RSS Feed

RSS Feed by Calculated Risk on 7/29/2010 02:26:00 PM

Thursday, July 29, 2010

More Builder Evidence of impact of tax credit

Home builder Ryland announced Q2 earnings today. From Briefing.com (ht Brian):

Ryland says that the big question from last quarter's conference call was what impact the expiration of the tax credit will have on the new home market. Says they found out the answer to that question in Q2, as sales slowed significantly. ... Says they knew there would be a slowdown in May once the event passed, but they didn't expect it to be as severe or prolonged as it's been...

Hotel Occupancy Rate at 71.8% last week

by Calculated Risk on 7/29/2010 01:17:00 PM

Hotel occupancy is one of several industry specific indicators I follow ...

From HotelNewsNow.com: STR: Strong luxury results week ending 24 July

Overall [year over year], the industry’s occupancy increased 7.3 percent to 71.8 percent, ADR rose 1.3 percent to US$99.60, and RevPAR increased 8.6 percent to US$71.54.The following graph shows the four week moving average for the occupancy rate by week for 2008, 2009 and 2010 (and a median for 2000 through 2007).

Click on graph for larger image in new window.

Click on graph for larger image in new window.Notes: the scale doesn't start at zero to better show the change. The graph shows the 4-week average, not the weekly occupancy rate.

On a 4-week basis, occupancy is up 7.0% compared to last year (the worst year since the Great Depression) and 4.8% below the median for 2000 through 2007.

On a weekly basis this is the second week since summer 2008 with the occupancy rate above 70%. However last week was probably the peak for the occupancy rate for 2010 - although the 4-week average will move up over the next few weeks.

In 2009, the occupancy rate peaked at 67% in mid-July.

Data Source: Smith Travel Research, Courtesy of HotelNewsNow.com

Kansas City Fed: Manufacturing activity rebounded moderately in July

by Calculated Risk on 7/29/2010 11:00:00 AM

Note: Usually I don't post all the regional manufacturing surveys, however with the inventory adjustment over, export growth appearing to slow, and domestic consumer demand sluggish, these surveys might provide a hint of weakness in the manufacturing sector.

From the Kansas City Fed: Tenth District manufacturing activity rebounded moderately in July

Tenth District manufacturing activity rebounded moderately in July, and expectations for future production remained positive. However, plans for future hiring and capital spending were essentially flat. Price indexes were mostly unchanged.This was a little more positive than the other regional reports that are all showing a slowdown in growth:

It appears overall that growth in the manufacturing sector moderated in July, and some of the internals are even weaker.

Toss in the weaker tone of in the Fed's Beige Book (released yesterday), and this raises the question: Is Fed Chairman Bernanke and the FOMC behind the curve (again)? In his testimony last week, Bernanke said:

My colleagues on the Federal Open Market Committee (FOMC) and I expect continued moderate growth ... Most FOMC participants expect real GDP growth of 3 to 3-1/2 percent in 2010That seems pretty optimistic.

Weekly Initial Unemployment Claims: Eight Months of Moving Sideways

by Calculated Risk on 7/29/2010 08:30:00 AM

The DOL reports on weekly unemployment insurance claims:

In the week ending July 24, the advance figure for seasonally adjusted initial claims was 457,000, a decrease of 11,000 from the previous week's revised figure of 468,000. The 4-week moving average was 452,500, a decrease of 4,500 from the previous week's revised average of 457,000.

...

The advance number for seasonally adjusted insured unemployment during the week ending July 17 was 4,565,000, an increase of 81,000 from the preceding week's revised level of 4,484,000.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the 4-week moving average of weekly claims since January 2000.

The four-week average of weekly unemployment claims decreased this week by 4,500 to 452,500.

The dashed line on the graph is the current 4-week average.

The 4-week average of initial weekly claims has been at about the same level since December 2009 (eight months) and the 4-week average of 452,500 is high historically, and suggests a weak labor market.

Wednesday, July 28, 2010

Blinder and Zandi Paper

by Calculated Risk on 7/28/2010 10:41:00 PM

For those interested, here is the paper by Alan Blinder and Mark Zandi that I mentioned last night: How the Great Recession Was Brought to an End

More Builder Evidence of Tax Credit Goose, Post-Credit Bust

by Calculated Risk on 7/28/2010 06:04:00 PM

CR Note: This is from housing economist Tom Lawler.

Meritage Homes, the 11th largest US home builder in 2009, reported that net home orders in the quarter ended 6/30/10 totaled 900, down 21.5% from the comparable quarter of 2009. Home deliveries, in contrast, jumped by 35.6% from a year ago to 1,207, reflecting buyers’ (and the builders) rush to close prior to the expected 6/30 closing date deadline for the federal home buyer tax credit. Compared to the previous quarter, net orders fell 15.4% while home closings surged by 49.4%. As a result, the company order backlog as of 6/30/10 fell to 1,044, down 22.7% from 3/31/10 and down 34.4% from a year ago.

Company officials were reportedly “surprised” by the extent of the post-tax-credit slowdown, and some analysts were a little spooked by the company’s move to increase active communities this year in California, Arizona, and Florida, while reducing its footprint in “lower-margin” Texas markets, as well as its recent acquisitions of land/lots. Meritage noted that margins on its newer communities have been higher than on older communities, in part because it purchased “deeply discounted” lots – especially in CA/AZ/FL. The company also said that it had “reduced our incentives while maintaining prices,” though whether it can do so in the post-tax-credit world remained unclear. Meritage, btw, appears to be one of those builders cited in yesterday’s WSJ article that may increase building in troubled markets that have not fully recovered yet because of land/lot acquisitions. (“Housing Glut is Likely to Build,”, July 27th, p. A2. This article, by the way, vastly overstates the potential for an increase in housing production related to SOME builders buying land/lots, often mainly either from other troubled builders or from banks. It also ignored surveys of builders indicating that most have dramatically cut their building production plans following the post-tax-credit plunge in sales, and ignored the sharp drop in SF building permits in May and June!!!)

M/I Homes, the 16th largest US home builder in 2009, reported that net home orders in the quarter ended 6/30/10 totaled 602, down 20.7% from the comparable quarter of 2009. Home deliveries last quarter totaled 790, up 60.6% form a year ago, as buyers (and the builder) rushed to close prior to the expected 6/30 closing date deadline for the federal home buyer tax credit. Compared to the previous quarter, net orders in the latest quarter fell by 21.3% while home deliveries surged by 64.9%. As a result, the company’s order backlog fell to 748 on 6/30/10, down 20.1% from 3/31/10 and down 32.4% from a year ago.

M/I CEO Robert Schottenstein noted that “coincident with the expiration of the tax credit on April 30, 2010 (for contract signings), we experienced a noticeable decline in our sales activity for May and June, resulting in a 21% decline in sales for the quarter” (implying BIG declines in May and June!) – breaking the company's previous string of six consecutive YOY gains in net orders.

At the risk of repeating myself (yet again!!!), the incoming data on home builders highlight that new home sales based on settlements actually surged in Q2/10 vs. Q1/10, even though contracts signed on a seasonally adjusted basis declined. Similarly, existing home sales closed in Q2 increased from Q1, even though new pending home sales declined. So for you “home data folks” who I guess because of ignorance add closed existing home sales to new SF home sales based on contracts signed/deposits taken (as reported by Census) to measure total home sales – stop it, it’s just wrong, and doing so makes you look like a fool!

CR Note: This was from Tom Lawler.

Schwarzenegger orders furloughs, California may start issuing IOUs in August

by Calculated Risk on 7/28/2010 04:01:00 PM

From the Sacramento Bee: Schwarzenegger orders more furloughs

[Gov. Arnold Schwarzenegger's] new executive order requires employees take three unpaid days off per month. But unlike that policy, it has no termination date: Furloughs will end when lawmakers pass a 2010-11 budget.And the beat goes on ...

...

The governor made the decision this week after Controller John Chiang said that unless lawmakers enacted a budget soon, the state's cash would go into the red by October. Chiang said he'll start issuing IOUs in August or September to conserve funds as long as possible.

Fed's Beige Book: Activity continued to increase, "steady" in some districts

by Calculated Risk on 7/28/2010 02:00:00 PM

Note: This is based on information collected on or before July 19, 2010.

From the Federal Reserve: Beige book

Economic activity has continued to increase, on balance, since the previous survey, although the Cleveland and Kansas City Districts reported that the level of economic activity generally held steady.And on real estate:

...

Manufacturing activity continued to expand in most Districts, although several Districts reported that activity had slowed or leveled off during the reporting period. Districts also noted improved conditions in the services sector.

...

Reports on retail sales during the early summer months were generally positive, although in most Districts the increases were modest.

Nearly all Districts reported sluggish housing markets in the months since the homebuyer tax credit expired on April 30. While some Districts, such as Boston and St. Louis, reported an increase in May and June home sales on a year-over-year basis, some contacts noted that these sales may reflect closings of homes under contract by the April tax credit deadline. The Boston, Philadelphia, Atlanta, and Kansas City Districts reported that home sales are expected to weaken going forward. Residential construction remained limited in several Districts. In the Atlanta District, residential construction activity softened from already weak levels. Homebuilders in the Cleveland District do not expect a turnaround in new home construction any time this year. Builders in the Chicago District are not introducing new inventory without a signed contract on a home. Housing starts were expected to decline for the second half of the year in the Dallas District and to increase slightly over the next three months in the Kansas City District.

Commercial and industrial real estate markets continued to struggle in all twelve Districts. Overall, vacancy rates were flat to slightly increased and continued to exert downward pressure on rents. Construction activity remained weak in most Districts. ... The outlook for commercial and industrial real estate across the Districts ranged from further declines in activity to slow growth.

Treasury: HAMP Re-default Rate incorrect

by Calculated Risk on 7/28/2010 10:55:00 AM

Several analysts noted the reported re-default rate appeared too low ... it was.

Shahien Nasiripour at the HuffPo has the story: HAMP Report Revised After Analysts Question New Metric

The Obama administration has revised its latest monthly report on its signature foreclosure-prevention plan, deleting a heavily-criticized performance metric used to measure whether assisted homeowners are re-defaulting on their taxpayer-financed mortgages.As Nasiripour notes, most analysts think a majority of HAMP modifications will eventually re-default. Nasiripour mentions a Fitch analyst's forecast that 75 percent will re-default; Barclays estimates 60 percent.

...

"Subsequent to releasing the report, Treasury received inquiries regarding the calculation methodology used in this table," spokesman Mark Paustenbach said Tuesday. "These inquiries were related to the treatment of modifications that are cancelled from HAMP and ultimately become ineligible for TARP incentives after 90 days delinquency.

"In an effort to review and better explain the methodology, we learned from our program administrator, Fannie Mae, that not all cancelled loans were included in the underlying information provided to Treasury," Paustenbach continued. "The error caused inconsistent reporting of permanent modifications during the snapshots reported. These omissions have impacted our previous analysis... with respect to the performance of HAMP permanent modifications."

...

In place of the now-deleted table, in a revised report posted Monday to their FinancialStability.gov Web site, Treasury said:

"Since the Making Home Affordable report was posted on July 20th, Fannie Mae, which administers the program, has reported to Treasury an issue in its implementation of the delinquency statistic methodology used to report performance of permanent modifications. Fannie Mae is now revising the data, and Treasury has retained a third-party consultant to provide additional review and validation. Upon completion of that independent review, a revised table will be provided.".

Last month, the reported median back end DTI1 was 63.7% AFTER modification. That just screams "re-default".

From HAMP: 1 Ratio of total monthly debt payments (including principal and interest on the first mortgage, taxes, insurance, homeowners association and/or condo fees, plus payments on installment debts, junior liens, alimony, car lease payments and investment property payments) to monthly gross income.

Durable Goods orders fall 1% in June

by Calculated Risk on 7/28/2010 08:33:00 AM

From the Census Bureau:

New orders for manufactured durable goods in June decreased $2.0 billion or 1.0 percent to $190.5 billion, the U.S. Census Bureau announced today. This was the second consecutive monthly decrease and followed a 0.8 percent May decrease.From Reuters: Durable Goods Orders Fall Short as Demand Stays Weak

...

Shipments of manufactured durable goods in June, down two consecutive months, decreased $0.7 billion or 0.3 percent to $195.0 billion. This followed a 0.7 percent May decrease.

The Commerce Department said durable goods orders fell 1.0 percent after a revised 0.8 percent drop in May.This was well below expectations, and is further evidence of a slowdown in the manufacturing sector.

Analysts polled by Reuters had forecast orders increasing 1.0 percent in June from May's previously reported 0.6 percent fall.

MBA: Mortgage Purchase Applications increase slightly last week

by Calculated Risk on 7/28/2010 07:53:00 AM

The MBA reports: Mortgage Applications Decrease in Latest MBA Weekly Survey

The Refinance Index decreased 5.9 percent from the previous week. The seasonally adjusted Purchase Index increased 2.0 percent from one week earlier and is the highest Purchase Index observed in the survey since the end of June.

...

The average contract interest rate for 30-year fixed-rate mortgages increased to 4.69 percent from 4.59 percent, with points decreasing to 0.88 from 1.04 (including the origination fee) for 80 percent loan-to-value (LTV) ratio loans.

Click on graph for larger image in new window.

Click on graph for larger image in new window.This graph shows the MBA Purchase Index and four week moving average since 1990.

Although the weekly applications index increased slightly, the 4-week average is still near the levels of 1996.

This collapse in the mortgage application index has already shown up as a decline in new home sales, and will show up in the July and August existing home sales reports (counted at close of escrow).

Tuesday, July 27, 2010

Paper: Policy helped avert Great Depression II

by Calculated Risk on 7/27/2010 10:58:00 PM

Alan Blinder and Mark Zandi will release a new paper tomorrow analyzing the impact of the policy response to the crisis ... Sewell Chan at the NY Times has a preview: In Study, 2 Economists Say Intervention Helped Avert a 2nd Depression

In a new paper, [Alan S. Blinder, a Princeton professor and former vice chairman of the Fed, and Mark Zandi, chief economist at Moody’s Analytics] argue that without the Wall Street bailout, the bank stress tests, the emergency lending and asset purchases by the Federal Reserve, and the Obama administration’s fiscal stimulus program, the nation’s gross domestic product would be about 6.5 percent lower this year.I'll post a link tomorrow (if it is available). David Leonhardt adds:

In addition, there would be about 8.5 million fewer jobs, on top of the more than 8 million already lost; and the economy would be experiencing deflation, instead of low inflation.

As Mr. Blinder and Mr. Zandi note, their estimates of the fiscal stimulus are similar to the estimates of others — including the Congressional Budget Office.Although Zandi completely missed the housing bubble, I've been using his estimates of the impact of policy (and estimates from Goldman Sachs), and I think they have been very useful in forecasting.

How far will the homeownership rate fall?

by Calculated Risk on 7/27/2010 07:32:00 PM

Earlier today the Census Bureau released the homeownership and vacancy rates for Q2 2010.

I posted a few graphs this morning, and I noted that the homeownership rate had fallen to the 1999 level of 66.9%.

A few years ago - when the homeownership rate was at 69%, I forecast that the rate would probably fall to the 66% to 67% range. Here is a repeat of the graph from this morning showing the trend of the homeownership rate since 1965. Click on graph for larger image in new window.

Click on graph for larger image in new window.

Note: graph starts at 60% to better show the change.

As I noted this morning, the homeownership rate increased in the '90s and first half of the '00s because of changes in demographics and "innovations" in mortgage lending. My guess is the increase due to demographics (older population) will probably stick, but the mortgage "innovation" increase will disappear.

Using the data from the Census Bureau on number of households per age cohort, we can calculate what would have happened to the overall homeownership rate if the rate per age cohort had stayed the same as in 1989 or in 1999.

Using the 1989 percentages, the homeownership rate would have increased from 63.9% in 1989 to 66.2% in 2009 just because of the aging population. Using the 1999 homeownership percentages, the homeownership rate would be 66.8% given the changes in demographics. That was the basis for my original forecast of the homeownership rate falling to the 66% to 67% range.

It is certainly possible that the homeownership rate might fall further than I originally expected since certain cohorts now own at a lower than historically normal rate - and many of these people might be turned off on home ownership for some time (if not forever). The second graph shows the homeownership rate by age cohort for 1989, 1999, 2005 (peak of housing bubble), and Q2 2010.

The second graph shows the homeownership rate by age cohort for 1989, 1999, 2005 (peak of housing bubble), and Q2 2010.

For those currently under 30, the homeownership rate is above the 1989 and 1999 levels - probably because most of these people were too young to participate in the insanity and some have taken advantage of the first time home buyer tax credit.

For the 30 to 60 groups, the homeownership rate is currently below the 1989 and 1999 levels. These groups were in their early 20s to early 50s during the bubble years - the prime buying years.

For the groups above 60 years old, the homeownership rate has stayed above the 1989 level. Most of these people already owned and probably didn't participate in the insanity.

But notice the highest cohort (over 75 years old). The homeownership rate is above the bubble years! This could mean that some people are staying in their homes, perhaps waiting for a better market to sell.

This does shows that the most impacted cohorts are currently in the 30 to 60 age groups, with the 30 to 35 year old cohort the hardest hit group (in their mid to late 20s during the bubble). The next hardest hit groups are the 45 to 59 cohorts - probably because some people were moving up to more home than they could afford.

For now I'll stick with my prediction of the homeownership rate falling to 66% or so, but it could certainly fall lower.

Survey: Local Government job losses projected to approach 500,000

by Calculated Risk on 7/27/2010 05:02:00 PM

As a follow-up to point 6 of the previous posts on the 2nd half slowdown (cutbacks at the state and local level), here is a new report released today: Job losses projected to approach 500,000 (ht Brian)

The effects of the Great Recession on local budgets will be felt most deeply from 2010 to 2012. In response, local governments are cutting services and personnel. This report from the National League of Cities (NLC), National Association of Counties (NACo), and the U.S. Conference of Mayors (USCM) reveals that local government job losses in the current and next fiscal years will approach 500,000, with public safety, public works, public health, social services and parks and recreation hardest hit by the cutbacks.According to the BLS, local governments (ex-education) have cut 89,000 jobs over the last year, and this survey suggests there will be much deeper cuts ahead.

...

In May and June of 2010 NLC, NACo and USCM conducted a survey of cities and counties across the country for the purpose of gauging the extent of job losses. The survey was emailed and faxed to all cities over 25,000 in population and to all counties over 100,000 in population. The survey results presented below are based on 270 responses, 214 responses from cities and 56 responses from counties.

...

The surveyed local governments report cutting 8.6 percent of total full-time equivalent (FTE) positions over the previous fiscal year to the next fiscal year (roughly 2009-2011). If applied to total local government employment nationwide, an 8.6 percent cut in the workforce would mean that 481,000 local government workers were, or will be, laid off over the two-year period. Projected cuts for the next fiscal year will likely increase as many of the nation’s local governments draft new budgets, deliberate about how to balance shortfalls and adopt new budgets.

The survey has a list or respondents (page 6) and several examples.

2nd Half Slowdown Update

by Calculated Risk on 7/27/2010 01:25:00 PM

"For me a double-dip is another recession before we've healed from this recession ... The probability of that kind of double-dip is more than 50 percent. I actually expect it."Now that the 2nd half slowdown is here, it might be worth reviewing some of the arguments for a slowdown:

Professor Robert Shiller, July 27, 2010 (via Reuters: Chance of Double-Dip US Recession is High: Shiller)

1) less Federal stimulus spending in the 2nd half of 2010.

The only additional stimulus has been the extension of the qualifying dates for unemployment benefits. Even with this extension, the overall stimulus peaked in Q2 or possibly Q3.

2) the end of the inventory correction.

This is pretty clear in the data, and we are seeing a slowdown in growth for the manufacturing sector (but not contraction). This is one of the reasons I'm tracking the regional manufacturing surveys so closely this week.

3) more household saving leading to slower growth in personal consumption expenditures.

This still isn't clear, although the personal saving rate ticked up in May.

4) another downturn in housing (lower prices, less residential investment).

It is clear that residential investment will be a drag on GDP in Q3. As far as prices, the declining prices will not show up until the September reports - or possibly the October reports (released with a significant lag). So this still seems correct, especially with the existing home months-of-supply in double digits. Diana Olick at CNBC quoted NAR chief economist Lawrence Yun:

Even the always glass-is-half-full chief economist Lawrence Yun made clear several times in the briefing before the report's release, that he expects home prices to come under significant pressure over the coming months, as inventories rise.Usually Yun is too optimistic.

...

Inventories will surpass ten months," says Yun. "If sustained, prices will surely be under pressure." Yun added that he originally expected the drag after the tax credit expiration to last about two months; he's now pushing that forecast to three to four months.

5) slowdown in China and Europe and

Growth in China has slowed, from the WSJ:

China's central bank struck a confident note Tuesday, saying the country's current economic slowdown is beneficial for long-term sustainable growth, and there is little risk of a "double-dip" recession.6) cutbacks at the state and local level.

"Although economic growth is showing signs of slowing down, China's current economic fundamentals are still very good. While a further slowdown and stabilization of growth is likely, the possibility of a double-dip is low," the People's Bank of China said in a quarterly report on the economy's performance.

This is starting to happen, and I expect the number of layoffs to increase later this year.

I still think we will avoid a technical double dip recession, but that won't matter to the people impacted by the slowdown.

Note: if the economy does slide into a recession, it will probably be consider a continuation of the recession that started in December 2007, see: Recession Dating and a "Double Dip"

Richmond Fed: Manufacturing Activity Moderates in July; Expectations Slip

by Calculated Risk on 7/27/2010 11:13:00 AM

Note: Usually I don't post all the regional manufacturing surveys, however with the inventory adjustment over, export growth appearing to slow, and domestic consumer demand sluggish, these surveys might provide a hint of weakness in the manufacturing sector.

From the Richmond Fed: Manufacturing Activity Moderates in July; Expectations Slip

In July, the seasonally adjusted composite index of manufacturing activity — our broadest measure of manufacturing — declined seven points to 16 from June's reading of 23. Among the index's components, shipments lost nine points to 22, new orders dropped 12 points to finish at 13, while the jobs index moved up six points to 15.This is similar to the Dallas Fed report yesterday: Texas Manufacturing Activity Remains Sluggish. It appears growth in the manufacturing sector is slowing.

...

Other indicators also suggested somewhat slower activity. The backlog of orders measure moved down two points to 1, and the index for capacity utilization fell eight points to 13.

Q2 2010: Homeownership Rate Lowest Since 1999

by Calculated Risk on 7/27/2010 10:00:00 AM

The Census Bureau reported the homeownership and vacancy rates for Q2 2010 this morning. Here are a few graphs ... Click on graph for larger image in new window.

The homeownership rate declined to 66.9%. This is the lowest level since 1999.

Note: graph starts at 60% to better show the change.

The homeownership rate increased in the '90s and early '00s because of changes in demographics and "innovations" in mortgage lending. The increase due to demographics (older population) will probably stick, so I've been expecting the rate to decline to the 66% to 67% range - and not all the way back to 64% to 65%.

I'll have to revisit this now that the homeownership rate has fallen back to the top of the range I expected!  The homeowner vacancy rate declined to 2.5% in Q2 2010.

The homeowner vacancy rate declined to 2.5% in Q2 2010.

A normal rate for recent years appears to be about 1.7%.

This leaves the homeowner vacancy rate about 0.8% above normal. This data is not perfect, but based on the approximately 75 million homeowner occupied homes, we can estimate that there are close to 500 thousand excess vacant homes.

The rental vacancy rate was steady at 10.6% in Q2 2010.  Other reports have suggested that the rental vacancy rate has declined slightly. This report is nationwide and includes homes for rent.

Other reports have suggested that the rental vacancy rate has declined slightly. This report is nationwide and includes homes for rent.

It's hard to define a "normal" rental vacancy rate based on the historical series, but we can probably expect the rate to trend back towards 8%. According to the Census Bureau there are close to 41 million rental units in the U.S. If the rental vacancy rate declined from 10.6% to 8%, then 2.6% X 41 million units or 1.07 million excess units would have to be absorbed.

This suggests there are still about 1.6 million excess housing units. These excess units will keep pressure on housing starts, rents and house prices for some time.

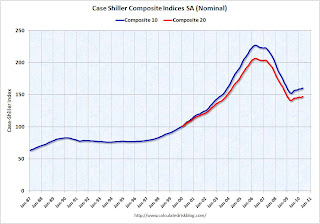

Case-Shiller: House Price indexes increase in May

by Calculated Risk on 7/27/2010 09:00:00 AM

IMPORTANT: These graphs are Seasonally Adjusted (SA). S&P has cautioned that the seasonal adjustment is probably being distorted by irregular factors. These distortions could include distressed sales and the various government programs.

S&P/Case-Shiller released the monthly Home Price Indices for May (actually a 3 month average).

This includes prices for 20 individual cities, and two composite indices (10 cities and 20 cities).

From S&P: For the Past Year Home Prices Have Generally Moved Sideways

Data through May 2010, released today by Standard & Poor’s for its S&P/Case-Shiller1 Home Price Indices, the leading measure of U.S. home prices, show that the annual growth rates in 15 of the 20 MSAs and the 10- and 20-City Composites improved in May compared to those reported for April 2010. The 10-City Composite is up 5.4% and the 20-City Composite is up 4.6%from where they were in May 2009. While 19 MSAs and both Composites reported positive monthly changes in May over April, only 12 of the MSAs and the two Composites saw better month-over-month growth rates in May than those reported in April.

Click on graph for larger image in new window.

Click on graph for larger image in new window. The first graph shows the nominal seasonally adjusted Composite 10 and Composite 20 indices (the Composite 20 was started in January 2000).

The Composite 10 index is off 29.3% from the peak, and up 1.0% in May (SA).

The Composite 20 index is off 28.7% from the peak, and up 1.1% in May (SA).

The second graph shows the Year over year change in both indices.

The second graph shows the Year over year change in both indices.The Composite 10 is up 5.4% compared to May 2009.

The Composite 20 is up 4.6% compared to May 2009.

This is the fourth month with YoY price increases in a row.

The third graph shows the price declines from the peak for each city included in S&P/Case-Shiller indices.

Prices increased (SA) in 15 of the 20 Case-Shiller cities in May seasonally adjusted.

Prices increased (SA) in 15 of the 20 Case-Shiller cities in May seasonally adjusted.Prices in Las Vegas are off 56.1% from the peak, and prices in Dallas only off 4.8% from the peak.

Case Shiller is reporting on the NSA data (19 cities with increasing prices), and I'm using the SA data. I'm not sure why S&P calls a 5% increase "moving sideways". Prices are probably starting to fall right now, but this will not show up in the Case-Shiller index for a few months.

Monday, July 26, 2010

Home builders to start building more homes?

by Calculated Risk on 7/26/2010 09:13:00 PM

The following article discusses both new and existing home supply. Here is a short excerpt on new homes ...

From Robbie Whelan at the WSJ: Supply of Homes Set to Grow

Home builders ... are stuck with thousands of acres that are prone to lose value as the market struggles. Many will build homes on the land, rather than write off its value and wait for the market to improve.In some communities with excess supply, home builders are competing with the distressed sales by building smaller homes. As an example, a couple months ago David Streitfeld at the NY Times wrote about a building boom in Las Vegas: In City of Homes That Sit Empty, Building Booms

... "They're discounting the homes, they're making very small profit margins, but they're building homes." [said Brad Hunter, chief economist at Metrostudy]

...

Other indicators also point to builders preparing to increase home construction, despite lagging sales. The number of finished vacant lots, or parcels of land that have been developed and readied for building, stands at about 1.2 million nationwide, according to Metrostudy, or just 5% below the peak in late 2008.

Home prices in Las Vegas are down by 60 percent from 2006 in one of the steepest descents in modern times. There are 9,517 spanking new houses sitting empty. An additional 5,600 homes were repossessed by lenders in the first three months of this year and could soon be for sale.But just because they have the lots, I hope they don't start overbuilding again.

Yet builders here are putting up 1,100 homes, and they are frantically buying lots for even more. ... Land and labor costs have fallen significantly, so the newest homes are competitively priced.

Jim the Realtor: Beach Cheapie?

by Calculated Risk on 7/26/2010 05:57:00 PM

Earlier (with graphs): New Home Sales: Worst June on Record

I haven't checked in with Jim for some time. This 800 sq ft REO is "cheap"?