RSS Feed

RSS Feed by Calculated Risk on 9/17/2010 09:41:00 PM

Friday, September 17, 2010

WSJ: Pension Gaps Loom Larger

From David Reilly at the WSJ: Pension Gaps Loom Larger

The median expected investment return for more than 100 U.S. public pension plans surveyed by the National Association of State Retirement Administrators remains 8%, the same level as in 2001, the association says.I keep expecting the plans to lower their expected returns, but that increases the funding requirements ...

...

Return assumptions can affect the size of so-called funding gaps—the amounts by which future liabilities to retirees exceed current pension assets. ... The concern is that the reluctance to plan for smaller gains will understate the scale of the potential time bomb facing America's government and corporate pension plans

Bank Failure #125: Maritime Savings Bank, West Allis, Wisconsin

by Calculated Risk on 9/17/2010 07:05:00 PM

Bankers wailing sea chanties

While the sea consumes

by Soylent Green is People

From the FDIC: North Shore Bank, FSB, Brookfield, Wisconsin, Assumes All of the Deposits of Maritime Savings Bank, West Allis, Wisconsin

As of June 30, 2010, Maritime Savings Bank had approximately $350.5 million in total assets and $248.1 million in total deposits. ... The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $83.6 million. ... Maritime Savings Bank is the 125th FDIC-insured institution to fail in the nation this year, and the first in Wisconsin.

Bank Failures #121 to 124: Georgia and Ohio

by Calculated Risk on 9/17/2010 06:19:00 PM

Autumn leaves fall to the ground

As do many banks.

by Soylent Green is People

From the FDIC: Community & Southern Bank, Carrollton, Georgia, Assumes All of the Deposits of Three Georgia Institutions

As of June 30, 2010, Bank of Ellijay had total assets of $168.8 million and total deposits of $160.7 million; First Commerce Community Bank had total assets of $248.2 million and total deposits of $242.8 million; and The Peoples Bank had total assets of $447.2 million and total deposits of $398.2 million.From the FDIC: Foundation Bank, Cincinnati, Ohio, Assumes All of the Deposits of Bramble Savings Bank, Milford, Ohio

...

The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) for Bank of Ellijay will be $55.2 million; for First Commerce Community Bank, $71.4 million; and for The Peoples Bank, $98.9 million. ... These failures bring the total number of failures to 123 for the nation and to 14 for Georgia. Prior to these failures, the last bank closed in the state was Northwest Bank & Trust, Acworth, on July 31, 2010.

As of June 30, 2010, Bramble Savings Bank had approximately $47.5 million in total assets and $41.6 million in total deposits. ... The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be $14.6 million. ... Bramble Savings Bank is the 124th FDIC-insured institution to fail in the nation this year, and the second in Ohio.Five down today. The FDIC is back to work ...

Bank Failure #120: ISN Bank, Cherry Hill, New Jersey

by Calculated Risk on 9/17/2010 04:18:00 PM

Wild times had with Cherry Hill

Never meant to be.

by Soylent Green is People

From the FDIC: New Century Bank, Phoenixville, Pennsylvania, Assumes All of the Deposits of ISN Bank, Cherry Hill, New Jersey

As of June 30, 2010, ISN Bank had approximately $81.6 million in total assets and $79.7 million in total deposits. ... The FDIC estimates that the cost to the Deposit Insurance Fund (DIF) will be approximately $23.9 million. Compared ... ISN Bank is the 120th FDIC-insured institution to fail in the nation this year, and the first in New Jersey. The last FDIC-insured institution closed in the state was First BankAmericano, Elizabeth, on July 31, 2009.Off to a quick start ...

Inflation: Core CPI, Median CPI, 16% trimmed-mean CPI

by Calculated Risk on 9/17/2010 02:25:00 PM

The Cleveland Fed has released the median CPI:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.1% (0.6% annualized rate) in August. The 16% trimmed-mean Consumer Price Index increased 0.1% (1.2% annualized rate) during the month.

...

Over the last 12 months, the median CPI rose 0.5%, the trimmed-mean CPI rose 0.9%, the CPI rose 1.1%, and the CPI less food and energy rose 0.9%.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows three measure of inflation, Core CPI, Median CPI (from the Cleveland Fed), and 16% trimmed CPI (also from Cleveland Fed).

They all show that inflation has been falling, and that measured inflation is up less than 1% year-over-year. Core CPI was flat, and median CPI and the 16% trimmed mean CPI were up 0.1% in August.

Note: The Cleveland Fed has a discussion of a number of measures of inflation: Measuring Inflation

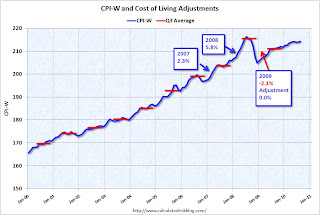

No increase to Social Security Benefits for 2011 (unofficial)

by Calculated Risk on 9/17/2010 11:28:00 AM

It won't be official until the BLS releases the September CPI-W report, but we can already say there will be no increase in Social Security benefits or the Maximum Contribution Base in 2011 (assuming no new legislation).

The BLS reported this morning that the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) was at 214.205 in August (CPI-W was at 213.898 in July).

Here is an explanation of why there will be no change (some repeated from a post last month):

The calculation dates have changed over time (see Cost-of-Living Adjustments), but the current calculation uses the average CPI-W for the three months in Q3 (July, August, September) and compares to the average for the highest previous average of Q3 months. Note: this is not the headline CPI-U.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows CPI-W over the last ten years. The red lines are the Q3 average of CPI-W for each year.

The COLA adjustment is based on the increase from Q3 of one year from the highest previous Q3 average. So a 2.3% increase was announced in 2007 for 2008, and a 5.8% increase was announced in 2008 for 2009.

In Q3 2009, CPI-W was lower than in Q3 2008, so there was no change in benefits for 2010.

For 2011, the calculation is not based on Q3 2010 over Q3 2009, but based on the average CPI-W for Q3 2010 over the highest preceding Q3 average - the 215.495 in Q3 2008. This means CPI-W in Q3 2010 has to average above 215.495 for there to be an increase in Social Security benefits in 2011.

In July 2010, CPI-W was at 213.898, and in August CPI-W was at 214.205 - so CPI-W would have to increase by almost 2% in September for the Q3 average to be at or above the Q3 2008 average. There is no evidence of a huge surge in inflation this month, so there will be no increase in Social Security benefits in 2011.

Even though there was no increase last year, and there will be no increase this year, those receiving benefits are still ahead because of the huge increase in Q3 2008.

Note: See post last month for a discussion of CPI-W and the Contribution Base.

Now the question is: Will Social Security benefits be flat in 2012 too? That is possible.

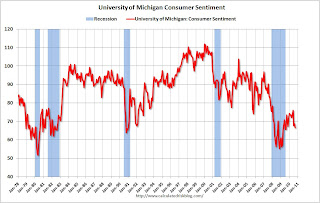

Consumer Sentiment declines in September, lowest level in a year

by Calculated Risk on 9/17/2010 09:55:00 AM

From MarketWatch: U.S. Sept. consumer sentiment falls to 66.6

The UMich index declined to 66.6 in September - the lowest level since August 2009 -- from 68.9 in August.

Click on graph for larger image in new window.

Click on graph for larger image in new window.Consumer sentiment is a coincident indicator - and this is further evidence of a sluggish economy.

This was a big story in July when consumer sentiment collapsed to the lowest level since late 2009. Now it is even lower ...

Consumer Price Index increases 0.3%, core rate unchanged in August

by Calculated Risk on 9/17/2010 08:30:00 AM

From the BLS report on the Consumer Price Index this morning:

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent in August on a seasonally adjusted basis, the U.S. Bureau of Labor Statistics reported today. ... Over the last 12 months, the all items index increased 1.1 percent before seasonal adjustment.The general disinflationary trend continues - core CPI is up less than 1% over the last year - and with all the slack in the system (especially the 9.6% unemployment rate), the various measures of inflation will probably stay low or even fall further.

...

The index for all items less food and energy was unchanged in August ... Over the last 12 months, the index for all items less food and energy rose 0.9 percent ...

The index for owners' equivalent rent was unchanged and the lodging away from home index fell 1.3 percent....

Note: I'll post a graph later after the Cleveland Fed releases the 16% trimmed CPI (another measure of inflation).

Thursday, September 16, 2010

Weekly Update on European Bond Spreads

by Calculated Risk on 9/16/2010 08:38:00 PM

Here are the European bond spreads from the Atlanta Fed weekly Financial Highlights released today (graph as of Sept 15th): Click on graph for larger image in new window.

Click on graph for larger image in new window.

From the Atlanta Fed:

European bond spreads have risen and remain elevated since the August FOMC meeting.A quiet week, but definitely still worth watching ... especially with all the currency manipulation going on.

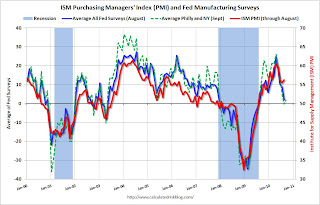

Update: Regional Fed Surveys and ISM

by Calculated Risk on 9/16/2010 04:35:00 PM

Note: Usually I don't watch this very closely, but right now I'm looking for signs of a slowdown in manufacturing. Eventually a watched pot does boil ...

By request - now that the Empire State and Philly Fed manufacturing surveys for September have been released - here is an update to the graph I posted last month: Click on graph for larger image in new window.

Click on graph for larger image in new window.

For this graph I averaged the New York and Philly Fed surveys (dashed green, through September), and averaged five surveys including New York, Philly, Richmond, Dallas and Kansas City (blue, through August).

The Institute for Supply Management (ISM) PMI (red) is through August (right axis).

Last month, when the ISM survey came in slightly better than expected, I wrote: "Based on this graph, I'd expect either the Fed surveys to bounce back in September - or the ISM to decline."

So far there has been little "bounce back" in the Fed surveys.

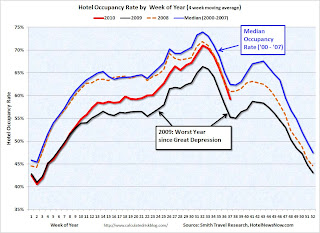

Hotel Occupancy Rate: "Bumpy Week"

by Calculated Risk on 9/16/2010 01:57:00 PM

Hotel occupancy is one of several industry specific indicators I follow ...

From HotelNewsNow.com: STR: US hotel industry has bumpy week

The U.S. hotel industry reported a decrease in average daily rate ADR for the first time in 13 consecutive weeks for the week of 5-11 September 2010, according to data from STR.The following graph shows the four week moving average for the occupancy rate by week for 2008, 2009 and 2010 (and a median for 2000 through 2007).

ADR fell 2.0% to US$92.84, occupancy increased 2.7% to 54.2%, and revenue per available room ended the week virtually flat with a 0.7% increase to US$50.32.

Click on graph for larger image in new window.

Click on graph for larger image in new window.Notes: the scale doesn't start at zero to better show the change. The graph shows the 4-week average, not the weekly occupancy rate.

On a 4-week basis, occupancy is up 7.2% compared to last year (the worst year since the Great Depression) and 5.1% below the median for 2000 through 2007.

The occupancy rate has fallen below the levels of 2008 again - and 2008 was a tough year for the hotel industry!

Important: Even with the occupancy rate close to 2008 levels, 2010 is a much more difficult year. The average daily rate (ADR) is off 14% from 2008 levels - so even with the similar occupancy rates, hotel room revenue is off sharply.

Data Source: Smith Travel Research, Courtesy of HotelNewsNow.com

Misc: China's Exchange Rate, Foreclosures, Poverty and Walking Away

by Calculated Risk on 9/16/2010 11:57:00 AM

A few articles:

It is the judgment of the IMF that, in view of the very limited movement in the Chinese currency, the rapid pace of productivity and income growth in China relative to its trading partners, the size of its current account surplus, and the substantial level of ongoing intervention in exchange markets to limit the appreciation of the Chinese currency, the renminbi is significantly undervalued.

We share that assessment. We are concerned, as are many of China’s trading partners, that the pace of appreciation has been too slow and the extent of appreciation too limited.

We will take China’s actions into account as we prepare the next Foreign Exchange Report, and we are examining the important question of what mix of tools, those available to the United States as well as multilateral approaches, might help encourage the Chinese authorities to move more quickly.

Bank repossessions ... increased about 3 percent from the month before to 95,364, a record high. At the same time the number of properties that received default notices—the first step in the foreclosure process—decreased 1 percent from a month ago and fell 30 percent from a year ago ...

Forty-four million people in the United States, or one in seven residents, lived in poverty in 2009, an increase of 4 million from the year before, the Census Bureau reported on Thursday.Here is the Census Bureau report.

The poverty rate climbed to 14.3 percent — the highest since 1994 — from 13.2 percent in 2008.

[T]he majority of Americans still believe [walking away] is unacceptable, according to a report from Pew Research Center.Here is the Pew Research report.

On the other hand, more than a third (36 percent) say the practice is at least sometimes acceptable.

Philly Fed Index shows contraction in September

by Calculated Risk on 9/16/2010 10:00:00 AM

Here is the Philadelphia Fed Index: Business Outlook Survey

The survey’s broadest measure of manufacturing conditions, the diffusion index of current activity, increased from a reading of -7.7 in August to -0.7 in September. The index, which has been negative for two consecutive months, suggests that growth has stalled over the last two months (see Chart). Indexes for new orders and shipments continued to indicate weakness this month: The new orders index fell 1 point, remaining negative for the third consecutive month, and the shipments index decreased 3 points, remaining negative for the second consecutive month.

Firms reported near steady employment this month but lower average work hours for existing employees. The percentage of firms reporting increases in employment (18 percent) narrowly edged out the percentage reporting decreases (16 percent). The index for employment was slightly positive this month, increasing 5 points from its negative reading in August. Indicative of weaker activity, more firms reported declines in average work hours for existing employees (30 percent) than reported increases (8 percent).emphasis added

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the Philly index for the last 40 years.

This index turned down sharply in June and July and was negative in August and September (indicating contraction).

These surveys are timely, but noisy. However this is further evidence of a slowdown in manufacturing. This was slightly worse than the consensus view of a reading of 3.8 (slight expansion).

Weekly initial unemployment claims decline slightly

by Calculated Risk on 9/16/2010 08:32:00 AM

The DOL reports on weekly unemployment insurance claims:

In the week ending Sept. 11, the advance figure for seasonally adjusted initial claims was 450,000, a decrease of 3,000 from the previous week's revised figure of 453,000 [revised up from 451,000]. The 4-week moving average was 464,750, a decrease of 13,500 from the previous week's revised average of 478,250.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the 4-week moving average of weekly claims since January 2000.

The dashed line on the graph is the current 4-week average. The four-week average of weekly unemployment claims decreased this week by 13,500 to 464,750.

This is the lowest level for weekly claims since early July, but it is still very high - the 4-week moving average has been moving sideways at an elevated level for about 10 months - and that suggests a weak job market.

Wednesday, September 15, 2010

Elizabeth Warren to lead Consumer Financial Protection Bureau, unofficially

by Calculated Risk on 9/15/2010 09:22:00 PM

From the NY Times: Warren to Unofficially Lead Consumer Agency

Elizabeth Warren, who conceived of the Consumer Financial Protection Bureau, will oversee its establishment as an assistant to President Obama, an official briefed on the decision said Wednesday evening.I think Ms. Warren is an excellent choice.

The decision, which Mr. Obama is to announce this week, would allow Ms. Warren, a Harvard law professor, to effectively run the new agency without having to go through a potentially contentious confirmation battle in the Senate.

The two key housing problems

by Calculated Risk on 9/15/2010 07:00:00 PM

I think there are two key problems for the housing market: 1) the excess supply of existing housing units, and 2) negative equity.

The excess supply is keeping pressure on residential investment, and therefore on employment and economic growth. As new households are formed, the excess supply will be absorbed - but this is happening very slowly.

Hence the quote of the day:

Time Warner Cable ... CFO Robert Marcus said "subscriber environment very, very weak," thanks to high unemployment, high ... vacancies and "really anemic new home formation."It takes jobs to create households, and usually housing is the key driver for employment growth in the early stages of a recovery. So this is a trap: the excess supply means weak employment growth, leading to few new households, so the excess supply is absorbed slowly - putting off more robust employment growth.

The excess supply is also pushing down house prices (prices are just starting to fall again). Lower prices will eventually help clear the market, however lower prices will push more homeowners into negative equity.

And negative equity is the other key problem for housing. It is difficult for homeowners with negative equity to sell, it is difficult to move for employment or other reasons, it is hard to refinance, and it is demoralizing for many homeowners (especially those with substantial negative equity).

Negative equity frequently leads to distressed sales (short sales or foreclosures), and losses for lenders.

At the end of Q2, CoreLogic reported that "11 million, or 23 percent, of all residential properties with mortgages were in negative equity". And an "additional 2.4 million borrowers had less than five percent equity". With house prices falling, several million more properties will be in a negative equity position later this year and in 2011.

"Negative equity continues to both drive foreclosures and impede the housing market recovery. With nearly 5 million borrowers currently in severe negative equity, defaults will remain at a high level for an extended period of time," said Mark Fleming, chief economist with CoreLogic.The negative equity problem is intractable. The administration has pushed modifications (HAMP), short sales (HAFA), the Fannie 125% LTV refinance program (HARP), the FHA short refinance option (for lenders willing to write down principal) and a number of other programs. These have had limited success so far (the FHA short refinance option just started).

It is important to note that falling house prices helps clear the excess supply, although more jobs and more households is the preferred solution. However falling prices makes the negative equity problem worse.

The "good" news is the banks were stress tested for much lower house prices. The following graph shows the two bank stress test scenarios compared to the Case-Shiller Composite 10 Index.

Click on graph for larger image in new window.

Click on graph for larger image in new window.The heavy government support for house prices has kept prices well above the baseline scenario. With prices higher than projected, fewer homeowners are in negative equity, and banks have taken fewer write downs than originally expected. Meanwhile many homeowners have been able to refinance into Fannie and Freddie (or FHA insured) loans putting the future risk on the taxpayer.

Based on the stress test results, the large banks should be able to handle further price declines - and falling prices will help clear the excess supply.

Both of these problems are very frustrating and will take time to resolve, but this suggests that policy should not be targeted at trying to support house prices.

Quote of the Day from Time Warner Cable: "anemic new home formation"

by Calculated Risk on 9/15/2010 03:44:00 PM

Via Dow Jones (ht Brian):

Time Warner Cable ... CFO Robert Marcus said "subscriber environment very, very weak," thanks to high unemployment, high ... vacancies and "really anemic new home formation."Although housing completions are at a record low (adding few net new housing units to the housing stock), additional household formation is key to absorbing the overhang of excess housing units.

Cartoon: "Signs of the Times"

by Calculated Risk on 9/15/2010 02:47:00 PM

From cartoonist Eric G. Lewis:

CoreLogic: House Prices decline 0.6% in July

by Calculated Risk on 9/15/2010 11:18:00 AM

Notes: CoreLogic reports the year-over-year change. The headline for this post is for the change from June 2010 to July 2010. The CoreLogic HPI is a three month weighted average of May, June and July and is NSA.

From CoreLogic (formerly First American LoanPerformance): CoreLogic Home Price Index Remained Flat in July

CoreLogic ... today released its Home Price Index (HPI) that showed that home prices in the U.S. remained flat in July as transaction volumes continue to decline. This was the first time in five months that no year-over-year gains were reported. According to the CoreLogic HPI, national home prices, including distressed sales showed no change in July 2010 compared to July 2009. June 2010 HPI showed a 2.4 percent year-over-year gain compared to June 2009. ...

Although home prices were flat nationally, the majority of states experienced price declines and price declines are spreading across more geographies relative to a few months ago. Home prices fell in 36 states in July, nearly twice the number in May and the highest since last November when national home prices were declining," said Mark Fleming, chief economist for CoreLogic.

Click on graph for larger image in new window.

Click on graph for larger image in new window. This graph shows the national CoreLogic HPI data since 1976. January 2000 = 100.

The index is flat over the last year, and off 28% from the peak.

The index is 6.1% above the low set in March 2009, and I expect to see a new post-bubble low for this index later this year or early in 2011.

Industrial Production, Capacity Utilization increase in August

by Calculated Risk on 9/15/2010 09:15:00 AM

From the Fed: Industrial production and Capacity Utilization

Industrial production rose 0.2 percent in August after a downwardly revised increase of 0.6 percent in July [revised down from 1.0 percent]. ... The index for manufacturing output rose 0.2 percent in August after having advanced 0.7 percent in July; the step-down in the rate of increase reflected a fallback in the production of motor vehicles and parts, which had jumped sharply in July. Excluding motor vehicles and parts, manufacturing output increased 0.5 percent in August after having gained 0.2 percent in July. ... At 93.2 percent of its 2007 average, total industrial production in August was 6.2 percent above its year-earlier level. The capacity utilization rate for total industry rose to 74.7 percent, a rate 4.7 percentage points above the rate from a year earlier and 5.9 percentage points below its average from 1972 to 2009.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows Capacity Utilization. This series is up 9.6% from the record low set in June 2009 (the series starts in 1967).

Capacity utilization at 74.7% is still far below normal - and well below the the pre-recession levels of 81.2% in November 2007. (Note: this is actual a decrease before the revision to July)

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.This is the highest level for industrial production since Oct 2008, but production is still 7.2% below the pre-recession levels at the end of 2007.

The increase in August was about consensus, however the sharp downward revision to July puts this below consensus.