RSS Feed

RSS Feed by Calculated Risk on 1/06/2026 08:11:00 AM

Tuesday, January 06, 2026

ICE: "Annual home price growth ended 2025 at just +0.7%"

The ICE Home Price Index (HPI) is a repeat sales index. ICE reports the median price change of the repeat sales.

From ICE (Intercontinental Exchange):

Annual home price growth ended 2025 at just +0.7% — the smallest calendar-year increase since 2011, when prices fell by 2.9%.As ICE mentioned, "regional trends ... show significant variation". The Northeast and Midwest are saw solid house price gains in 2025, whereas cities in the South and West have been leading the way in inventory increases and price declines (especially Florida and Texas).

With income growth outpacing home price gains and 30-year mortgage rates starting 2026 at 6.15%, housing affordability is at its best level in nearly four years.

At current prices and rates, purchasing an average-priced home with 20% down and a 30-year loan requires a monthly payment of $2,093 — 27.8% of median household income. That’s down from $2,256 (31.1%) at the start of 2025.

According to Andy Walden, Head of Mortgage and Housing Market Research for Intercontinental Exchange:

“Improved affordability and income growth have provided a much-needed boost to housing market dynamics, even as regional trends and property types show significant variation. The Northeast and Midwest have emerged as clear leaders, while condos continue to face headwinds in most markets.”

Drilling down into regional and property type specifics:

• Regional Standouts: New Haven, CT led all markets with an impressive 8.6% price growth, followed by Syracuse, NY (+6.8%) and Hartford, CT (+6.25%). Notably, 24 of the 25 fastest-appreciating markets were in the Northeast and Midwest.

• Price Declines: On the flip side, 35 of the 100 largest U.S. markets saw home prices decline in 2025 — up from just 10 in 2024 and marking the largest share of declines since 2011.

• Property Type Trends: Single-family homes outperformed condos, with prices rising 1.0% compared to a 1.7% decline for condos. Condos underperformed in 90% of markets nationwide.

Monday, January 05, 2026

"Mortgage Rates Holding at 2-Month Low"

by Calculated Risk on 1/05/2026 07:53:00 PM

From Matthew Graham at Mortgage News Daily: Mortgage Rates Holding at 2-Month Low Excerpt:

From Matthew Graham at Mortgage News Daily: Mortgage Rates Holding at 2-Month Low Excerpt:

Bottom line: at current levels, any day that rates spend holding steady or moving microscopically lower will technically result in the lowest rates since October 28th. It would take a more noticeable improvement to break below that floor. When and if that happens, rates will be the lowest since early 2023.[30 year fixed 6.19%]Tuesday:

emphasis added

• No major economic releases scheduled.

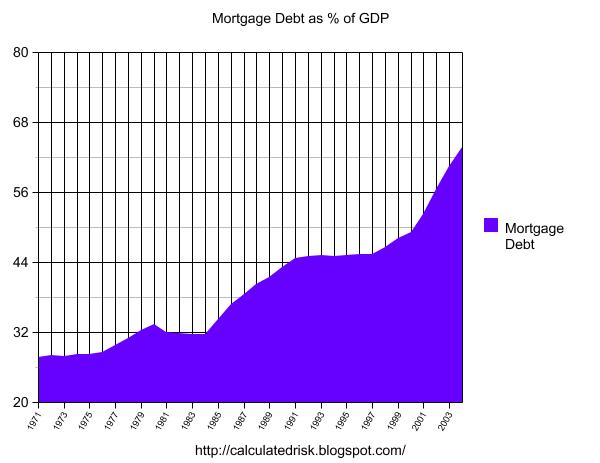

Update: The Housing Bubble and Mortgage Debt as a Percent of GDP

by Calculated Risk on 1/05/2026 02:51:00 PM

Today, in the Calculated Risk Real Estate Newsletter: Update: The Housing Bubble and Mortgage Debt as a Percent of GDP

A brief excerpt:

Three years ago, I wrote The Housing Bubble and Mortgage Debt as a Percent of GDP. Here is an update to a couple of graphs. The bottom line remains the same: There will not be cascading price declines in this cycle due to distressed sales.There is much more in the article.

In a 2005 post, I included a graph of household mortgage debt as a percent of GDP. Several readers asked if I could update the graph.

First, from February 2005 (21 years ago!):The following chart shows household mortgage debt as a % of GDP. Although mortgage debt has been increasing for years, the last four years have seen a tremendous increase in debt. Last year alone mortgage debt increased close to $800 Billion - almost 7% of GDP. ...And a serious problem is what happened!

Many homeowners have refinanced their homes, in essence using their homes as an ATM.

It wouldn't take a RE bust to impact the general economy. Just a slowdown in both volume (to impact employment) and in prices (to slow down borrowing) might push the general economy into recession. An actual bust, especially with all of the extensive sub-prime lending, might cause a serious problem.

ISM® Manufacturing index Decreased to 47.9% in December; "Lowest Reading of 2025"

by Calculated Risk on 1/05/2026 10:00:00 AM

(Posted with permission). The ISM manufacturing index indicated contraction. The PMI® was at 47.9% in December, down from 48.2% in November. The employment index was at 44.9%, up from 44.0% the previous month, and the new orders index was at 47.7%, up from 47.4%.

From ISM: Manufacturing PMI® at 47.9%

December 2025 ISM® Manufacturing PMI® Report

Economic activity in the manufacturing sector contracted in December for the 10th consecutive month, following a two-month expansion preceded by 26 straight months of contraction, say the nation’s supply executives in the latest ISM® Manufacturing PMI® Report.This suggests manufacturing contracted for the tenth consecutive month in December. This was below the consensus forecast, and employment was very weak and prices very strong.

The report was issued today by Susan Spence, MBA, Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee.

“The Manufacturing PMI® registered 47.9 percent in December, a 0.3-percentage point decrease compared to the reading of 48.2 percent in November and the lowest reading of 2025. The overall economy continued in expansion for the 68th month after one month of contraction in April 2020. (A Manufacturing PMI® above 42.3 percent, over a period of time, generally indicates an expansion of the overall economy.) The New Orders Index contracted for a fourth straight month in December following one month of growth; the figure of 47.7 percent is 0.3 percentage point higher than the 47.4 percent recorded in November. The December reading of the Production Index (51 percent) is 0.4 percentage point lower than November’s figure of 51.4 percent. The Prices Index remained in expansion (or ‘increasing’ territory), registering 58.5 percent, the same as November’s reading. The Backlog of Orders Index registered 45.8 percent, up 1.8 percentage points compared to the 44 percent recorded in November. The Employment Index registered 44.9 percent, up 0.9 percentage point from November’s figure of 44 percent.

emphasis added

Housing January 5th Weekly Update: Inventory Down 2.2% Week-over-week

by Calculated Risk on 1/05/2026 08:11:00 AM

Altos reports that active single-family inventory was down 2.2% week-over-week.

Note that Inventory usually bottoms seasonally in January or February.

The first graph shows the seasonal pattern for active single-family inventory since 2015.

Click on graph for larger image.

Click on graph for larger image.The red line is for 2025. The black line is for 2019.

Inventory was up 13.3% compared to the same week in 2025 (last week it was up 13.1%), and down 6.0% compared to the same week in 2019 (last week it was down 11.8%).

Inventory started 2026 down almost 12% compared to 2019.

This second inventory graph is courtesy of Altos Research.

This second inventory graph is courtesy of Altos Research.

As of January 2nd, inventory was at 720 thousand (7-day average), compared to 736 thousand the prior week.

Mike Simonsen discusses this data and much more regularly on YouTube

Sunday, January 04, 2026

Sunday Night Futures

by Calculated Risk on 1/04/2026 06:13:00 PM

Weekend:

• Schedule for Week of January 4, 2026

Monday:

• Early, Light vehicle sales for December. The consensus is for 15.5 million SAAR in December, down from 15.6 million SAAR in November (Seasonally Adjusted Annual Rate).

• At 10:00 AM ET, ISM Manufacturing Index for December. The consensus is for 48.3%, up from 48.2%.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are mostly unchanged (fair value).

Oil prices were moxed over the last week with WTI futures at $57.32 per barrel and Brent at $60.75 per barrel. A year ago, WTI was at $75, and Brent was at $77 - so WTI oil prices are down about 24% year-over-year.

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $2.77 per gallon. A year ago, prices were at $3.04 per gallon, so gasoline prices are down $0.27 year-over-year.

Update: Lumber Prices Mostly Unchanged Year-over-year

by Calculated Risk on 1/04/2026 08:12:00 AM

Here is another update on lumber prices.

NOTE: The CME group discontinued the Random Length Lumber Futures contract on May 16, 2023. I switched to a physically-delivered Lumber Futures contract that was started in August 2022. Unfortunately, this impacts long term price comparisons since the new contract was priced about 24% higher than the old random length contract for the period when both contracts were available.

This graph shows CME random length framing futures through August 2022 (blue), and the new physically-delivered Lumber Futures (LBR) contract starting in August 2022 (Red).

On January 2, 2026, LBR was at $534.00 per 1,000 board feet, down 1.6% from a year ago.

Click on graph for larger image.

Click on graph for larger image.There is somewhat of a seasonal demand for lumber, and lumber prices frequently peak in the first half of the year.

The pickup in early 2018 was due to the Trump lumber tariffs in 2017. There were huge increases during the pandemic due to a combination of supply constraints and a pickup in housing starts.

Now, even with the tariffs, prices are mostly unchanged year-over-year suggesting weak demand for framing lumber.

Saturday, January 03, 2026

Real Estate Newsletter Articles this Week: Case-Shiller House Prices up 1.4% YoY

by Calculated Risk on 1/03/2026 02:11:00 PM

At the Calculated Risk Real Estate Newsletter this week:

Click on graph for larger image.

Click on graph for larger image.

• Case-Shiller: National House Price Index Up 1.4% year-over-year in October

• FHFA’s Q3 National Mortgage Database: Outstanding Mortgage Rates, LTV and Credit Scores

• Freddie Mac House Price Index Up 1.0% Year-over-Year in November

• Inflation Adjusted House Prices 2.7% Below 2022 Peak

This is usually published 4 to 6 times a week and provides more in-depth analysis of the housing market.

Schedule for Week of January 4, 2026

by Calculated Risk on 1/03/2026 08:11:00 AM

The key reports this week are the December employment report and Housing Starts for September and October.

Other key indicators include the November Trade Deficit, November Job Openings, December ISM Manufacturing and December Vehicle Sales.

Early: Light vehicle sales for December.

Early: Light vehicle sales for December.The consensus is for 15.5 million SAAR in December, down from 15.6 million SAAR in November (Seasonally Adjusted Annual Rate).

This graph shows light vehicle sales since the BEA started keeping data in 1967.

The dashed line is the current sales rate.

10:00 AM: ISM Manufacturing Index for December. The consensus is for 48.3%, up from 48.2%.

----- Tuesday, January 6th -----

No major economic releases scheduled.

----- Wednesday, January 7th -----

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index. This will be two weeks of data.

8:15 AM: The ADP Employment Report for December. This report is for private payrolls only (no government). The consensus is for 50,000, up from -32,000 jobs added in November.

10:00 AM ET: Job Openings and Labor Turnover Survey for November from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for November from the BLS.

This graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings increased in October to 7.67 million from 7.66 million in September.

10:00 AM: the ISM Services Index for December.

----- Thursday, January 8th -----

8:30 AM: Trade Balance report for November from the Census Bureau.

8:30 AM: Trade Balance report for November from the Census Bureau.

This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $59.4 billion. The U.S. trade deficit was at $52.8 billion in September.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 205K, up from 199K.

----- Friday, January 9th -----

8:30 AM: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.

8:30 AM: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.

There were 64,000 jobs added in November, and the unemployment rate was at 4.6%.

This graph shows the jobs added per month since January 2021.

10:00 AM: Housing Starts for September and October.

10:00 AM: Housing Starts for September and October.

This graph shows single and total housing starts since 2000.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for January)

12:00 PM: Q3 Flow of Funds Accounts of the United States from the Federal Reserve.

10:00 AM: ISM Manufacturing Index for December. The consensus is for 48.3%, up from 48.2%.

No major economic releases scheduled.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index. This will be two weeks of data.

8:15 AM: The ADP Employment Report for December. This report is for private payrolls only (no government). The consensus is for 50,000, up from -32,000 jobs added in November.

10:00 AM ET: Job Openings and Labor Turnover Survey for November from the BLS.

10:00 AM ET: Job Openings and Labor Turnover Survey for November from the BLS. This graph shows job openings (black line), hires (dark blue), Layoff, Discharges and other (red column), and Quits (light blue column) from the JOLTS.

Jobs openings increased in October to 7.67 million from 7.66 million in September.

10:00 AM: the ISM Services Index for December.

8:30 AM: Trade Balance report for November from the Census Bureau.

8:30 AM: Trade Balance report for November from the Census Bureau. This graph shows the U.S. trade deficit, with and without petroleum, through the most recent report. The blue line is the total deficit, and the black line is the petroleum deficit, and the red line is the trade deficit ex-petroleum products.

The consensus is the trade deficit to be $59.4 billion. The U.S. trade deficit was at $52.8 billion in September.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 205K, up from 199K.

8:30 AM: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.

8:30 AM: Employment Report for December. The consensus is for 55,000 jobs added, and for the unemployment rate to decline to 4.5%.There were 64,000 jobs added in November, and the unemployment rate was at 4.6%.

This graph shows the jobs added per month since January 2021.

10:00 AM: Housing Starts for September and October.

10:00 AM: Housing Starts for September and October. This graph shows single and total housing starts since 2000.

10:00 AM: University of Michigan's Consumer sentiment index (Preliminary for January)

12:00 PM: Q3 Flow of Funds Accounts of the United States from the Federal Reserve.

Friday, January 02, 2026

Inflation Adjusted House Prices 2.7% Below 2022 Peak

by Calculated Risk on 1/02/2026 11:12:00 AM

Today, in the Calculated Risk Real Estate Newsletter: Inflation Adjusted House Prices 2.7% Below 2022 Peak

Excerpt:

It has almost 20 years since the housing bubble peak, ancient history for many readers!There is much more in the article!

In the October Case-Shiller house price index released Tuesday, the seasonally adjusted National Index (SA), was reported as being 78% above the bubble peak. However, in real terms, the National index (SA) is about 9.7% above the bubble peak (and historically there has been an upward slope to real house prices). The composite 20, in real terms, is 1.1% above the bubble peak.

...

People usually graph nominal house prices, but it is also important to look at prices in real terms. As an example, if a house price was $300,000 in January 2010, the price would be $448,000 today adjusted for inflation (49% increase). That is why the second graph below is important - this shows "real" prices.br />

The third graph shows the price-to-rent ratio, and the fourth graph is the affordability index. The last graph shows the 5-year real return based on the Case-Shiller National Index.

...

The second graph shows the same two indexes in real terms (adjusted for inflation using CPI).

In real terms (using CPI), the National index is 2.7% below the recent peak, and the Composite 20 index is 3.0% below the recent peak in 2022.

Both the real National index and the Comp-20 index increased in October. This was the first increase in the real National index has in 10 months.

It has now been 41 months since the real peak in house prices. Typically, after a sharp increase in prices, it takes a number of years for real prices to reach new highs (see House Prices: 7 Years in Purgatory)