RSS Feed

RSS Feed by Calculated Risk on 6/17/2025 12:18:00 PM

Tuesday, June 17, 2025

Housing Market Index and Single Family Starts

Today, in the Calculated Risk Real Estate Newsletter: Housing Market Index and Single Family Starts

A brief excerpt:

This morning, the National Association of Home Builders (NAHB) released their monthly housing market index: Builder Sentiment at Third Lowest Reading Since 2012There is much more in the article.

...

There are several negatives for new home builders now. The NAHB lists the following: rising inventory levels (this is true for both new homes and existing homes that compete with new homes), price declines for existing home sales in a “growing number of markets”, buyer hesitancy due to “elevated mortgage rates and tariff and economic uncertainty”.

In addition, margins are being squeezed by rising costs (both material and labor), and price cuts. This will be a difficult period for homebuilders.

The following graph shows the NAHB HMI and single family starts since 1985.

NAHB: "Builder Sentiment at Third Lowest Reading Since 2012" in June

by Calculated Risk on 6/17/2025 10:00:00 AM

The National Association of Home Builders (NAHB) reported the housing market index (HMI) was at 32, down from 34 last month. Any number below 50 indicates that more builders view sales conditions as poor than good.

From the NAHB: Builder Sentiment at Third Lowest Reading Since 2012

In a further sign of declining builder sentiment, the use of price incentives increased sharply in June as the housing market continues to soften.

Builder confidence in the market for newly built single-family homes was 32 in June, down two points from May, according to the National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) released today. The index has only posted a lower reading twice since 2012 – in December 2022 when it hit 31 and in April 2020 at the start of the pandemic when it plunged more than 40 points to 30.

“Buyers are increasingly moving to the sidelines due to elevated mortgage rates and tariff and economic uncertainty,” said NAHB Chairman Buddy Hughes, a home builder and developer from Lexington, N.C. “To help address affordability concerns and bring hesitant buyers off the fence, a growing number of builders are moving to cut prices.”

Indeed, the latest HMI survey also revealed that 37% of builders reported cutting prices in June, the highest percentage since NAHB began tracking this figure on a monthly basis in 2022. This compares with 34% of builders who reported cutting prices in May and 29% in April. Meanwhile, the average price reduction was 5% in June, the same as it’s been every month since last November. The use of sales incentives was 62% in June, up one percentage point from May.

“Rising inventory levels and prospective home buyers who are on hold waiting for affordability conditions to improve are resulting in weakening price growth in most markets and generating price declines for resales in a growing number of markets,” said NAHB Chief Economist Robert Dietz. “Given current market conditions, NAHB is forecasting a decline in single-family starts for 2025.”

...

All three of the major HMI indices posted losses in June. The HMI index gauging current sales conditions fell two points in June to a level of 35, the component measuring sales expectations in the next six months dropped two points lower to 40 while the gauge charting traffic of prospective buyers posted a two-point decline to 21, the lowest reading since November 2023.

Looking at the three-month moving averages for regional HMI scores, the Northeast fell one point to 43, the Midwest moved one point higher to 41, the South dropped three points to 33 and the West declined four points to 28.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the NAHB index since Jan 1985.

This was well below the consensus forecast.

Industrial Production Decreased 0.2% in May

by Calculated Risk on 6/17/2025 09:15:00 AM

From the Fed: Industrial Production and Capacity Utilization

Industrial production (IP) fell 0.2 percent in May after increasing 0.1 percent in April. Manufacturing output ticked up 0.1 percent in May, driven by a gain of 4.9 percent in the index for motor vehicles and parts; the index for manufacturing excluding motor vehicles and parts fell 0.3 percent. The index for mining increased 0.1 percent, and the index for utilities decreased 2.9 percent. At 103.6 percent of its 2017 average, total IP in May was 0.6 percent above its year-earlier level. Capacity utilization moved down to 77.4 percent, a rate that is 2.2 percentage points below its long-run (1972–2024) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up from the record low set in April 2020, and close to the level in February 2020 (pre-pandemic).

Capacity utilization at 77.4% is 2.2% below the average from 1972 to 2023. This was below consensus expectations.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production decreased to 103.6. This is above the pre-pandemic level.

Industrial production was below consensus expectations and the previous months were revised down.

Retail Sales Decreased 0.9% in May

by Calculated Risk on 6/17/2025 08:30:00 AM

On a monthly basis, retail sales decreased 0.9% from April to May (seasonally adjusted), and sales were up 3.3 percent from May 2024.

From the Census Bureau report:

Advance estimates of U.S. retail and food services sales for May 2025, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $715.4 billion, down 0.9 percent from the previous month, and up 3.3 percent rom May 2024. ... The March 2025 to April 2025 percent change was revised from up 0.1 percent to down 0.1 percent.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline was down 0.8% in May.

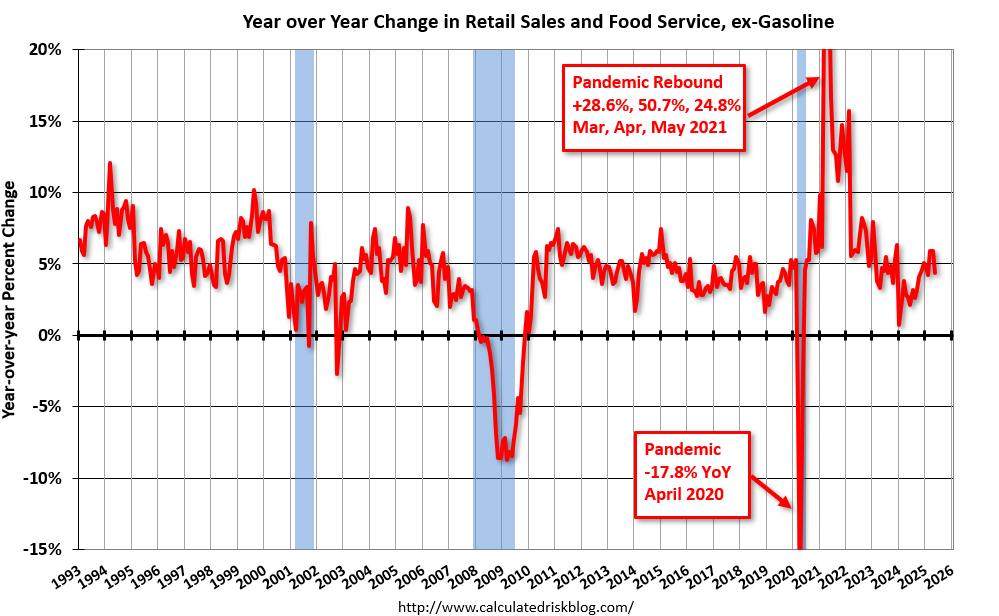

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail and Food service sales, ex-gasoline, increased by 4.4% on a YoY basis.

The change in sales in May were below expectations and the previous two months were revised down.

The change in sales in May were below expectations and the previous two months were revised down.A weak report.

Monday, June 16, 2025

Tuesday: Retail Sales, Industrial Production, Homebuilder Survey

by Calculated Risk on 6/16/2025 07:11:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Drift Slightly Higher to Start The Week

From Matthew Graham at Mortgage News Daily: Mortgage Rates Drift Slightly Higher to Start The Week

While there's been no shortage of political and geopolitical headlines over the past 2 business days, there hasn't been much by way of inspiration for the bond market. Bonds (and, thus, rates) have moved nonetheless.Tuesday:

...

Tomorrow's Retail Sales data is capable of causing volatility in either direction, depending on the outcome. Then on Wednesday, we'll hear from the Fed. While they will not be cutting rates at this meeting, they will be updating their rate outlook--something that frequently gets the market's attention. [30 year fixed 6.91%]

emphasis added

• At 8:30 AM ET, Retail sales for May is scheduled to be released. The consensus is for a 0.5% decrease in retail sales.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for May. The consensus is for a 0.1% increase in Industrial Production, and for Capacity Utilization to be unchanged at 77.7%.

• At 10:00 AM, The June NAHB homebuilder survey. The consensus is for a reading of 36, up from 34 last month. Any number below 50 indicates that more builders view sales conditions as poor than good.

3rd Look at Local Housing Markets in May

by Calculated Risk on 6/16/2025 10:49:00 AM

Today, in the Calculated Risk Real Estate Newsletter: 3rd Look at Local Housing Markets in May

A brief excerpt:

The NAR is scheduled to release May existing home sales on Monday, June 23rd at 10:00 AM. Housing economist Tom Lawler expects the NAR to report sales at a seasonally adjusted annual rate (SAAR) of 4.03 million for May, up slightly from April and down slightly year-over-year.There is much more in the article.

...

In May, sales in these markets were down 4.3% YoY. Last month, in April, these same markets were down 3.4% year-over-year Not Seasonally Adjusted (NSA).

Important: There were fewer working days in May 2025 (21) as in May 2024 (22). So, the year-over-year change in the headline SA data will be higher than for the NSA data.

...

More local markets to come!

Housing June 16th Weekly Update: Inventory up 2.1% Week-over-week, Up 33.1% Year-over-year

by Calculated Risk on 6/16/2025 08:11:00 AM

Altos reports that active single-family inventory was up 2.1% week-over-week.

Inventory is now up 32.2% from the seasonal bottom in January and is increasing.

Usually, inventory is up about 18% from the seasonal low by this week in the year. So, 2025 is seeing a larger than normal pickup in inventory.

The first graph shows the seasonal pattern for active single-family inventory since 2015.

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025. The black line is for 2019.

Inventory was up 33.1% compared to the same week in 2024 (last week it was up 32.2%), and down 12.4% compared to the same week in 2019 (last week it was down 13.0%).

This is the highest level since 2019.

It now appears inventory will be close to 2019 levels towards the end of 2025.

This second inventory graph is courtesy of Altos Research.

This second inventory graph is courtesy of Altos Research.

As of June 13th, inventory was at 826 thousand (7-day average), compared to 809 thousand the prior week.

Mike Simonsen discusses this data regularly on Youtube

Sunday, June 15, 2025

Sunday Night Futures

by Calculated Risk on 6/15/2025 06:24:00 PM

Weekend:

• Schedule for Week of June 15, 2025

Monday:

• At 8:30 AM ET, The New York Fed Empire State manufacturing survey for June. The consensus is for a reading of -6.0, up from -9.2.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 are down 17 and DOW futures are down 134 (fair value).

Oil prices were up over the last week with WTI futures at $75.49 per barrel and Brent at $76.72 per barrel. A year ago, WTI was at $79, and Brent was at $81 - so WTI oil prices are down about 4% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.09 per gallon. A year ago, prices were at $3.43 per gallon, so gasoline prices are down $0.34 year-over-year.

FOMC Preview: No Change to Fed Funds Rate

by Calculated Risk on 6/15/2025 09:31:00 AM

Most analysts expect no change to FOMC policy at the meeting this week, keeping the target range at 4 1/4 to 4 1/2 percent. Market participants currently expect the FOMC to also be on hold at the July meeting, with the next rate cut in September, and a second rate cut in December.

From BofA:

The Fed has made it clear that the policy rate will remain unchanged at its June meeting. We expect the FOMC to make some changes to the language around uncertainty in the statement. The May statement said that “Uncertainty about the economic outlook has increased further”. Given the 115pp reduction in bilateral US-China tariffs on May 12, we think a more appropriate characterization could be: “Uncertainty about the economic outlook remains elevated”.From Goldman:

Per the usual, markets will be focused on the Summary of Economic Projections (SEP). The March SEP was pre-“Liberation Day”. Therefore, meaningful revisions to the 2025 forecasts are likely. However, we think there is too much uncertainty around policy along multiple dimensions (most notably trade and fiscal) for the Fed to do a wholesale reassessment of its views. So we think the forecasts for 2026 and beyond will remain largely unchanged.

emphasis added

We are not making any changes to our Fed forecast and continue to expect the first of three normalization cuts in December, followed by two more in 2026 to a terminal rate of 3.5-3.75%. An earlier cut is possible if the economy deteriorates more than we expect or if inflation continues to surprise to the downside, but we think that the peak summer tariff effects on the monthly inflation prints will most likely be too fresh for the FOMC to cut before December.

Projections will be released at this meeting. For review, here are the March projections.

1 Projections of change in real GDP and inflation are from the fourth quarter of the previous year to the fourth quarter of the year indicated.

The unemployment rate was at 4.2% in May after averaging 4.1% for Q1. The forecast for the Q4 unemployment rate is likely low.

2 Projections for the unemployment rate are for the average civilian unemployment rate in the fourth quarter of the year indicated.

As of April 2025, PCE inflation increased 2.1 percent year-over-year (YoY). There will likely be some increase in PCE inflation from policy, but this appears to in the forecast range.

PCE core inflation increased 2.5 percent YoY in April. This is in the range of FOMC projections for Q4.

The FOMC participants’ midpoint of the target level for the federal funds rate is now at 4.0% at the end of 2025 (3.9%-4.4%) and the long run range is 2.6% to 3.6%. This is fewer rate cuts than market participants expect.

Since the last projections were released, economic growth has been below expectations (but distorted), the unemployment rate was close to expectations, and inflation at expectations.

The BEA's advance estimate for Q1 GDP showed real growth at -0.2% annualized. There is a wide range of estimates for Q2 GDP, but it is forecast to be over 3.0% (as Q1 distortions reverse). That would put real growth on pace to be in the range of the March FOMC projections for Q4 over Q4.

However, Q2, Q3 and Q4 all saw solid growth last year - and we haven't seen the impact of policy changes on hard data yet - so there is still significant uncertainty about the economy this year.

| GDP projections of Federal Reserve Governors and Reserve Bank presidents, Change in Real GDP1 | ||||

|---|---|---|---|---|

| Projection Date | 2025 | 2026 | 2027 | |

| Mar 2025 | 1.5 to 1.9 | 1.6 to 1.9 | 1.6 to 2.0 | |

| Dec 2024 | 1.8 to 2.2 | 1.9 to 2.1 | 1.8 to 2.0 | |

The unemployment rate was at 4.2% in May after averaging 4.1% for Q1. The forecast for the Q4 unemployment rate is likely low.

| Unemployment projections of Federal Reserve Governors and Reserve Bank presidents, Unemployment Rate2 | ||||

|---|---|---|---|---|

| Projection Date | 2025 | 2026 | 2027 | |

| Mar 2025 | 4.3 to 4.4 | 4.2 to 4.5 | 4.1 to 4.4 | |

| Dec 2024 | 4.2 to 4.5 | 4.1 to 4.4 | 4.0 to 4.4 | |

As of April 2025, PCE inflation increased 2.1 percent year-over-year (YoY). There will likely be some increase in PCE inflation from policy, but this appears to in the forecast range.

Without policy changes (tariffs) it appears inflation would be well below the FOMC forecast!

| Inflation projections of Federal Reserve Governors and Reserve Bank presidents, PCE Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2025 | 2026 | 2027 | |

| Mar 2025 | 2.6 to 2.9 | 2.1 to 2.3 | 2.0 to 2.1 | |

| Dec 2024 | 2.3 to 2.6 | 2.0-2.2 | 2.0 | |

PCE core inflation increased 2.5 percent YoY in April. This is in the range of FOMC projections for Q4.

| Core Inflation projections of Federal Reserve Governors and Reserve Bank presidents, Core Inflation1 | ||||

|---|---|---|---|---|

| Projection Date | 2025 | 2026 | 2027 | |

| Mar 2025 | 2.7 to 3.0 | 2.1 to 2.4 | 2.0 to 2.1 | |

| Dec 2024 | 2.5 to 2.7 | 2.0-2.3 | 2.0 | |

Saturday, June 14, 2025

Real Estate Newsletter Articles this Week: Total Mortgage Equity Withdrawal (MEW) was Negative in Q1

by Calculated Risk on 6/14/2025 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Lawler: Early Read on Existing Home Sales in May

• Part 1: Current State of the Housing Market; Overview for mid-June 2025

• Part 2: Current State of the Housing Market; Overview for mid-June 2025

• The "Home ATM" Mostly Closed in Q1

• 2nd Look at Local Housing Markets in May

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.