RSS Feed

RSS Feed by Calculated Risk on 7/16/2025 09:15:00 AM

Wednesday, July 16, 2025

Industrial Production Increased 0.3% in June

From the Fed: Industrial Production and Capacity Utilization

Industrial production (IP) increased 0.3 percent in June after remaining unchanged in April and May; for the second quarter as a whole, IP increased at an annual rate of 1.1 percent. In June, manufacturing output ticked up 0.1 percent, and the index for mining decreased 0.3 percent. The index for utilities rose 2.8 percent. At 104.0 percent of its 2017 average, total IP in June was 0.7 percent above its year-earlier level. Capacity utilization moved up to 77.6 percent, a rate that is 2.0 percentage points below its long-run (1972–2024) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and close to the level in February 2020 (pre-pandemic).

Capacity utilization at 77.6% is 2.0% below the average from 1972 to 2023. This was above consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production decreased to 104.0. This is above the pre-pandemic level.

Industrial production was above consensus expectations.

MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

by Calculated Risk on 7/16/2025 07:00:00 AM

From the MBA: Mortgage Applications Decrease in Latest MBA Weekly Survey

Mortgage applications decreased 10.0 percent from one week earlier, according to data from the Mortgage Bankers Association’s (MBA) Weekly Mortgage Applications Survey for the week ending July 11, 2025. Last week’s results included an adjustment for the Fourth of July holiday.

The Market Composite Index, a measure of mortgage loan application volume, decreased 10.0 percent on a seasonally adjusted basis from one week earlier. On an unadjusted basis, the Index increased 13 percent compared with the previous week. The Refinance Index decreased 7 percent from the previous week and was 25 percent higher than the same week one year ago. The seasonally adjusted Purchase Index decreased 12 percent from one week earlier. The unadjusted Purchase Index increased 11 percent compared with the previous week and was 13 percent higher than the same week one year ago.

“Treasury yields finished higher last week on average despite an intra-week drop, driven partly by renewed concerns of the impact of tariffs on the economy. As a result, mortgage rates rose after two weeks of declines, which contributed to slower application activity,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. “Jumbo rates were lower than conventional rates for the third straight week, as some depositories may be positioning themselves for growth in balance sheet lending.”

Added Kan, “Purchase applications remained sensitive to both the uncertain economic outlook and the volatility in rates and declined to the slowest pace since May. Refinance applications also dipped because of higher rates, with refinance applications falling, led by VA refinances partially reversing their previous week’s gain, dropping 22 percent.”

...

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($806,500 or less) increased to 6.82 percent from 6.77 percent, with points remaining unchanged at 0.62 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans.

emphasis added

Click on graph for larger image.

Click on graph for larger image.The first graph shows the MBA mortgage purchase index.

According to the MBA, purchase activity is up 13% year-over-year unadjusted.

Red is a four-week average (blue is weekly).

Purchase application activity is still depressed, but above the lows of October 2023 and slightly above the lowest levels during the housing bust.

The second graph shows the refinance index since 1990.

The refinance index decreased and remains very low.

Tuesday, July 15, 2025

Wednesday: PPI, Industrial Production, Beige Book

by Calculated Risk on 7/15/2025 07:14:00 PM

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Note: Mortgage rates are from MortgageNewsDaily.com and are for top tier scenarios.

Wednesday:

• At 7:00 AM ET, The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

• At 8:30 AM, The Producer Price Index for June from the BLS. The consensus is for a 0.2% increase in PPI, and a 0.2% increase in core PPI.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for June. The consensus is for a 0.1% increase in Industrial Production, and for Capacity Utilization to be unchanged at 77.4%.

• At 2:00 PM, the Federal Reserve Beige Book, an informal review by the Federal Reserve Banks of current economic conditions in their Districts.

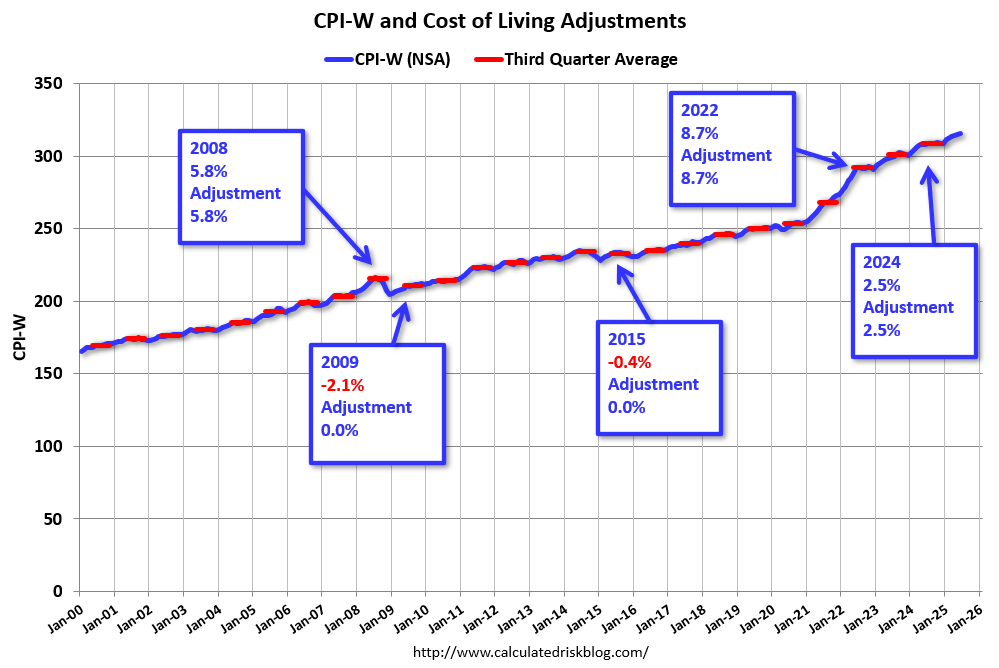

An Early Look at 2026 Cost-Of-Living Adjustments and Maximum Contribution Base

by Calculated Risk on 7/15/2025 04:06:00 PM

The BLS reported earlier today:

The Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W) increased 2.6 percent over the last 12 months to an index level of 315.945 (1982-84=100). For the month, the index increased 0.4 percent prior to seasonal adjustment.CPI-W is the index that is used to calculate the Cost-Of-Living Adjustments (COLA). The calculation dates have changed over time (see Cost-of-Living Adjustments), but the current calculation uses the average CPI-W for the three months in Q3 (July, August, September) and compares to the average for the highest previous average of Q3 months. Note: this is not the headline CPI-U and is not seasonally adjusted (NSA).

• In 2024, the Q3 average of CPI-W was 308.729.

The 2024 Q3 average was the highest Q3 average, so we only have to compare Q3 this year to last year.

Click on graph for larger image.

Click on graph for larger image.This graph shows CPI-W since January 2000. The red lines are the Q3 average of CPI-W for each year.

Note: The year labeled is for the calculation, and the adjustment is effective for December of that year (received by beneficiaries in January of the following year).

CPI-W was up 2.6% year-over-year in June (up from 2.2% YoY in May), and although this is very early - we need the data for July, August and September - my early guess is COLA will probably be in 3% range this year, up from 2.5% in 2025.

Contribution and Benefit Base

The contribution base will be adjusted using the National Average Wage Index. This is based on a one-year lag. The National Average Wage Index is not available for 2024 yet, although we know wages increased solidly in 2024. If wages increased 5% in 2024, then the contribution base next year will increase to around $185,000 in 2026, from the current $176,100.

Remember - this is a very early look. What matters is average CPI-W, NSA, for all three months in Q3 (July, August and September).

Cleveland Fed: Median CPI increased 0.2% and Trimmed-mean CPI increased 0.3% in June

by Calculated Risk on 7/15/2025 11:14:00 AM

The Cleveland Fed released the median CPI and the trimmed-mean CPI.

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% in May. The 16% trimmed-mean Consumer Price Index increased 0.3%. "The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report".

Click on graph for larger image.

Click on graph for larger image.

This graph shows the year-over-year change for these four key measures of inflation.

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% in May. The 16% trimmed-mean Consumer Price Index increased 0.3%. "The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report".

Click on graph for larger image.

Click on graph for larger image.This graph shows the year-over-year change for these four key measures of inflation.

On a year-over-year basis, the median CPI rose 3.6% (up from 3.5% YoY in May), the trimmed-mean CPI rose 3.2% (up from 3.0%), and the CPI less food and energy rose 2.9% (up from 2.8%).

Core PCE is for May was up 2.7% YoY, up from 2.5% in April.

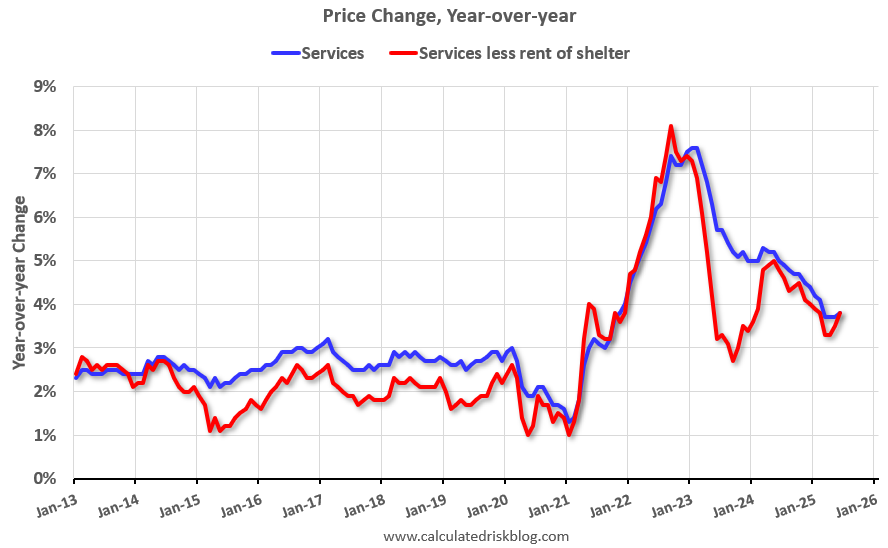

YoY Measures of Inflation: Services, Goods and Shelter

by Calculated Risk on 7/15/2025 08:49:00 AM

Here are a few measures of inflation:

The first graph is the one Fed Chair Powell had mentioned two years ago when services less rent of shelter was up around 8% year-over-year. This declined and is now up 3.8% YoY.

Click on graph for larger image.

Click on graph for larger image.

This graph shows the YoY price change for Services and Services less rent of shelter through June 2025.

Services were up 3.8% YoY as of June 2025, up from 3.7% YoY in May.

Services less rent of shelter was up 3.8% YoY in June, up from 3.5% YoY in April.

Services less rent of shelter was up 3.8% YoY in June, up from 3.5% YoY in April.

The second graph shows that goods prices started to increase year-over-year (YoY) in 2020 and accelerated in 2021 due to both strong demand and supply chain disruptions.

The second graph shows that goods prices started to increase year-over-year (YoY) in 2020 and accelerated in 2021 due to both strong demand and supply chain disruptions.Durables were up 0.6% YoY as of June 2025, up from unchanged YoY in May.

Commodities less food and energy commodities were at 0.6% YoY in June, up from 0.3% YoY in May.

Commodities less food and energy commodities were at 0.6% YoY in June, up from 0.3% YoY in May.

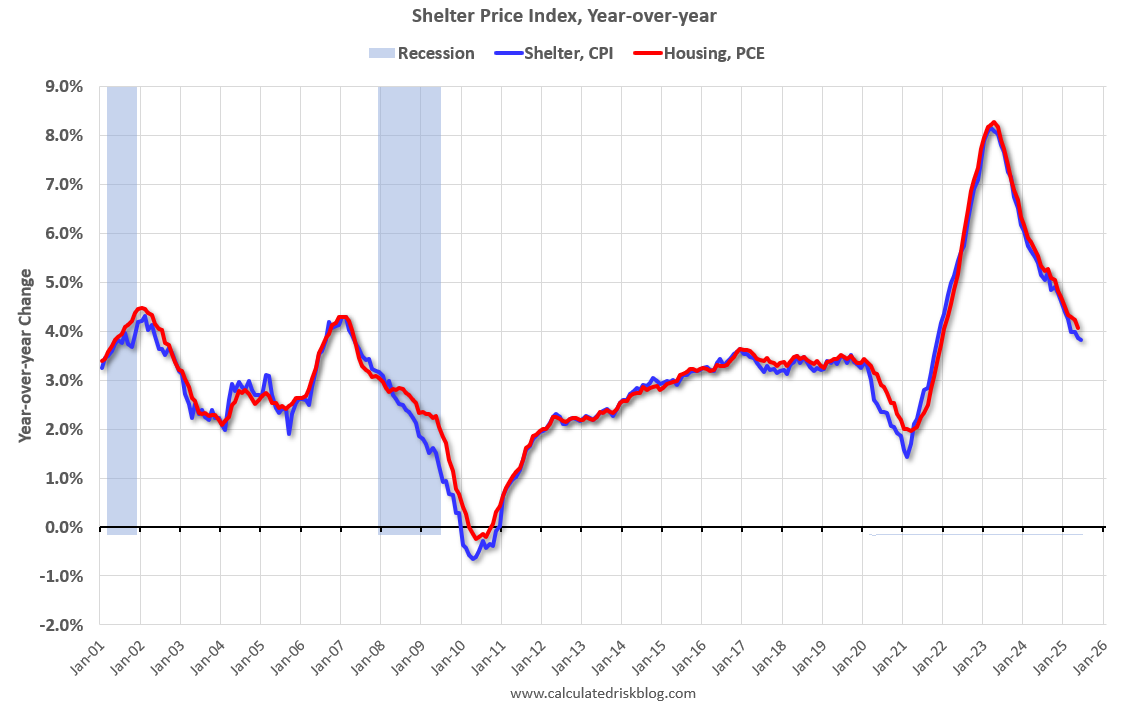

Here is a graph of the year-over-year change in shelter from the CPI report (through June) and housing from the PCE report (through May)

Here is a graph of the year-over-year change in shelter from the CPI report (through June) and housing from the PCE report (through May)Shelter was up 3.8% year-over-year in June, down from 3.9% in May. Housing (PCE) was up 4.1% YoY in June, down from 4.2% in May.

This is still catching up with private new lease data (this includes renewals whereas private data is mostly for new leases).

Core CPI ex-shelter was up 2.1% YoY in June, up from 1.9% in May.

BLS: CPI Increased 0.3% in June; Core CPI increased 0.2%

by Calculated Risk on 7/15/2025 08:30:00 AM

The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3 percent on a seasonally adjusted basis in June, after rising 0.1 percent in May, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 2.7 percent before seasonal adjustment.The change in CPI was close to expectations. I'll post a graph later today after the Cleveland Fed releases the median and trimmed-mean CPI.

The index for shelter rose 0.2 percent in June and was the primary factor in the all items monthly increase. The energy index rose 0.9 percent in June as the gasoline index increased 1.0 percent over the month. The index for food increased 0.3 percent as the index for food at home rose 0.3 percent and the index for food away from home rose 0.4 percent in June.

The index for all items less food and energy rose 0.2 percent in June, following a 0.1-percent increase in May. Indexes that increased over the month include household furnishings and operations, medical care, recreation, apparel, and personal care. The indexes for used cars and trucks, new vehicles, and airline fares were among the major indexes that decreased in June.

The all items index rose 2.7 percent for the 12 months ending June, after rising 2.4 percent over the 12 months ending May. The all items less food and energy index rose 2.9 percent over the last 12 months. The energy index decreased 0.8 percent for the 12 months ending June. The food index increased 3.0 percent over the last year.

emphasis added

Monday, July 14, 2025

Tuesday: CPI, NY Fed Mfg

by Calculated Risk on 7/14/2025 07:43:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Just a Hair Higher Ahead of Important Inflation Report

From Matthew Graham at Mortgage News Daily: Mortgage Rates Just a Hair Higher Ahead of Important Inflation Report

Today's movement in mortgage rates, in and of itself, is barely worth mentioning. The average lender remains close enough to Friday's levels but is technically just a hair higher. That fact is offset by the counterpoint that most of the past two months saw higher rates.Tuesday:

The future is far more interesting than the present--specifically, the immediate future. Tomorrow morning brings the release of the Consumer Price Index (CPI). This is one of the most important economic reports as far as interest rates are concerned and tomorrow's example is especially notable.

This CPI marks the first major opportunity for the official data to show (or not show) a meaningful impact on inflation from tariffs.[30 year fixed 6.83%]

emphasis added

• At 8:30 AM ET, The Consumer Price Index for June from the BLS. The consensus is for a 0.3% increase in CPI, and a 0.3% increase in core CPI. The consensus is for CPI to be up 2.6% year-over-year and core CPI to be up 2.9% YoY.

• Also at 8:30 AM, The New York Fed Empire State manufacturing survey for July. The consensus is for a reading of -10.1, up from -16.0.

CPI Preview

by Calculated Risk on 7/14/2025 02:31:00 PM

The Consumer Price Index for May is scheduled to be released tomorrow. The Consumer Price Index for June from the BLS. The consensus is for a 0.3% increase in CPI, and a 0.3% increase in core CPI. The consensus is for CPI to be up 2.6% year-over-year and core CPI to be up 2.9% YoY.

From Goldman Sachs economists:

We expect a 0.23% increase in June core CPI (vs. +0.3% consensus), corresponding to a year-over-year rate of 2.93% (vs. +3.0% consensus). We expect a 0.30% increase in headline CPI (vs. +0.3% consensus), reflecting higher food prices (+0.25%) and energy prices (+1.2%).From BofA:

...

Going forward, tariffs will likely provide a somewhat larger boost to monthly inflation, and we expect monthly core CPI inflation between 0.3-0.4% over the next few months.

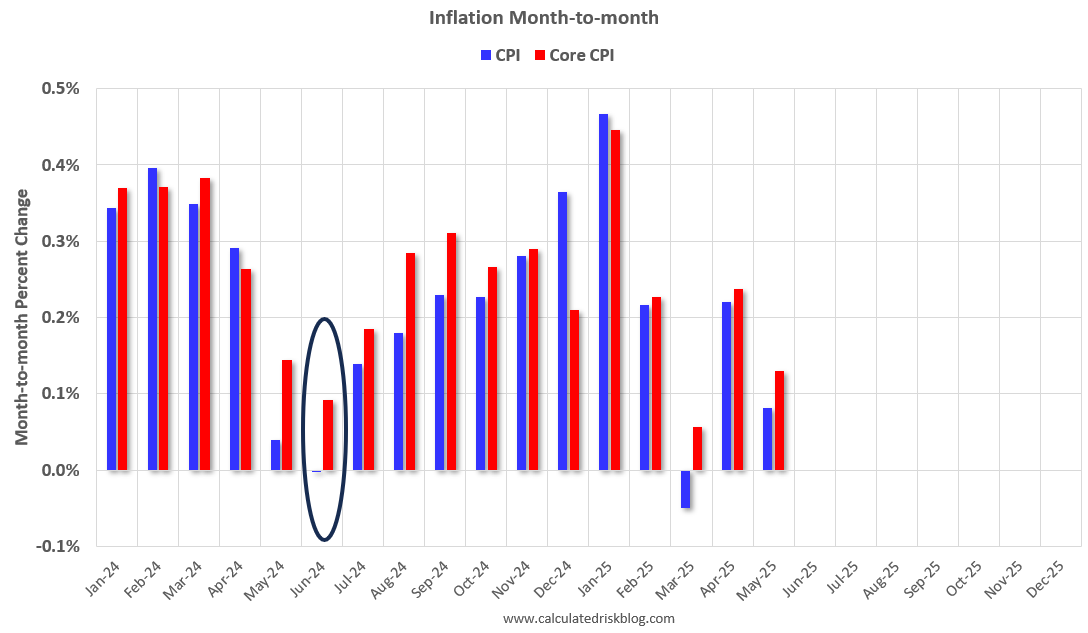

We forecast headline and core CPI to print at 0.3% m/m in June, which would be a notable acceleration from the recent trend. Stronger price hikes for core goods, discretionary services, and medical services should drive the pickup in core inflation. Based on our forecast, we project core PCE to print at 0.22% m/m in June, which would lower the likelihood of a September cut.Note that month-to-month inflation was soft in May and June 2024.

Click on graph for larger image.

Click on graph for larger image.This graph shows the month-to-month change in both headline and core inflation since January 2024.

The circled area is the change for last when inflation was soft. CPI was down fractionally in June 2024, and core CPI was up 0.09%.

So even a somewhat benign reading in June will push up year-over-year inflation.

Starting in July, the tariff related inflation is expected to kick in.

Will House Prices Decline Nationally in 2025?

by Calculated Risk on 7/14/2025 11:26:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Will House Prices Decline Nationally in 2025?

A brief excerpt:

Most forecasts for 2025 were for U.S. house prices to increase modestly in the 3% to 4% range. My early view was “mostly flat prices nationally in 2025” with some areas seeing price declines. I didn’t expect either a crash in prices or a surge in prices.There is much more in the article.

With inventory increasing, year-over-year (YoY) price growth has slowed nationally, and declining in many areas. The following table shows the YoY price slowdown. Note that the median price is impacted by the mix of homes sold.

The seasonally adjusted Case-Shiller National Index is essentially unchanged year-to-date (YTD). The index was at 327.81 in December 2024 and was at 327.90 in the April report.

And the Freddie Mac HPI SA is down slightly YTD. The index was at 299.29 in December, and is now at 297.69, a decline of 0.5%.

Other measures are also indicating a slowdown in the YoY growth, but not a collapse in prices.