RSS Feed

RSS Feed by Calculated Risk on 2/17/2020 10:27:00 AM

Monday, February 17, 2020

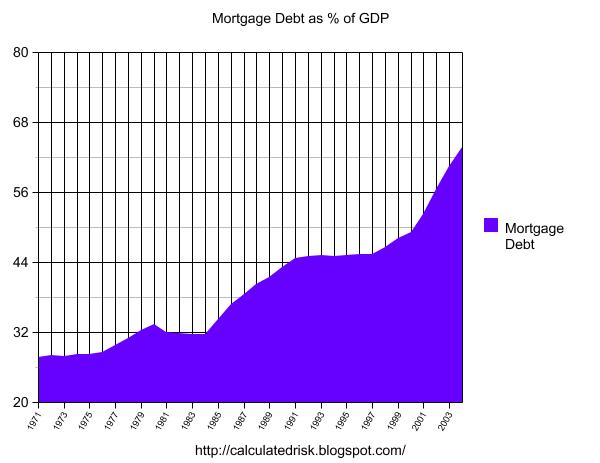

The Housing Bubble, Mortgage Debt as Percent of GDP

Three years ago, on Presidents' Day, I excerpted from a post I wrote in February 2005 (yes, 15 years ago).

In that 2005 post, I included a graph of household mortgage debt as a percent of GDP. Several readers asked if I could update the graph.

First, from 2005:

The following chart shows household mortgage debt as a % of GDP. Although mortgage debt has been increasing for years, the last four years have seen a tremendous increase in debt. Last year alone mortgage debt increased close to $800 Billion - almost 7% of GDP. ...CR Note: And a serious problem is what happened!

Many homeowners have refinanced their homes, in essence using their homes as an ATM.

It wouldn't take a RE bust to impact the general economy. Just a slowdown in both volume (to impact employment) and in prices (to slow down borrowing) might push the general economy into recession. An actual bust, especially with all of the extensive sub-prime lending, might cause a serious problem.

The second graph shows household mortgage debt as a percent of GDP through Q3 2019. Hopefully the graphs have improved!

The second graph shows household mortgage debt as a percent of GDP through Q3 2019. Hopefully the graphs have improved!The "bubble" is pretty obvious on this graph, and the sharp increase in mortgage debt was one of the warning signs.

Sunday, February 16, 2020

Fannie and Freddie: REO inventory declined in Q4, Down 17% Year-over-year

by Calculated Risk on 2/16/2020 11:57:00 AM

Fannie and Freddie earlier reported results last week for Q4 2019. Here is some information on Real Estate Owned (REOs).

Freddie Mac reported the number of REO declined to 4,989 at the end of Q4 2019 compared to 7,100 at the end of Q4 2018.

For Freddie, this is down 93% from the 74,897 peak number of REOs in Q3 2010.

Fannie Mae reported the number of REO declined to 17,501 at the end of Q4 2019 compared to 20,156 at the end of Q4 2018.

For Fannie, this is down 90% from the 166,787 peak number of REOs in Q3 2010.

Click on graph for larger image.

Click on graph for larger image.

Here is a graph of Fannie and Freddie Real Estate Owned (REO).

REO inventory decreased in Q4 2019, and combined inventory is down 17% year-over-year.

This is close to normal levels of REOs.

Saturday, February 15, 2020

Schedule for Week of February 16, 2020

by Calculated Risk on 2/15/2020 08:11:00 AM

The key reports this week are January Housing Starts and Existing Home sales.

For manufacturing, the February NY and Philly Fed manufacturing surveys will be released this week.

All US markets will be closed in observance of Washington's Birthday Holiday.

8:30 AM: The New York Fed Empire State manufacturing survey for February. The consensus is for a reading of 5.0, up from 4.8.

10:00 AM: The February NAHB homebuilder survey. The consensus is for a reading of 75, unchanged from 75. Any number above 50 indicates that more builders view sales conditions as good than poor.

7:00 AM ET: The Mortgage Bankers Association (MBA) will release the results for the mortgage purchase applications index.

8:30 AM: Housing Starts for January.

8:30 AM: Housing Starts for January. This graph shows single and total housing starts since 1968.

The consensus is for 1.415 million SAAR, down from 1.608 million SAAR.

8:30 AM ET: The Producer Price Index for December from the BLS. The consensus is for a 0.1% increase in PPI, and a 0.1% increase in core PPI.

During the day: The AIA's Architecture Billings Index for January (a leading indicator for commercial real estate).

2:00 PM: FOMC Minutes, Meeting of January 28-29, 2020

8:30 AM: The initial weekly unemployment claims report will be released. The consensus is for 210 thousand initial claims, up from 205 thousand the previous week.

8:30 AM: the Philly Fed manufacturing survey for February. The consensus is for a reading of 12.0, down from 17.0.

10:00 AM: Existing Home Sales for January from the National Association of Realtors (NAR). The consensus is for 5.45 million SAAR, down from 5.54 million.

10:00 AM: Existing Home Sales for January from the National Association of Realtors (NAR). The consensus is for 5.45 million SAAR, down from 5.54 million.The graph shows existing home sales from 1994 through the report last month.

Friday, February 14, 2020

Census: A Changing Nation: Population Projections Under Alternative Immigration Scenarios

by Calculated Risk on 2/14/2020 03:16:00 PM

Note: Housing economist Tom Lawler was been way ahead on this, see for example: Lawler: Updated “Demographic” Outlook Using Recent Population Estimates by Age, Lawler: “Off-Calendar” Census Population Projection Update Coming; To Include Alternative Migration Scenarios, Lawler: US Population Growth Slowed Again in 2019.

From the Census Bureau: A Changing Nation: Population Projections Under Alternative Immigration Scenarios

Higher international immigration over the next four decades would produce a faster growing, more diverse, and younger population for the United States. In contrast, an absence of migration into the country over this same period would result in a U.S. population that is smaller than the present. Different levels of immigration between now and 2060 could change the projection of the population in that year by as much as 127 million people, with estimates ranging anywhere from 320 to 447 million U.S. residents.

…

The 2017 National Projections main series, released in September 2018, present one scenario for the future population. These projections will only hold true if the assumptions about births, deaths, and migration match the actual trends in these components of population change. International migration is difficult to project because political and economic conditions are nearly impossible to anticipate, yet factor heavily into migration movements into and out of a country. While we do not attempt to predict future policy or economic cycles, we do recognize the uncertainty surrounding migration and the impact that different migration outcomes could have on the future population. To account for this, we have produced three alternate sets of projections that use the same methodology and assumptions for fertility, mortality, and emigration, but differ in the levels of immigration that they assume: high, low, and zero immigration. This report compares the results from the three alternative scenarios of projections and the main series, focusing on differences in the pace at which the U.S. population grows, diversifies, and ages.

Click on graph for larger image.

Click on graph for larger image.This graph is from the Census Bureau report.

Based on Lawler's recent analysis of births, deaths, and immigration, these projections are probably optimistic.

Depending on the which scenario happens, this could have a significant impact on the US economy and especially housing - and is a key reason the future is not as bright as it was a few years ago.

Sacramento Housing in January: Sales Up 5.6% YoY, Active Inventory down 32.7% YoY

by Calculated Risk on 2/14/2020 01:25:00 PM

From SacRealtor.org: January 2020 Statistics – Sacramento Housing Market – Single Family Homes

January ended with 944 sales, down 24.1% from December. Compared to one year ago (894), the current figure is up 5.6%.1) Overall sales increased to 944 in January, up from 894 in January 2019. Sales were down from December 2019 (previous month), and up 5.6% from January 2019.

...

The Active Listing Inventory increased 7.1% from December to January, from 1,315 units to 1,409 units. Compared with January 2019 (2,095), inventory is down 32.7%. The Months of Inventory increased from 1.1 to 1.5 Months. This figure represents the amount of time (in months) it would take for the current rate of sales to deplete the total active listing inventory.

...

The Median DOM (days on market) decreased from 19 to 17 and the Average DOM increased from 32 to 33. “Days on market” represents the days between the initial listing of the home as “active” and the day it goes “pending.”

emphasis added

2) Active inventory was at 1,409, down from 2,095 in January 2019. That is down 32.7% year-over-year. This is the ninth consecutive month with a YoY decline in inventory, following 20 months of YoY increases in inventory.

Q1 GDP Forecasts: 0.7% to 2.4%

by Calculated Risk on 2/14/2020 11:42:00 AM

From Merrill Lynch:

The data cut our 4Q 2019 GDP tracking estimate by 0.1pp to 2.0% and our 1Q 2020 estimate by 0.3pp to 0.7% qoq saar. [Feb 14 estimate]From the NY Fed Nowcasting Report

emphasis added

The New York Fed Staff Nowcast stands at 1.4% for 2020:Q1. News from this week’s data decreased the nowcast for 2020:Q1 by 0.3 percentage point. [Feb 14 estimate]And from the Altanta Fed: GDPNow

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2020 is 2.4 percent on February 14, down from 2.7 percent on February 7. [Feb 14 estimate]CR Note: These early estimates suggest real GDP growth will be between 0.7% and 2.4% annualized in Q1.

Industrial Production Decreased in January

by Calculated Risk on 2/14/2020 09:22:00 AM

From the Fed: Industrial Production and Capacity Utilization

Industrial production declined 0.3 percent in January, as unseasonably warm weather held down the output of utilities and as a major manufacturer significantly slowed production of civilian aircraft. The index for manufacturing edged down 0.1 percent in January; excluding the production of aircraft and parts, factory output advanced 0.3 percent. The index for mining rose 1.2 percent. At 109.2 percent of its 2012 average, total industrial production was 0.8 percent lower in January than it was a year earlier. Capacity utilization for the industrial sector fell 0.3 percentage point in January to 76.8 percent, a rate that is 3.0 percentage points below its long-run (1972–2019) average.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows Capacity Utilization. This series is up 10.1 percentage points from the record low set in June 2009 (the series starts in 1967).

Capacity utilization at 76.8% is 3.0% below the average from 1972 to 2017 and below the pre-recession level of 80.8% in December 2007.

Note: y-axis doesn't start at zero to better show the change.

The second graph shows industrial production since 1967.

The second graph shows industrial production since 1967.Industrial production decreased in December to 109.2. This is 25.4% above the recession low, and 3.7% above the pre-recession peak.

The change in industrial production was below consensus expectations.

Retail Sales increased 0.3% in January

by Calculated Risk on 2/14/2020 08:41:00 AM

On a monthly basis, retail sales increased 0.3 percent from December to January (seasonally adjusted), and sales were up 4.4 percent from January 2019.

From the Census Bureau report:

Advance estimates of U.S. retail and food services sales for January 2020, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $529.8 billion, an increase of 0.3 percent from the previous month, and 4.4 percent above January 2019. Total sales for the November 2019 through January 2020 period were up 4.4 percent from the same period a year ago. The November 2019 to December 2019 percent change was revised from up 0.3 percent to up 0.2 percent.

emphasis added

Click on graph for larger image.

Click on graph for larger image.This graph shows retail sales since 1992. This is monthly retail sales and food service, seasonally adjusted (total and ex-gasoline).

Retail sales ex-gasoline were up 0.3% in January.

The second graph shows the year-over-year change in retail sales and food service (ex-gasoline) since 1993.

Retail and Food service sales, ex-gasoline, increased by 3.9% on a YoY basis.

Retail and Food service sales, ex-gasoline, increased by 3.9% on a YoY basis.The increase in January was at expectations, however sales in November and December were revised down.

Thursday, February 13, 2020

Friday: Retail Sales, Industrial Production

by Calculated Risk on 2/13/2020 07:25:00 PM

Friday:

• At 8:30 AM ET, Retail sales for January is scheduled to be released. The consensus is for a 0.3% increase in retail sales.

• At 9:15 AM, The Fed will release Industrial Production and Capacity Utilization for January. The consensus is for a 0.2% decrease in Industrial Production, and for Capacity Utilization to decrease to 76.8%.

• At 10:00 AM, University of Michigan's Consumer sentiment index (Preliminary for February). The consensus is for a reading of 99.3.

Hotels: Occupancy Rate Decreases Year-over-year

by Calculated Risk on 2/13/2020 03:53:00 PM

From HotelNewsNow.com: STR: US hotel results for week ending 8 February

The U.S. hotel industry reported mixed year-over-year results in the three key performance metrics during the week of 2-8 February 2020, according to data from STR.The following graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

In comparison with the week of 3-9 February 2019, the industry recorded the following:

• Occupancy: -1.4% to 59.0%

• Average daily rate (ADR): +1.5% to US$128.75

• Revenue per available room (RevPAR): 0.0% at US$75.98

emphasis added

Click on graph for larger image.

Click on graph for larger image.The red line is for 2020, dash light blue is 2019, blue is the median, and black is for 2009 (the worst year probably since the Great Depression for hotels).

2020 is off to a solid start, however, STR notes that the new coronavirus could have a significant negative impact on hotels.