RSS Feed

RSS Feed by Calculated Risk on 5/23/2021 07:00:00 PM

Sunday, May 23, 2021

Sunday Night Futures

Weekend:

• Schedule for Week of May 23, 2021

Monday:

• At 8:30 AM ET, Chicago Fed National Activity Index for April. This is a composite index of other data.

From CNBC: Pre-Market Data and Bloomberg futures S&P 500 and DOW futures are mostly unchanged (fair value).

Oil prices were down over the last week with WTI futures at $63.73 per barrel and Brent at $66.55 per barrel. A year ago, WTI was at $33, and Brent was at $34 - so WTI oil prices are UP almost double year-over-year (oil prices collapsed at the beginning of the pandemic).

Here is a graph from Gasbuddy.com for nationwide gasoline prices. Nationally prices are at $3.03 per gallon. A year ago prices were at $1.95 per gallon, so gasoline prices are up $1.08 per gallon year-over-year.

May 23rd COVID-19 New Cases, Hospitalizations, Vaccinations

by Calculated Risk on 5/23/2021 04:27:00 PM

From Dr. Bob Wachter, Chair, UCSF Dept of Medicine today:

In case anyone cares, I've started eating indoors in SF restaurants. It wasn't any one thing; the risk just fell below my personal threshold: 2/3rds of SF adults fully vaxxed; avg 16 new cases/d in SF, asymptomatic test + @UCSF now 0.16% (ie, 1/600). Plus too cold to eat outside.The economy will pick up speed as more and more people get vaccinated!

According to the CDC, on Vaccinations. Total administered: 285,720,586, as of yesterday 283,941,223. Day: 1.78 million. (U.S. Capacity is around 4 million per day)

1) 61.3% of the population over 18 has had at least one dose (70% is the goal by July 4th).

2) 130.0 million Americans are fully vaccinated (160 million goal by July 4th)

Note: I'll stop posting this daily once all four of these criteria are met:

1) 70% of the population over 18 has had at least one dose of vaccine, and

2) new cases are under 5,000 per day, and

3) hospitalizations are below 3,000, and

4) average daily deaths under 50 (currently 510 per day).

And check out COVID Act Now to see how each state is doing.

Almost 12,000 US deaths were reported so far in May due to COVID.

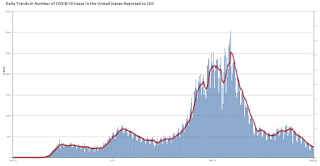

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

The 7-day average is 24,315, down from 25,315 yesterday, and down sharply from the recent peak of 69,881 on April 13, 2021. This is the lowest since June 15, 2020.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.

The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 23,917, down from 24,720 reported yesterday, but still above the post-summer surge low of 23,000.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 23,917, down from 24,720 reported yesterday, but still above the post-summer surge low of 23,000.

REALTORS® Confidence Index Survey April 2021

by Calculated Risk on 5/23/2021 10:41:00 AM

Some interesting information from the REALTORS® Confidence Index Survey April 2021

Several metrics indicates a very strong buyer market with short supply. The REALTORS® Buyer Traffic Index increased from 79 in March 2021 to 80 (very strong conditions) in April 2021 while the REALTORS® Seller Traffic Index remains below 50 which is “weak” traffic compared to the level one year ago. On average, a home sold had five offers. On average, REALTORS® expect home prices in the next three months to increase nearly 6% from one year ago and sales in the next three months to increase nearly 3% from last year’s sales level.

With little supply in the market, homes typically sold within 17 days (27 days one year ago), as buyer competition heats up.

The share of first-time buyers decreased to 31% (32% in the prior month, 36% one year ago).

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph, from the NAR report, shows buyer traffic is strong just about everywhere.

DOT: Vehicle Miles Driven Increased Sharply year-over-year in March

by Calculated Risk on 5/23/2021 08:09:00 AM

This will be something to watch as the economy recovers.

The Department of Transportation (DOT) reported:

Travel on all roads and streets changed by 19.0% (42.0 billion vehicle miles) for March 2021 as compared with March 2020. Travel for the month is estimated to be 263.0 billion vehicle miles.

The seasonally adjusted vehicle miles traveled for March 2021 is 261.1 billion miles, an 18.5% (40.7 billion vehicle miles) increase over March 2020. It also represents a 6.2% increase (15.2 billion vehicle miles) compared with February 2021.

Cumulative Travel for 2021 changed by -2.1% (-14.9 billion vehicle miles). The cumulative estimate for the year is 691.5 billion vehicle miles of travel.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows the monthly total vehicle miles driven, seasonally adjusted.

Miles driven declined sharply in March 2020, and really collapsed in April. After partially recovering fairly quickly, miles driven was mostly flat for 6+ months - but really picked up in March 2021.

Saturday, May 22, 2021

May 22nd COVID-19 New Cases, Hospitalizations, Vaccinations

by Calculated Risk on 5/22/2021 07:04:00 PM

The economic recovery depends on progress against the virus, so I'm tracking the progress.

KUDOS to all who are vaccinated! You are part of the solution and helping the economy. Thank you!

According to the CDC, on Vaccinations. Total administered: 283,941,223, as of yesterday 281,595,351. Day: 2.35 million. (U.S. Capacity is around 4 million per day)

1) 61.1% of the population over 18 has had at least one dose (70% is the goal by July 4th).

2) 129.0 million Americans are fully vaccinated (160 million goal by July 4th)

Note: I'll stop posting this daily once all four of these criteria are met:

1) 70% of the population over 18 has had at least one dose of vaccine, and

2) new cases are under 5,000 per day, and

3) hospitalizations are below 3,000, and

4) average daily deaths under 50 (currently 504 per day).

And check out COVID Act Now to see how each state is doing.

Almost 11,500 US deaths were reported so far in May due to COVID.

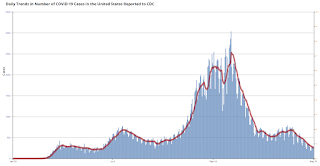

Click on graph for larger image.

Click on graph for larger image.

This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

Click on graph for larger image.

Click on graph for larger image.This graph shows the daily (columns) 7 day average (line) of positive tests reported.

This data is from the CDC.

The 7-day average is 25,315, down from 26,362 yesterday, and down sharply from the recent peak of 69,881 on April 13, 2021. This is the lowest since June 15, 2020.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.

The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 24,720, down from 25,313 reported yesterday, but still above the post-summer surge low of 23,000.

The second graph shows the number of people hospitalized.

This data is also from the CDC.

This data is also from the CDC.The CDC cautions that due to reporting delays, the area in grey will probably increase.

The current 7-day average is 24,720, down from 25,313 reported yesterday, but still above the post-summer surge low of 23,000.

Schedule for Week of May 23, 2021

by Calculated Risk on 5/22/2021 08:11:00 AM

The key reports this week are the second estimate of Q1 GDP, April New Home Sales, March Case-Shiller house prices, and Personal Income and Outlays for April.

For manufacturing, the May Richmond and Kansas City Fed manufacturing surveys will be released.

8:30 AM ET: Chicago Fed National Activity Index for April. This is a composite index of other data.

9:00 AM: S&P/Case-Shiller House Price Index for March.

9:00 AM: S&P/Case-Shiller House Price Index for March.This graph shows the year-over-year change in the seasonally adjusted National Index, Composite 10 and Composite 20 indexes through the most recent report (the Composite 20 was started in January 2000).

The consensus is for a 12.3% year-over-year increase in the Comp 20 index for March.

9:00 AM: FHFA House Price Index for March 2021. This was originally a GSE only repeat sales, however there is also an expanded index.

10:00 AM: New Home Sales for April from the Census Bureau.

10:00 AM: New Home Sales for April from the Census Bureau. This graph shows New Home Sales since 1963. The dashed line is the sales rate for last month.

The consensus is for 975 thousand SAAR, down from 1.021 million SAAR in March.

10:00 AM: Richmond Fed Survey of Manufacturing Activity for May.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for a decrease to 420 thousand from 444 thousand last week.

8:30 AM: Gross Domestic Product, 1st quarter 2021 (Second estimate). The consensus is that real GDP increased 6.5% annualized in Q1, up from the advance estimate of 6.4%.

8:30 AM: Durable Goods Orders for April from the Census Bureau. The consensus is for a 0.8% increase in durable goods orders.

10:00 AM: Pending Home Sales Index for April. The consensus is for a 1.2% increase in the index.

11:00 AM: the Kansas City Fed manufacturing survey for May.

8:30 AM ET: Personal Income and Outlays, April 2021. The consensus is for a 14.8% decrease in personal income, and for a 0.5% increase in personal spending. And for the Core PCE price index to increase 0.6%.

9:45 AM: Chicago Purchasing Managers Index for May.

10:00 AM: University of Michigan's Consumer sentiment index (Final for May). The consensus is for a reading of 83.0.

Friday, May 21, 2021

Homebuilder Comments in Mid-May: "Reducing Sales, Limiting Sales"

by Calculated Risk on 5/21/2021 02:31:00 PM

Some twitter comments from Rick Palacios Jr., Director of Research at John Burns Real Estate Consulting

Here's May mid-month home builder channel check I hinted at earlier. Builders are pushing prices w/little pushback, though some starting. Some builders are using price escalators & highest/best offer. Many limiting pre-sales, shifting to spec, & pricing home later in build cycle.

#Dallas builder: “Not selling build jobs in May, starting specs only, and not selling until drywall. Costs are too out of control for us to take the inflation risk on build jobs. So sales are way down.”

#SanAntonio builder: “Only selling specs at Sheetrock stage. Last month, it was frame stage.”

#Austin builder: “Stopped sales until we pour a foundation. Lumber too erratic to sell prior. I know others have gone to a bid process. I have heard all parties, including that people who win the bid, feel like they have lost.”

#LasVegas builder: “Reducing sales releases in attempt to moderate the impact of labor & material shortages. Homes are priced once a Truss delivery date is confirmed which triggers the lumber lock pricing. We are also considering online auctions, but appraisals are a concern.”

#Denver builder: “Limiting sales at all communities and gapping out on lots. Material availability is becoming more concerning.”

#Phoenix builder: “Metering sales. Could be higher if we released more, but construction can’t keep up & trades are raising costs post start of home, so we are delaying sales releases even further. Delaying release of to-be-built homes & selling only specs deeper in the cycle.”

#SaltLakeCity builder: “Very, very careful with home releases, generally 2 – 4 permits pulled for each subdivision each month. Those homes are not released for sale until the homes are 60-80 days into the construction schedule.”

#Charlotte builder: “No pre-sales as of now. Starting specs and will price at drywall. Sales are still strong but we are starting to see a little bit of a slowdown as we have pushed pricing considerably.”

#Nashville builder: “Prices are starting to flatten out. Sales are down by design as we are not offering presale contracts, & are not writing contracts on inventory homes until they have completed rough ins, with all remaining items confirmed as to availability."

#RaleighDurham builder: “Starting to see some reluctance/concern around home prices balance, to some extent, the buying frenzy that we have seen over the last few months. Continue to raise prices – we get material/labor cost increase notices EVERY SINGLE DAY!”

#Wilmington builder: “Presales are limited & have escalation clause. Not pricing specs until Sheetrock - then they are gone & we wait for next houses to get to drywall. Raising prices across all segments to keep up with cost until the market or appraisal stops us.”

#Atlanta builder: “Locking in costs with purchase orders at time of foundation. Cannot sell a home until foundations go in. Costs are crazy. We are hitting the top of the market in some places and can't push prices. We are seeing margin compression.”

#Birmingham builder: “We have presales turned off in about half our communities to burn through current backlog. We’re holding off sales and using escalation clauses.”

#Charleston builder: “Holding off on selling a home until framing, as that has been our most volatile cost from month to month. We aren't selling to-be-built homes in order to control costs and not commit to a sales price before some of our largest expenses are actualized.”

#Chicago builder: “Many builders are putting everything on hold or putting foundations in the ground and not going any further until they see where costs are headed. Trim, windows and doors supplier says they are starting to feel a slowdown and are preparing for a bigger one.”

#Indianapolis builder: “Not selling/pricing spec inventory until late in the construction process, to account for rising costs. We continue to raise prices on contract builds but have not added escalation clauses.”

#DC builder: “Capping sales by community with few exceptions. We cannot continue to sell further out to future. Limited sales at most communities and raised prices dramatically to keep pace with rising costs.”

#Philadelphia builder: “Holding off opening up some of the new sections until we can catch up to the sales backlog a bit.”

#Tampa builder: “We’re closed for the first half of May. Working on catching up to what we already have. We will significantly limit sales for the next several months.”

#Orlando builder: “Restricting releases to limit quantity of sales while production catches up. Increasing pricing every few sales.”

#Sarasota builder: “Everyone is starting construction on homes after permits are obtained and then quickly hitting unpredictable material shortages, masonry block as one primary example.”

#Jacksonville builder: “Revised all sales contracts, allowing us to adjust base price of home due to cost increases up until time slab is poured. Converting to spec sale program on single-family detached homes as new phases come online this summer.”

#LosAngeles builder: “Waiting to offer homes for sale until we have building permits in hand and can lock lumber pricing.”

#Riverside builder: “We sell out within a week of release. If sales volume drops it’s a result of no inventory. Banging prices each week. Scary high. Costs are stupid high. I’m not saying we’re out of buyers but sales team is telling me that their buyer list is getting smaller."

#SanJose builder: “Doing highest bidder approach at two communities. Seeing $100K over asking at one of them. Buying lumber sooner now, but may push out starting more units with the anticipation of lumber prices coming back down. Costs are eating up all price increases.”

#EastBayCA builder: “Holding back on releasing for sales until we have the phase contracted, so we know what our costs are going to be.”

#Reno builder: “We have gone to ‘Offer & Acceptance’ approach on sales releases where we are able to improve price and terms. This approach has been effective in maintaining our margins and keeping pace with all the increases we are getting." THE END

BLS: April Unemployment rates down in 12 States

by Calculated Risk on 5/21/2021 02:21:00 PM

From the BLS: Regional and State Employment and Unemployment Summary

Unemployment rates were lower in April in 12 states and the District of Columbia and stable in 38 states, the U.S. Bureau of Labor Statistics reported today. Forty-eight states and the District had jobless rate decreases from a year earlier and two states had little change. The national unemployment rate, 6.1 percent, was little changed over the month, but was 8.7 percentage points lower than in April 2020.Hawaii has been impacted by lower levels of tourism.

Nonfarm payroll employment increased in 9 states and the District of Columbia, decreased in 2 states, and was essentially unchanged in 39 states in April 2021. Over the year, nonfarm payroll employment increased in all states and the District.

...

Hawaii had the highest unemployment rate in April, 8.5 percent, followed by California, 8.3 percent, and New Mexico and New York, 8.2 percent each. Nebraska, New Hampshire, South Dakota, and Utah had the lowest rates, 2.8 percent each.

Q2 GDP Forecasts: Around 10%

by Calculated Risk on 5/21/2021 11:36:00 AM

From Merrill Lynch:

Our 2Q GDP tracking remains at 11% qoq saar. [May 21 estimate]From Goldman Sachs:

emphasis added

We left our Q2 GDP tracking estimate unchanged at +10.5% (qoq ar). [May 21 estimate]From the NY Fed Nowcasting Report

The New York Fed Staff Nowcast stands at 4.6% for 2021:Q2. [May 21 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2021 is 10.1 percent on May 18, down from 10.5 percent on May 14. [May 18 estimate]

Comments on April Existing Home Sales

by Calculated Risk on 5/21/2021 11:25:00 AM

Earlier: NAR: Existing-Home Sales Decreased to 5.85 million in April

A few key points:

1) This was the highest sales rate for April since 2006, and the 4th highest sales rate for April on record (behind 2004, 2005, and 2006). Some of the increase over the last ten months was probably related to record low mortgage rates, a move away from multi-family rentals, strong second home buying (to escape the high-density cities), a strong stock market and favorable demographics.

Also, the delay in the 2020 buying season pushed the seasonally adjusted number to very high levels over the winter. This means there are going to be some difficult comparisons in the second half of 2021!

2) Inventory is very low, and was down 20.5% year-over-year (YoY) in April. Also, as housing economist Tom Lawler has noted, the local MLS data shows even a larger decline in active inventory (the NAR appears to include some pending sales in inventory). Lawler noted:

"As I’ve noted before, the inventory measure in most publicly-released local realtor/MLS reports excludes listings with pending contracts, but that is not the case for many of the reports sent to the NAR (referred to as the “NAR Report!”), Since the middle of last Spring inventory measures excluding pending listings have fallen much more sharply than inventory measures including such listings, and this latter inventory measure understates the decline in the effective inventory of homes for sale over the last several months."

It seems likely that active inventory is down close to 50% year-over-year.

3) As usual, housing economist Tom Lawler's forecast was closer to the NAR report than the Consensus. The NAR reported 5.85 million SAAR, Lawler estimated the NAR would report 5.96 million SAAR, and the consensus was 6.09 million SAAR.

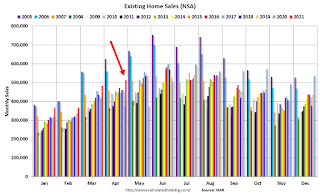

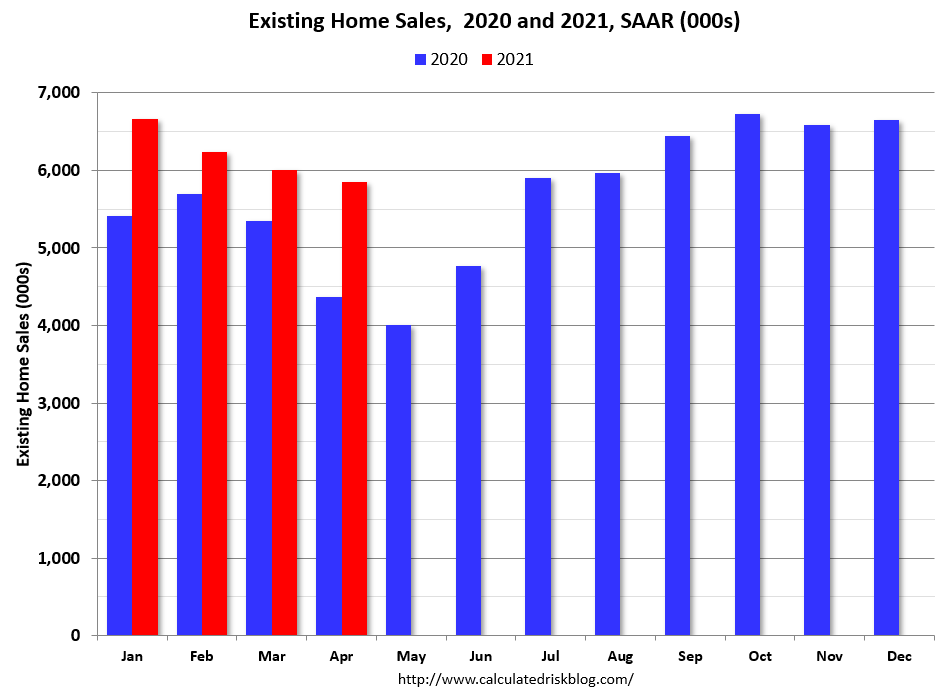

Click on graph for larger image.

Click on graph for larger image.

This graph shows existing home sales by month for 2020 and 2021.

The year-over-year comparisons will be easy in May and June, and then difficult in the second half of the year.

The second graph shows existing home sales for each month, Not Seasonally Adjusted (NSA), since 2005.

Sales NSA in April (513,000) were 37.5% above sales last year in April (373,000).

Sales NSA in April (513,000) were 37.5% above sales last year in April (373,000).

This was the highest sales for April (NSA) since 2006.

Click on graph for larger image.

Click on graph for larger image.This graph shows existing home sales by month for 2020 and 2021.

The year-over-year comparisons will be easy in May and June, and then difficult in the second half of the year.

The second graph shows existing home sales for each month, Not Seasonally Adjusted (NSA), since 2005.

Sales NSA in April (513,000) were 37.5% above sales last year in April (373,000).

Sales NSA in April (513,000) were 37.5% above sales last year in April (373,000).This was the highest sales for April (NSA) since 2006.