U.S. rail intermodal traffic, which is not included in carload counts, totaled 1.36 million containers and trailers in April 2025, up 7.4% (93,244 units) over April 2024. Weekly intermodal volume averaged 272,300 units in April 2025. The only April with higher intermodal volume was April 2021. In fact, April 2021 holds the all-time intermodal record for any month, averaging 290,955 units per week. Year-to-date intermodal volume in 2025 through April was 4.90 million units, up 8.1% (365,456 units) over 2024 and the second highest ever for the first four months of a year (again behind 2021). Intermodal volume closely tracks port activity, making it a bellwether for international trade trends.As yet, there is no apparent impact on carloads and intermodal from policy changes.

Thursday, May 08, 2025

"Mortgage Rates Move Higher After Trade Deal"

by Calculated Risk on 5/08/2025 07:25:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Move Higher After Trade Deal

From Matthew Graham at Mortgage News Daily: Mortgage Rates Move Higher After Trade Deal

Mortgage rates moved back up to the higher levels seen earlier this week after the official announcement of a trade deal between the U.S. and the U.K.

...

In the bigger picture, today's mortgage rate increase is unremarkable--sort of average--and it leaves the rate index well below the early April highs, despite being well above the range seen during the month of March.

Realtor.com Reports Most Actively "For Sale" Inventory since 2019

by Calculated Risk on 5/08/2025 01:39:00 PM

What this means: On a weekly basis, Realtor.com reports the year-over-year change in active inventory and new listings. On a monthly basis, they report total inventory. For May, Realtor.com reported inventory was up 30.6% YoY, but still down 16.3% compared to the 2017 to 2019 same month levels.

Now - on a weekly basis - inventory is up 31.1% YoY.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending May 3, 2025 Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Inventory was up year-over-year for the 78th consecutive week.

Realtor.com has monthly and weekly data on the existing home market. Here is their weekly report: Weekly Housing Trends View—Data for Week Ending May 3, 2025

• Active inventory climbed 31.1% year-over-year

The number of homes actively for sale remains on a strong upward trajectory, now 31.1% higher than this time last year. This represents the 78th consecutive week of annual gains in inventory. There were more than 1 million homes for sale last week, crossing this threshold for the first time since December 2019.

• New listings—a measure of sellers putting homes up for sale—rebounded, rising 9.3% year-over-year

New listings picked up last week, rising 9.3% compared to a year ago. The momentum from earlier this spring is still going strong, pointing to a lively market heading into late spring and early summer. Last week boasted the highest number of new listings since mid-2022.

• The median list price was up 0.9% year-over-year

Home prices posted another slight gain this week, with the national median listing price rising 0.9% year-over-year.

Here is a graph of the year-over-year change in inventory according to realtor.com.

Here is a graph of the year-over-year change in inventory according to realtor.com. Inventory was up year-over-year for the 78th consecutive week.

New listings were the highest since 2022.

Median list prices are up slightly year-over-year.

Hotels: Occupancy Rate Increased 1.8% Year-over-year

by Calculated Risk on 5/08/2025 10:41:00 AM

From STR: U.S. hotel results for week ending 3 May

The U.S. hotel industry reported positive year-over-year comparisons, according to CoStar’s latest data through 3 May. ...The following graph shows the seasonal pattern for the hotel occupancy rate using the four-week average.

27 April through 3 May 2025 (percentage change from comparable week in 2024):

• Occupancy: 65.8% (+1.8%)

• Average daily rate (ADR): US$164.33 (+2.2%)

• Revenue per available room (RevPAR): US$108.06 (+4.1%)

Performance growth was lifted early in the week on the positive side of the Passover calendar shift.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025, blue is the median, and dashed light blue is for 2024. Dashed purple is for 2018, the record year for hotel occupancy.

The 4-week average of the occupancy rate is tracking below both last year and is close to the median rate for the period 2000 through 2024 (Blue).

Note: Y-axis doesn't start at zero to better show the seasonal change.

The 4-week average will mostly move sideways until the summer travel season. We will likely see a hit to occupancy during the summer months due to less international tourism.

Weekly Initial Unemployment Claims Decrease to 228,000

by Calculated Risk on 5/08/2025 08:30:00 AM

The DOL reported:

In the week ending May 3, the advance figure for seasonally adjusted initial claims was 228,000, a decrease of 13,000 from the previous week's unrevised level of 241,000. The 4-week moving average was 227,000, an increase of 1,000 from the previous week's unrevised average of 226,000.The following graph shows the 4-week moving average of weekly claims since 1971.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims increased to 227,000.

The previous week was unrevised.

Weekly claims were above the consensus forecast.

Wednesday, May 07, 2025

Thursday: Unemployment Claims

by Calculated Risk on 5/07/2025 07:59:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Thursday:

• At 8:30 AM ET, The initial weekly unemployment claims report will be released. The consensus is for initial claims of 223 thousand, down from 241 thousand last week.

Leading Index for Commercial Real Estate Increased 1% in April

by Calculated Risk on 5/07/2025 04:01:00 PM

From Dodge Data Analytics: Dodge Momentum Index Increases 1% in April

The Dodge Momentum Index (DMI), issued by Dodge Construction Network, grew 0.9% in April to 205.1 (2000=100) from the downwardly revised March reading of 203.1. Over the month, commercial planning grew 3.3% while institutional planning fell 4.2%.

“Despite an uptick in April, the bulk of the DMI’s growth was driven by a surge in data center planning, while momentum in other nonresidential sectors lagged behind,” stated Sarah Martin, associate director of forecasting at Dodge Construction Network. “Owners and developers are navigating heightened economic and policy uncertainty, which likely bogged down much of this month’s planning activity.”

A wave of data center projects entering planning played a key role in boosting commercial growth. Without data centers, commercial planning would have receded 2.3% in April and the entire DMI would have receded 3.0%. Office and hotel planning saw a sharp retreat this month, while warehouse and retail planning modestly ticked up. On the institutional side, planning momentum waned for education, healthcare, and government buildings. This was slightly offset by an uptick in recreational projects.

...

The DMI is a monthly measure of the value of nonresidential building projects going into planning, shown to lead construction spending for nonresidential buildings by a full year.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the Dodge Momentum Index since 2002. The index was at 205.1 in April, up from 220.9 the previous month.

According to Dodge, this index leads "construction spending for nonresidential buildings by a full year". This index suggests a pickup in mid-2025, however, uncertainty might impact these projects.

Commercial construction is typically a lagging economic indicator.

FOMC Statement: No Change to Fed Funds Rate

by Calculated Risk on 5/07/2025 02:00:00 PM

Fed Chair Powell press conference video here or on YouTube here, starting at 2:30 PM ET.

FOMC Statement:

Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace. The unemployment rate has stabilized at a low level in recent months, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook has increased further. The Committee is attentive to the risks to both sides of its dual mandate and judges that the risks of higher unemployment and higher inflation have risen.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Michelle W. Bowman; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Neel Kashkari; Adriana D. Kugler; Alberto G. Musalem; and Christopher J. Waller. Neel Kashkari voted as an alternate member at this meeting.

emphasis added

1st Look at Local Housing Markets in April

by Calculated Risk on 5/07/2025 11:11:00 AM

Today, in the Calculated Risk Real Estate Newsletter: 1st Look at Local Housing Markets in April

A brief excerpt:

This is the first look at several early reporting local markets in April. I’m tracking over 40 local housing markets in the US. Some of the 40 markets are states, and some are metropolitan areas. I’ll update these tables throughout the month as additional data is released.There is much more in the article.

Closed sales in April were mostly for contracts signed in February and March when 30-year mortgage rates averaged 6.84% and 6.65%, respectively (Freddie Mac PMMS). This was a decrease from the average rate for homes that closed in March. Any negative economic impacts from policy mostly happened in April, and that will probably not impact existing home sales until the May or June reports.

...

In April, sales in these markets were down 0.9% YoY. Last month, in March, these same markets were down 1.3% year-over-year Not Seasonally Adjusted (NSA).

Note that most of these early reporting markets have shown stronger year-over-year sales than most other markets for the last several months.

Important: There were the same number of working days in April 2025 (22) as in April 2024 (22). So, the year-over-year change in the headline SA data will be close to the change in the NSA data (there are other seasonal factors).

...

Many more local markets to come!

Wholesale Used Car Prices Increased in April; Up 4.9% Year-over-year

by Calculated Risk on 5/07/2025 09:32:00 AM

From Manheim Consulting today: Wholesale Used-Vehicle Prices Increased in April

Wholesale used-vehicle prices (on a mix, mileage, and seasonally adjusted basis) were much higher in April compared to March. The Manheim Used Vehicle Value Index (MUVVI) increased to 208.2, an increase of 4.9% from a year ago and also higher than March levels by 2.7%. This is the highest reading for the index since October 2023. The seasonal adjustment dampened the rise seen in the month, as non-seasonally adjusted values increased sharply on the back of the tariff announcement in early April. The non-adjusted price in April increased by 3.3% compared to March, moving the unadjusted average price up 4.3% year over year.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This index from Manheim Consulting is based on all completed sales transactions at Manheim’s U.S. auctions.

The Manheim index suggests used car prices increased in April (seasonally adjusted) and were up 4.9% YoY.

The tariffs are likely making some used cars more attractive.